The Global Welding Sticks (Shielded Metal Arc Welding – SMAW Electrodes) Market is projected to grow from USD 5.7 billion in 2025 to USD 8.8 billion by 2034, at a CAGR of 4.9%, underscoring the continued structural relevance of stick welding in field-intensive fabrication and repair environments. Despite the proliferation of automated and wire-fed welding processes, SMAW electrodes retain a durable position in global welding spend due to their portability, robustness in uncontrolled conditions, and low capital dependence. Market demand is therefore less cyclical than other welding consumables and is closely tied to infrastructure build–out, asset maintenance cycles, and regulatory-driven repair activity.

Construction and infrastructure remain foundational demand anchors, particularly in bridges, pipelines, structural steel, rail, and heavy civil projects, where outdoor work, power variability, and joint condition tolerance favor stick electrodes over gas-shielded alternatives. Leading manufacturers such as Lincoln Electric, ESAB, voestalpine Böhler Welding, Kobe Steel, and Ador Welding continue to position SMAW portfolios around all-position usability, arc stability, and slag detachability, directly addressing productivity constraints in field welding. Carbon steel electrodes (E6013, E7018) remain volume drivers, but value growth is increasingly concentrated in low-hydrogen and alloyed grades specified for higher integrity joints.

A second structural pillar is the expanding maintenance, repair, and overhaul (MRO) cycle across oil & gas, power generation, mining, and process industries. Asset owners are extending service life rather than accelerating greenfield replacement, driving recurring demand for electrodes used in on-site repairs, hardfacing, and crack remediation. Industry procurement patterns increasingly emphasize consistent hydrogen control, moisture resistance, and re-drying stability, as weld quality failures carry disproportionate downtime and safety risk. Low-hydrogen electrodes with controlled diffusible hydrogen levels are therefore gaining share in pressure vessels, boilers, and high-temperature service environments.

The market is also experiencing a premiumization shift toward heat-resistant, creep-resistant, and corrosion-resistant alloy electrodes, reflecting tighter codes and harsher operating conditions. Electrodes designed for Cr-Mo steels, low-alloy steels, and dissimilar metal welding are seeing stronger uptake as operators retrofit aging assets to meet updated performance and safety standards. Manufacturers are responding with improved flux formulations that enhance arc control, slag coverage, and mechanical properties, while also improving shelf life in humid climates—an important differentiator in emerging markets.

Market Size Outlook, 2021-2034.png)

Market Analysis: 2026 momentum—automation tie-ins, tariff headwinds, AI R&D, and workforce rebuild

Through 2025, welding sticks benefited from ecosystem advances in automation, digitalization, and training even as raw-material dynamics tightened. In October 2025, voestalpine Böhler Welding concluded multiple stops of its Perfect Weld Seam Tour 2025 in Kapfenberg, Austria, launching its CORE series inverters for MMA and running live stick demonstrations that link power sources, procedures, and consumables for quality assurance. In September 2025, Lincoln Electric previewed new FABTECH releases—including the LT-10D SAW tractor and fresh power sources—underscoring how automation platforms are curated alongside full electrode portfolios to raise productivity and bead consistency.

Portfolio scale and channel reach intensified with ESAB’s (August 2025) signing of EWM, complementing earlier gas-control deals to knit heavy industrial/robotic equipment with stick electrodes in integrated workflows. That same month, Miller Electric and Hobart® Filler Metals showcased innovations at FABTECH—such as FABCOR® Element™ XP metal-cored wire—illustrating how parallel process gains in GMAW/FCAW still catalyze SMAW consumable demand when plants standardize filler metals across mixed processes. Macro inputs were mixed: Air Liquide (July 2025) reported US equipment softness in Industrial Merchant but noted a +2.6% price effect H1 2025; tariff hikes (April 2025) on imported metals/minerals raised costs for specialized electrodes, prompting scrap recycling investment and JV sourcing for supply security.

Digital and human-capital levers supported throughput. voestalpine Böhler (July 2025) extended its tour into CEE markets, promoting weldNet® Process Manager; in May 2025, TU Graz and voestalpine launched the ‘Spark Science Center’ to apply AI to weld optimization. Miller (May 2025) introduced Copilot™ Builder™ collaborative welding, widening access to automation and driving demand for consistent, code-qualified sticks. Workforce constraints eased as March 2025 apprenticeship initiatives expanded the certified welder pool—lifting SMAW utilization across job sites where flexibility, fit-up tolerance, and all-position capability remain decisive.

Welding Sticks (SMAW Electrodes) Market Share Insights, 2025-2034

Market Share by Flux Coating Type

The Rutile-coated welding sticks segment dominates the global market, holding approximately 37.3% of the projected 2025 share, underlining its critical role in general-purpose fabrication, construction, and repair welding. Rutile electrodes, typified by grades such as E6013, are widely adopted for their user-friendly arc characteristics, smooth weld bead appearance, and low spatter levels, making them the preferred choice for both professional and semi-skilled welders. Their ability to operate efficiently on AC or DC power sources enhances field versatility, particularly in regions with fluctuating power conditions. This ease of operation and adaptability makes rutile-coated electrodes indispensable for infrastructure, manufacturing, and light fabrication sectors, driving consistent global demand. Moreover, as emerging economies ramp up steel fabrication and construction activities, the popularity of rutile electrodes continues to rise due to their low cost, reliability, and minimal post-weld finishing requirements.

The Basic or Low-Hydrogen electrodes (e.g., E7018) form the second most significant category, widely regarded for their superior mechanical properties, crack resistance, and weld integrity. These electrodes dominate in critical structural welding applications—such as bridges, offshore platforms, and heavy industrial machinery—where toughness and hydrogen control are essential to prevent weld failures under stress or impact. Their prevalence is further reinforced by strict quality standards and welding codes in industries like oil & gas, power generation, and shipbuilding, where only certified low-hydrogen consumables are permitted. Meanwhile, Cellulosic-coated electrodes (e.g., E6010, E7010) represent a vital niche, particularly in pipeline construction and repair, due to their deep penetration capability and high deposition rates in vertical and overhead positions. These attributes make them indispensable for cross-country pipeline welding, where speed and weld penetration outweigh appearance.

Iron Powder electrodes, another high-performance variant, are gaining traction in shipbuilding and heavy fabrication industries for their superior deposition rates and improved efficiency. Their growing use aligns with the industry’s focus on reducing welding time and increasing throughput without compromising mechanical performance. The “Others” segment, comprising specialized acid, oxidizing, and hardfacing electrodes, caters to maintenance, repair, and custom alloy joining applications, such as welding cast iron, stainless steel, or wear-resistant overlays.

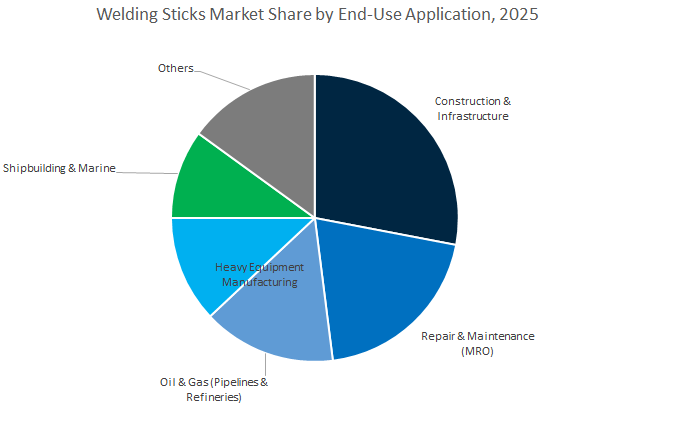

Market Share by End-Use Industry

The construction and infrastructure sector remains the leading end-use industry, accounting for approximately 26.8% of the global welding sticks market in 2025, driven by accelerating urbanization, steel-intensive infrastructure projects, and the widespread use of shielded metal arc welding (SMAW) in on-site fabrication and erection. Welding sticks, particularly rutile and basic electrodes, are indispensable in steel structure assembly, bridges, pipelines, and rebar joining, where reliability, portability, and adaptability to outdoor environments are essential. As global infrastructure spending rises—particularly in Asia-Pacific, the Middle East, and Latin America—demand for field-welding consumables continues to grow. The Repair and Maintenance (MRO) segment complements this dominance, serving as the market’s most stable and recurring revenue stream. SMAW’s simplicity and independence from complex machinery make it ideal for equipment maintenance, plant repair, and emergency fixes in industries ranging from mining and power to agriculture and railways.

Oil & Gas, Heavy Equipment Manufacturing, and Shipbuilding represent the high-value core of the industrial welding sector. In the Oil & Gas industry, cellulosic and low-hydrogen electrodes are the standard for pipeline construction, pressure vessel welding, and refinery maintenance, ensuring compliance with stringent safety and durability standards. The Shipbuilding and Marine segment relies heavily on iron powder and basic-coated electrodes for structural hull welding and underwater maintenance, where corrosion resistance and mechanical performance under load are critical. Similarly, Heavy Equipment Manufacturing, including machinery and steel fabrication, utilizes a broad range of electrodes for components exposed to high mechanical stress, thermal cycling, and vibration, reinforcing SMAW’s position as a durable, cost-efficient joining solution.

Market Trend 1: Strategic Shift to Low-Hydrogen, High-Toughness Electrodes for Critical Infrastructure and Offshore Applications

The rising focus on structural integrity and fracture control in large-scale infrastructure and offshore wind projects is driving the accelerated adoption of low-hydrogen welding sticks. These specialized electrodes—classified under AWS H4 and H8 categories—are designed to meet stringent standards like AASHTO/AWS D1.5M/D1.5, which mandates a maximum hydrogen content of 4–8 mL per 100g of weld metal. The strict requirement ensures high resistance to hydrogen-induced cracking in fracture-critical components such as bridge girders, offshore platforms, and wind turbine towers.

In extreme environments such as Arctic pipelines and deep-sea foundations, high-strength low-alloy (HSLA) consumables like E9018-G and E11018-M are being engineered to deliver Charpy V-Notch (CVN) impact toughness values exceeding 27 Joules at −45°C, ensuring mechanical reliability under cryogenic and sub-zero conditions. The performance benchmark drives the essential role of high-toughness electrodes in global energy infrastructure expansion.

In addition, electrode formulations incorporating Nickel (Ni) and Molybdenum (Mo)—notably in E8018-C3 electrodes with 1% Ni—enhance low-temperature ductility, tensile strength, and creep resistance, essential for pressure vessel and power generation fabrication. As governments continue investing in bridge retrofits, LNG terminals, and offshore platforms, premium low-hydrogen, high-alloy electrodes are becoming indispensable for safety, durability, and long-term weld performance.

Market Trend 2: Reformulation to Eliminate Hazardous Materials in Response to Global Safety and Environmental Regulations

The welding sticks industry is undergoing a pivotal transformation driven by occupational health standards and environmental regulations that target hazardous substances like hexavalent chromium (Cr(VI)) and volatile welding fumes. The U.S. OSHA standard limits Cr(VI) exposure to 5 μg/m³ (8-hour TWA)—a dramatic reduction from earlier limits—while the EU has implemented comparable restrictions under the REACH framework, enforcing complete chemical traceability for all consumable components.

To meet these requirements, manufacturers are advancing low-fume and chromium-free electrode coatings through nanotechnology-enabled formulations. Academic trials using nano-titania (TiO₂) and nano-alumina flux additives have achieved a 40%–76% reduction in Cr(VI) generation, proving that effective fume suppression can coexist with mechanical weld performance. These innovations are especially critical in stainless steel and hardfacing electrodes, where chromium oxidation has historically been unavoidable.

The REACH regulatory framework also mandates full documentation of flux, binder, and coating ingredients, pushing suppliers toward eco-friendly formulations using benign mineral binders and high-purity alloy powders. The shift aligns with the industry’s broader sustainability goals and reinforces compliance with global environmental protection standards, enabling safer production environments while reducing post-weld exposure risks.

Market Opportunity 1: Development of Rapid-Alloy-Specific Electrodes for On-Site Maintenance and Hardfacing

As heavy machinery in mining, construction, cement, and power generation faces increasing wear, the global market for hardfacing and repair welding electrodes is expanding rapidly. Manufacturers are capitalizing on the demand by designing rapid-deposition, alloy-specific welding sticks that enable on-site maintenance without complex preheating or post-weld heat treatment processes.

Advanced hardfacing electrodes with high chromium carbide content—typically delivering hardness values between 60–65 HRC—are being deployed for crusher jaws, conveyor screws, and cement mill rollers. These materials drastically extend equipment life, reducing downtime and component replacement frequency.

Similarly, austenitic manganese steel electrodes (EFeMn-A/B/C) are used for high-impact components such as rail crossings, shovel buckets, and excavator teeth. Their unique work-hardening capability increases surface hardness from 200 HB to 450–500 HB during service, ensuring superior wear performance under repetitive impact.

The segment represents a lucrative opportunity for manufacturers to expand into rapid-repair consumables for mobile maintenance units. The focus on cost efficiency, downtime reduction, and durability continues to fuel innovation in specialized wear-resistant and hardfacing electrode technologies globally.

Market Opportunity 2: Engineering of Low-Power-Consumption Electrodes for Renewable Energy Project Construction

The shift toward remote renewable energy infrastructure, including wind farms, solar plants, and hydro installations, is creating a strong market pull for energy-efficient welding sticks optimized for low-amperage operation. These specialized electrodes enable welding in power-constrained environments where portable or generator-based setups are prevalent.

For example, a 160-Amp SMAW setup operating at 70% efficiency on a 220V generator requires approximately 50.3 kW of sustained power, highlighting the significant fuel and energy load typical of remote construction projects. To address the, manufacturers are developing low-power-consumption welding electrodes with enhanced arc stability and deeper penetration at reduced amperage levels (e.g., 90A for 1/8” E7018 rods).

These innovations not only conserve fuel but also enable lightweight, portable welding systems suited for off-grid renewable energy construction in remote terrains. Additionally, advancements in coating composition—allowing for consistent slag detachment and arc control at lower voltages—support field assembly of turbine towers, transmission pylons, and solar frame structures.

The welding sticks market is shaped by global leaders integrating materials science, automation, and service networks. Differentiation centers on low-hydrogen alloy design, code qualifications, application engineering, and supply-chain resilience (recycling, local melts, and multi-sourcing) to counter metal price/tariff volatility.

Overview (market structure): Tier-1 OEMs—Lincoln Electric, ESAB, Air Liquide, Hobart (ITW), and voestalpine Böhler Welding—pair broad SMAW electrode catalogs with equipment, software, and training, enabling cradle-to-bead control and faster PQR/WPS qualification in construction, energy, shipbuilding, and heavy fabrication.

Strategic focus (2025): outgrow the market via innovation, automation, additive and software. The company supplies a full range of SMAW electrodes, including super-duplex solutions (e.g., nitrogen-over-alloyed consumables) engineered for SCC-resistant joints in process pipework. With 50% of 2024 equipment sales from new products, Lincoln’s materials science and application expertise “The Welding Expert™” supports high-deposition sticks tuned for pipeline, structural steel, and power generation procedures.

M&A cadence: two Gas Control deals and the signing of EWM expand ESAB’s heavy-industrial and robotic footprint, deepening linkages between equipment and consumables (including low-hydrogen SMAW). A record Core adj. EBITDA margin of 20.4% (Q2 2025) showcases operating leverage via the EBX system. Global reach (150 countries) and multi-brand stick lines position ESAB strongly in shipbuilding, oil & gas, and power, where reliability and procedure repeatability are critical.

Integration advantage: Industrial gases plus hardgoods place Air Liquide to deliver complete welding solutions alongside third-party electrodes. H1 2025 Gas & Services revenue grew +2.9% (Americas) and +2.1% (Asia), reflecting solid industrial activity. A new ASU investment in Japan (2025) targets energy transition and semiconductors—sectors demanding high-purity gases and high-spec electrodes—while +9.6% recurring net profit growth (H1 2025) supports continued capex in industrial supply chains.

Recent filler-metal innovation: FabCOR® Elevate™ metal-cored wire boosts deposition 10% vs other metal-cored and 30% vs solid, complementing SMAW lanes. Hobart’s E6010 (Hobart® 610) addresses pipe and construction all-position work, while low-hydrogen/low-alloy sticks like Hoballoy® 11018M (high-tensile steels) and 7018-C3L (ammonia tanks) target crack resistance and notch toughness. Backed by ITW scale, Hobart aligns metallurgy with code-critical applications.

Digitalization: weldNet® process tools and the Perfect Weld Seam Tour 2025 demonstrate end-to-end support for parameter control and QA. In September 2025, the CORE series for MMA debuted in Kapfenberg, enhancing portability and field performance—driving paired demand for Böhler electrodes. The TU Graz ‘Spark Science Center’ (May 2025) advances AI-supported weld optimization, while European roadshows expand distributor enablement and customer trials across CEE markets.

Welding Sticks (SMAW Electrodes) Market Report Scope

Welding Sticks (SMAW Electrodes) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.7 Billion

|

|

Market Size (2034)

|

$8.8 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Product Type (Carbon Steel Electrode, Low Alloy Steel Electrode, Stainless Steel Electrode, Heat-Resistant Steel Electrode, Cast Iron Electrode, Others), By Coating Type (Rutile (High Titania), Basic (Low Hydrogen), Cellulosic), By End-Use Industry (Building & Construction, Automotive & Transportation, Marine & Shipbuilding, Oil & Gas/Energy, Repair & Maintenance

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Lincoln Electric Company, ESAB Corporation (Colfax), voestalpine Böhler Welding Group GmbH, Illinois Tool Works Inc. (ITW), KOBE STEEL, LTD. (Kobelco Welding), Air Liquide S.A., Hyundai Welding Co., Ltd., Ador Welding Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Carbon Steel Electrode

- Low Alloy Steel Electrode

- Stainless Steel Electrode

- Heat-Resistant Steel Electrode

- Cast Iron Electrode

- Others

By Coating Type

- Rutile (High Titania)

- Basic (Low Hydrogen)

- Cellulosic

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Marine & Shipbuilding

- Oil & Gas/Energy

- Repair & Maintenance

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Welding Sticks Market-

- The Lincoln Electric Company

- ESAB Corporation (Colfax)

- voestalpine Böhler Welding Group GmbH

- Illinois Tool Works Inc. (ITW)

- KOBE STEEL, LTD. (Kobelco Welding)

- Air Liquide S.A.

- Hyundai Welding Co., Ltd.

- Ador Welding Limited

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Welding Sticks (SMAW Electrodes) Market, mapping demand across construction, MRO-intensive industries, shipbuilding, and energy projects while linking electrode metallurgy to code-critical performance; our analysis reviews all-position usability, slag control, and arc stability alongside sourcing risks and tariff-sensitive alloys, and it highlights breakthroughs in low-hydrogen H4/H8 classifications, Ni/Mo-alloyed high-toughness grades for sub-zero service, and fume-reduced coatings that align with OSHA/REACH—making this report an essential resource for procurement teams, welding engineers, and specifiers seeking faster WPS/PQR qualification, safer job-site execution, and resilient consumable strategies, etc……

Scope Highlights

Segmentation:

- By Product Type: Carbon Steel Electrode; Low Alloy Steel Electrode; Stainless Steel Electrode; Heat-Resistant Steel Electrode; Cast Iron Electrode; Others

- By Coating Type: Rutile (High Titania); Basic (Low Hydrogen); Cellulosic

- By End-Use Industry: Building & Construction; Automotive & Transportation; Marine & Shipbuilding; Oil & Gas/Energy; Repair & Maintenance

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies (analysis/profiles of 15+): The Lincoln Electric Company; ESAB Corporation; voestalpine Böhler Welding Group GmbH; Illinois Tool Works Inc. (Hobart Filler Metals); KOBE STEEL, LTD. (Kobelco Welding); Air Liquide S.A.; Hyundai Welding Co., Ltd.; Ador Welding Limited; Kiswel Inc.; Nippon Steel Welding & Engineering (NSSW); Tianjin Golden Bridge Welding Materials; D&H Sécheron; Oerlikon Welding; Fronius International GmbH; Miller Electric Mfg. LLC* (*select equipment/consumables interplay where relevant).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.