Water-Soluble Paints Market Size Expansion Anchored in Bio-Based Innovation and Low-Emission Coatings Demand

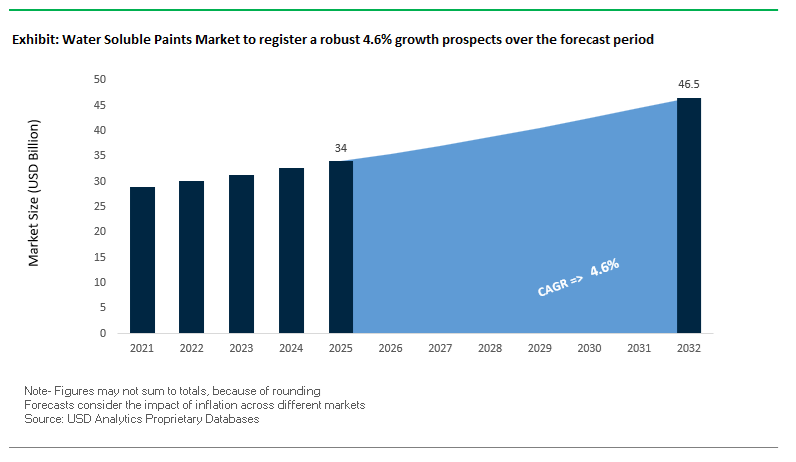

The global Water-Soluble Paints Market was valued at $34 billion in 2025 and is projected to grow at a CAGR of 4.6% from 2025 to 2032, reaching $46.6 billion by 2032. This growth trajectory reflects the increasing global shift toward low-emission, environmentally compliant coating technologies, particularly across automotive, architectural, wood coatings, and marine applications. Water-soluble paints—formulated using water as the primary solvent—are gaining strong traction due to their minimal VOC emissions, reduced toxicity, improved workplace safety, and compliance with stringent environmental regulations.

A key structural driver of this market is the transition toward sustainable and bio-based coating chemistries, supported by regulatory frameworks targeting carbon reduction and indoor air quality improvement. The adoption of bio-attributed resins, renewable raw materials, and advanced dispersion technologies is enhancing performance parameters such as durability, adhesion, gloss retention, and resistance to environmental stressors. In parallel, the rising demand for high-performance coatings in electric vehicles (EVs), green buildings, and marine efficiency applications is accelerating the penetration of water-soluble systems into traditionally solvent-dominated segments.

The market is also benefiting from increasing investments in functional coatings, including heat-reflective, anti-fungal, antimicrobial, and UV-resistant formulations. These innovations are particularly relevant in regions experiencing extreme climatic variability, where coatings are expected to deliver both protective and energy-efficiency benefits. Additionally, the integration of fast-drying resins and energy-efficient curing technologies is improving application efficiency, reducing operational downtime, and lowering lifecycle costs for end users.

From a regional perspective, Asia-Pacific leads in volume demand due to rapid urbanization and industrial expansion, while Europe and North America are driving premiumization through advanced R&D, sustainability certifications, and bio-based product innovation. Overall, the Water-Soluble Paints Market is transitioning toward high-performance, environmentally optimized, and application-specific coating solutions, positioning it as a critical segment within the broader sustainable coatings ecosystem.

Market Analysis: Bio-Based Product Launches, and Regional Capacity Expansion Driving Market Evolution

The Water-Soluble Paints Market is undergoing a significant transformation driven by strategic mergers, breakthrough product innovations, and targeted capacity expansions, reshaping competitive dynamics across key end-use industries. A central development is the continued progress of the AkzoNobel–Axalta merger, which is expected to close by late 2026. This strategic combination aims to create a $17 billion global coatings leader, with a unified R&D focus on next-generation water-soluble technologies across automotive refinish and industrial wood coatings. The merger reflects a broader industry trend toward innovation consolidation and scale-driven efficiency.

Technological innovation is emerging as a primary growth lever. In February 2025, AkzoNobel introduced Sikkens Autowave Optima, a next-generation waterborne basecoat system capable of reducing process time by up to 50% while cutting energy consumption and carbon emissions by as much as 60%. Similarly, Benjamin Moore’s 2026 Eco Spec® launch emphasizes zero VOC and zero-emission formulations, combined with rapid re-occupancy capabilities tailored for healthcare and commercial infrastructure environments. These developments underscore the market’s pivot toward high-efficiency, low-emission, and user-centric coating solutions.

Regional expansion and localized innovation strategies are also playing a critical role. PPG Industries’ 2025 commissioning of its Thailand-based waterborne coatings facility—with a 2,000-ton annual capacity—highlights the growing importance of Southeast Asia as a manufacturing hub for automotive OEM coatings, particularly in support of EV production. Meanwhile, Asian Paints’ 2026 launch of solar-reflective and anti-fungal exterior coatings addresses climate-driven performance requirements, offering surface temperature reductions of up to 5°C in high-heat urban environments.

Sustainability-driven product development continues to accelerate across the value chain. AkzoNobel’s RUBBOL WF 3350 bio-based coating, featuring 20% renewable content verified through ASTM standards, represents a significant advancement in eco-friendly wood coatings. Additionally, BASF’s “Driving the Proxy” color collection integrates advanced pigments with bio-attributed resins, aligning aesthetic innovation with sustainability goals. In the marine segment, Jotun’s water-soluble coatings contributed to avoiding 11.8 million tonnes of CO₂ emissions in 2025, highlighting the role of advanced coatings in improving fuel efficiency and environmental performance.

Further reinforcing this trajectory, AkzoNobel China’s Dulux “Angel Edition” launch incorporates 48% bio-based content, targeting improved indoor air quality for residential and institutional settings. Collectively, these developments indicate a market transitioning toward integrated, sustainable, and high-performance water-soluble coating technologies, supported by mergers, R&D investments, and evolving regulatory frameworks.

Market Trend: SCAQMD Rule 1113 Driving Ultra-Low VOC Water-Soluble Paint Formulations

The enforcement of SCAQMD Rule 1113 continues to position the water-soluble paints market at the forefront of global low-VOC coatings innovation. As of 2026, the 50 g/L VOC cap for both flat and non-flat coatings has become a de facto global benchmark, with an aggressive push toward 25 g/L VOC limits for high-volume architectural primers. This regulatory environment is accelerating the transition toward ultra-low VOC water-soluble paints and environmentally compliant architectural coatings.

A critical technical evolution in 2026 is the industry-wide shift from EPA Test Method 24 to SCAQMD Method 313, which utilizes gas chromatography for more precise VOC measurement. This advancement is particularly important for modern waterborne systems where traditional methods exhibit a 10% to 20% margin of error, ensuring accurate compliance verification and enhancing product credibility in regulated markets.

To maintain application performance under strict VOC limits, manufacturers are incorporating reactive diluents that chemically integrate into the polymer matrix, preserving open time and workability. These innovations enable water-soluble paints to achieve Class 1 scrub resistance as per ISO 11998, even with significantly reduced solvent content. This balance between durability and environmental compliance is reinforcing the adoption of high-performance water-soluble coatings in residential and commercial construction.

Market Trend: China GB/T 41659-2025 Standard Enhancing Hygrothermal Stability and Durability

China’s GB/T 41659-2025 standard, fully enforced nationwide by late 2025, is redefining performance expectations for water-soluble paints, particularly in high-humidity regions such as the Pearl River Delta. The regulation emphasizes hygrothermal stability, addressing the failure of traditional coatings under prolonged moisture exposure.

A key requirement is the minimum wet-state bond strength of ≥ 0.4 MPa after 168 hours of continuous water immersion. This benchmark has effectively phased out non-polymer-modified water-soluble paints from coastal commercial applications, accelerating the adoption of polymer-enhanced formulations designed for moisture resistance and long-term durability.

Additionally, the standard mandates zero chalking performance, requiring a Rating of 0 under ASTM D4214 after 500 hours of accelerated weathering in high-humidity conditions. This ensures superior surface integrity and long-term aesthetic performance, particularly in government infrastructure and large-scale urban development projects. These stringent requirements are driving demand for high-durability water-soluble coatings and advanced moisture-resistant paint technologies across Asia-Pacific markets.

Market Opportunity: Zero-VOC Water-Soluble Paints Driving Growth in Green Building and Indoor Air Quality Markets

The tightening of global green building standards such as LEED v4.1, WELL Building Standard, and BREEAM is creating strong opportunities for zero-VOC water-soluble paints, defined as having VOC levels below 5 g/L. These ultra-low emission coatings are becoming a mandatory specification in healthcare, education, and high-performance building projects where indoor air quality is a critical parameter.

Advanced 2026 formulations are demonstrating up to 90% reduction in total volatile organic compound emissions within the first 11 days of application, as validated by UL GREENGUARD Gold certification criteria. This rapid emission reduction is enabling faster project handovers, particularly in occupied environments such as hospitals and institutional buildings.

In addition to low emissions, modern water-soluble paints are incorporating bio-renewable resin systems with bio-based carbon content of 25% or higher, validated through ASTM D6866 testing. This enables developers to secure renewable material credits under evolving LEED v5 and BREEAM frameworks, aligning coating solutions with broader sustainability and carbon reduction goals.

Further enhancing their value proposition, zero-VOC water-soluble paints are increasingly integrated with formaldehyde-scavenging functionality. These coatings chemically capture ambient formaldehyde through functionalized amine groups, reducing indoor concentrations by approximately 15% to 20% through passive interaction. This positions zero-VOC paints as a key solution in the healthy building materials market.

Market Opportunity: Anti-Mold and Anti-Fungal Water-Soluble Paints Addressing Hygienic Surface Requirements

Rising concerns over mold remediation costs in hospitality and multifamily housing sectors are driving demand for anti-mold and anti-fungal water-soluble paints. These advanced coatings incorporate mineral-based biocides, delivering active protection against microbial growth in high-moisture environments.

2026-generation anti-mold water-soluble paints achieve a Rating of 0 under ASTM G21 testing, indicating zero fungal growth even after 28 days of continuous exposure to humid conditions. This level of performance is critical for applications in bathrooms, kitchens, and coastal residential developments where moisture-induced degradation is a persistent issue.

The longevity of biocidal performance has significantly improved through the use of nano zinc oxide and silver-ion encapsulation technologies. These systems maintain antimicrobial efficacy for more than five years, outperforming traditional liquid biocides that degrade or leach within the first year of application.

In addition to microbial resistance, these coatings are engineered with a low surface free energy below 25 mN/m, creating easy-clean surfaces that reduce the adhesion of organic contaminants by approximately 40%. This not only enhances hygiene but also reduces maintenance requirements, making anti-fungal water-soluble paints a high-growth segment within the functional coatings market.

Water Soluble Paints Market Share and Segmentation Insights

Polyacrylate-Based Paints Lead with 38.9% Share Due to Versatility and Regulatory Compliance

The polyacrylate-based segment dominates the water soluble paints market with a 38.9% market share in 2025, driven by its exceptional versatility, performance, and environmental compliance. In the water-based coatings and eco-friendly paints market, polyacrylate formulations offer excellent adhesion, gloss retention, and UV resistance, making them ideal for both industrial coatings and decorative paint applications. These paints are widely used in metal primers, automotive coatings, wood finishes, and general industrial applications, where durability and finish quality are critical. A key advantage is their water solubility, enabling easy cleanup and reduced solvent usage, aligning with global sustainability goals. Additionally, polyacrylate-based paints comply with strict low-VOC regulations such as EPA, REACH, and EU environmental standards, without compromising performance. As industries increasingly shift toward sustainable, high-performance coating technologies, polyacrylate-based systems continue to lead the global water soluble paints market.

Direct Sales Channel Leads with 44.7% Share Driven by Industrial Bulk Procurement and Customization

The direct sales segment leads the water soluble paints market by distribution channel with a 44.7% market share in 2025, supported by strong demand from large-scale industrial manufacturers and OEMs. Within the industrial coatings and water-based paint supply chain, industries such as automotive, industrial equipment, and furniture manufacturing procure paints directly in bulk quantities including drums, intermediate bulk containers (IBCs), and tankers. This approach ensures cost efficiency, consistent quality, and uninterrupted supply for high-volume production lines. Additionally, direct supplier relationships enable the development of custom formulations tailored to specific performance requirements, including color matching, corrosion resistance, and substrate compatibility. OEMs rely on this collaboration to meet strict quality standards and application-specific demands, reinforcing the importance of direct sales. The combination of volume efficiency, technical support, and formulation customization continues to drive the dominance of direct sales in the global water soluble paints market.

Competitive Landscape Analysis of the Water Soluble Paints Market

AkzoNobel Strengthens Aesthetic and Sustainable Leadership in Water Soluble Paints

AkzoNobel N.V. continues to lead the water soluble paints market by integrating high-performance water-soluble pigments into its 2026 “Rhythm of Blues” collection, including Mellow Flow™, Slow Swing™, and Free Groove™. The company streamlined its portfolio by divesting AkzoNobel Pakistan in April 2026, focusing on high-margin European and North American segments. Holding an estimated 18–20% share of the global waterborne architectural market, AkzoNobel leverages AI-optimized formulations to reduce raw material waste by 12%. Its Global Aesthetic Center drives innovation in sustainable paint chemistry and design-led coatings, reinforcing its leadership in premium decorative and industrial applications.

PPG Expands Instant-Dry Waterborne Coatings and Data Center Protection Solutions

PPG Industries, Inc. is advancing in the water soluble paints market through pricing strategies and innovation in high-performance coatings. Entering Q2 2026, the company exceeded financial expectations after implementing global price increases of up to 20% to offset raw material volatility. PPG is investing in a new radiation-curable coatings testing line in France to accelerate the development of instant-dry waterborne coatings for industrial assembly lines. Its specialized coatings for data centers provide thermal reflectance and electromagnetic shielding, addressing critical infrastructure needs. These innovations position PPG strongly in industrial protective coatings and advanced waterborne solutions.

Sherwin-Williams Drives Professional Adoption with Washable Low-Odor Water Soluble Paints

The Sherwin-Williams Company dominates the water soluble paints market in North America through its strong professional contractor network and high-performance coatings portfolio. Its 2026 Color of the Year aligns with “Warm Minimalism” trends, extending repaint cycles in commercial and residential spaces. Sherwin-Williams offers washable satin and eggshell finishes with low-odor technology, enabling painting in occupied buildings without operational disruption. The company’s forecast-aligned procurement system uses big data analytics to reduce supply chain lag by 15%. Its water-reducible alkyd hybrids provide the durability of oil-based paints with easy water cleanup, strengthening its position in industrial wood and metal coatings.

Asian Paints Leads Premium Decorative Water-Based Finishes with Digital Integration

Asian Paints Limited is a dominant player in the water soluble paints market, particularly in premium interior segments. Its 2026 Color of the Year, Moonlit Silk (7809), is a water-based silk emulsion designed for high-end decorative applications. The company is transitioning into an integrated building solutions provider, focusing on smart coatings, self-cleaning surfaces, and temperature-responsive finishes. Its “Solar Punk” and “Day Dream” palettes introduce water-soluble mineral finishes such as lime plaster and stone textures, redefining interior aesthetics. With over 70,000 retail touchpoints and the Beautiful Homes digital ecosystem, Asian Paints seamlessly connects design trends with on-demand tinting solutions.

Nippon Paint Expands APAC Leadership with Quick-Dry Waterborne Enamels

Nippon Paint (NIPSEA Group) is strengthening its presence in the water soluble paints market, particularly in the Asia-Pacific region, which accounts for the majority of global growth. Ranked among the top global competitors, Nippon Paint India expanded its workforce to 2,399 employees by March 2026, reflecting regional growth. The company’s quick-dry waterborne enamels cater to automotive and decorative applications, contributing to a 47.9% growth share in APAC markets. Its “HERizons” initiative and sustainability partnerships highlight its commitment to inclusive growth and eco-friendly supply chains. The acquisition of Vibgyor Paints further enhances its capacity in South Asian infrastructure coatings.

China’s “Blue Sky” Policy Driving Industrial-Scale Adoption of Water-Based Coatings

China continues to dominate the global water soluble paints market, fueled by aggressive environmental regulation and rapid industrial expansion. The enforcement of the GB 30981-2020 VOC emission standard has effectively eliminated high-VOC coatings across most industrial applications, mandating water-based alternatives in nearly all government-funded infrastructure projects. This regulatory push has significantly accelerated the adoption of eco-friendly water-borne coatings across sectors such as construction, automotive, and public utilities.

The country’s industrial ecosystem is also evolving to support this shift. Covestro’s newly completed Shanghai facility for water-borne polyurethane dispersions (PUDs) highlights the growing demand from automotive and textile industries. Infrastructure development remains a key growth driver, with massive utilization of water-based coatings in projects related to 5G networks, high-speed rail, and utilities. China’s leadership in electric vehicle (EV) manufacturing is further reinforcing demand, with a majority of new EV plants adopting advanced 3-wet water-borne spray technologies. Additionally, smart coatings with self-cleaning and thermal insulation properties are gaining traction in urban developments, while antibacterial water-borne latex applications are expanding rapidly across healthcare infrastructure.

United States: Regulatory Compliance and High-Performance Coating Innovations

The United States water soluble paints market is undergoing a transformation driven by stringent environmental regulations and infrastructure modernization initiatives. The Infrastructure Investment and Jobs Act (IIJA) has significantly boosted demand for water-borne acrylic coatings in bridge and highway maintenance, where corrosion resistance and durability are critical. Simultaneously, the expansion of CARB-compliant VOC standards across multiple states is enforcing stricter limits, accelerating the shift toward low-VOC and water-based paint formulations.

Innovation remains central to the U.S. market’s competitiveness. Leading manufacturers are developing high-performance water-based coatings that match the durability of solvent-based alternatives, particularly for heavy-duty sectors such as agricultural and construction equipment. Consumer demand is also rising, with strong growth in DIY and retail segments driven by low-odor, one-coat water-borne latex paints. The increasing adoption of bio-based resins in sustainable product lines is aligning with green building certifications like LEED. Additionally, the aerospace sector is witnessing growing use of water-borne epoxy primers, highlighting the broader shift toward safer, EPA-compliant coating solutions across industries.

Germany: Innovation Hub for Sustainable and High-Performance Water-Based Paints

Germany stands at the forefront of the European water soluble paints market, driven by strict EU regulations and advanced R&D capabilities. The implementation of updated Construction Products Regulation has further reduced permissible VOC levels, resulting in water-borne coatings dominating the architectural segment. This regulatory environment has created a robust demand for sustainable, high-performance coatings across residential and commercial construction.

The country is also witnessing a strong transition in industrial wood coatings, with increasing adoption of water-borne alkyd-hybrid systems to meet stringent indoor air quality standards. Innovation in renewable content is gaining momentum, as seen in new product launches targeting eco-conscious furniture markets. Government-backed renovation programs are further driving the use of water-based thermal-reflective coatings in energy-efficient retrofits. German manufacturers are investing heavily in advanced dispersion technologies, including self-crosslinking resins for enhanced durability. Additionally, compliance with EU Biocide Regulations is pushing the development of preservative-free water-based paints, catering to health-sensitive consumer segments.

India: Rapid Urbanization Accelerating Demand for Water-Based Decorative Coatings

India represents one of the fastest-growing markets for water soluble paints, supported by urbanization, infrastructure development, and a shift toward organized paint sectors. Major domestic players are significantly expanding production capacity, particularly in water-borne polymer emulsions, to meet rising demand. Government initiatives such as the “Housing for All” scheme are generating substantial consumption of water-based decorative coatings for both interior and exterior applications.

The Smart Cities Mission is further boosting the adoption of specialized water-borne coatings, including anti-carbonation solutions designed to protect urban infrastructure. Consumer behavior is also evolving, with increasing preference for water-based emulsions over traditional lime-wash, particularly in emerging Tier 2 and Tier 3 cities. Regulatory developments, including mandatory eco-friendly paint certifications by the Bureau of Indian Standards, are reinforcing the shift toward water-soluble chemistry. Additionally, the automotive refinish segment is witnessing rapid adoption of water-borne basecoats, driven by the need for improved finish quality and enhanced workplace safety.

Japan: Advanced Functional Coatings for Infrastructure Longevity and Electronics

Japan’s water soluble paints market is characterized by its focus on high-performance, functional coatings designed for longevity and precision applications. Government initiatives targeting aging infrastructure are promoting the use of advanced water-borne fluoropolymer coatings, offering extended maintenance cycles for bridges and public assets. This aligns with Japan’s broader strategy of life-extension technologies in construction and infrastructure.

The country is also a leader in high-purity, water-based coatings for electronics manufacturing, including applications in EV batteries and semiconductor cleanrooms. Urban sustainability initiatives, such as efforts to mitigate the Urban Heat Island effect, are driving increased adoption of solar-reflective water-borne paints. Strict formaldehyde emission standards have made VOC-free coatings the standard for residential interiors. Innovation continues in areas such as flexible elastomeric coatings for seismic resilience and robotic application technologies for prefabricated housing, highlighting Japan’s integration of automation with advanced coating solutions.

Brazil: Cost Advantage and Automotive Expansion Strengthening Regional Leadership

Brazil plays a pivotal role in the South American water soluble paints market, leveraging its natural resource base and strong automotive manufacturing sector. The availability of Titanium Dioxide (TiO₂) enables domestic production of high-opacity water-based paints at competitive costs, providing a significant advantage over imports. Industry initiatives such as the Abrafati Quality Program have improved product standards, accelerating the transition toward water-borne coatings in the formal architectural segment.

The automotive sector remains a key growth driver, with widespread adoption of water-based coatings in OEM paint shops. Brazilian R&D efforts are focused on enhancing UV resistance in water-borne acrylic coatings to withstand tropical climatic conditions. Government-backed social housing programs continue to generate steady demand for water-based emulsions, supporting large-scale residential construction. Additionally, the agricultural machinery sector is increasingly adopting water-borne protective coatings to meet international compliance standards, driven by rising exports of key crops such as soy and corn.

Water Soluble Paints Market Report Scope

Water Soluble Paints Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34 Billion

|

|

Market Size (2032)

|

$46.6 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product (Polyacrylate-based, Alkyd-based, Epoxy-based, Epoxy Ester-based, Polyester-based, Polyurethane-based, Vinyl-based), By Technology (Water-Soluble, Waterborne Dispersions, Colloidal Dispersions, Bio-based), By Application (Architectural Coatings, Industrial Coatings, Automotive and Transportation, Packaging Coatings, Other Specialty Applications), By End-User Industry (Building and Construction, Automotive and Transportation, Industrial Manufacturing, Consumer Goods, Packaging and Graphic Arts), By Distribution Channel (Direct Sales, Retail Sales, E-commerce and Online Marketplaces, Wholesale), By Grade (Premium, Standard Grade, Economy Grade)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, BASF SE, Kansai Paint Co., Ltd., Axalta Coating Systems, Jotun A/S, RPM International Inc., Berger Paints India Limited, Hempel A/S, Masco Corporation, Tikkurila Oyj, Chenyang Waterborne Paint

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Soluble Paints Market Segmentation

By Product

- Polyacrylate-based

- Alkyd-based

- Epoxy-based

- Epoxy Ester-based

- Polyester-based

- Polyurethane-based

- Vinyl-based

By Technology

- Water-Soluble

- Waterborne Dispersions

- Colloidal Dispersions

- Bio-based

By Application

- Architectural Coatings

- Industrial Coatings

- Automotive and Transportation

- Packaging Coatings

- Other Specialty Applications

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Industrial Manufacturing

- Consumer Goods

- Packaging and Graphic Arts

By Distribution Channel

- Direct Sales

- Retail Sales

- E-commerce and Online Marketplaces

- Wholesale

By Grade

- Premium

- Standard Grade

- Economy Grade

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Water Soluble Paints Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- BASF SE

- Kansai Paint Co., Ltd.

- Axalta Coating Systems

- Jotun A/S

- RPM International Inc.

- Berger Paints India Limited

- Hempel A/S

- Masco Corporation

- Tikkurila Oyj

- Chenyang Waterborne Paint

*- List not Exhaustive