Waterborne Architectural Coatings Market Size Driven by Green Building Mandates and Energy-Efficient Coating Technologies

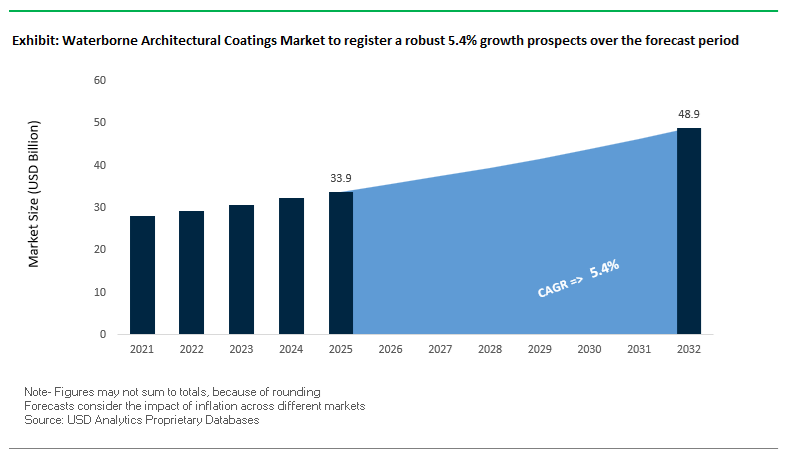

The global Waterborne Architectural Coatings Market was valued at $33.9 billion in 2025 and is projected to expand at a CAGR of 5.4% from 2025 to 2032, reaching $49 billion by 2032. This growth is being structurally driven by the rapid adoption of low-VOC, environmentally compliant coatings across residential, commercial, and institutional construction sectors. Waterborne architectural coatings have become the preferred choice due to their low odor, reduced toxicity, superior indoor air quality performance, and alignment with green building certifications such as LEED and WELL.

A defining characteristic of this market is the increasing convergence of aesthetic innovation and functional performance. Modern waterborne coatings are no longer limited to decorative applications; they are being engineered to deliver thermal insulation, UV resistance, anti-corrosion protection, and antimicrobial properties. The integration of advanced polymer emulsions, alkyd hybrids, and bio-based resins is enabling manufacturers to enhance durability, gloss retention, and substrate compatibility across diverse climatic conditions. Additionally, the demand for smart coatings that respond to environmental stimuli—such as light-adaptive colors and heat-reflective surfaces—is reshaping product development pipelines.

Sustainability remains a central growth catalyst. The market is witnessing strong momentum in carbon footprint reduction, renewable raw material adoption, and energy-efficient manufacturing processes. Architectural coatings are increasingly being positioned as active contributors to energy efficiency, particularly through technologies that reduce heat absorption, improve insulation, and extend building lifecycle performance. Furthermore, rapid urbanization in emerging economies, combined with renovation cycles in developed markets, is fueling demand for premium, high-performance waterborne coating systems.

Market Analysis: Low-Carbon Innovation, Cross-Segment Applications, and Digitalization Reshaping Market Dynamics

The Waterborne Architectural Coatings Market is undergoing a transformative phase marked by sustainability-led innovation, strategic collaborations, and cross-industry application expansion. A significant development is the March 2026 transition of BASF Coatings into a standalone entity, following its deal with Carlyle. This move is expected to accelerate innovation cycles in waterborne and low-carbon coating technologies, particularly in Europe and North America, where regulatory pressure and sustainability benchmarks are most stringent.

Technological advancements are increasingly focused on integrating coatings into energy-efficient building ecosystems. In October 2025, AkzoNobel launched its solar-absorbing wall technology, enabling building facades to function as thermal energy management systems. This innovation represents a shift toward coatings as active energy assets rather than passive protective layers. Complementing this trend, the AkzoNobel–Arkema–BASF consortium announced in September 2025 aims to reduce the carbon footprint of architectural coatings by 20% to 30% through bio-attributed resin integration, highlighting the industry’s commitment to decarbonization without compromising performance.

Product innovation is also advancing in terms of durability and environmental resilience. Jotun’s 2025 launch of next-generation waterborne barrier technologies introduced enhanced zinc-rich formulations with faster curing times, specifically designed for coastal and high-humidity infrastructure environments. Meanwhile, AkzoNobel’s expansion into marine-architectural hybrid applications demonstrates the versatility of waterborne coatings, with industrial-grade formulations now being used in ferry cabin structures, bridging the gap between architectural and marine performance requirements.

Digitalization is emerging as a key differentiator. BASF’s launch of its Product Carbon Footprint (PCF) digital tool enables architects, contractors, and developers to quantify the exact CO₂ impact of waterborne coatings, supporting compliance with green building standards and enhancing transparency across the value chain. Additionally, PPG’s 2026 “Parallels” design theme reflects the growing importance of adaptive aesthetics, with coatings capable of altering visual perception under varying lighting conditions—an innovation that blends design sophistication with material science.

Capacity expansion and regional growth strategies further reinforce market momentum. Asian Paints’ new high-capacity facility in Madhya Pradesh, capable of producing 400,000 kiloliters annually, is scaling to meet rising demand in Tier 2 and Tier 3 cities, where urbanization and housing development are accelerating. Alongside this, AkzoNobel’s investment in renewable energy infrastructure, including its solar-powered production facility in Poland, underscores the industry's shift toward sustainable manufacturing practices.

Market Trend: USP <1790> Lifecycle Approach Elevating Quality Standards in Waterborne Coating Systems

The application of USP <1790> standards is redefining quality assurance protocols in the waterborne architectural coatings market, particularly in pharmaceutical coating applications where functional performance is critical. In 2026, regulatory authorities are extending the scope of visual inspection principles to waterborne sustained-release coatings, treating membrane uniformity as a critical quality attribute that requires statistical validation across the product lifecycle.

Manufacturers are now required to implement sensitivity verification protocols to demonstrate that automated inspection systems can detect coating thickness variations as small as ≤10 micrometers on multiparticulate surfaces. This represents a significant shift from traditional visual inspection methods, reinforcing the need for precision coating technologies and advanced quality control systems.

In addition, lifecycle management mandates continuous monitoring from product development through post-market surveillance. As a result, 2026 manufacturing processes are increasingly integrating in-line Near-Infrared spectroscopy to enable real-time verification of coating thickness and uniformity. This trend is accelerating the adoption of smart manufacturing technologies and digital quality assurance systems in waterborne coating applications.

Market Trend: FDA Functional Coating Defect Guidelines Driving Zero-Defect Manufacturing Standards

The evolving FDA guidance on functional coating defects is intensifying regulatory scrutiny within the waterborne coatings market, particularly for sustained-release and delayed-release pharmaceutical applications. In 2026, the agency has introduced a zero-tolerance approach toward critical defects such as pinholes, micro-cracking, and delamination, recognizing their potential to cause dose dumping and compromise drug safety.

Inspection observations from recent FDA Form 483 reports highlight increased enforcement against micro-cracking issues associated with improper film coalescence in aqueous dispersions. This is driving manufacturers to optimize formulation chemistry and processing conditions to ensure consistent film integrity and eliminate structural weaknesses.

Delamination of the functional coating layer is now considered a high-risk defect during pre-approval inspections, prompting a shift toward soft-resin waterborne blends that maintain flexibility over the product shelf life. These advancements are reinforcing the importance of robust film-forming polymers and flexible coating matrices in achieving regulatory compliance and long-term product stability.

Market Opportunity: Ethylcellulose Aqueous Dispersions Driving Efficiency in Multiparticulate Drug Coatings

The increasing adoption of multiparticulate drug delivery systems is creating significant opportunities for ethylcellulose aqueous dispersions within the waterborne coatings market. These advanced formulations are replacing traditional solvent-based systems, offering both processing efficiency and environmental benefits.

Modern waterborne ethylcellulose dispersions enable high solids loading of up to 30% by weight, reducing coating cycle times by approximately 35% to 45% compared to solvent-based alternatives. This efficiency gain is particularly valuable in high-volume pharmaceutical manufacturing, where throughput optimization is a key operational priority.

The elimination of organic solvents such as isopropanol and methylene chloride significantly reduces the need for explosion-proof infrastructure and solvent recovery systems, which can account for up to 20% of facility operating costs. This positions waterborne coatings as a cost-effective and sustainable solution in pharmaceutical production environments.

In terms of performance, these coatings demonstrate high mechanical robustness, achieving drug recovery rates of 95% or higher after stress testing. This ensures that coated multiparticulates can withstand downstream processing such as capsule filling and tablet compression, maintaining product integrity throughout the manufacturing chain.

Market Opportunity: pH-Independent Waterborne Coatings Advancing Controlled Drug Release Technologies

The development of pH-independent sustained-release coatings represents a major technological opportunity in 2026, particularly for weakly basic drugs that are sensitive to gastrointestinal pH variations. Waterborne coating systems are enabling consistent drug release profiles across a broad pH range, addressing a key challenge in oral drug delivery.

Advanced formulations are achieving drug release variance of less than ±5% across pH conditions ranging from 1.2 to 6.8, ensuring reliable bioavailability in both fed and fasted states. This level of precision is essential for meeting bioequivalence requirements and regulatory approval standards.

The dominance of cellulose and ethylcellulose polymers, which account for approximately 37.5% of the sustained-release coatings market volume in 2026, highlights their effectiveness in forming pH-independent porous membranes. These materials are widely adopted due to their compatibility with waterborne coating technologies and their ability to deliver controlled release profiles.

By incorporating water-soluble pore formers such as hydroxypropyl methylcellulose into ethylcellulose matrices, manufacturers are achieving zero-order drug release kinetics for durations of 12 to 18 hours. This advancement significantly reduces dosing frequency and enhances patient compliance, particularly in the treatment of chronic conditions, strengthening the role of waterborne coatings in advanced pharmaceutical delivery systems.

Waterborne Architectural Coatings Market Share and Segmentation Insights

Acrylic Resins Lead with 47.3% Share Due to Superior Durability and All-Weather Application

The acrylic resin segment dominates the waterborne architectural coatings market with a 47.3% market share in 2025, driven by its exceptional durability, weather resistance, and versatility in exterior and interior applications. In the architectural coatings and water-based paints market, 100% acrylic binders are widely regarded as the premium standard for exterior wall coatings, offering superior UV resistance, flexibility, crack resistance, and strong adhesion to substrates such as concrete, masonry, and wood. These properties ensure long-lasting performance in harsh environmental conditions, reducing maintenance frequency and lifecycle costs. Additionally, acrylic coatings provide low-temperature application capability—down to 35°F (2°C)—allowing extended painting seasons in temperate and colder climates, a key advantage over alternative resin systems like vinyl-acrylic or VAE. As demand rises for high-performance, low-VOC, and environmentally compliant coatings, acrylic resins continue to lead innovation and adoption in the global waterborne architectural coatings market.

Home Improvement Centers Dominate with 33.9% Share Driven by DIY and Contractor Demand

The home improvement centers segment leads the waterborne architectural coatings market with a 33.9% market share in 2025, supported by strong demand from both DIY homeowners and professional painting contractors. Within the decorative paints and home improvement retail market, major chains such as Home Depot, Lowe’s, B&Q, and Leroy Merlin serve as key distribution hubs, offering a wide range of waterborne paints for interior and exterior applications. A major growth driver is the increasing trend of DIY home renovation and repainting projects, where consumers prioritize convenience, product variety, and immediate availability. These retailers enhance customer experience through advanced color matching systems, extended store hours, and in-store expertise, making them the preferred purchasing destination. Additionally, contractor service desks, bulk pricing, and easy logistics support attract professional users, further boosting sales volumes. This dual appeal to both retail and trade customers reinforces the dominance of home improvement centers in the global waterborne architectural coatings market.

Competitive Landscape Analysis of the Waterborne Architectural Coatings Market

AkzoNobel Strengthens Low-Carbon Waterborne Coatings Through Axalta Merger Synergies

AkzoNobel N.V. is reinforcing its leadership in the waterborne architectural coatings market through its planned all-stock merger with Axalta, a move expected to strengthen R&D in water-reducible binders and sustainable coating technologies. In Q1 2026, the company reported an 80 bps profitability improvement, supported by pricing discipline and cost control. Its Rhythm of Blues 2026 Color of the Year collection uses advanced waterborne resins to improve edge-hide and opacity in premium decorative paints. AkzoNobel also deployed drone-based inspection tools and a waterborne basecoat that cuts bodyshop application time by 20%. Its Dulux and Sikkens brands remain benchmarks for low-carbon architectural systems with up to 35% recycled content.

PPG Expands Waterborne Architectural Coatings Into Traffic Safety and Data Centers

PPG Industries, Inc. is advancing in the waterborne architectural coatings market through pricing power, acquisitions, and high-performance protective technologies. In Q1 2026, the company exceeded guidance after implementing a 15–20% global price increase to offset raw material volatility. Its April 2026 acquisition of Ozark Materials expanded PPG’s position in waterborne pavement markings and traffic safety coatings, a fast-growing architectural niche. The company is also investing in a radiation-curable coatings testing line in France to develop instant-cure waterborne finishes for commercial wood and metal components. PPG’s strategic focus on data center infrastructure coatings includes waterborne systems with solar reflectance and thermal management properties.

Sherwin-Williams Dominates Pro Painter Channel With One-Coat Waterborne Systems

The Sherwin-Williams Company maintains a commanding position in the waterborne architectural coatings market, holding a 63% share of the U.S. professional painter channel. In early 2026, it reported a 6.8% rise in net sales to USD 5.67 billion, supported by its Performance Coatings Group. With more than 4,800 company-operated stores, Sherwin-Williams ensures just-in-time supply of its Emerald® and Solo™ waterborne coating lines. Its Solo™ 100% Acrylic latex leads the 2026 one-coat application segment, using advanced leveling agents to reduce brush marks and cut labor costs by 15%. The integration of BASF’s Decorative Paints business expands its reach in Italian and French renovation markets.

Nippon Paint Advances PFAS-Free Waterborne Emulsions Across Asia-Pacific

Nippon Paint Holdings is strengthening its regional dominance in the waterborne architectural coatings market as Asia-Pacific accounts for 39.77% of global waterborne demand. The company expanded its India workforce to 2,399 employees by March 2026, reflecting strong regional growth. In July 2026, Nippon Paint launched n-SHIELD, entering the paint protection film segment while using waterborne adhesive technologies for architectural glass. Its partnership with Humble Bee targets bee-inspired biomaterials for PFAS-free waterborne emulsions by 2028. Through its N-Prime digital ecosystem, the company uses AI to predict surface degradation in humid climates and recommend waterborne sealers that prevent efflorescence.

Asian Paints Leads Integrated Wall Systems and Washable Waterborne Emulsions

Asian Paints Limited leads the waterborne architectural coatings market in the Indian Subcontinent through its unified wall-system strategy covering waterborne putty, primers, and emulsion topcoats. Its Moonlit Silk 2026 Colour of the Year is formulated as a washable waterborne silk emulsion, offering superior stain resistance and a whiteness index above 94. The company also dominates the high-gloss waterborne enamel segment in emerging markets, replacing oil paints for wood and metal trims in residential renovation. With more than 70,000 retail touchpoints and its Beautiful Homes service, Asian Paints delivers end-to-end painting solutions, capturing both DIY and professional consumer demand.

China’s Regulatory Overhaul and Green Urbanization Driving Waterborne Architectural Coatings Demand

China continues to lead the waterborne architectural coatings market, driven by strict regulatory frameworks and large-scale urban redevelopment. The implementation of GB 30981.1-2025, effective June 2026, significantly tightens limits on harmful substances, making low-VOC waterborne coatings mandatory under China Compulsory Certification (CCC) for wall and floor applications. This regulatory push is accelerating the transition toward environmentally compliant water-based architectural paints across both residential and commercial sectors.

Massive government-led redevelopment initiatives are further boosting demand. The “Old Neighborhood” renewal program targets over 50,000 aging residential communities, mandating 100% water-based interior and exterior emulsions in public procurement. Industrial expansion is also underway, with increasing investments in waterborne polyurethane dispersions (PUDs) production facilities in Shanghai and Fujian to meet rising demand. Technological innovation is reshaping the market, including graphene-enhanced coatings for coastal infrastructure and large-scale automated production hubs such as Anhui’s “Paint Valley.” Additionally, antimicrobial water-based coatings are becoming standard in healthcare infrastructure, with over 1,500 hospital projects integrating silver-ion technologies.

United States: Infrastructure Modernization and High-Performance Waterborne Systems

The U.S. waterborne architectural coatings market is evolving rapidly, supported by infrastructure modernization and innovation in coating performance. Under the Infrastructure Investment and Jobs Act (IIJA), federal specifications increasingly favor waterborne acrylic epoxy hybrids for bridges and public infrastructure due to their durability, fast drying, and crosslinking efficiency. This shift highlights the growing competitiveness of water-based coatings against traditional solvent-based systems in heavy-duty applications.

Regulatory tightening is further reinforcing market growth, with CARB and Ozone Transport Commission (OTC) states lowering VOC limits to 50 g/L for architectural coatings. At the same time, innovation in high-hiding, one-coat waterborne systems is transforming the DIY segment, driving strong retail demand through major distribution channels. The integration of bio-renewable resins is aligning products with LEED and WELL certifications, strengthening their appeal in sustainable construction. Additionally, urban initiatives such as cool roof programs are increasing the use of heat-reflective waterborne coatings, while the surge in commercial-to-residential retrofits is creating demand for ultra-low odor, zero-VOC primers in dense urban markets.

Germany: Precision Engineering and Sustainable Innovation in Waterborne Coatings

Germany remains a cornerstone of the European waterborne architectural coatings market, driven by stringent EU regulations and technological leadership. The upcoming Construction Products Regulation (CPR) updates emphasize Product Environmental Footprint (PEF) transparency, compelling manufacturers to enhance sustainability across water-based product lines. This has positioned Germany as a leader in eco-friendly, high-performance coatings for architectural applications.

Innovation is particularly strong in renewable and health-focused coatings. German facilities are advancing bio-based waterborne varnishes with high renewable content, targeting premium architectural wood segments. Simultaneously, there is a growing shift toward preservative-free formulations to meet the needs of allergy-sensitive consumers and the “healthy home” trend. Advanced functional coatings, such as photocatalytic self-cleaning facades, are gaining traction in major cities, improving building maintenance efficiency. Government-backed renovation programs are also promoting waterborne thermal-insulative coatings, while AI-powered tinting systems are enhancing precision and reducing waste in professional applications.

India: Rapid Urbanization and Premiumization Fueling Water-Based Emulsion Growth

India is emerging as the fastest-growing market for waterborne architectural coatings, driven by rapid urbanization, infrastructure development, and consumer preference shifts. Major paint manufacturers are investing heavily in waterborne production capacity, with over $1.3 billion allocated toward new mega-plants dedicated to water-based technologies. This expansion is aimed at meeting the rising demand for high-quality architectural coatings across residential and commercial sectors.

Government housing initiatives such as Pradhan Mantri Awas Yojana (PMAY) are significantly boosting consumption of water-based exterior acrylic coatings across hundreds of cities. The Smart Cities Mission is further driving the adoption of specialized coatings, including anti-carbonation solutions for urban infrastructure durability. Consumer trends are also evolving, with strong growth in premium water-based emulsions replacing traditional lime-wash, particularly among the expanding middle class. Regulatory developments such as BIS eco-labeling are reinforcing the shift toward sustainable coatings, while rural market penetration strategies are expanding the adoption of affordable waterborne distempers in smaller packaging formats.

Japan: Advanced Functional and Seismic-Resilient Waterborne Coatings

Japan’s waterborne architectural coatings market is defined by advanced functionality, durability, and regulatory rigor. The country’s F**** (F-Four Star) compliance standard—one of the strictest globally—mandates the use of low-emission waterborne coatings in all indoor public environments. This has made water-based paints the default choice for residential and commercial interiors, ensuring superior indoor air quality.

Technological innovation is a key differentiator in Japan. High-elasticity waterborne coatings are being developed to withstand seismic activity by maintaining film integrity and bridging structural cracks. Infrastructure maintenance strategies are also evolving, with water-borne fluoropolymer-latex hybrids used for long-life bridge coatings. Urban sustainability initiatives such as Tokyo’s “Cool City” program are driving demand for solar-reflective roof coatings. Additionally, advancements in robotic spray technologies are optimizing the application of waterborne coatings in prefabricated housing, while the aging population is fueling demand for low-odor, durable coatings in senior living facilities.

Brazil: Resource Integration and Regional Leadership in Waterborne Paints

Brazil is a dominant force in the Latin American waterborne architectural coatings market, supported by strong raw material availability and expanding domestic production capabilities. Industry initiatives such as the Abrafati Quality Program have significantly improved product standards, ensuring that the majority of architectural coatings meet waterborne performance benchmarks. This transition is strengthening the country’s position as a regional leader in sustainable coatings.

The availability of high-quality Titanium Dioxide (TiO₂) provides a cost advantage for domestic manufacturers, enabling competitive production of high-opacity waterborne emulsions. Innovation is focused on tropicalized formulations that resist mold and algae growth in high-humidity environments, making them ideal for Brazil’s climate. Government housing programs are driving large-scale demand for masonry paints, while sustainability trends are encouraging the adoption of recycled packaging for waterborne products. Brazil is also expanding its role as an export hub, supplying water-based coating technologies to neighboring South American markets and reinforcing its regional dominance.

Waterborne Architectural Coatings Market Report Scope

Waterborne Architectural Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$33.9 Billion

|

|

Market Size (2032)

|

$49 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Resin Type (Acrylic, Vinyl-Acrylic, Styrene-Acrylic, Alkyd, Polyurethane, Epoxy, Polyester, Vinyl Acetate-Ethylene, Natural), By Application Area (Interior Coatings, Exterior Coatings), By Product Function (Paints, Primers and Undercoats, Varnishes and Lacquers, Stains and Dyes, Sealers, Fillers and Putties), By End-User Industry (Residential, Non-Residential, Infrastructure), By Sheen (Flat, Eggshell, Satin, Semi-Gloss, High-Gloss), By Technology and Specialty Feature (Low-VOC, Antimicrobial, Elastomeric Coatings, Smart, Odorless Formulations), By Distribution Channel (Direct Sales, Specialty Paint Stores, Home Improvement Centers, E-commerce, Wholesale)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Kansai Paint Co., Ltd., Jotun A/S, Masco Corporation, Benjamin Moore and Co., RPM International Inc., BASF SE, DAW SE, Hempel A/S, Berger Paints India Limited, Tikkurila Oyj

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne Architectural Coatings Market Segmentation

By Resin Type

- Acrylic

- Vinyl-Acrylic

- Styrene-Acrylic

- Alkyd

- Polyurethane

- Epoxy

- Polyester

- Vinyl Acetate-Ethylene

- Natural

By Application Area

- Interior Coatings

- Wall and Ceiling Paints

- Trim and Cabinetry Enamels

- Floor Coatings

- Exterior Coatings

- Facade and Masonry Paints

- Roof Coatings

- Deck and Porch Stains

- Infrastructure

By Product Function

- Paints

- Primers and Undercoats

- Varnishes and Lacquers

- Stains and Dyes

- Sealers

- Fillers and Putties

By End-User Industry

- Residential

- Non-Residential

- Infrastructure

By Sheen

- Flat

- Eggshell

- Satin

- Semi-Gloss

- High-Gloss

By Technology and Specialty Feature

- Low-VOC

- Antimicrobial

- Elastomeric Coatings

- Smart

- Odorless Formulations

By Distribution Channel

- Direct Sales

- Specialty Paint Stores

- Home Improvement Centers

- E-commerce

- Wholesale

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Waterborne Architectural Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Kansai Paint Co., Ltd.

- Jotun A/S

- Masco Corporation

- Benjamin Moore & Co.

- RPM International Inc.

- BASF SE

- DAW SE

- Hempel A/S

- Berger Paints India Limited

- Tikkurila Oyj

*- List not Exhaustive