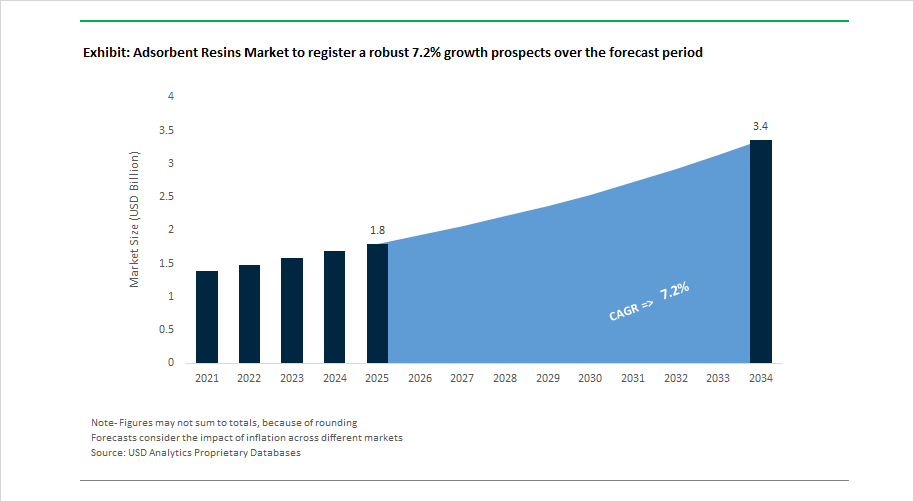

Market Overview: Adsorbent Resins Market Growth to $3.4 Billion by 2034 Led by Bioprocessing Demand, Semiconductor Water Purification, and Sustainable Separation Technologies

The global adsorbent resins market is projected to grow from $1.8 billion in 2025 to $3.4 billion by 2034, registering a 7.2% CAGR. Expansion is supported by rising demand for polymeric adsorbents, ion exchange resins, affinity chromatography resins, and specialty purification media across biopharmaceutical manufacturing, ultrapure water systems for semiconductors, food-grade organic acid purification, lithium extraction, and industrial wastewater treatment. Adsorbent resins are essential for molecular separation, impurity removal, solvent recovery, protein purification, and selective ion capture, with performance criteria focused on binding capacity, fouling resistance, cycle life, chemical stability, and regulatory compliance. Growth is increasingly tied to high-purity processing, water circularity infrastructure, and sustainable feedstock integration, positioning advanced adsorption materials as critical components in life sciences, electronics fabrication, and resource recovery value chains.

Sustainability-oriented product development strengthened in 2024 when BASF introduced low-residual monomer polymeric adsorbents for pharmaceutical purification, reducing solvent usage significantly. In the same year, Mitsubishi Chemical Group expanded its DIAION sustainable resin series using partially renewable feedstocks, while Thermax Limited launched modular adsorption systems enabling solvent recovery and water reuse in industrial plants. Bioprocessing innovation accelerated in July 2024 as Purolite introduced DurA Cycle A50 Protein A resin designed for extended cycle life in monoclonal antibody production. Corporate restructuring reshaped supplier focus in April 2025 when LANXESS divested its Urethane Systems business, allowing deeper investment in liquid purification technologies including ion exchange and adsorbent resins. Infrastructure expansion followed in early 2025 as Sunresin New Materials established a major Anhui facility for wastewater purification and lithium extraction resins.

Biopharma and electronics sectors drove further innovation. In June 2025, Ecolab launched Purolite AP+50, a 50-micron affinity chromatography resin offering high binding capacity and consistency for antibody production. Ecolab strengthened its semiconductor water portfolio in December 2025 through acquisition of Ovivo’s electronics ultrapure water business, integrating specialized resin and membrane technologies for microelectronics fabrication. Strategic collaboration in early 2025 saw Purolite partner with a U.S. biopharma company to develop resins for continuous protein purification processes. Portfolio rationalization emerged in July 2025 when Mitsubishi Chemical Corporation exited the polyester toner resin segment, redirecting resources toward higher-value materials. Food and beverage purification advanced in January 2026 with DuPont launching AmberLite FPA57 weak base anion resin for lactic and citric acid processing, improving cycle time and fouling resistance. Regional diversification continued through Sika’s acquisition of KEMA in the Middle East, expanding access to specialty resin technologies serving industrial adsorption and construction-related purification needs.

Strategic Market Trends and Growth Opportunities Reshaping the Adsorbent Resins Market

Market Trend: Pharma-Grade Purification Demand Accelerates Capacity Expansion and Technology Focus

A surge in global biologics production is driving unprecedented demand for high-purity chromatographic adsorbent resins, particularly for monoclonal antibodies (mAbs) and GLP-1-based therapies like Wegovy and Zepbound. Manufacturers are investing in both resin performance and supply reliability, focusing on stronger dynamic binding capacities, better batch uniformity, and shorter lead times.

Ecolab’s Purolite division is at the forefront of this shift. The launch of Purolite AP+50 in June 2025 features patented jetted bead technology tailored to maximize mAb capture efficiency, reducing operational time and boosting productivity for bioprocessors. Complementing this, the new Bioprocessing Applications Laboratory in Pennsylvania helps scale R&D breakthroughs to commercial deployment, ensuring biologics manufacturers can maintain regulatory purity requirements across global supply networks. As targeted therapies expand, leading pharma companies continue to secure long-term resin supply contracts, transforming adsorbent resins into priority materials for the biologics value chain.

Market Trend: Strategic Resin Alliances Strengthen Lithium Supply Security Through Direct Extraction

Energy transition investments are pushing adsorbent resins into the battery materials market through Direct Lithium Extraction (DLE) technologies. Producers are working directly with mining and water-technology majors to replace evaporation ponds with efficient, footprint-optimized recovery systems. Commercial collaborations such as the July 2025 MoU between Veolia Water Technologies and Nobian show how ion exchange and crystallization systems are enabling battery-grade lithium hydroxide production directly from brines.

As lithium becomes central to regional energy independence strategies, especially in Europe and the United States, DLE resin technologies are being deployed into existing chemical infrastructure to cut operating expenses by up to 30% while delivering recovery rates above 90%. Resin-enabled DLE unlocks previously uneconomic resources and is now viewed as a foundational technology for the next surge in gigafactory construction.

Market Opportunity: PFAS Removal Regulations Create a Multi-Billion-Dollar Water Treatment Market

Public health regulations are rapidly transforming adsorbent resins into a compliance-critical filtration material. PFAS removal requirements issued by the U.S. Environmental Protection Agency in April 2024 mandate strict drinking-water limits of 4 parts per trillion for PFOA and PFOS. Municipal water systems have until 2027–2029 to deploy upgrades, triggering immediate procurement of high-selectivity ion exchange resins that can meet tight performance targets at full utility scale.

According to the American Water Works Association, U.S. infrastructure upgrades alone will require USD 37.1–48.3 billion in capital spending by 2031. Regenerable resins are gaining rapid attention because they reduce disposal burdens and operating cost over system lifetime, aligning with municipal budget constraints and sustainability mandates. Companies that provide both technology and long-term service capabilities are positioned to capture recurring revenue from multi-decade PFAS remediation programs.

Market Opportunity: Functionalized Adsorbent Resins Emerging as a Core Technology for Carbon Capture and DAC

Direct Air Capture (DAC) and industrial flue-gas decarbonization are creating a new, premium application segment for functionalized polymer resins engineered to capture CO₂ with lower heat and power consumption than amine-based liquid systems. A growing number of carbon removal developers are integrating resin-based adsorption into gigaton-scale plans.

Skytree’s multi-year development and supply agreement with Purolite, signed in June 2024, illustrates how large-scale industrial partnerships are accelerating product refinement for higher capture efficiency and reduced regeneration energy. Lewis acid–base hybrid sorbents have achieved more than 5 mol CO₂ per kg capacity in recent trials, tripling the output of earlier solid sorbents. Major deployment initiatives like the STRATOS project in Texas, which will remove over 500,000 tons of CO₂ annually, show escalating commercial adoption supported by corporate buyers such as Microsoft seeking verified carbon credits.

Purpose-built adsorbent resins are becoming essential to meeting the world’s most important industrial and environmental objectives. As regulatory timelines tighten and low-carbon technologies scale, resin manufacturers with application leadership in bioprocessing, battery materials, water purification, and carbon capture will remain the primary beneficiaries of future market acceleration.

Adsorbent Resins Market Share and Segmentation Insights

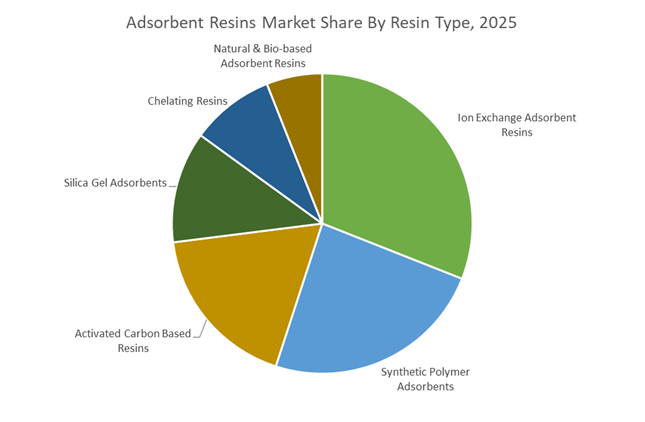

Market Share by Resin Type: Ion Exchange Leads as Synthetic Polymer Adsorbents Accelerate

Ion exchange adsorbent resins account for approximately 31% of global adsorbent resin demand in 2025, maintaining leadership due to their indispensable role in water softening, ultrapure water production for semiconductors and power generation, and hydrometallurgy. Municipal water treatment upgrades and PFAS removal mandates are sustaining growth in developed markets, while industrialization supports rising volumes in emerging economies. Synthetic polymer adsorbents rank second and represent the fastest-growing premium category at +8% YoY, offering high selectivity for pharmaceutical purification, peptide synthesis, and blood purification. The surge in monoclonal antibodies and mRNA vaccines has sharply increased chromatography resin demand. Activated carbon based resins remain dominant for bulk organic contaminant removal but face displacement from regenerable synthetic systems in closed-loop processes. Chelating resins serve high-value niches in heavy metal removal and critical mineral recovery, while natural and bio-based adsorbents remain smallest, gaining traction in low-cost food applications amid EU-driven sustainability R&D.

Market Share by End-Use Industry: Healthcare Dominates While Semiconductor Manufacturing Fuels Growth

Healthcare & lifesciences command approximately 37% of adsorbent resin consumption in 2025, making it the largest and highest-margin end-use. Resins are essential for downstream drug purification, hemoperfusion in sepsis and liver failure, and diagnostic applications, with aging populations and biosimilar expansion in Asia-Pacific providing structural tailwinds. Power generation ranks second, supported by ion exchange resins used in nuclear coolant purification and condensate polishing in coal and gas plants, even as Western coal retirements offset volumes. Electronics & semiconductors represent the fastest-growing segment, as fabs require millions of gallons of ultrapure water daily, driving demand for ion exchange and polymer adsorbents to remove TOC and trace metals to parts-per-trillion levels. Oil & gas remains mature, while agriculture and food processing deliver steady, population-linked demand through juice clarification and fermentation-based antibiotic extraction.

Competitive Landscape: High-Purity Separation Technologies and Sustainability Innovation Defining the Adsorbent Resins Market

The global Adsorbent Resins Market is being reshaped by rising demand for ultrapure water, life sciences separations, PFAS remediation, and renewable energy applications. Competitive leadership now centers on polymeric adsorbents with high surface area, monodisperse bead technology, and application-specific functionalization for food processing, pharmaceuticals, carbon capture, and green hydrogen. Leading suppliers are pairing advanced resin chemistries with digital monitoring, lifecycle service models, and low-leachable formulations, while regional players are scaling domestic manufacturing and bio-based alternatives. Below is a structured assessment of how key companies are positioning across industrial purification, emerging contaminants, and next-generation energy systems.

DuPont Water Solutions advances food-grade and pharmaceutical purification with AmberLite™ innovation

DuPont Water Solutions remains a global leader in separation technologies, leveraging its AmberLite™ portfolio across high-purity industrial and food-grade applications. In January 2026, DuPont launched AmberLite™ FPA57, a next-generation weak base anion resin for organic acid purification, delivering longer operating cycles and improved fouling resistance in citric and lactic acid processing. Its AmberLite™ SD-2 polymeric adsorbents provide a cleaner alternative to activated carbon for sweetener decolorization. DuPont maintains strong positions in taste and odor removal for beverages and API isolation in pharmaceuticals, while integrating digital monitoring into resin beds to enable predictive maintenance and optimized regenerant chemical usage.

Purolite scales PFAS-selective adsorbents through Ecolab’s global service platform

Following its acquisition by Ecolab, Purolite has evolved into a high-value purification specialist serving life sciences and industrial markets. In 2025, Purolite expanded its PuroSorb™ and Macronet™ production lines to address surging demand for PFAS-selective adsorbent resins. The company also partnered with Skytree to improve energy efficiency in Direct Air Capture systems using tailored resin chemistries. Purolite’s jet-dispensed uniform bead technology enhances column flow kinetics, while Ecolab’s service network enables a Resin-as-a-Service model covering installation, monitoring, and off-site regeneration.

Mitsubishi Chemical Group sets technical benchmarks for pharmaceutical-grade synthetic adsorbents

Mitsubishi Chemical Group is widely regarded as the technical standard bearer for aromatic and methacrylate-based adsorbents under its DIAION™ and SEPABEADS™ brands. The DIAION™ HP and SEPABEADS™ SP series are industry benchmarks for peptide, protein, and polyphenol purification. In early 2026, the company introduced HP20SS and SP20SS small-diameter resins for ultra-high-resolution separations in advanced biopharma, including monoclonal antibodies and oligonucleotides. Mitsubishi Chemical also supplies low-odor, low-leachable resins for ultrapure water systems and entered a January 2026 decarbonization agreement with Asahi Kasei Corporation and Mitsui Chemicals to improve sustainability across resin feedstocks.

LANXESS AG deploys Lewatit® resins for green hydrogen and heavy metal remediation

LANXESS AG focuses on high-performance adsorbents through its Lewatit® platform, with a strong push into renewable energy infrastructure. In 2026, the company began deploying Lewatit® UltraPure resins in PEM electrolysis systems, supporting megawatt-scale green hydrogen projects with global gas partners. LANXESS also announced a global price increase for Lewatit® and Ionac® resins in January 2026 to sustain high-purity production amid volatile energy costs. Beyond energy, LANXESS leads in arsenic and heavy metal removal for municipal groundwater treatment, supported by vertically integrated monodisperse resin manufacturing that delivers superior mechanical and osmotic stability.

ResinTech, Inc. expands domestic capacity for PFAS and emerging contaminant remediation

ResinTech has emerged as a prominent Made-in-USA producer, opening one of the first new resin manufacturing facilities in the country in over three decades. In May 2025, the company launched Advanced Hybrid Resins designed for comprehensive groundwater remediation of PFAS and 1,4-dioxane. ResinTech pioneered a solvent-free manufacturing process at its Camden, New Jersey campus, ensuring drinking water resins are free from harmful byproducts. Through ResinTech Lab Services, customers receive detailed foulant analysis and capacity projections. The company now produces over half a million cubic feet annually of specialty cation and adsorbent resins for North American power and semiconductor markets.

Thermax Limited customizes adsorbent resins for food processing, oxygen systems, and metal recovery

Thermax Limited plays a critical role across Asia-Pacific and the Middle East, delivering customized adsorbent solutions for demanding industrial environments. Its TULSION® resin portfolio includes grades for sugar syrup decolorization and bitter compound removal in fruit juices. Thermax has developed low-cost polymeric adsorbents with enhanced thermal stability for air separation units and medical oxygen concentrators. Strategically, the company is transitioning toward bio-based adsorbent resins derived from renewable plant materials to support clean-label food processing. Its chelating resin expertise enables selective metal binding, supporting precious metal recovery from electronic waste and complex industrial effluents.

United States Adsorbent Resins Market: Bioprocessing Scale-Up, PFAS Remediation, and Clean Energy Integration

The United States remains a global innovation center for adsorbent resins, driven by biologics manufacturing, environmental regulation, and energy transition. In May 2025, Ecolab Life Sciences (Purolite) opened a state-of-the-art Bioprocessing Applications Laboratory in Pennsylvania. The facility provides high-throughput process development tools that optimize monoclonal antibody purification using advanced jetted resin technology, supporting faster scale-up and higher productivity in large biologics plants. This investment aligns with rising domestic demand for high-durability chromatography resins as U.S. biomanufacturing capacity expands.

Environmental regulation is an equally powerful driver. Following the EPA’s finalized enforceable limits for PFAS in drinking water in April 2024, U.S. municipalities have accelerated deployment of specialty adsorbent resins such as AmberLite™ for trace contaminant removal in large water treatment plants. Climate technology is reinforcing growth prospects. In June 2024, Purolite entered a multi-year development agreement with Skytree to supply tailored resins for Direct Air Capture systems aimed at lowering energy consumption per ton of captured CO₂. Product innovation continues with the June 2025 launch of Purolite™ AP+50, a 50-micron affinity chromatography resin engineered for high-durability mAb capture. On the industrial side, DuPont scaled deployment of AmberLite™ P2X110 to maintain ultra-high water purity in green hydrogen electrolyzers, while expanded manufacturing capacity in Landenberg, Pennsylvania during 2024 to 2025 addressed surging domestic demand for high-purity resins.

China Adsorbent Resins Market: Capacity Expansion, Pharma Compliance, and Resource Recovery Technologies

China’s adsorbent resins market is advancing through coordinated capacity build-out, healthcare innovation, and strategic resource recovery. Purolite announced a new resin manufacturing plant in the Quzhou Industrial Park, with construction starting in 2024 and full delivery of water and industrial resins expected by late 2026. This expansion reflects sustained domestic demand across water treatment, chemicals, and energy applications.

Local innovation is accelerating. As of July 2025, Sunresin New Materials achieved 10 Drug Master File registrations for its chromatography resins, enabling broader adoption of Chinese-made adsorbents in global vaccine and gene therapy manufacturing. In healthcare, Sunresin launched a hemoperfusion resin for bilirubin removal in October 2025, improving safety and efficacy in blood purification therapies. Resource recovery is another growth pillar. Sunresin secured an Australian patent in June 2025 for lithium adsorbent technology used in direct lithium extraction, strengthening intellectual property protection across Asia and Oceania. Industrial efficiency gains were demonstrated through continuous adsorption systems deployed for stevia purification in October 2025, while phosphorus removal resins introduced in late 2025 support freshwater remediation under the national Beautiful China initiative.

India Adsorbent Resins Market: API Localization, Emissions Compliance, and Food-Grade Separation Demand

India is emerging as a structurally important growth market for adsorbent resins as pharmaceutical localization and environmental regulation intensify. Under the Production Linked Incentive scheme, cumulative investment exceeding ₹4,763 crore by September 2025 has strengthened domestic manufacturing of critical starting materials and APIs. This has created strong demand for ion exchange and adsorption resins used in purification, decolorization, and solvent recovery across pharma value chains.

Regulatory developments are expanding industrial adoption. The Carbon Credit Trading Scheme notified in October 2025 introduced legally binding emission intensity targets for petrochemicals and textiles, driving deployment of adsorbent resins for VOC capture and effluent treatment. In the sugar industry, LANXESS showcased Lewatit® S resins at the STAI International Sugar Expo 2025, offering 10% higher operating capacity for sugar decolorization. Infrastructure investment further supports growth. Three Bulk Drug Parks with a combined ₹3,000 crore budget are providing shared facilities for resin-based separation processes. At the same time, stricter food safety enforcement by the Food Safety and Standards Authority of India in late 2025 mandates certified Halal and Kosher food-grade adsorbents for liquid sugar demineralization.

Germany Adsorbent Resins Market: Decarbonization, Circular Water Systems, and Advanced Materials Research

Germany’s adsorbent resins market is shaped by decarbonization goals, circular economy compliance, and advanced research capabilities. Specialty chemical producers are transitioning to all-electric resin extrusion drives and bio-based feedstocks to meet EU Carbon Border Adjustment Mechanism targets from 2026. These changes are increasing demand for energy-efficient and regenerable resin systems.

Circularity is driving adoption in industrial wastewater treatment. German automotive manufacturers are increasingly using regenerable resins to capture trace metals from electroplating wastewater, aligning operations with EU Green Deal requirements. Technology transfer also plays a role. In October 2025, German-affiliated purification technology was deployed by Sunresin for hydrogen peroxide purification in caprolactam production, enhancing nylon feedstock efficiency. Research leadership remains strong, with Germany contributing significantly to the global nanoscale chemical adsorbents market, projected at $5.94 billion by 2025, reinforcing its position in next-generation adsorbent development.

Japan Adsorbent Resins Market: Strategic Realignment Toward Semiconductors and Clean Energy

Japan’s adsorbent resins industry is undergoing strategic realignment toward high-growth applications. Mitsubishi Chemical Group announced its exit from the polyester resin business for printer toner by June 2026, reallocating capital toward adsorbent resins used in semiconductors, clean energy, and recycling. This restructuring includes a planned 400 billion yen asset exit by March 2030, prioritizing high-purity specialty chemicals.

Demand is concentrated in ultra-pure systems. Japanese producers are expanding mixed-bed nuclear and ultrapure water resins to support revitalized domestic chip manufacturing hubs. These resins are critical for maintaining contamination-free process water in advanced semiconductor fabrication, reinforcing Japan’s role in precision-grade adsorbent technologies.

Sweden Adsorbent Resins Market: European Life Sciences Access and Regulatory Enablement

Sweden is emerging as a strategic European hub for life sciences focused adsorbent resins. In October 2025, Sunresin New Materials established its European Regional Headquarters for Life Sciences in Sweden, positioning operations close to major biopharma clusters. This move enhances localized technical support and shortens supply chains for chromatography media across Europe.

Regulatory alignment is a key advantage. The Swedish subsidiary is designed to streamline compliance with European Medicines Agency requirements and to support IND and NDA filings for pharmaceutical customers using Sunresin resins. This positioning strengthens Sweden’s role as a gateway for global resin suppliers into regulated European biopharmaceutical markets.

Country-Level Positioning in the Adsorbent Resins Industry

Adsorbent Resins Market County Level Snapshot

|

Country

|

Core Demand Drivers

|

Strategic Market Impact

|

|

United States

|

Biologics scale-up, PFAS regulation, hydrogen

|

Innovation leadership and high-purity capacity growth

|

|

China

|

Capacity expansion, pharma compliance, lithium recovery

|

Integrated growth across healthcare and resources

|

|

India

|

API localization, emissions targets, food safety

|

Rapid adoption in pharma and industrial treatment

|

|

Germany

|

Decarbonization, circular wastewater, R&D

|

Advanced and regenerable resin leadership

|

|

Japan

|

Semiconductor purity, clean energy focus

|

High-value specialty realignment

|

|

Sweden

|

Biopharma proximity, EMA compliance

|

European life sciences access hub

|

Adsorbent Resins Market Report Scope

Adsorbent Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Resin Type (Synthetic Polymer Adsorbents, Activated Carbon Based Resins, Silica Gel Adsorbents, Natural and Bio Based Adsorbent Resins, Chelating Resins, Ion Exchange Adsorbent Resins), By Application (Water and Wastewater Treatment, Pharmaceutical and Biotechnology, Food and Beverage, Chemical and Petrochemical, Mining and Metallurgy, Environmental Remediation), By Matrix Structure (Macroporous Resins, Gel Type Resins, Hyper Crosslinked Resins), By End Use Industry (Healthcare and Lifesciences, Power Generation, Electronics and Semiconductors, Oil and Gas, Agriculture and Food Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont Water Solutions, Ecolab, Mitsubishi Chemical Corporation, LANXESS AG, Sunresin New Materials, Arkema, BASF, Thermax, ResinTech, Bio Rad Laboratories, Samyang Corporation, Tosoh Corporation, Fineex, Jacobi Carbons, Suqing Water Treatment

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Adsorbent Resins Market Segmentation

By Resin Type

- Synthetic Polymer Adsorbents

- Styrenic

- Acrylic

- Methacrylic

- Activated Carbon Based Resins

- Silica Gel Adsorbents

- Natural and Bio Based Adsorbent Resins

- Chelating Resins

- Ion Exchange Adsorbent Resins

By Application

- Water and Wastewater Treatment

- PFAS Removal

- Deionization

- Softening

- Pharmaceutical and Biotechnology

- Chromatography

- API Purification

- Blood Purification

- Food and Beverage

- Sugar Decolorization

- Juice Debittering

- Caffeine Removal

- Chemical and Petrochemical

- Catalysis

- Solvent Recovery

- Feedstock Purification

- Mining and Metallurgy

- Lithium Extraction

- Precious Metal Recovery

- Environmental Remediation

- Carbon Capture

- VOC Abatement

By Matrix Structure

- Macroporous Resins

- Gel Type Resins

- Hyper Crosslinked Resins

By End Use Industry

- Healthcare and Lifesciences

- Power Generation

- Electronics and Semiconductors

- Oil and Gas

- Agriculture and Food Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Adsorbent Resins Industry

- DuPont Water Solutions

- Ecolab

- Mitsubishi Chemical Corporation

- LANXESS AG

- Sunresin New Materials

- Arkema

- BASF

- Thermax

- ResinTech

- Bio Rad Laboratories

- Samyang Corporation

- Tosoh Corporation

- Fineex

- Jacobi Carbons

- Suqing Water Treatment

*- List not Exhaustive