Wet Scrubber Market Overview 2025–2034: $1.5 Billion to $3.1 Billion at 8.5% CAGR Fueled by Maritime Decarbonization, Discharge Regulations, and Industrial Air Compliance

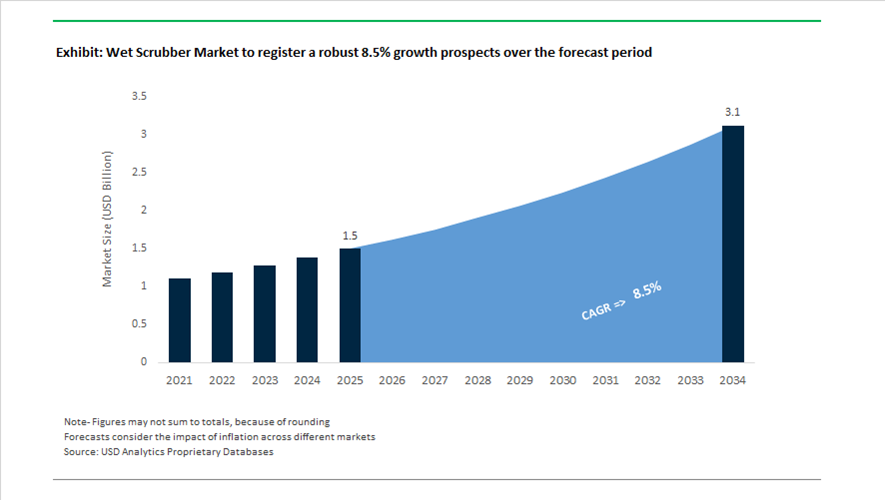

The Wet Scrubber market is valued at $1.5 billion in 2025 and is projected to reach $3.1 billion by 2034, expanding at a CAGR of 8.5%. Demand is being driven by tightening global sulfur oxide (SOx), nitrogen oxide (NOx), particulate matter (PM2.5), and hazardous air pollutant regulations across maritime and industrial sectors. The market encompasses open-loop, closed-loop, and hybrid marine scrubbers, venturi scrubbers, packed-bed scrubbers, wet electrostatic precipitators (WESP), and CCS-integrated exhaust treatment systems. Growth is particularly strong in marine exhaust gas cleaning systems (EGCS), refinery and petrochemical air pollution control, and high-particulate industrial processes in Asia-Pacific and North America.

Regulatory pressure intensified through 2024 and 2025. In December 2024, the U.S. Environmental Protection Agency secured $1.7 billion in enforcement fines, prompting accelerated capital investment in wet scrubbing systems among chemical manufacturers and refiners. In January 2025, discussions at the International Maritime Organization (IMO) formally addressed demands for a global ban on scrubber wash water discharge, raising uncertainty around open-loop systems and driving retrofitting toward hybrid and closed-loop configurations. In July 2025, Denmark and Sweden implemented coordinated bans on open-loop scrubber discharge within territorial waters, with Denmark’s restriction effective July 1, 2025, and additional limits on closed-loop systems scheduled for 2029. These regulatory developments are reshaping product demand toward discharge-compliant scrubbers and advanced wastewater treatment integration.

Technology innovation accelerated in parallel. In 2024, Valmet introduced a new wet electrostatic precipitator designed to integrate with hybrid scrubber systems, targeting ultra-fine particulate removal beyond current IMO and industrial air standards. Between 2024 and 2025, Wärtsilä launched its modular “IQ Series” exhaust treatment systems optimized for retrofit installations in space-constrained vessels. In May 2025, Wärtsilä commercially introduced a CCS-ready scrubber solution following pilot trials on the gas carrier Clipper Eris, enabling simultaneous SOx removal and CO2 capture from exhaust streams. This marks a significant evolution from compliance-driven scrubbing to carbon-integrated emission control. Nederman reported record 2024 net sales of SEK 5.90 billion in its February 2025 year-end release, attributing growth to IoT-enabled scrubber digitalization and predictive maintenance platforms.

Strategic acquisitions reinforced vertical integration in the marine segment. In August 2024, BW LPG completed a $1.05 billion acquisition of 12 scrubber-equipped Very Large Gas Carriers, underscoring the asset value of scrubber-fitted fleets under high fuel-spread conditions. In June 2025, TORM A/S acquired ME Production, securing in-house scrubber manufacturing capabilities to support its decarbonization strategy. In July 2024, Wärtsilä signed a six-year lifecycle agreement with Nautica Ship Management covering hybrid scrubber optimization, reflecting a shift toward service-based maintenance contracts. China’s 2025 “Blue Sky” Action Plan, targeting a 10% reduction in PM2.5 levels, accelerated adoption of high-efficiency venturi and packed-bed scrubbers across industrial clusters and river ports.

The wet scrubber market is evolving toward CCS-integrated exhaust systems, discharge-compliant hybrid scrubbers, modular retrofit designs, WESP integration, and digitally monitored predictive maintenance platforms. Maritime decarbonization, industrial air enforcement, and particulate reduction mandates remain the core growth drivers supporting high-single-digit expansion through 2034.

Trends and Opportunities in the Wet Scrubber Market

Trend 1: Strategic Integration with Zero Liquid Discharge (ZLD) Systems

Wet scrubbers are increasingly positioned as the front-end interface of fully integrated Zero Liquid Discharge (ZLD) systems, particularly in chemicals, refining, mining, and metals processing. Scrubber blowdown, once treated as a hazardous wastewater liability, is now being routed into evaporation and crystallization units to enable complete water recovery and by-product valorization.

In January 2024, GEA formally announced its “Zero Freshwater-Use” initiative, committing to deliver gas cleaning systems that are ZLD-ready by design. In chemical and mining applications, this architecture pairs wet scrubbers with forced-circulation evaporators and crystallizers to recover salts such as sodium sulfate from acidic exhaust streams. This approach converts regulatory compliance costs into monetizable mineral outputs while enabling 100% water reuse, a critical advantage in water-stressed industrial regions.

Refineries are accelerating adoption under decarbonization pressure. In December 2025, Babcock & Wilcox secured a $40 million contract for advanced Wet Gas Scrubbing (WGS) technology at a Canadian refinery. The system is engineered to operate within a multi-pollutant control train, simultaneously removing SOx, NOx precursors, and particulate matter while feeding downstream carbon capture and wastewater treatment units. This reflects a broader trend toward integrated emissions-water-carbon solutions rather than isolated abatement equipment.

Trend 2: Deployment of Modular, Skid-Mounted Scrubbers for Rapid Scaling

The rapid buildout of semiconductor fabs, battery gigafactories, and specialty chemical plants is driving demand for modular, skid-mounted wet scrubbers that significantly reduce installation timelines and construction risk. Pre-fabricated systems are increasingly favored over custom-built towers due to their predictable performance, faster commissioning, and lower civil engineering requirements.

Industry benchmarks from 2024–2025 indicate that modular wet scrubber systems can reduce onsite construction and integration time by up to 40%, a decisive advantage in industries where time-to-revenue is critical. These plug-and-play units integrate dosing systems, reaction tanks, mist eliminators, and automated controls within a standardized footprint, enabling phased capacity expansion as production ramps.

Service models are evolving in parallel. In May 2025, Wärtsilä expanded its lifecycle service agreements for modular scrubber installations, embedding remote monitoring and AI-driven chemical dosing optimization. These agreements are outcome-based, guaranteeing emissions performance such as sulfur equivalence below 0.1%, while shifting operational complexity away from end-users. This model is increasingly attractive to operators facing skilled labor shortages and tightening emissions enforcement.

Opportunity 1: Capturing Mandated Emissions Reductions in Marine and Port Operations

The global marine scrubber market is entering a structurally mandated growth phase driven by International Maritime Organization regulations and the expansion of Emission Control Areas. The IMO 2025 sulfur cap, combined with new ECAs in the North-East Atlantic, is sustaining strong retrofit and newbuild demand for Exhaust Gas Cleaning Systems (EGCS).

According to outcomes from the Marine Environment Protection Committee (MEPC 83) session in April 2025, approximately 5,061 scrubbers were projected to be installed globally by the start of 2025. The continued price spread between High Sulfur Fuel Oil and Low Sulfur Fuel Oil remains the primary economic driver, enabling shipowners to recover scrubber capital expenditure in less than 24 months on high-utilization vessels.

Regulatory constraints on washwater discharge are reshaping system design. As more ports restrict or ban open-loop scrubber discharge, hybrid and closed-loop configurations are becoming the default specification for newbuilds. These systems allow vessels to operate in closed-loop mode within port waters, capturing sulfur compounds and particulates for onshore disposal. This capability is increasingly viewed as essential to future-proof fleets against evolving maritime wastewater regulations.

Opportunity 2: Neutralizing Acid-Gas Emissions in Lithium-Ion Battery Recycling

The rapid scaling of lithium-ion battery recycling is creating a high-growth, compliance-driven opportunity for advanced wet scrubber systems capable of handling corrosive and toxic acid gases. Mechanical shredding and hydrometallurgical processing of spent batteries generate concentrated streams of hydrogen fluoride and hydrogen chloride, both of which pose acute safety and environmental risks.

In February 2025, ANDRITZ entered a cooperation agreement with Duesenfeld to deliver EPC-scale lithium-ion battery recycling plants. These facilities integrate vacuum drying and mechanical pre-treatment stages that require high-efficiency wet scrubbers to neutralize fluorine-bearing exhaust gases. When properly configured, these systems support material recovery rates exceeding 90% while ensuring regulatory-compliant air emissions.

Regulatory pressure is intensifying. In September 2025, the U.S. Environmental Protection Agency finalized stricter rules under the Resource Conservation and Recovery Act, classifying most lithium-ion battery waste as ignitable and reactive. This designation effectively mandates the use of Best Available Control Technology, with multi-stage wet scrubbers emerging as the default solution for mitigating toxic gas release during recycling operations. As battery recycling capacity expands across North America, Europe, and East Asia, wet scrubbers are becoming non-negotiable infrastructure rather than optional safeguards.

Wet Scrubber Market Share and Segmentation Insights

Type Market Share: Wet Scrubber Systems Lead with Multi-Pollutant Removal Efficiency

Wet scrubber systems dominate the market with a 68.40% share in 2025, driven by their ability to effectively remove both particulate matter and gaseous pollutants from industrial exhaust streams. Their versatility in handling high-temperature and moisture-laden gases makes them suitable across multiple industries. Dry and hybrid scrubber systems serve specific applications with different cost and operational profiles. A key trend is the surge in marine scrubber installations, where compliance with global sulfur emission regulations has accelerated adoption of wet scrubber systems in commercial shipping, supporting continued use of high-sulfur fuels while meeting emission standards.

Industry Vertical Market Share: Marine Sector Leads with IMO 2020 Compliance and Retrofit Demand

Marine accounts for 32.80% of the wet scrubber market in 2025, driven by the implementation of sulfur emission limits under IMO 2020 regulations. Shipowners have widely adopted scrubber systems to comply with emission standards while maintaining fuel cost efficiency. Power generation, oil and gas, mining and metallurgy, semiconductor, food, and pharmaceutical industries contribute to additional demand. A key market trend is the maturation of the retrofit cycle, where focus has shifted toward system optimization, maintenance services, and operational efficiency, alongside emerging regulatory considerations related to washwater discharge and carbon emission reduction strategies.

Wet Scrubber Market Competitive Landscape

The Wet Scrubber market in 2026 is shaped by smart-scrubbing ecosystems, hybrid-loop adaptability, and compact retrofit engineering, with increasing adoption of real-time monitoring, AI-driven chemical optimization, and energy-efficient emission control systems to meet tightening SOx, particulate, and wash-water discharge regulations.

Alfa Laval Leads Marine Scrubber Innovation with Compact PureSOx U-Design and Energy Reduction Modes

Alfa Laval dominates the marine wet scrubber market through its advanced PureSOx platform engineered for compact retrofits and operational efficiency. The 2025 U-design upgrade reduces system height by up to 26%, enabling installation in space-constrained vessels without auxiliary fans. Its Energy Reduction Mode lowers scrubber power consumption by 25%, improving vessel carbon intensity metrics. Integration with PureNOx Prime enables multi-pollutant control across alternative fuels such as ethane and ammonia. Over 80% of customers adopt lifecycle service agreements with predictive maintenance and remote monitoring. This lifecycle connectivity ensures compliance with stringent SECA sulfur limits and enhances operational reliability.

Babcock & Wilcox Expands Multi-Pollutant Wet Scrubbing with AI-Integrated Industrial Infrastructure

Babcock & Wilcox is repositioning wet scrubbers as critical infrastructure within AI-powered industrial ecosystems and clean energy projects. Its $2.4 billion agreement for AI Factory campuses integrates advanced wet scrubbing for ultra-low emissions compliance. The company secured a $40 million refinery contract for low-pressure wet gas scrubbing systems targeting acid mist and mercury removal. Acquisition of Hamon Research-Cottrell strengthens its wet flue gas desulfurization portfolio across multiple industries. Ongoing R&D focuses on multi-pollutant scrubbers capable of removing SO2, particulates, and mercury in a single unit. This integrated approach reduces system footprint while improving CAPEX-to-OPEX efficiency.

ANDRITZ Integrates Wet Scrubbers into Circular Economy Waste-to-Resource Systems

ANDRITZ is leveraging its environmental engineering expertise to integrate wet scrubbers into circular economy infrastructure, particularly in sludge-to-energy applications. The company reported a €10.5 billion backlog in 2026, supported by high-margin service contracts and strong execution. Its wet scrubbing systems are deployed in German sludge incineration plants to enable phosphorus recovery and regulatory compliance. Strategic acquisitions, including LDX Solutions, enhance its air pollution control capabilities in North America. Integration with hydropower and pulp operations provides a comprehensive environmental solution for industrial clients. This cross-sector synergy strengthens its role in sustainable waste treatment and emissions control.

Wärtsilä Advances Carbon Capture-Ready Wet Scrubbers for Maritime Decarbonization

Wärtsilä is transforming wet scrubbers into carbon capture-ready platforms aligned with maritime decarbonization strategies. Its systems integrate CO2 capture modules capable of reducing emissions by up to 70% without major engine modifications. The company generated €6.4 billion in revenue and is shifting toward performance-based service agreements tied to emissions outcomes. Its digital ecosystem enables real-time optimization of scrubber operations using wash-water and back-pressure data. Focus on fuel flexibility ensures compatibility with biofuels, LNG blends, and ammonia-based fuels. This approach positions wet scrubbers as long-term assets in evolving marine fuel landscapes.

GEA Group Strengthens Modular Wet Scrubber Systems for High-Purity Industrial Applications

GEA Group is expanding its presence in precision air cleaning through modular wet scrubber systems tailored for food, pharma, and chemical industries. The company reported EBITDA margins of 16.5% and secured €560.6 million in major contracts driven by demand for odor control and particulate recovery. Its Separation & Flow Technologies division supports scalable scrubber deployment with reduced water consumption. Sustainable technologies now contribute over 45% of total revenue, reflecting strong alignment with industrial decarbonization trends. A vitality index near 20% highlights rapid innovation in next-generation gas cleaning systems. These advancements enhance particulate removal efficiency while supporting regulatory compliance in sensitive processing environments.

China Wet Scrubber Market Driven by Maritime Newbuilds and High-Tech Emissions Control

China’s wet scrubber market in 2025–2026 is being reshaped by a convergence of maritime manufacturing strength, semiconductor regulation, and industrial process upgrades. In late 2025, Wärtsilä finalized a strategic agreement with Guangzhou Shipyard International to supply advanced exhaust gas cleaning systems for two 218-meter RoPax vessels. This project underscores how Chinese shipyards have become global hubs for scrubber-integrated newbuilds, particularly as shipowners seek compliance-ready vessels for international sulfur and particulate regulations. The implication for the wet scrubber market is structural. Demand is increasingly front-loaded into the shipbuilding phase rather than retrofits, favoring suppliers with deep integration capabilities and lifecycle service models.

Beyond shipping, China’s Clean Electronics Initiative for 2025–2026 is accelerating adoption of thermal wet scrubbers across advanced semiconductor fabs. All new 28 nm and below fabrication plants are now required to deploy wet scrubbing systems capable of neutralizing high-concentration VOCs and acid gases generated during etching and deposition. Parallel industrial momentum is visible in the pulp and paper sector. In December 2025, Andritz secured a contract from Guangxi Botare Yuantrove Paper for a lime kiln plant featuring a customized wet scrubbing stage designed for ultra-low particulate emissions. At the lighter end of the spectrum, July 2025 marked a notable shift toward autonomous cleaning systems when Haier launched the RHXG-H1 AI-enabled floor scrubber, signaling that “wet scrubbing” in China now spans from heavy industry to intelligent logistics infrastructure.

United States Wet Scrubber Market Anchored in Power, Refrigeration, and Data Infrastructure

The United States wet scrubber market is increasingly defined by system upgrades rather than greenfield builds, with emissions compliance, energy transition, and digital infrastructure acting as primary catalysts. In December 2025, Babcock & Wilcox received a limited notice to proceed on an $80 million SolveBright post-combustion carbon capture project. This development highlights a growing trend of coupling wet scrubbing stages with regenerable solvent-based CO₂ capture at existing power and industrial plants, extending asset life while aligning with tightening air quality requirements.

Regulatory drivers are reinforcing this trajectory. The U.S. Environmental Protection Agency’s November 2025 decision to extend compliance timelines for certain industrial refrigeration equipment to 2030 has increased the need for specialized wet scrubbers to manage leakage and by-product gases during the transition to low-GWP refrigerants. Service and refurbishment activity remains strong. In November 2025, BWCC, a Babcock & Wilcox subsidiary, secured a $17 million contract to refurbish wet scrubbing and emission control systems at a major coal-fired power plant to ensure compliance with 2026 air standards. A newer demand vector is emerging from AI data centers. As hyperscale facilities drive unprecedented power consumption, B&W has signaled plans to deploy its natural gas and scrubbing technologies to support emission control needs, targeting a multi-billion-dollar opportunity pipeline tied directly to digital infrastructure growth.

India Wet Scrubber Market Shaped by Power Sector Mandates and Infrastructure Spillovers

India’s wet scrubber market is undergoing a decisive expansion phase, primarily driven by regulatory clarity in the thermal power sector. A Ministry of Power notification issued on July 11, 2025 established firm timelines for Flue Gas Desulphurization installations. Category A plants located near million-plus cities must comply by December 31, 2027, triggering a sharp increase in procurement of wet FGD systems. This regulatory certainty has shifted investment from tentative planning to execution, particularly among utilities with long remaining asset lives.

At the same time, the policy framework has created a bifurcated market. Plants scheduled for retirement before December 31, 2030 are exempt from new SO₂ standards, concentrating demand for advanced wet scrubbers in strategically important, long-term facilities. Maharashtra exemplifies this dynamic. Government disclosures from August 2025 classified 14 units totaling 4,910 MW as Category A, effectively mandating immediate investment in wet scrubbing infrastructure. Outside power generation, ancillary demand is emerging through water and chemical infrastructure. The expansion of the Jal Jeevan Mission has indirectly increased deployment of localized wet scrubbers in chemical dosing stations and chlorine gas neutralization units at rural and peri-urban treatment hubs, broadening the addressable market beyond utilities alone.

Germany Wet Scrubber Market Centered on Resource Recovery and Smart Emissions Control

Germany continues to occupy a premium position in the global wet scrubber market, defined less by volume and more by technological leadership and regulatory ambition. In November 2025, Andritz secured a €100 million contract to construct a mono-incineration plant in Wuppertal. The facility integrates a multi-stage wet flue gas cleaning system explicitly designed to enable phosphorus recovery, aligning wet scrubbing with the EU’s critical raw materials agenda. This integration of emissions control and resource recovery is becoming a defining characteristic of the German market.

Innovation depth is supported by intellectual property strength. Data from the Federal Environment Agency indicates that Germany now accounts for approximately 18% of global air pollution control patents, with 2025–2026 R&D focusing on SmartFilter concepts that combine wet scrubbing with UV-C sterilization. Application diversification is also accelerating. In 2025, German suppliers including EcoClean Systems launched specialized wet scrubber variants such as SmartFilter Li-Batt to address lithium oxide particulates and toxic fumes from EV battery recycling. This positions wet scrubbers as enabling infrastructure for Europe’s circular battery economy rather than purely compliance equipment.

Japan Wet Scrubber Market Advancing Through Maritime Carbon Capture and Semiconductor Integration

Japan’s wet scrubber market is increasingly linked to decarbonization innovation and point-of-use precision. In late 2025, collaborative research led by the National Maritime Research Institute demonstrated that modified PureSOx wet scrubbers, developed with Alfa Laval, can capture CO₂ from auxiliary ship engines in closed-loop mode. This proof point has elevated onboard carbon capture from concept to near-term application, with industry data suggesting that Japan-developed systems could cut maritime emissions by up to 90% by 2028.

Semiconductors represent a second growth pillar. Japanese equipment manufacturers are increasingly integrating compact wet scrubbers directly into fabrication tools as point-of-use abatement systems. These units are designed to neutralize hazardous etch-gas effluents before they enter centralized exhaust lines, improving safety and process stability. This approach aligns closely with regional semiconductor expansion strategies, including supply chain alignment with neighboring Korea, and reinforces Japan’s role as a precision engineering leader in the global wet scrubber market.

Country-Level Snapshot of the Wet Scrubber Market

Wet Scrubber Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Core Applications

|

Strategic Market Character

|

|

China

|

Shipbuilding and semiconductor mandates

|

Marine exhaust, fab VOC control

|

Scale-driven, vertically integrated

|

|

United States

|

Power upgrades and digital infrastructure

|

Power plants, refrigeration, data centers

|

Retrofit- and service-led growth

|

|

India

|

Thermal power FGD deadlines

|

Coal power plants, chemical neutralization

|

Regulation-driven expansion

|

|

Germany

|

Resource recovery and advanced recycling

|

Sludge incineration, battery recycling

|

Technology- and IP-led

|

|

Japan

|

Maritime decarbonization and fabs

|

Onboard carbon capture, POU scrubbers

|

Innovation-focused, precision systems

|

Wet Scrubber Market Report Scope

Wet Scrubber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$3.1 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Type (Wet Scrubber Systems, Dry Scrubber Systems, Hybrid Scrubber Systems), By Application (Particulate Matter Removal, Gaseous Pollutant Removal, Onboard Carbon Capture, Odor Control), By Industry Vertical (Marine, Power Generation, Oil and Gas, Semiconductor and Electronics, Mining and Metallurgy, Food and Beverage, Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wärtsilä Corporation, Andritz AG, Babcock and Wilcox Enterprises Inc., Alfa Laval AB, GEA Group AG, Mitsubishi Shipbuilding Co. Ltd., Yara Marine Technologies, DuPont Sustainable Solutions, Hamon Group, CECO Environmental Corp., Fuji Electric Co. Ltd., Kwality Polyplast, Verantis Environmental Solutions Group, Evoqua Water Technologies, KCH Services Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wet Scrubber Market Segmentation

By Type

- Wet Scrubber Systems

- Venturi

- Packed Bed

- Spray Tower

- Cyclonic Spray

- Dry Scrubber Systems

- Hybrid Scrubber Systems

By Application

- Particulate Matter Removal

- Gaseous Pollutant Removal

- Onboard Carbon Capture

- Odor Control

By Industry Vertical

- Marine

- Power Generation

- Oil and Gas

- Semiconductor and Electronics

- Mining and Metallurgy

- Food and Beverage

- Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Wet Scrubber Market

- Wärtsilä Corporation

- Andritz AG

- Babcock and Wilcox Enterprises Inc.

- Alfa Laval AB

- GEA Group AG

- Mitsubishi Shipbuilding Co. Ltd.

- Yara Marine Technologies

- DuPont Sustainable Solutions

- Hamon Group

- CECO Environmental Corp.

- Fuji Electric Co. Ltd.

- Kwality Polyplast

- Verantis Environmental Solutions Group

- Evoqua Water Technologies

- KCH Services Inc.

*- List not Exhaustive