Water-Based Enamel Market Size, Growth Trajectory, and Sustainability-Driven Transformation

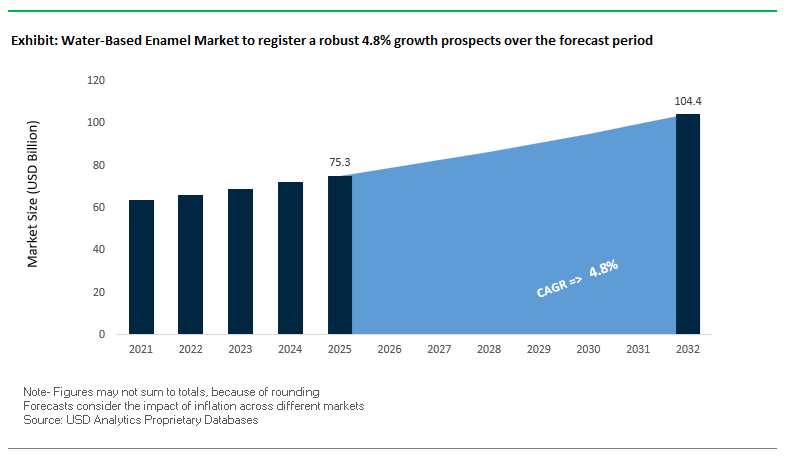

The global Water-Based Enamel Market reached a valuation of $75.3 billion in 2025, reflecting the accelerating shift toward environmentally compliant coating technologies across architectural, industrial, and automotive applications. The market is projected to expand at a CAGR of 4.8% from 2025 to 2032, reaching $104.5 billion by 2032, driven by tightening VOC regulations, rising green building certifications, and rapid innovation in waterborne resin chemistry.

Water-based enamels are increasingly displacing solvent-based coatings due to their low VOC emissions, reduced odor profiles, faster drying times, and improved environmental safety compliance. This transition is particularly evident in residential construction, commercial infrastructure, and automotive refinishing sectors, where regulatory mandates and consumer awareness are converging to reshape procurement strategies. The integration of advanced acrylic and polyurethane dispersions is further enhancing performance characteristics such as gloss retention, durability, corrosion resistance, and adhesion to diverse substrates.

A notable structural shift within the market is the alignment of product innovation with sustainability frameworks, including LEED certification requirements and global decarbonization goals. Manufacturers are actively investing in bio-based additives, antimicrobial coatings, and energy-efficient application technologies, positioning water-based enamel as a cornerstone of next-generation coating solutions. Additionally, the growing penetration of electric vehicles (EVs), smart infrastructure, and high-performance architectural coatings is amplifying demand for specialized waterborne enamel systems with enhanced UV stability, thermal resistance, and anti-fungal properties.

From a geographic standpoint, Asia-Pacific remains a dominant consumption hub due to rapid urbanization and infrastructure development, while North America and Europe are leading in technology innovation and regulatory-driven adoption. Overall, the market is transitioning from commoditized coatings toward high-performance, application-specific, and sustainability-oriented enamel solutions, establishing a strong foundation for long-term growth.

Market Analysis: Strategic Consolidation, Product Innovation, and Regulatory Alignment Reshaping Market Dynamics

The Water-Based Enamel Market is undergoing a phase of intense strategic consolidation and technological advancement, as leading coatings manufacturers accelerate efforts to strengthen portfolios and global footprint. A pivotal development is the March 2026 progression of the AkzoNobel–Axalta merger, which consolidates their complementary strengths across decorative and automotive refinish segments. This $17 billion combined entity is expected to create a unified innovation ecosystem with centralized R&D hubs in Amsterdam and Philadelphia, enabling accelerated development of advanced waterborne enamel technologies tailored for both industrial and consumer applications.

Product innovation remains a primary competitive lever. In March 2026, PPG Industries launched AQUACRON™ WSP, a next-generation waterborne spray enamel engineered to reduce application time by 20% by eliminating the need for primers across multiple substrates while meeting stringent 2026 VOC regulations. Similarly, Benjamin Moore’s January 2026 launch of Eco Spec® low-odor enamel underscores the growing demand for indoor air quality-compliant coatings, particularly in sensitive environments such as healthcare facilities and educational institutions. These developments reflect a broader industry trend toward high-efficiency, user-friendly, and health-conscious coating systems.

Regional expansion and supply chain optimization are also shaping market dynamics. In February 2026, Kansai Nerolac’s amalgamation with Nerofix enhanced its integrated coatings and construction chemical capabilities across South Asia, strengthening distribution efficiency for water-based enamel products. Meanwhile, Jotun’s R&D expansion and localization strategy in Africa, supported by new manufacturing facilities in Ethiopia and Algeria, signals increasing focus on emerging markets with region-specific performance requirements.

Earlier innovations in late 2025 further reinforce the market’s technological trajectory. Asian Paints introduced its Neo-Finish series, delivering solvent-like gloss with anti-fungal and heat-reflective features for humid climates, while Axalta’s Solar Boost UV-stable enamel technology targets premium EV coatings with enhanced color durability. Additionally, PPG’s expansion of its Velocity waterborne refinish system—integrated with automated mixing platforms—demonstrates a shift toward digitalization and process efficiency in coating applications, reducing material waste by up to 15%. Concurrently, Nippon Paint scaled its antimicrobial Health-Guard series, addressing post-pandemic demand for hygienic surfaces resistant to harsh disinfectants.

Market Trend: EPA Design for the Environment Certification Driving Low-VOC and PFAS-Free Water-Based Enamel Adoption

The expansion of the U.S. Environmental Protection Agency Design for the Environment certification in 2026 is significantly influencing the water-based enamel market, particularly in architectural coatings and industrial enamel applications. This certification is increasingly acting as a mandatory procurement filter for federal and state-level projects, accelerating the shift toward environmentally compliant waterborne enamel coatings.

DfE-certified water-based enamels are required to maintain VOC levels at or below 50 g/L, with advanced 2026 formulations achieving ultra-low VOC levels below 5 g/L. This performance is critical for projects targeting LEED v4.1 indoor air quality credits, driving demand for low-VOC enamel coatings in green building construction and sustainable infrastructure development.

Biodegradability requirements under OECD 301B standards mandate that surfactants and coalescing agents achieve over 60% degradation within 28 days, ensuring minimal environmental persistence. This is pushing manufacturers toward eco-friendly coating additives and water-based resin systems that reduce environmental impact during application.

Additionally, DfE certification enforces strict chemical safety standards, requiring zero intentionally added PFAS and alkylphenol ethoxylates. This has triggered a widespread transition toward bio-based rheology modifiers derived from renewable sources such as castor oil and tall oil fatty acids, strengthening the positioning of water-based enamel coatings within the sustainable coatings market.

Market Trend: China GB/T 41658-2025 Standard Elevating Durability and Aesthetic Performance in Asia-Pacific Markets

The implementation of China’s GB/T 41658-2025 standard in early 2026 is raising the baseline quality standards for water-based enamel coatings across the Asia-Pacific region. This regulation specifically addresses performance failures in humid climates, reinforcing the demand for durable and weather-resistant waterborne enamel formulations.

A key requirement under the updated standard is enhanced scrub resistance, with Grade A water-based enamels required to withstand a minimum of 2,000 scrub cycles as per ISO 11998. This represents a 25% increase over previous standards, driving innovation in high-durability enamel coatings for residential and commercial applications.

The regulation also introduces strict anti-yellowing benchmarks, requiring a Delta b value below 1.5 after 500 hours of UV exposure. This is encouraging the adoption of high-purity acrylic-urethane hybrid systems over conventional water-based alkyd enamels, improving long-term color retention and aesthetic performance in light-colored coatings. These advancements are strengthening the demand for UV-resistant enamel coatings and high-performance architectural finishes in rapidly urbanizing markets.

Market Opportunity: Ultra-High-Gloss Water-Based Enamels Bridging Performance Gap with Solvent-Based Coatings

Technological advancements in nano-particle emulsions are enabling ultra-high-gloss water-based enamel coatings, effectively closing the performance gap with traditional solvent-borne alkyd systems. Premium 2026 waterborne enamel formulations are achieving gloss levels of 90 Gloss Units or higher at a 60° angle, delivering superior visual appeal and surface reflectivity for high-end architectural and industrial applications.

These coatings also demonstrate a 20% improvement in distinctness of image compared to earlier benchmarks, enhancing surface clarity and finish quality. The ability to achieve high-gloss enamel finishes using low-VOC formulations is a significant driver in the premium coatings segment.

A key advantage of these advanced water-based enamels is their non-yellowing performance, maintaining color stability for over 10 years even in low-light environments. This makes them particularly suitable for white trims, decorative surfaces, and high-visibility industrial safety equipment.

In addition to aesthetic benefits, these coatings offer enhanced surface durability through self-crosslinking technology, achieving pencil hardness ratings of 2H to 3H within seven days. This level of scratch resistance is critical for high-traffic applications such as commercial furniture, railings, and interior fixtures, positioning ultra-high-gloss waterborne enamels as a high-value segment in the global coatings market.

Market Opportunity: Rapid-Dry Water-Based Enamels Enhancing Industrial Maintenance Efficiency and Productivity

The demand for rapid-curing coatings in the industrial maintenance sector is creating strong growth opportunities for fast-drying water-based enamel formulations. The primary value driver in 2026 is reduced return-to-service time, enabling faster project completion and improved operational efficiency in maintenance environments.

Next-generation rapid-dry waterborne enamels achieve a dust-free state in less than 10 minutes at standard ambient conditions of 25°C, significantly minimizing the risk of surface contamination during application. These coatings reach touch-dry status within 15 to 30 minutes and achieve a hard-dry state in under one hour, enabling same-day double coating. This reduces total project labor time by approximately 35%, offering significant cost savings for industrial users.

Despite the accelerated drying profile, these coatings maintain high adhesion performance, achieving a 5B rating in ASTM D3359 cross-hatch adhesion tests on properly prepared metal and wood substrates. This ensures long-term durability and bond integrity without compromising performance for speed.

The combination of rapid curing, strong adhesion, and low-VOC compliance is positioning water-based enamel coatings as a preferred solution in industrial maintenance coatings, infrastructure repair projects, and commercial refurbishment applications.

Water-Based Enamel Market Share and Segmentation Insights

Acrylic Enamel Leads with 46.4% Share Due to Fast Drying and Superior Color Stability

The acrylic enamel segment dominates the water-based enamel market with a 46.4% market share in 2025, driven by its fast drying time, excellent color retention, and compliance with environmental regulations. In the architectural coatings and decorative paints market, acrylic enamels are widely used for interior trim, doors, cabinets, and furniture applications, where durability and finish quality are critical. These coatings typically dry to touch within 30–60 minutes, significantly improving project turnaround times for both DIY users and professional painters. Additionally, acrylic enamels offer superior resistance to yellowing and long-term gloss retention, outperforming traditional alkyd systems in maintaining aesthetic appeal. A major growth driver is their low-VOC formulation, which complies with EPA, CARB, and EU Paints Directive standards, making them ideal for environmentally conscious consumers and regulated markets. As demand increases for high-performance, eco-friendly coatings, acrylic enamels continue to lead the global water-based enamel market.

Retail Channel Dominates with 51.7% Share Driven by DIY Demand and Color Customization

The retail segment (paint stores and big box retailers) leads the water-based enamel market with a 51.7% market share in 2025, fueled by strong demand from DIY consumers and small-scale professional contractors. Within the home improvement and decorative coatings market, these channels provide easy access to water-based enamels in quart and gallon packaging, suitable for residential painting and renovation projects. A key advantage of retail stores is the availability of advanced color matching and tinting services, offering thousands of customizable shades that drive in-store purchasing decisions over online or direct channels. Additionally, retail outlets provide expert guidance, product demonstrations, and immediate availability, enhancing customer experience and convenience. The growing trend of home renovation, interior décor upgrades, and eco-friendly paint adoption further strengthens retail dominance. This combination of accessibility, customization, and consumer engagement reinforces the leading position of retail channels in the global water-based enamel market.

Competitive Landscape Analysis of the Water-Based Enamel Market

AkzoNobel Strengthens Water-Based Enamel Leadership Through Axalta Merger Strategy

AkzoNobel N.V. is reinforcing its dominance in the water-based enamel market with its ongoing merger with Axalta, positioning itself as the global leader in high-performance enamel coatings. In Q1 2026, the company reported an 80 basis point increase in profitability, supported by pricing discipline and operational efficiency. Its “Rhythm of Blues” 2026 collection incorporates advanced non-yellowing waterborne enamel resins for superior aesthetic durability. AkzoNobel’s Dulux and Sikkens lines now integrate AI-driven color formulation systems, reducing tinting waste by 12%. With continued investment in low-VOC, energy-efficient manufacturing and operational restructuring, the company maintains a strong competitive edge in sustainable waterborne enamel technologies.

PPG Advances AI-Designed Waterborne Enamel Coatings for Automotive and Aerospace

PPG Industries, Inc. is driving innovation in the water-based enamel coatings market through its advanced DELTRON® NXT technology, which uses machine learning to optimize molecular structures for faster drying and improved finish quality. The company reported USD 15.9 billion in 2025 net sales, with sustainably advantaged products contributing 43% of total revenue. PPG is investing heavily in digital visualization platforms and e-commerce tools, enabling customers to simulate enamel finishes under different lighting conditions. Its leadership in aerospace and automotive refinish enamels is supported by formulations that meet stringent Scope 3 emission targets, reinforcing its position in high-performance, eco-friendly coating systems.

Sherwin-Williams Dominates North American Architectural Water-Based Enamel Market

The Sherwin-Williams Company holds the largest share in the North American architectural enamel market, driven by its strong contractor network and product innovation. The company has integrated bio-based monomers derived from castor and soy into its waterborne enamel formulations to meet ESG mandates. Its Emerald® and Solo™ enamel lines are widely distributed through over 4,800 stores, ensuring just-in-time delivery for professional painters. Sherwin-Williams reported a 6.8% increase in consolidated net sales in early 2026, supported by rising demand for high-build water-based enamel coatings in commercial MRO applications. Its proprietary self-leveling acrylic enamel technology delivers smooth, alkyd-like finishes.

Nippon Paint Expands Multi-Surface Waterborne Enamel Solutions in Asia-Pacific

Nippon Paint Holdings is accelerating growth in the water-based enamel market through its strategic focus on the Asia-Pacific region, which accounts for over 45% of global demand. The company has introduced quick-dry polyurethane enamel coatings designed for high-humidity climates, maintaining performance even at 85% relative humidity. Its Green Choice-certified enamel products target low-odor indoor applications across China and India. Nippon Paint leads in multi-surface enamel coatings, providing consistent gloss across wood, metal, and masonry substrates, reducing SKU complexity for contractors. This strategy positions the company strongly in both consumer and business segments within emerging markets.

Asian Paints Leads Decorative Waterborne Enamel Innovation in Emerging Markets

Asian Paints Limited is a key player in the water-based enamel market, particularly in the Indian subcontinent, where it dominates decorative coatings. In 2026, the company launched Apcolite Advanced PU Enamel, offering a 4-year rust protection warranty—an industry first in waterborne enamel systems. Its on-site tinting technology enables over 2,000 shades at retail points, enhancing customization for consumers. The Rustshield PU and Tractor Enamel lines provide durable and cost-effective solutions for residential and agricultural applications. Asian Paints also leverages its digital “Find Contractor” ecosystem, connecting trained professionals with end-users to ensure proper application of advanced water-based enamel coatings.

China Driving Zero-VOC Water-Based Enamel Adoption Across Infrastructure and Electronics

China is rapidly scaling the water-based enamel market, driven by aggressive environmental mandates and large-scale industrial deployment. Government initiatives under the “Green Manufacturing Upgrade 2026” are incentivizing manufacturers to achieve up to 90% VOC reduction, significantly accelerating the transition toward waterborne enamel systems.

Technological advancements include the development of graphene-reinforced water-based enamels, enhancing EMI shielding performance for EV battery enclosures and 5G infrastructure components. Major investments in polymer supply chains are strengthening domestic production capabilities, reducing reliance on imports. Infrastructure expansion is driving demand for anti-corrosion enamel primers, particularly in the rollout of 5G base stations.

Key applications include coatings for consumer electronics, EV components, and telecommunications infrastructure. Regulatory updates enforcing strict limits on hazardous substances are further pushing adoption of 100% water-reducible enamel coatings, positioning China as a global leader in high-volume, low-emission enamel technologies.

United States Advancing PFAS-Free Enamel Systems and Aerospace Applications

The United States is transforming the water-based enamel coatings market through regulatory compliance and innovation in aerospace and industrial applications. Updated EPA VOC standards are accelerating the shift toward HAP-free water-based enamels, particularly for federal infrastructure and high-performance coatings.

Technological advancements include the commercialization of hybrid laser-UV-waterborne curing systems, enabling high-durability enamel coatings for aerospace maintenance and repair operations. Product innovations such as self-cleaning water-based enamels are improving surface performance and reducing maintenance needs.

Strategic investments are supporting the development of advanced basecoat systems with improved color consistency and performance. Key applications include low-outgassing enamel coatings for semiconductor clean-room environments and high-reflectivity enamel markings for transportation infrastructure. These developments position the U.S. as a leader in high-performance and sustainable water-based enamel technologies.

Germany Leading Sustainable Enamel Innovation with Cobalt-Free and Circular Solutions

Germany is at the forefront of sustainable water-based enamel coatings, driven by strict regulatory frameworks and circular economy initiatives. The transition to cobalt-free drying systems using manganese-based alternatives is eliminating hazardous substances from enamel formulations.

Technological advancements include the development of polyurethane-alkyd hybrid enamels, meeting strict formaldehyde emission limits while maintaining high performance. Product innovation such as de-bonding enamel layers is enabling easier recycling of coated substrates, supporting circular economy goals.

Strategic investments in low-migration enamel centers are enhancing food-safe coating solutions. Key applications include corrosion-resistant enamel coatings for offshore wind turbines and breathable coatings for heritage building renovation. Government initiatives promoting sustainable construction materials are further driving adoption, positioning Germany as a leader in eco-friendly and high-performance enamel coatings.

India’s Rapid Expansion Driven by Infrastructure Projects and Domestic Manufacturing Growth

India is emerging as a high-growth market in the water-based enamel sector, supported by infrastructure expansion and strong government initiatives. Large-scale investments by major players are increasing production capacity for high-gloss water-based enamels, particularly for housing and industrial applications.

Technological advancements include the development of tropical-grade water-based enamels, designed to resist fungal growth in high-humidity environments. Infrastructure projects such as the Vande Bharat rail network are driving demand for anti-graffiti enamel coatings, improving durability and reducing maintenance.

Strategic developments in pigment supply chains are stabilizing costs and ensuring consistent quality. Key applications include water-based enamels for EV components and consumer appliances, supporting energy-efficient manufacturing processes. Government incentives under the PLI Scheme are further boosting domestic production, positioning India as a key hub for cost-effective and scalable enamel coating solutions.

Japan’s Leadership in Nano-Precision Water-Based Enamels for Electronics and Medical Applications

Japan continues to lead in nano-engineered water-based enamel coatings, focusing on precision applications in electronics, healthcare, and high-performance materials. Innovations such as nanostructured enamel coatings are enhancing anti-static and dust-repellent properties in semiconductor clean-room environments.

Technological advancements include the use of electron-beam curing systems, significantly reducing energy consumption while improving coating efficiency. Product innovations such as photocatalytic self-cleaning enamel coatings are contributing to environmental sustainability by breaking down pollutants on building surfaces.

Strategic investments are supporting the development of high-performance enamel primers for automotive and electronics sectors. Key applications include anti-fogging enamel coatings for medical devices, ensuring clarity and durability under repeated use. These developments position Japan as a leader in precision-driven and high-value enamel coating technologies.

Brazil Advancing Sustainable Water-Based Enamels for Construction and Urban Renewal

Brazil is emerging as a key market in the water-based enamel coatings industry, driven by construction growth and sustainability initiatives. Regulatory updates limiting hazardous substances are accelerating the adoption of eco-friendly enamel formulations.

Product innovations include agro-waste-based enamel binders, reducing reliance on petrochemical inputs and lowering environmental impact. Technological advancements such as anti-humidity enamel coatings are addressing challenges in tropical climates, improving durability and indoor air quality.

Strategic investments in production facilities are supporting increased supply for the housing sector. Key applications include corrosion-resistant enamel coatings for coastal infrastructure and urban renewal projects. Infrastructure investments in retrofit hubs are further driving demand, positioning Brazil as a growing hub for sustainable and cost-effective water-based enamel solutions.

Water-Based Enamel Market Report Scope

Water-Based Enamel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$75.3 Billion

|

|

Market Size (2032)

|

$104.5 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Resin Type (Acrylic Enamel, Polyurethane, Water-Reducible Alkyd Enamel, Styrene-Butadiene Enamel, Hybrid Systems), By Raw Material (Resins, Pigments, Solvents, Additives), By Technology (Low-VOC Formulations, Zero-VOC Formulations, Antimicrobial, Quick-Dry Technology, Direct-to-Metal), By Substrate (Wood and Furniture, Metal, Concrete and Masonry, Plastics and PVC, Drywall and Plaster), By End-User Industry (Building and Construction, Automotive and Transportation, Industrial Manufacturing, Consumer Goods and Furniture, Packaging and Food Industry), By Sales Channel (Direct Sales, Retail, Online)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Kansai Paint Co., Ltd., BASF SE, Benjamin Moore and Co., Jotun A/S, Berger Paints India Limited, Hempel A/S, Tikkurila Oyj, Brillux GmbH and Co. KG, Masco Corporation, Shalimar Paints Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Based Enamel Market Segmentation

By Resin Type

- Acrylic Enamel

- Polyurethane

- Water-Reducible Alkyd Enamel

- Styrene-Butadiene Enamel

- Hybrid Systems

By Raw Material

- Resins

- Pigments

- Solvents

- Additives

By Technology

- Low-VOC Formulations

- Zero-VOC Formulations

- Antimicrobial

- Quick-Dry Technology

- Direct-to-Metal

By Substrate

- Wood and Furniture

- Metal

- Concrete and Masonry

- Plastics and PVC

- Drywall and Plaster

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Industrial Manufacturing

- Consumer Goods and Furniture

- Packaging and Food Industry

By Sales Channel

- Direct Sales

- Retail

- Online

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Water Based Enamel Industry

- AkzoNobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- BASF SE

- Benjamin Moore & Co.

- Jotun A/S

- Berger Paints India Limited

- Hempel A/S

- Tikkurila Oyj

- Brillux GmbH & Co. KG

- Masco Corporation

- Shalimar Paints Limited

*- List not Exhaustive