Waterborne Coating Additives Market Size Expansion Driven by Bio-Based Chemistry and High-Performance Formulation Demand

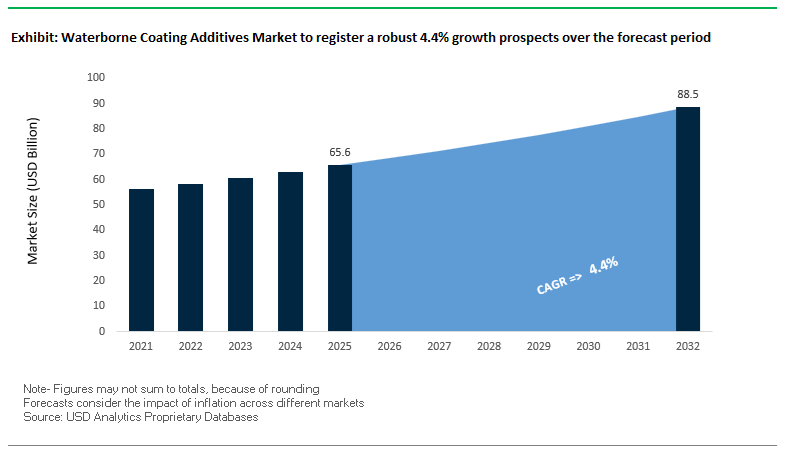

The global Waterborne Coating Additives Market reached a valuation of $65.6 billion in 2025 and is projected to grow at a CAGR of 4.4% from 2025 to 2032, reaching $88.7 billion by 2032. This growth is being fueled by the increasing adoption of low-VOC waterborne coating systems across architectural, automotive, packaging, and industrial applications, where additives play a critical role in enhancing dispersion, rheology control, surface wetting, adhesion, and durability.

A key structural driver of this market is the transition toward advanced formulation chemistry, where additives are no longer auxiliary components but performance-critical enablers. Waterborne coatings inherently require highly optimized additive systems to overcome challenges such as lower film formation efficiency, sensitivity to humidity, and substrate compatibility issues. As a result, demand is surging for next-generation dispersants, defoamers, rheology modifiers, slip agents, and wetting agents that enable superior coating performance while maintaining environmental compliance.

Sustainability is a defining force shaping market evolution. Manufacturers are increasingly focusing on bio-attributed additives, renewable waxes, and mass-balance certified materials to reduce carbon footprints and align with global decarbonization targets. The integration of ISCC PLUS-certified production processes, circular feedstocks, and recyclable raw materials is transforming the value chain, particularly in sectors such as food packaging, construction, and electronics, where regulatory scrutiny is intensifying.

Additionally, the rise of digital printing, electric vehicles (EVs), and smart infrastructure is creating demand for highly specialized additive systems that support precision coatings, enhanced pigment dispersion, and multifunctional properties.

Market Analysis: Sustainability Certification, Advanced Dispersant Innovation, and Capacity Expansion Reshaping Market Dynamics

The Waterborne Coating Additives Market is witnessing rapid transformation driven by sustainability certifications, technological breakthroughs, and strategic capacity expansions, redefining competitive positioning across the value chain. A landmark development is Arkema’s achievement of ISCC PLUS certification across over 70% of its global coating additive sites (January 2026), enabling the company to offer a broad portfolio of bio-attributed additives with at least 20% lower product carbon footprint (PCF). This milestone highlights the increasing importance of traceability, mass balance approaches, and low-carbon material sourcing in additive manufacturing.

Regulatory-driven innovation is also shaping product development. In February 2026, Clariant secured EU approval for its renewable rice bran wax additives, designed for food-contact waterborne coatings. These additives provide critical functionalities such as slip and anti-blocking performance, while meeting stringent safety standards, reinforcing the growing intersection between sustainability and regulatory compliance in packaging applications. Simultaneously, Clariant’s joint venture with FUHUA is accelerating the development of halogen-free flame retardant additives, targeting construction and electronics sectors with enhanced environmental safety requirements.

Technological innovation in dispersants and process chemistry is another key growth lever. Lubrizol’s expansion of Solsperse™ hyperdispersant capacity (September 2025) and the launch of Solsperse™ W60 (February 2025) address the rising need for faster pigment wetting, higher color strength, and formulation efficiency in waterborne systems. Complementing this, Evonik’s AERODISP® portfolio (May 2025) introduces advanced silica- and alumina-based dispersions designed for inkjet primer applications, supporting the transition toward digital printing technologies with enhanced resolution and color sharpness.

Process innovation is further enhancing sustainability and efficiency. Lubrizol’s LED-based chlorination breakthrough (February 2026) represents a significant step toward energy-efficient polymer additive production, aligning with broader industry goals of reducing manufacturing energy intensity. Meanwhile, BYK’s global price adjustment (February 2026) reflects ongoing cost pressures related to supply chain volatility, regulatory complexity, and rising R&D investments, signaling a shift toward value-based pricing strategies in the additives segment.

Digitalization is emerging as a strategic enabler. Arkema’s launch of a unified digital platform (2025–2026) provides customers with integrated access to technical data, mass balance certifications, and formulation guidance, streamlining additive selection for high-growth sectors such as e-mobility and data centers. Additionally, BASF’s “Driving the Proxy” collection showcases the role of advanced additive systems in enabling next-generation color effects, utilizing specialized rheology and wetting agents to achieve multidimensional finishes.

Market Trend: EPA DfE Certification Accelerating APEO-Free Additives Transition in Waterborne Coatings Market

The increasing influence of the U.S. EPA Design for the Environment certification is significantly reshaping the waterborne coating additives market, particularly through the enforced phase-out of alkylphenol ethoxylates in 2026. The Safer Chemical Ingredients List is now acting as a de facto regulatory benchmark, compelling manufacturers to eliminate APEO-based surfactants such as nonylphenol ethoxylates from architectural and industrial coatings formulations.

Under the 2026 DfE framework, surfactants must achieve “Green Circle” or “Yellow Triangle” classification, ensuring the use of environmentally safer alternatives. This is driving widespread adoption of alcohol ethoxylates and alkyl glucosides, which demonstrate biodegradation rates exceeding 60% within 28 days under OECD standards. These bio-based and biodegradable surfactants are becoming essential components in sustainable coating additives and eco-friendly paint formulations.

Technical audits in 2026 reveal that approximately 25% of legacy dispersants still contain trace levels of APEOs, placing a significant portion of the market at risk. Manufacturers that fail to reformulate by the second quarter of 2026 are increasingly excluded from federal procurement programs and Green Seal-certified tenders. This is accelerating innovation in non-toxic coating additives and strengthening the competitive advantage of compliant suppliers in the global waterborne coatings additives industry.

Market Trend: EU REACH Annex XVII Driving Isothiazolinone-Free and Preservative-Free Coating Additives

The enforcement of stricter regulations under EU REACH Annex XVII is transforming preservative chemistry in the waterborne coating additives market. As part of the European Chemicals Agency’s One Substance, One Assessment framework, new concentration limits for isothiazolinones such as methylisothiazolinone and benzisothiazolinone are driving a shift toward safer biocidal systems.

For consumer-facing coatings, the methylisothiazolinone limit remains capped at 15 ppm, while new 2026 updates mandate hazard labeling for benzisothiazolinone concentrations exceeding 50 ppm. These requirements are accelerating the transition toward isothiazolinone-free additives and preservative-free high-pH silicate coatings, particularly in residential and decorative applications.

To maintain antimicrobial performance while meeting regulatory constraints, manufacturers are increasingly utilizing alternative biocidal technologies such as silver-ion encapsulation and zinc pyrithione synergy. These advanced systems enable coatings to achieve ISO 22196 antimicrobial efficacy standards without relying on traditional preservatives, reinforcing the demand for safe and compliant coating additives in Europe and other regulated markets.

Market Opportunity: VOC-Free and APEO-Free Dispersing Additives Enabling High-Performance Pigment Stabilization

The growing demand for high-performance pigments, including organic pigments and carbon black dispersions, is creating strong opportunities for VOC-free and APEO-free wetting and dispersing additives. These next-generation additives are designed to stabilize complex pigment systems without contributing to the overall VOC content of waterborne coatings.

Modern dispersing agents are leveraging advanced molecular architectures based on high-molecular-weight polyurethanes and acrylic block copolymers engineered through controlled polymerization techniques such as ATRP. These structures provide effective steric stabilization, eliminating the need for traditional APEO-based surfactants while enhancing dispersion quality and long-term stability.

In terms of efficiency, these additives deliver significant process improvements by reducing grind viscosity by 20% to 30%. This enables higher pigment loading and shorter mill-base processing times, contributing to reduced energy consumption and lower carbon emissions in coating manufacturing.

Premium-grade dispersing additives are also achieving a 0.0 g/L VOC profile as measured by ASTM D6886 and SCAQMD Method 313, making them essential for coatings targeting ultra-low VOC thresholds of 5 g/L or lower. This positions VOC-free dispersants as a critical component in next-generation sustainable coatings formulations.

Market Opportunity: Zero-VOC Coalescing Agents Advancing Low-Temperature Film Formation in Waterborne Coatings

The development of zero-VOC coalescing agents represents a key growth opportunity in the waterborne coating additives market, particularly for applications requiring consistent film formation under challenging environmental conditions. As VOC limits continue to tighten below 50 g/L, traditional coalescents are being replaced by high-boiling-point specialty esters designed for enhanced performance and regulatory compliance.

These advanced coalescing agents, with boiling points exceeding 280°C, enable acrylic emulsions to form continuous films at temperatures as low as 3°C to 5°C and relative humidity levels up to 85%. This capability is critical for maintaining coating performance in early-season construction and outdoor applications where temperature and humidity conditions are suboptimal.

Unlike legacy plasticizers, modern coalescing additives are engineered to either volatilize without contributing to VOC content or chemically integrate into the polymer matrix. This results in improved coating hardness, with up to a 15% increase in Koenig hardness within seven days compared to traditional low-VOC systems.

Additionally, these additives significantly reduce the minimum film formation temperature of high glass transition temperature resins, lowering it from approximately 25°C to below 2°C at low loading levels of 4% to 6% based on resin solids. This prevents defects such as mud cracking and enhances the durability and aesthetic quality of waterborne coatings, supporting their adoption in demanding architectural and industrial applications.

Waterborne Coating Additives Market Share and Segmentation Insights

Rheology Modifiers Lead with 22.8% Share as Critical Enablers of Waterborne Coating Performance

The rheology modifiers segment dominates the waterborne coating additives market with a 22.8% market share in 2025, reflecting its essential role in optimizing paint application properties and formulation stability. In the waterborne coatings additives and specialty chemicals market, rheology modifiers such as HEUR (hydrophobically modified ethoxylated urethanes), HASE (hydrophobically modified alkali swellable emulsions), and cellulose ethers are crucial for controlling viscosity, sag resistance, spatter, and leveling behavior. These additives effectively replicate and enhance the flow characteristics traditionally achieved with solvent-based systems, enabling the shift toward low-VOC and environmentally friendly coatings. Their widespread use across architectural paints, industrial coatings, automotive finishes, and wood coatings highlights their versatility and indispensability. As waterborne technologies continue to replace solvent-borne formulations, rheology modifiers remain foundational to achieving performance consistency, ease of application, and high-quality finishes, reinforcing their leadership in the global waterborne coating additives market.

Direct Sales Channel Leads with 52.4% Share Through Technical Partnerships and Custom Additive Solutions

The direct sales segment dominates the waterborne coating additives market by sales channel with a 52.4% market share in 2025, driven by the need for close technical collaboration between additive suppliers and coating formulators. Within the specialty chemicals and paint formulation market, leading companies such as BYK, Evonik, Dow, BASF, and Elementis work directly with manufacturers to optimize rheology, wetting, dispersing, and defoaming performance for specific waterborne systems. This direct engagement enables the development of custom additive blends tailored to precise formulation requirements, including VOC compliance, gloss levels, drying time, and substrate compatibility. Additionally, direct relationships ensure faster innovation cycles, technical support, and consistent product performance, which are critical in high-performance coatings applications. As demand increases for advanced, sustainable, and application-specific coating solutions, direct sales continue to dominate the global waterborne coating additives supply chain, reinforcing their strategic importance in the market.

Competitive Landscape Analysis of the Waterborne Coating Additives Market

BYK Leads Dispersing Additives Innovation with Sustainable and High-Performance Solutions

BYK (ALTANA AG) is a dominant force in the waterborne coating additives market, particularly in the wetting and dispersing additives segment. In May 2026, the company implemented a global price increase of 18% to 30% to sustain high R&D investments amid rising raw material costs. Its breakthrough AQUACER 492, inspired by lotus leaf superhydrophobicity, has set a benchmark for water-based wax additives in textile and architectural coatings. BYK is also expanding its SCONA functional polymer line, improving compatibility in recycled plastic-based coating systems. Its DISPERBYK series, optimized for LED-UV and electron beam curing, reinforces its leadership in advanced high-performance waterborne additive technologies.

Evonik Advances AI-Driven Additives and High-Performance Defoamer Technologies

Evonik Industries AG is strengthening its position in the waterborne coating additives market through innovation in specialty additives and digital formulation tools. The company reported a 12% volume surge in waterborne applications within its Specialty Additives division, contributing to its €1.7–€2.0 billion EBITDA target for 2026. Its TEGO® product line leads the defoamer and deaerator segment, with the introduction of a label-free silicone surfactant that eliminates surface defects in high-speed coating lines. Evonik’s AI-powered digital twin formulation tools reduce R&D cycles by up to 40%. The company is also targeting eMobility coatings, offering additives with high dielectric strength and moisture resistance for EV battery insulation.

BASF Expands Sustainable Additives Portfolio with Mass-Balance Dispersions

BASF SE maintains a leading 17% share in the waterborne coating additives market, supported by its strong vertical integration in acrylic and polyurethane dispersions. In 2026, BASF expanded its Joncryl® portfolio with mass-balance certified additives, enabling up to 60% reduction in fossil carbon footprint for coating manufacturers. Its high-efficiency rheology modifiers improve production efficiency by 20% for architectural coatings. BASF is also transitioning its Efka® and Hydropalat® lines to PFAS-free and APEO-free formulations ahead of regulatory deadlines. These initiatives position BASF as a leader in sustainable coating additives and high-performance formulation technologies.

Dow Strengthens Circular Additives and Rheology Modifier Innovation

Dow Inc. is a key player in the waterborne coating additives market, focusing on sustainability and performance-driven solutions. Through its Renuva™ circularity platform, Dow utilizes recycled polyols to create additives that reduce CO₂ emissions by 54%. Its 2026 introduction of HEUR rheology modifiers enhances spatter resistance and leveling in premium interior paints. Dow also dominates the traffic and infrastructure coatings segment, offering waterborne additives that enable 30% faster drying times for road markings. With one of the world’s largest emulsion polymer networks, Dow ensures reliable global supply and just-in-time delivery, strengthening its leadership in coating additive manufacturing and distribution.

Arkema Advances Bio-Based Additives and High-Performance Polymer Solutions

Arkema (Coatex / Coating Solutions) is advancing in the waterborne coating additives market through its focus on specialty materials and high-performance polymers. In 2026, the company showcased SNAP® and NEOCAR® acrylic emulsions along with Coatex rheology modifiers, some containing up to 93% bio-based content. Arkema’s expertise in aqueous PVDF dispersions (Kynar Aquatec®) provides over 20 years of weather resistance for architectural coatings. Its Crayvallac® surface additives include advanced polyamide-based waxes that enhance scratch and mar resistance in furniture coatings. With its transition to a pure specialty materials company, Arkema is well-positioned in sustainable and high-performance waterborne additive technologies.

China’s Shift Toward High-Performance Additives in Waterborne Coatings

China is rapidly transitioning from volume-based production to high-value specialty segments within the waterborne coating additives market. This shift is strongly supported by environmental policies such as the GB 30981-2020 standards and the broader “Blue Sky” defense plan, which are accelerating the adoption of water-based technologies across industrial applications. Regulatory frameworks like HJ 1179-2021 now mandate water-based or high-solids coatings for new facilities, significantly boosting the consumption of additives such as wetting agents and dispersants.

Industrial expansion is reinforcing this transformation, with BASF launching a dedicated dispersant production line in Nanjing to meet rising demand for pigment stabilization in waterborne coatings. Innovation is also accelerating, particularly in nanotechnology, where nano-silica additives are being developed to enhance scratch resistance and performance parity with solvent-based systems. Large-scale infrastructure initiatives, including the deployment of 5G base stations, are driving demand for advanced additive packages such as deaerators for high-speed applications. Additionally, the introduction of China Environmental Labelling (CEC) standards is pushing manufacturers toward APEO-free surfactants, further strengthening the country’s leadership in sustainable additive technologies.

United States: Clean-Label Innovation and Regulatory-Driven Additive Demand

The United States waterborne coating additives market is experiencing a “clean-label” transformation, characterized by the elimination of hazardous chemicals and increased adoption of bio-based alternatives. Regulatory pressure is a key driver, with leading manufacturers removing PFAS compounds from their portfolios to comply with evolving EPA and state-level regulations. Additionally, the EPA’s strategic water program is accelerating demand for additives that enhance coating durability and prevent leaching in water-contact applications.

Innovation in sustainable additives is gaining momentum, with the introduction of bio-based defoamers and plant-derived materials designed to meet green building certifications such as LEED. Infrastructure investments under the IIJA are further fueling demand for rheology modifiers that enable thick-film application in corrosion protection systems. Regulatory tightening by CARB is also increasing reliance on advanced wetting agents to maintain performance under low-VOC conditions. The aerospace sector is contributing to growth, with the Department of Defense specifying waterborne epoxy systems incorporating advanced flow additives to reduce hazardous emissions in maintenance operations.

Germany: Circular Economy Leadership and Smart Additive Technologies

Germany remains a global leader in advanced waterborne coating additives, driven by its strong emphasis on sustainability and technical precision. The market is increasingly aligned with circular economy principles, with manufacturers transitioning to bio-based raw materials such as ethyl acrylate for rheology modifiers. Stringent environmental regulations, including the Industrial Emissions Directive (IED), are accelerating the shift toward waterborne technologies, thereby increasing the demand for high-performance additives.

Innovation is particularly strong in niche applications such as hydrogen infrastructure, where specialized additives are being developed to ensure zero-porosity coatings and prevent material degradation. The expansion of renewable energy projects is also driving demand for UV-stabilizing additives in wind turbine coatings. Germany’s leadership in Industry 4.0 is evident in the integration of AI-enabled systems for precise additive dosing, reducing waste and improving efficiency. Furthermore, ongoing compliance with REACH regulations is prompting reformulation of additives to eliminate microplastics and environmentally harmful compounds, reinforcing the country’s position at the forefront of sustainable coating technologies.

India: Infrastructure Growth and Localization of Waterborne Additives

India is emerging as a high-growth market for waterborne coating additives, driven by infrastructure expansion and increasing domestic manufacturing capabilities. Strategic partnerships, such as the renewed collaboration between PPG and Asian Paints, are focusing on localizing the production of additives for automotive and industrial applications. Capacity expansion initiatives, including advanced coating facilities, are further strengthening the domestic supply chain for high-performance additives.

Government-led infrastructure programs are key demand drivers. The Pradhan Mantri Awas Yojana is generating consistent demand for dispersants, thickeners, and other additives used in large-scale production of water-based emulsions. Additionally, increased investments in oil and gas pipeline infrastructure are boosting demand for anti-corrosive additives designed for harsh environments. The rise of electric vehicle manufacturing is also contributing to growth, with increasing demand for additives used in thermal management coatings. Consumer trends are shifting toward premium finishes, with growing use of wax-based additives that enhance stain resistance and ease of cleaning in interior applications.

South Korea: High-Tech Functional Additives and Green Building Compliance

South Korea is positioning itself as a leader in high-performance, functional waterborne coating additives, particularly in moisture protection and antimicrobial technologies. Regulatory frameworks such as G-SEED are mandating the use of low-VOC additives in new residential and commercial developments, significantly boosting demand for advanced wetting and dispersing agents.

Technological innovation is a key differentiator in the South Korean market. Companies are developing nano-enhanced additives to improve moisture resistance and thermal insulation in coatings designed for humid climates. Government initiatives supporting carbon neutrality are encouraging small and medium enterprises to transition toward water-based production, increasing demand for sophisticated defoamer systems. High levels of R&D investment are enabling the development of hybrid antimicrobial additives, particularly for healthcare infrastructure upgrades. Additionally, the integration of conductive additives in smart building applications is opening new opportunities in electrostatic discharge management, reflecting the country’s focus on advanced, multifunctional coating solutions.

Brazil: Regulatory Transformation and Regional Expansion of Waterborne Additives

Brazil continues to lead the Latin American waterborne coating additives market, supported by regulatory reforms and strong domestic demand. Recent legislation aimed at reducing lead content in paints is accelerating the shift toward additive-stabilized waterborne systems. Industry initiatives such as the Abrafati Quality Program have further strengthened product standards, ensuring widespread adoption of high-quality dispersing agents in architectural coatings.

Market consolidation is also shaping the competitive landscape, with major acquisitions streamlining supply chains and enhancing regional distribution networks. Innovation in Brazil is focused on developing additives that can withstand extreme environmental conditions, including high UV radiation and humidity. This includes the use of HALS (Hindered Amine Light Stabilizers) to improve durability in outdoor applications. Additionally, niche applications such as street art preservation are driving the development of specialized additive solutions. The automotive refinish sector is also transitioning toward waterborne systems, increasing demand for advanced additive technologies that enhance coating performance and worker safety.

Waterborne Coating Additives Market Report Scope

Waterborne Coating Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$65.6 Billion

|

|

Market Size (2032)

|

$88.7 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Type (Rheology Modifiers, Wetting and Dispersing Agents, Defoamers and Deaerators, Flow and Leveling Additives, Surface Control Additives, Light Stabilizers, Biocides and Preservatives, Adhesion Promoters, Coalescents and Co-solvents, Specialty Additives), By Composition (Synthetic Additives, Bio-based, Nano-based Additives), By Formulation Technology (Emulsion-based Additives, Water-soluble Additives, Colloidal Dispersions), By Application (Architectural Coatings, Industrial Coatings, Automotive and Transportation Coatings, Printing Inks, Packaging Coatings), By End-User Industry (Building and Construction, Automotive and Transportation, Furniture and Woodworking, Packaging and Graphic Arts, Electronics and Electrical, Aerospace and Defense), By Sales Channel (Direct Sales, Specialized Chemical Distributors, Technical Wholesalers, Online B2B Marketplaces)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, ALTANA AG, Dow Inc., Arkema, Lubrizol Corporation, Clariant AG, Ashland Inc., Elementis PLC, Eastman Chemical Company, Nouryon, allnex GmbH, iGM Resins B.V., Münzing Chemie GmbH, Croda International Plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Waterborne Coating Additives Market Segmentation

By Type

- Rheology Modifiers

- Wetting and Dispersing Agents

- Defoamers and Deaerators

- Flow and Leveling Additives

- Surface Control Additives

- Light Stabilizers

- Biocides and Preservatives

- Adhesion Promoters

- Coalescents and Co-solvents

- Specialty Additives

By Composition

- Synthetic Additives

- Bio-based

- Nano-based Additives

By Formulation Technology

- Emulsion-based Additives

- Water-soluble Additives

- Colloidal Dispersions

By Application

- Architectural Coatings

- Industrial Coatings

- Automotive and Transportation Coatings

- Printing Inks

- Packaging Coatings

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Furniture and Woodworking

- Packaging and Graphic Arts

- Electronics and Electrical

- Aerospace and Defense

By Sales Channel

- Direct Sales

- Specialized Chemical Distributors

- Technical Wholesalers

- Online B2B Marketplaces

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Waterborne Coating Additives Industry

- BASF SE

- Evonik Industries AG

- ALTANA AG

- Dow Inc.

- Arkema

- Lubrizol Corporation

- Clariant AG

- Ashland Inc.

- Elementis PLC

- Eastman Chemical Company

- Nouryon

- allnex GMBH

- iGM Resins B.V.

- Münzing Chemie GmbH

- Croda International Plc

*- List not Exhaustive