Market Overview: Expanding Demand for Plastic Drums, UN-Certified Barrels, and Circular Solutions

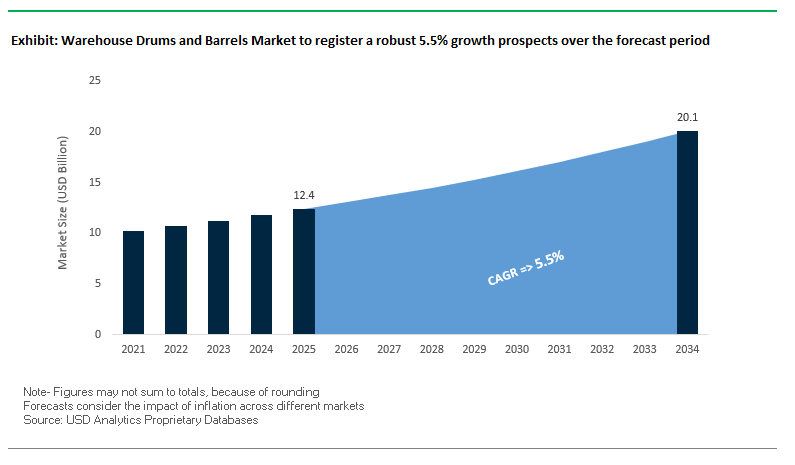

The global warehouse drums and barrels market is projected to grow from USD 12.4 billion in 2025 to USD 20.1 billion by 2034, registering a steady CAGR of 5.5%. This growth reflects the increasing demand from industries such as chemicals, petroleum, lubricants, pharmaceuticals, and food & beverages, where secure bulk storage and transport solutions are essential. For industry professionals and buyers, the critical questions revolve around how container manufacturers are balancing compliance, material innovation, and sustainability, while meeting rising global consumption needs.

Plastic drums, particularly HDPE-based designs, dominate the market thanks to their durability, lighter weight, and resistance to chemicals and moisture. UN certification for hazardous material transport remains a key design driver, ensuring regulatory compliance in critical applications. The petroleum sector is a leading consumer, heavily reliant on barrels and drums for secure storage and transport of refined fuels, lubricants, and chemicals. At the same time, the circular economy is reshaping strategies, with reconditioning and recycling services becoming a standard offering among top players.

Key Insights for Industry Professionals:

- Plastic drums lead the market: HDPE dominates due to durability, reusability, and chemical resistance.

- UN certification crucial: Regulatory compliance drives design and material choices.

- Petroleum industry dominance: A key consumer of industrial drums and barrels worldwide.

- Circular economy models: Reconditioning and recycling services expanding rapidly across regions.

Market Analysis: Recent Industry Developments Driving Transformation

The warehouse drums and barrels industry is experiencing a wave of consolidation, facility expansions, and sustainability-led innovation.

In August 2025, Ball Corporation sold a 41% stake in its Saudi joint venture to ORG Technology for USD 70 million, streamlining its packaging portfolio. A month earlier, in July 2025, Packaging Corporation of America (PCA) acquired Greif’s containerboard business for USD 1.8 billion, allowing Greif to sharpen its focus on polymer-based products, including drums and barrels. In June 2025, Mauser Packaging Solutions opened a new reconditioning facility in Tarragona, Spain, collaborating with BASF to optimize recycling and closed-loop solutions.

Regional expansion is also reshaping the industry. SCHÜTZ Container Systems launched production of PE-restricted plastic drums in Gujarat, India (April 2025) to meet growing Asian demand, while in August 2024, Mauser expanded in Africa by acquiring a South African plastic drums business. On the sustainability front, Greif introduced recyclable steel barrels in January 2025, targeting eco-friendly industrial storage, while Toray Plastics launched high-barrier PET films in October 2024, innovations that indirectly influence drum and barrel packaging for extended shelf life applications.

Trends and Opportunities Reshaping the Warehouse Drums and Barrels Market

Strategic Corporate Shift Towards Lightweight, High-Density Polyethylene (HDPE) Designs

The warehouse drums and barrels market is undergoing a strategic transformation as industries increasingly replace traditional steel drums with lightweight HDPE designs. This shift is driven by cost optimization, worker safety, and sustainability mandates. Unlike steel, HDPE drums offer superior corrosion resistance, making them well-suited for transporting acids, alkalis, and other hazardous chemicals without the risk of container degradation. A comparative industry analysis highlights that 55-gallon HDPE drums weigh considerably less than steel equivalents, reducing risks of back injuries and improving overall ergonomics in warehousing and logistics operations.

From a sustainability perspective, lightweight HDPE designs directly contribute to reduced carbon emissions by lowering overall shipping weight and fuel consumption. Many global chemical and lubricant producers are prioritizing these drums to align with corporate ESG goals while cutting logistics costs linked to rising fuel surcharges. The balance of durability, cost efficiency, and recyclability positions HDPE drums as a long-term replacement strategy for industries focused on both compliance and profitability.

Integration of IoT and Smart Tracking Technologies into Asset Management

The second major trend in the warehouse drums and barrels industry is the rapid integration of IoT-enabled sensors that transform passive containers into active data carriers. Moving beyond barcodes, reusable drums and steel barrels are now being fitted with GPS, RFID, and condition-monitoring sensors that provide real-time insights into location, environmental exposure, and usage. A case study in automated inventory management showed that these technologies reduce human error, optimize storage space, and streamline order fulfillment by offering real-time visibility into assets.

This innovation goes beyond logistics tracking. Smart drums enable proactive condition monitoring by detecting deviations in temperature, humidity, or shock exposure that could compromise sensitive goods such as pharmaceuticals or specialty chemicals. The data-driven insights generated allow operators to optimize inventory levels, forecast demand, and ensure regulatory compliance in industries with strict safety standards. By embedding IoT into drums and barrels, the industry is moving toward fully digitized supply chain ecosystems, where packaging plays an integral role in predictive maintenance and quality assurance.

Development and Scaling of Advanced Recycled Resin Formulations

A key growth opportunity lies in scaling recycled resin formulations for HDPE and polypropylene (PP) drums. With circular economy mandates from large end-users and regulatory bodies, there is a strong market pull for post-consumer recycled (PCR) content in industrial packaging. Research conducted by the Plastic Drum Institute confirmed that drums containing up to 100% PCR content can still pass rigorous UN drop and stack performance tests, demonstrating that recycled-content solutions can achieve both safety and durability benchmarks.

As Extended Producer Responsibility (EPR) regulations expand, demand for UN-certified recycled-content drums will grow significantly. Resin producers and drum manufacturers are uniquely positioned to capitalize on this opportunity by developing formulations that retain chemical resistance, structural strength, and regulatory compliance. Furthermore, by aligning with global sustainability strategies, producers can offer industrial customers a dual benefit of environmental stewardship and compliance cost reduction.

Expansion of Drum Reconditioning and ‘Drum-as-a-Service’ Rental Models

The second major opportunity is the rapid scaling of reconditioning services and rental-based business models. Rising raw material costs, stricter waste management regulations, and sustainability imperatives are fueling demand for certified reconditioned drums. According to the Reusable Industrial Packaging Association (RIPA), nearly 5.5 million 55-gallon plastic drums are reconditioned annually in the U.S., highlighting the significant scale of this circular model.

The emergence of “drum-as-a-service” models further strengthens this trend by shifting packaging from a one-time purchase to a service-based lifecycle solution. Providers manage logistics, collection, cleaning, and reconditioning while offering customers traceability and compliance assurance. This approach delivers substantial cost savings, reduced waste, and simplified logistics for industries with closed-loop supply chains, including chemicals, lubricants, and food processing. With sustainability at the forefront, the expansion of service-based and reuse-driven models positions reconditioning as a critical growth pillar for the global warehouse drums and barrels market.

Trends and Opportunities Reshaping the Warehouse Drums and Barrels Market

Strategic Corporate Shift Towards Lightweight, High-Density Polyethylene (HDPE) Designs

The warehouse drums and barrels market is shifting rapidly toward lightweight HDPE designs as companies seek to reduce logistics costs, meet sustainability targets, and improve worker safety. Traditional steel drums, while durable, present challenges in terms of weight, corrosion risk, and recyclability. By contrast, HDPE drums provide superior chemical resistance, protecting against acids, alkalis, and corrosive substances without degradation. A 55-gallon HDPE drum weighs significantly less than a steel drum, helping to lower workplace injury risks while simultaneously reducing freight weight and associated fuel surcharges.

For global chemical and lubricant producers, the carbon efficiency of lightweight packaging has become a key driver. Lower fuel consumption during transport translates into measurable reductions in Scope 3 emissions, aligning with corporate ESG targets. The shift from steel to HDPE is no longer a marginal change but a structural transition in packaging procurement strategies. This makes lightweight HDPE drums an integral component of cost-optimized and environmentally responsible logistics.

Integration of IoT and Smart Tracking Technologies into Asset Management

Another transformational trend is the integration of IoT into warehouse drums and barrels, turning passive containers into intelligent data assets. Embedded sensors are now tracking location, temperature, humidity, and shock in real time, allowing companies to mitigate risks for sensitive goods such as pharmaceuticals, chemicals, and food ingredients. Beyond traceability, these connected systems deliver predictive maintenance and condition monitoring, enabling operators to act before spoilage, leaks, or structural failures occur.

A study on autonomous inventory management found that IoT-enabled drums reduce errors, optimize warehouse space, and accelerate order fulfillment by providing real-time inventory data. The collected insights support data-driven decision-making, enabling more precise demand forecasting, asset utilization, and regulatory compliance reporting. This integration of IoT creates a new layer of value in the warehouse drums and barrels sector, where packaging itself becomes an active node in the digital supply chain.

Development and Scaling of Advanced Recycled Resin Formulations

The transition toward a circular economy is creating a robust opportunity for manufacturers to scale PCR-based resin formulations for drums. Research by the Plastic Drum Institute confirms that HDPE drums incorporating up to 100% post-consumer recycled content can meet UN drop and stack test standards, proving their safety and reliability for hazardous goods. This finding validates PCR integration as a viable path for scaling sustainable drum production.

With Extended Producer Responsibility (EPR) frameworks expanding worldwide, companies face rising pressure to demonstrate recycled content use. By developing high-performance PCR and PP resin blends, drum producers can address both compliance obligations and end-user sustainability targets. Maintaining chemical resistance and structural durability while meeting UN certification requirements will differentiate manufacturers in a market increasingly driven by regulatory scrutiny and customer sustainability mandates.

Expansion of Drum Reconditioning and ‘Drum-as-a-Service’ Rental Models

The reconditioning and reuse segment represents one of the fastest-growing opportunities in the warehouse drums and barrels market. Rising input costs and sustainability mandates are encouraging industries to adopt reconditioned containers as a cost-effective and eco-friendly alternative. According to the Reusable Industrial Packaging Association (RIPA), more than 5.5 million 55-gallon plastic drums are reconditioned annually in the U.S., underscoring the scale and acceptance of this model.

The “drum-as-a-service” concept extends this model further by offering lifecycle management as a subscription service. Under this framework, providers handle delivery, collection, cleaning, reconditioning, and compliance certifications, allowing customers to outsource non-core packaging operations. This model not only reduces upfront costs but also aligns with circular supply chain practices, delivering both environmental benefits and operational efficiencies. As companies adopt closed-loop logistics, reconditioning and rental services are poised to become a central pillar of competitive strategy in the industrial packaging sector.

Competitive Landscape: Key Companies in the Warehouse Drums and Barrels Market

The competitive landscape of the global warehouse drums and barrels market is shaped by global leaders expanding their recycling capabilities, innovative drum designs, and pooling logistics models. Companies are pursuing strategies that combine compliance with sustainability, while expanding their footprint across developed and emerging regions.

Mauser Packaging Solutions: Expanding Global Reconditioning and Recycling Capabilities

Mauser Packaging Solutions is a leader in industrial packaging, offering plastic drums, IBCs, metal and fiber packaging, and full lifecycle reconditioning services. In June 2025, it launched a reconditioning facility at BASF’s Spain site, and in August 2024, it acquired a South African drums business. With innovations such as the Infinity Series incorporating PCR content, Mauser underscores its commitment to sustainability. Its ability to offer end-to-end packaging lifecycle services positions it as a frontrunner in circular economy solutions.

Greif, Inc.: Strengthening Polymer-Based Industrial Packaging

Greif is a global industrial packaging provider with expertise in steel, plastic, and fiber drums. Its July 2025 divestment of containerboard to PCA reflects a strategy to prioritize polymer packaging and higher-growth segments. Greif’s reputation for durable UN-rated drums makes it a trusted supplier for chemicals, oil & gas, food, and pharma sectors. Its global presence across 35+ countries ensures resilience in supply and compliance with hazardous goods regulations.

SCHÜTZ GmbH & Co. KGaA: Expanding UN-Certified Drums Across Asia

SCHÜTZ is a global industrial packaging producer, known for its ECOBULK and RECOBULK IBCs and drum product lines. In April 2025, it opened a new facility in India to manufacture PE-restricted drums, reinforcing its commitment to the Asian market. With 55+ global production sites, SCHÜTZ supports a wide client base while promoting circularity through its RECONTAINER program, which collects and reconditions used drums and IBCs worldwide.

Brambles Ltd. (CHEP): Redefining Industrial Logistics Through Pooling

Brambles, operating under the CHEP brand, provides a share-and-reuse logistics model with pallets, crates, and containers that compete with one-way drum and barrel systems. Its Zero Waste World (ZWW) program reduces waste and transport inefficiencies, while its BXB Digital technology provides supply chain visibility. Recognized with double A-grades for forests and climate change in 2024, Brambles leverages sustainability as a core differentiator in industrial packaging logistics.

Schoeller Allibert: Leading in Returnable Plastic Packaging Solutions

Schoeller Allibert specializes in returnable transport packaging (RTP), including UN-certified plastic drums, pails, and rigid bulk containers. With product lines such as MaxiFlow® and AgriLog®, it delivers automation-friendly, reusable packaging that reduces logistics emissions. The company focuses on designing durable, reconditionable products to enable circular economy adoption for clients across agriculture, chemicals, and food industries.

Warehouse Drums and Barrels Market Share Insights

Chemicals & Solvents Dominate Warehouse Drums and Barrels Market Share by Application

Chemicals & solvents account for the largest share of the warehouse drums and barrels market in 2025, capturing 35% of demand, underscoring the sector’s reliance on robust, compliant bulk packaging solutions. Drums remain the gold standard for transporting hazardous and corrosive chemicals due to their leak-proof seals, chemical resistance, and ability to meet UN/DOT international safety standards. Reconditioning and reusability practices further reinforce their dominance, aligning with industry sustainability goals while lowering long-term costs. Petroleum & lubricants, paints, inks, and dyes contribute significant shares by requiring tight-head and open-head drums for liquid integrity and viscosity handling, while food & beverages and pharmaceuticals demand food-grade and GMP-compliant formats for purity and traceability. However, the overwhelming scale and diversity of global chemical production—from solvents and resins to acids and specialty chemicals position this segment as the undisputed growth engine, making warehouse drums and barrels indispensable for industrial and hazardous material logistics.

Tight-Head Drums Lead Warehouse Drums and Barrels Market Share by Product Type

Tight-head drums represent 40% of the global warehouse drums and barrels market in 2025, making them the leading product type, driven by their unmatched seal integrity for transporting and storing hazardous and volatile liquids. With permanently sealed tops and dual bung openings, they are the default solution for high-value chemicals, solvents, and petroleum products where leakage prevention, evaporation control, and contamination avoidance are mission-critical. Open-head drums continue to serve as versatile workhorses for solids, viscous pastes, and paints, while intermediate bulk containers (IBCs) are rapidly gaining share due to their cubic efficiency and ability to replace multiple drums in large-volume logistics. Barrels, particularly wooden ones, retain value in niche areas such as wine and whiskey maturation, where packaging is intrinsic to product identity. The overall leadership of tight-head drums reflects a strong industry emphasis on compliance, safety, and risk management, securing their role as the most trusted format in hazardous liquid transportation.

United States: Sustainability, Smart Technologies, and Industry-Specific Innovations Driving Warehouse Drums and Barrels Market

The United States warehouse drums and barrels market is experiencing steady growth due to strong demand from petroleum, chemical, and pharmaceutical industries that require compliant and secure packaging for hazardous and non-hazardous materials. As supply chains expand, the industry is prioritizing durable, regulatory-compliant packaging solutions to ensure safety and efficiency in storage and transportation. A notable trend in the U.S. is the strong focus on sustainability and reusability, as seen with Greif, Inc.’s expanded stake in Centurion Container LLC, boosting its footprint in intermediate bulk container (IBC) reconditioning and reusable packaging solutions.

Innovation is a defining feature of the U.S. market. Companies like Encore Container are introducing products such as 77-gallon plastic drums, diversifying their product portfolios to cater to industry-specific needs. The integration of smart technologies for real-time tracking and monitoring of drum shipments is another key development, enhancing supply chain visibility and improving security. Together, these factors highlight how the U.S. is shaping the future of industrial packaging through sustainable practices, product diversification, and digital transformation.

Germany: Regulatory Compliance and Circular Economy Fueling Demand for Sustainable Drums and Barrels

Germany’s warehouse drums and barrels market is characterized by a stringent regulatory framework, particularly the EU Packaging and Packaging Waste Regulation (PPWR), which mandates eco-friendly and recyclable packaging materials. This regulatory push has positioned Germany as a leader in sustainable packaging innovation, with manufacturers and end-users collaborating to design drums and barrels that meet national and EU recyclability targets.

In line with its commitment to a circular economy, Germany is promoting packaging with high recycled content and durability. At the same time, the country is at the forefront of green logistics adoption, with warehouses and logistics hubs integrating renewable energy, rainwater harvesting, and low-carbon materials. This shift is directly influencing the demand for sustainable drums and barrels that align with eco-design principles. The combination of strict compliance, innovation, and green infrastructure makes Germany a benchmark market for sustainability-driven industrial packaging.

China: Industrial Expansion and Green Transformation Reshaping Warehouse Drums and Barrels Market

China’s warehouse drums and barrels industry is thriving on the back of its massive industrial expansion, particularly in chemicals, food, and construction, which require reliable and durable packaging solutions. The country’s status as a global manufacturing hub ensures consistently high demand for industrial packaging, making it one of the largest and fastest-growing markets worldwide. Strategic investments, such as Mauser Packaging Solutions’ new manufacturing facility near Shanghai, underscore the industry’s rapid growth and ability to meet the rising demand for industrial packaging.

Simultaneously, China’s “dual carbon” goals are driving industries toward sustainable practices, including recyclable and reusable packaging for logistics and warehousing. The green transformation of the express delivery and logistics industries is compelling companies to prioritize eco-friendly packaging solutions that reduce environmental impact. As a result, the Chinese market stands at the intersection of large-scale industrial growth and government-backed sustainability reforms, shaping the evolution of global packaging standards.

India: Manufacturing Expansion and Policy Support Accelerating Growth in Drums and Barrels Market

India’s warehouse drums and barrels market is expanding rapidly, supported by government-led initiatives such as “Make in India” and “Zero Effect Zero Defect,” which encourage quality domestic production and investment in industrial infrastructure. A key example is Balmer Lawrie & Co. Ltd., under the Ministry of Petroleum & Natural Gas, which has launched a new industrial packaging plant in Vadodara to manufacture steel drums, showcasing how public-sector initiatives are fueling industrial packaging growth.

The Indian market is also shaped by strong regulatory and sustainability pressures. The Plastic Waste Management (Amendment) Rules are phasing out single-use plastic, creating demand for biodegradable and reusable packaging alternatives. Furthermore, the adoption of technology and automation is redefining warehouse operations, with the use of drones, digitalization, and dark warehouses improving logistics efficiency. These advancements influence the design and handling requirements of drums and barrels, positioning India as a rapidly modernizing and sustainability-conscious market.

Brazil: Circular Economy Policies and Technological Modernization Driving Industrial Packaging Growth

The Brazilian warehouse drums and barrels market is undergoing transformation, largely due to the National Solid Waste Policy, which promotes a circular economy and restricts the use of single-use plastics. This legislative framework has accelerated the shift toward durable and reusable packaging solutions, making Brazil a key market for sustainable industrial packaging in Latin America.

Technological advancements are further shaping the industry, with robotics and artificial intelligence (AI) being widely integrated to improve production accuracy, automated sorting, and defect detection. At the same time, the Brazilian warehousing and logistics sector is attracting significant global and domestic investments, particularly in industrial hubs. This influx of capital is fueling demand for high-quality, reliable drums and barrels to support advanced manufacturing and logistics operations.

United Kingdom: E-Commerce Expansion and Strategic Acquisitions Reshaping Drums and Barrels Industry

The United Kingdom warehouse drums and barrels market is seeing new growth opportunities with the expansion of Chinese e-commerce and logistics companies, such as JD.com, which are securing significant warehouse spaces across the country. This surge in warehousing activities is generating substantial demand for durable and compliant industrial packaging solutions, including drums and barrels.

Sustainability is a central focus in the U.K. market, with companies like Encore Container expanding their portfolios to include environmentally friendly alternatives. Additionally, strategic acquisitions are reshaping the competitive landscape—such as Schütz GmbH & Co. KgaA’s acquisition of GEM Plastics Limited, enabling it to significantly expand its product portfolio for the U.K., Ireland, and neighboring markets. This combination of e-commerce-driven demand, sustainable packaging solutions, and strategic consolidation positions the U.K. market as a dynamic hub for industrial packaging innovation.

Warehouse Drums and Barrels Market Report Scope

Warehouse Drums and Barrels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.4 Billion

|

|

Market Size (2034)

|

$20.1 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material (Steel, Plastic, Fiber), By Application (Chemicals & Solvents, Petroleum & Lubricants, Food & Beverages, Pharmaceuticals & Healthcare, Paints Inks & Dyes, Construction & Building, Other Applications), By Product Type (Open-Head Drums, Tight-Head Drums, IBCs, Barrels, Other Products)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Mauser Packaging Solutions, Sonoco Products Company, Industrial Container Services, Schütz GmbH & Co. KgaA, Nippon Steel Drums Co., Ltd., Snyder Industries, LLC, Skolnik Industries, Inc., Rieke Packaging Systems, Balmer Lawrie & Co. Ltd., Encore Container, East India Drums & Barrels Mfg. Ltd., BWAY Corp., Colep Packaging, Tinplate Company of India (TCIL)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Warehouse Drums and Barrels Market Segmentation

By Material

By Application

- Chemicals & Solvents

- Petroleum & Lubricants

- Food & Beverages

- Pharmaceuticals & Healthcare

- Paints Inks & Dyes

- Construction & Building

- Other Applications

By Product Type

- Open-Head Drums

- Tight-Head Drums

- IBCs

- Barrels

- Other Products

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Warehouse Drums and Barrels Market

- Greif, Inc.

- Mauser Packaging Solutions

- Sonoco Products Company

- Industrial Container Services

- Schütz GmbH & Co. KgaA

- Nippon Steel Drums Co., Ltd.

- Snyder Industries, LLC

- Skolnik Industries, Inc.

- Rieke Packaging Systems

- Balmer Lawrie & Co. Ltd.

- Encore Container

- East India Drums & Barrels Mfg. Ltd.

- BWAY Corp.

- Colep Packaging

- Tinplate Company of India (TCIL)

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the evolving dynamics of the global warehouse drums and barrels market, emphasizing breakthroughs in lightweight HDPE designs, smart tracking IoT integration, recycled resin formulations, and circular economy-based reconditioning services. The analysis reviews historical performance from 2021 to 2024, evaluates current industry developments, and forecasts market trajectories through 2034, highlighting strategic shifts in materials, regulatory compliance, and sustainable packaging. This report provides a comprehensive examination of market drivers, challenges, competitive strategies, and regional growth patterns, making it an essential resource for packaging manufacturers, logistics managers, sustainability officers, and investors seeking actionable insights. USDAnalytics highlights key trends including the replacement of steel with plastic drums for cost efficiency and safety, adoption of IoT-enabled containers for predictive supply chain management, and scaling of circular models such as drum-as-a-service rentals. Industry professionals will find in-depth analysis of emerging opportunities, global regulatory influences, and competitive strategies critical for informed decision-making and long-term investment planning.

Scope Highlights:

- Segmentation: By Material (Steel, Plastic, Fiber), By Application (Chemicals & Solvents, Petroleum & Lubricants, Food & Beverages, Pharmaceuticals & Healthcare, Paints Inks & Dyes, Construction & Building, Other Applications), By Product Type (Open-Head Drums, Tight-Head Drums, IBCs, Barrels, Other Products)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Temporal Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: Profiles and strategic analysis of 15+ leading players including Greif, Mauser Packaging Solutions, Schütz GmbH & Co. KGaA, Balmer Lawrie & Co. Ltd., Encore Container, and others.

Methodology

The research methodology for this report is based on a robust combination of primary and secondary data sources to ensure accuracy and industry relevance. USDAnalytics leveraged interviews with industry executives, surveys of logistics and manufacturing stakeholders, and data from regulatory authorities to understand trends, product innovations, and market adoption patterns. Secondary sources, including corporate reports, trade publications, patent filings, and financial statements, were analyzed to triangulate insights and validate market assumptions. Quantitative modeling techniques were applied to estimate historical market sizes, project growth rates, and evaluate segment-wise performance, while scenario analysis provided foresight into future regulatory and sustainability impacts. The methodology emphasizes a balance between qualitative insights—such as emerging business models and corporate strategies—and quantitative data for a holistic market understanding, ensuring the report serves as a strategic guide for industry professionals navigating competitive, regulatory, and technological landscapes.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.