Global Airless Packaging Market Overview: Protecting Sensitive Formulations and Driving Sustainability

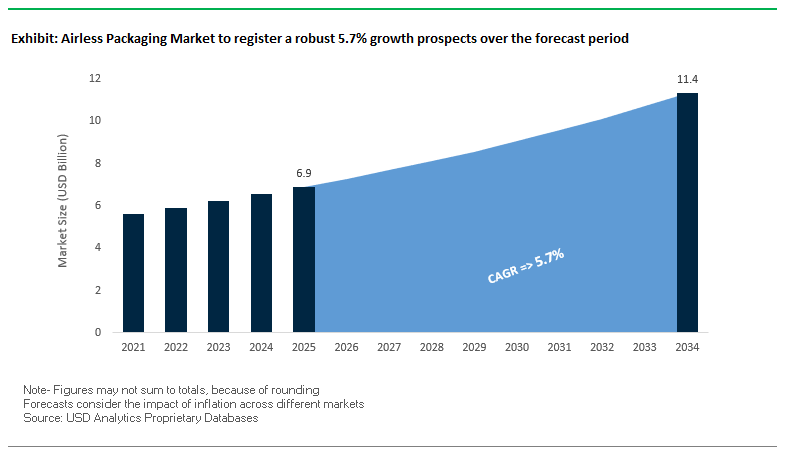

The global airless packaging market is projected to grow from USD 6.9 billion in 2025 to USD 11.4 billion by 2034, expanding at a CAGR of 5.7%. This growth underscores the industry’s pivotal role in safeguarding sensitive formulations, improving consumer experience, and reducing product and packaging waste. For industry professionals and buyers, airless technology has evolved into a strategic enabler that balances efficacy, safety, convenience, and sustainability, reshaping packaging choices across beauty, personal care, and pharmaceuticals.

Airless packaging has become indispensable for brands competing in categories where active ingredients, hygienic dispensing, and zero-waste functionality are top priorities. By ensuring nearly complete evacuation, preventing oxidation, and enabling refillable systems, airless formats are advancing both premiumization and eco-conscious innovation.

Key Insights for Industry Stakeholders

Protection of Active Ingredients: Over 70% of skincare products now contain actives like Vitamin C, retinoids, and peptides—airless systems protect these from oxygen and light degradation.

Precise Dosing in Healthcare: More than 40% of pharmaceutical applications require controlled, hygienic dosing, making airless packaging vital in topical and sterile treatments.

Zero-Waste Appeal: Around 50% of consumers actively prefer packaging that offers 95%+ product evacuation, aligning with the demand for waste-free formats.

Refillable Growth: Leading beauty brands are investing in refillable airless systems, driving repeat purchases and supporting global sustainability commitments.

Market Analysis: Recent Strategic Developments in the Airless Packaging Industry

The global airless packaging sector is undergoing rapid transformation, marked by investments in regional expansion, sustainability-focused innovation, and M&A consolidation. In January 2025, West Pharmaceutical Services reported strong growth in injectable delivery and containment components, signaling rising medical reliance on airless-compatible systems. By February 2025, Quadpack unveiled its Ultra Solo airless pack, a mono-material, metal-free solution fully recyclable in polyethylene streams—setting a benchmark for eco-design packaging.

The sustainability momentum carried into March 2025, where the Pharmapack event highlighted new industry research underscoring recyclability and refillability as central priorities. In April 2025, two major moves reshaped the market: Amcor and Berry Global agreed to merge in a $24 billion deal, creating a global leader in consumer and healthcare packaging; meanwhile, Aptar Beauty launched new locally produced airless solutions (Sierra, Moda, Luna) in Latin America to address regional needs through a “local-for-local” model.

Innovation and global reach continued to expand through mid-2025. July 2025 saw Quadpack invest in PET dip-in bottle production in Germany, strengthening capabilities for color cosmetics, while AptarGroup’s Q2 earnings release highlighted growth in Pharma and Closures driven by resilient demand for airless and dispensing systems. In August 2025, Albéa acquired Amfora Packaging, strategically deepening its presence in Latin America’s fast-growing beauty market. These moves collectively highlight how regional capacity expansion, M&A, and eco-innovation are setting the stage for long-term airless packaging dominance.

Emerging Trends and Opportunities Defining the Future of the Airless Packaging Market

Strategic Expansion into High-Growth Premium and Dermocosmetic Segments

Airless packaging is cementing its position as a critical enabler of product performance and brand identity in the skincare and dermocosmetic sectors. These categories depend heavily on ingredient efficacy, and airless systems deliver a unique advantage by preventing oxidation and contamination. Sensitive ingredients such as vitamin C, peptides, and antioxidants degrade quickly when exposed to air, but airless technology ensures their potency remains intact, enhancing consumer trust and reinforcing scientific efficacy claims. A notable development occurred in May 2025 when Aptar Beauty launched its Derma Series, a complete packaging line tailored to dermocosmetic brands that straddle the beauty and pharmaceutical sectors. The launch emphasized precision dispensing and enhanced protection, addressing the clinical performance demands of this niche. Moreover, the “clean beauty” movement is driving brands to minimize or eliminate chemical preservatives. Airless packaging, by maintaining a sterile, hermetically sealed environment, reduces the need for such additives, allowing brands to meet consumer expectations for natural and preservative-free formulations. This convergence of scientific performance and consumer wellness trends is making airless systems indispensable in the premium skincare market.

Accelerated Integration of Sustainable Materials and Circular Design Principles

Sustainability is emerging as a defining force in the evolution of airless packaging. While the technology already reduces waste by maximizing product evacuation, new innovations are targeting material circularity and recyclability. Packaging manufacturers are increasingly incorporating post-consumer recycled (PCR) content in polypropylene (PP) and polyethylene (PE) components of airless pumps, helping global beauty and personal care brands meet ambitious sustainability pledges. A significant breakthrough is the development of mono-material airless systems, where the entire pump and bottle are made from a single type of plastic, dramatically improving recyclability. Another fast-growing trend is refillability, particularly in the luxury market. Patented refillable systems now allow consumers to replace only the inner cartridge while reusing the outer bottle and actuator, significantly reducing plastic waste while offering a premium user experience. By combining recyclability, PCR integration, and refill systems, airless packaging is aligning with circular economy principles and strengthening its appeal to environmentally conscious brands and consumers alike.

Penetration into the Pharmaceutical and OTC Therapeutics Market

The pharmaceutical and over-the-counter (OTC) therapeutics sectors represent a high-value frontier for airless packaging, given their emphasis on safety, hygiene, and precision. Airless systems are ideally suited for topical medications such as creams and ointments that must maintain stability and potency over extended use. The closed, sterile design ensures that sensitive formulations are not compromised by repeated exposure, which is especially critical in clinical and home healthcare settings. Beyond hygiene, airless packaging offers controlled dosage, delivering a consistent and precise amount of medication with every pump. This accuracy is vital for therapeutic effectiveness and helps minimize the risks of under- or over-application. Multi-dose dispensing systems further extend the technology’s utility in medical environments where preventing contamination is paramount. With regulators and healthcare providers emphasizing patient safety and drug efficacy, airless technology is positioned to become an essential packaging solution in pharmaceutical and OTC product lines.

Addressing the Demand for Premiumization in Mass Market and Men’s Grooming Segments

Airless packaging is also moving beyond premium cosmetics and into mass-market skincare and men’s grooming, where it serves as a tool for premiumization and product differentiation. For mass-market brands, the technology solves one of the most common consumer frustrations: incomplete product evacuation. Vacuum-piston mechanisms ensure nearly 100% usage, enhancing perceived value and customer satisfaction. In the rapidly expanding men’s grooming market, airless packaging supports a masculine, modern aesthetic, offering sleek, functional designs that resonate with male consumers seeking sophistication and performance. Furthermore, airless systems help brands differentiate by highlighting product safety, efficiency, and innovation—benefits that jar- and tube-based competitors cannot match. With consumer expectations rising across categories, airless packaging is no longer a niche feature but a competitive necessity that allows brands to justify higher price points and capture loyalty in crowded markets.

Competitive Landscape: Key Companies Shaping the Future of Airless Packaging

The airless packaging industry is led by global packaging giants and niche innovators balancing R&D, design, sustainability, and regional expansion. These companies differentiate through technical precision, customizable aesthetics, refillability, and circular material adoption, positioning airless systems as essential for next-generation beauty and pharma packaging.

AptarGroup, Inc. expands global reach with local-for-local airless solutions

AptarGroup is a global leader in dispensing and drug delivery systems, offering an extensive portfolio of airless pumps, jars, and bottles for beauty, personal care, and pharmaceuticals. In April 2025, it launched new airless lines (Sierra, Moda, Luna) in Latin America under a local-for-local strategy, reducing lead times and enhancing regional agility. Aptar invests heavily in R&D, from recyclable nasal sprays to smart digital packaging, addressing both sustainability and connected-health needs. Its focus on mono-material solutions and targeted acquisitions strengthens its leadership in eco-innovation and global expansion.

Silgan Holdings Inc. leverages global network for sustainable dispensing

Silgan Holdings operates 123 manufacturing facilities worldwide, supplying a wide range of dispensing and specialty closures, including advanced airless systems. Known for its custom-engineered designs, Silgan tailors packaging to align with brand identity across healthcare and personal care markets. The company’s sustainability strategy includes partnerships with the Sustainable Packaging Coalition and the Ellen MacArthur Foundation, showcasing its commitment to circularity and PCR integration. Airless systems remain one of its high-value offerings, supporting its role as a versatile global supplier.

Albéa Group strengthens Latin American footprint with Amfora acquisition

Albéa Group is a major player in beauty packaging, providing airless solutions for skincare, fragrance, and makeup. Its August 2025 acquisition of Amfora Packaging reinforced its expansion in Latin America, one of the fastest-growing beauty regions. Albéa’s “Made to be Remade” strategy drives the development of refillable and mono-material designs, aligning with global sustainability mandates. It also provides turnkey services from concept to production, helping brands accelerate launches with customized, eco-conscious packaging.

Quadpack pioneers recyclable and design-led airless innovations

Quadpack is recognized for its design-driven and sustainable airless solutions, with a strong presence in the beauty industry. In February 2025, it introduced the Ultra Solo pack, a recyclable mono-material system without metal components, advancing its Positive-Impact Packaging philosophy. Its expansion into the U.S. market (2024) and new PET dip-in production line in Germany (July 2025) highlight its global growth strategy. By combining design innovation with sustainability, Quadpack positions itself as a key partner for brands seeking premium, recyclable airless packaging.

Pum-Tech Packaging delivers technical precision in airless pump design

Pum-Tech Packaging specializes in high-performance airless pump technology tailored for cosmetics and personal care markets. Its strength lies in consistent dosing and oxidation prevention, critical for formulations containing peptides, vitamins, and bio-actives. The company is advancing eco-friendly materials integration to align with global sustainability demands, while offering a broad portfolio of airless bottles and jars designed for varied product viscosities. By blending technical expertise with design flexibility, Pum-Tech remains a competitive force in niche, innovation-focused segments of the airless market.

Airless Packaging Market Share Insights

Market Share by Packaging Type in the Airless Packaging Industry

Bottles and jars dominate the global airless packaging market with a commanding 65% share in 2025, cementing their role as the gold standard for premium skincare and cosmetic applications. Their ability to deliver airtight protection against oxidation and microbial contamination makes them indispensable for high-value formulations such as serums, moisturizers, and anti-aging products. Beyond functionality, these formats provide a sleek, luxury-oriented aesthetic that aligns with the branding strategies of mass-tige and premium beauty players, making them integral to consumer perception of efficacy and quality. Airless tubes, with a 20% market share, have carved out a strong position in viscous formulations like creams, lotions, and masks. Their bottom-up dispensing technology not only ensures nearly 100% evacuation of the product but also eliminates the need for preservatives, aligning with clean beauty and sustainability trends. Pouches, though currently a smaller niche, represent an emerging frontier. They are increasingly used for travel-sized products, professional samples, and single-use applications, appealing to brands exploring lightweight, sustainable alternatives to rigid plastics. Finally, other innovative formats such as compacts, stick applicators, and hybrid dispensing solutions represent a dynamic growth area. These formats enable brands to differentiate through customization and specialized user experiences, often commanding premium pricing due to their novelty and application-specific utility.

Market Share by End-Use Industry in the Airless Packaging Industry

The personal care and cosmetics sector overwhelmingly dominates the airless packaging market, accounting for 85% of total demand in 2025. This leadership is tied directly to the sector’s reliance on packaging as a functional extension of the product itself. Sensitive ingredients such as retinoids, vitamin C, and organic extracts degrade quickly when exposed to air and light, making airless systems essential for product stability and marketing claims around potency and preservative-free formulations. The premiumization trend in beauty—especially in skincare—has elevated airless packaging into a key differentiator that directly enhances consumer trust and brand value. Healthcare and pharmaceuticals, holding a 10% share, represent a smaller but highly valuable niche. Applications include sterile ointments, wound care gels, and advanced dermatological treatments where preventing contamination and ensuring precise dosing are critical. Growth here is bolstered by the expansion of home healthcare and the need for packaging that balances medical-grade performance with patient usability. In food and beverage, adoption is limited to ultra-premium categories such as gourmet oils, condiments, and flavor extracts. While cost currently constrains broader uptake, the need for oxidation prevention keeps this segment relevant in high-value niches. The “other applications” category, covering sensitive chemicals, adhesives, and industrial compounds, reflects the untapped potential of airless systems outside traditional consumer markets. As costs decline and technology evolves, these non-traditional applications are expected to become more commercially viable, opening new revenue streams for packaging manufacturers.

United States: Sustainability, Premium Formulations, and Smart Dispensing Technologies Fuel Airless Packaging Growth

The United States is at the forefront of the airless packaging market, driven by a strong focus on sustainability and premium product protection. Leading companies such as Berry Global are investing in all-plastic, mono-material packaging like the Magic Star Light series, designed with plastic springs and certified for excellent recyclability. This innovation aligns with the country’s growing emphasis on sustainable packaging solutions and consumer demand for eco-conscious products. The rise of high-value skincare and cosmetic formulations containing sensitive active ingredients further fuels demand for airless packaging, as these solutions provide airtight barriers that preserve efficacy and extend shelf life.

Technological innovation in precision pumps and vacuum-sealed dispensers is another major trend, ensuring accurate dosing while minimizing waste an important factor for both premium beauty brands and eco-conscious consumers. The U.S. market is also seeing strong merger and acquisition activity, with AptarGroup’s acquisition of Fusion Packaging enhancing its premium airless and color cosmetics portfolio. Together, these factors reinforce the U.S. as a global leader in sustainable and technologically advanced airless packaging solutions.

Germany: Circular Economy Leadership and Preservative-Free Packaging Innovation

Germany stands out as a leader in the circular economy for airless packaging, driven by stringent environmental regulations and strong consumer preference for sustainable solutions. Manufacturers are increasingly using post-consumer recycled (PCR) content in airless systems, reflecting both regulatory compliance and consumer demand for recyclable solutions. Collaborative innovation among German companies is also paving the way for new airless designs aligned with Europe’s advanced recycling infrastructure, ensuring functionality without compromising sustainability.

Another defining trend is the growing demand for “clean beauty” products without preservatives, which rely heavily on airless packaging to provide hygienic, airtight protection that maintains product integrity naturally. This unique positioning allows German brands to cater to environmentally conscious and health-focused consumers while advancing in a highly regulated market.

France: Luxury Cosmetics Driving Demand for Sustainable and Refillable Airless Packaging

France, as a global hub for luxury cosmetics and perfumes, is a critical driver of growth in the airless packaging market. The country’s high-end beauty sector depends on airless solutions to protect sensitive formulations while providing a premium consumer experience. Regulatory compliance also plays a major role, with the EU’s Packaging and Packaging Waste Regulation (PPWR) pushing French companies toward waste reduction, recyclability, and sustainable materials.

In line with the country’s sustainability agenda, leading firms are developing refillable and reusable airless systems. For instance, Albéa partnered with L’Oréal to create a refillable pump for Lancôme skincare, showcasing how France is merging luxury with sustainability. By integrating eco-friendly design with the prestige of its global cosmetics brands, France is setting the benchmark for sustainable premium airless packaging.

China: E-Commerce Growth and Sustainability Reshaping Airless Packaging Demand

China’s booming cosmetics and skincare market—fueled by its expanding middle class and higher disposable incomes—is significantly increasing demand for both domestic and international brands, making it one of the largest and fastest-growing markets for airless packaging. Chinese manufacturers are advancing rapidly in technological innovation, producing cost-effective airless systems for mass-market products while also developing premium packaging for luxury lines.

The government’s strong emphasis on sustainability and environmental protection is accelerating the use of eco-friendly solutions, including glass airless packaging and biodegradable materials. Additionally, the country’s dominant e-commerce platforms are shaping packaging requirements, with a need for durable, visually appealing formats that withstand shipping logistics while maintaining premium aesthetics. This combination of technology, sustainability, and digital retail influence places China at the center of future airless packaging growth.

Japan: Bio-Based Materials and Technological Precision Elevating Airless Packaging Market

Japan’s pharmaceutical and cosmetics packaging sector is heavily influenced by consumer demand for safety and quality, making airless packaging a preferred solution to protect sensitive formulations and prevent contamination. Japanese companies are also pioneering in the adoption of bio-based plastics such as bio-polypropylene (bio-PP), working closely with chemical producers and trading firms to reduce greenhouse gas emissions and meet national sustainability objectives.

Innovation remains a core strength, with Japanese manufacturers developing advanced airless systems such as dual-chamber dispensers for products requiring ingredient mixing, as well as airless jars with “Fresh Lock System” technology. These solutions address the country’s high standards for product safety while supporting eco-friendly initiatives, reinforcing Japan’s reputation as a leader in technologically advanced and sustainable airless packaging.

South Korea: K-Beauty and Smart Packaging Technologies Accelerating Market Growth

South Korea’s K-beauty industry is a global powerhouse, driving strong demand for airless packaging, particularly for cosmeceuticals and clean beauty products that contain active ingredients sensitive to oxidation and contamination. This has made airless tubes and other hygienic solutions the packaging of choice for local and international brands.

The country is also emerging as the fastest-growing market for airless packaging technologies, with rapid adoption of new formats that cater to evolving consumer expectations of safety, hygiene, and sustainability. South Korean manufacturers are pushing boundaries with smart packaging integration, embedding QR codes, NFC tags, and AI-based solutions to enhance consumer engagement and provide product authentication. This blend of technology, beauty innovation, and eco-conscious design ensures South Korea’s strong global influence in the future of airless packaging.

Airless Packaging Market Report Scope

Airless Packaging Market

Parameter

Details

Market Size (2025)

$6.9 Billion

Market Size (2034)

$11.4 Billion

Market Growth Rate

5.7%

Segments

By Packaging Type (Bottles & Jars, Tubes, Pouches, Other Formats), By Dispensing System (Pump, Dropper, Other Dispensers), By Material (Plastic, Glass, Others), By End-Use Industry (Personal Care & Cosmetics, Healthcare & Pharmaceutical, Food & Beverage, Other Applications)

Study Period

2019- 2024 and 2025-2034

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Airless Packaging Market Segmentation

By Packaging Type

Bottles & Jars

Tubes

Pouches

Other Formats

By Dispensing System

Pump

Dropper

Other Dispensers

By Material

Plastic

Glass

Others

By End-Use Industry

Personal Care & Cosmetics

Healthcare & Pharmaceutical

Food & Beverage

Other Applications

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Airless Packaging Market

AptarGroup, Inc.

Berry Global Group, Inc.

Silgan Holdings Inc.

Albéa S.A.

Mondi plc

HCP Packaging

Quadpack Industries S.L.

Lumson S.p.A.

Fusion Packaging

Comar, LLC

Raepak Ltd.

Yonwoo Corporation

RPC Group Plc

Coster Group S.p.A.

Libo Cosmetics Co., Ltd.

* List Not Exhaustive

Research Coverage

This report investigates the global airless packaging market through a focused lens on ingredient protection, dosing accuracy, refillability, and circular-design innovations; it synthesizes recent commercial pilots, material-technology breakthroughs, and region-specific scale-up activity to show where product performance and sustainability intersect. The analysis reviews industry consolidation, local-for-local manufacturing moves, and regulatory factors shaping recyclability and medical adoption, and highlights strategic use-cases across dermocosmetics, pharma, and mass-market grooming. Drawing on proprietary modelling and expert interviews, USDAnalytics maps adoption pathways, commercialization risks, and priority investment themes—this report is an essential resource for packaging strategists, R&D leads, procurement teams, and sustainability officers seeking practical, evidence-based guidance to de-risk launches and accelerate circular design.

Scope Highlights

Segmentation: By Packaging Type (Bottles & Jars, Tubes, Pouches, Other Formats); By Dispensing System (Pump, Dropper, Other Dispensers); By Material (Plastic, Glass, Others); By End-Use Industry (Personal Care & Cosmetics, Healthcare & Pharmaceutical, Food & Beverage, Other Applications).

Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

Timeframe: Historical series (2021–2024) with forecasts covering 2025–2034.

Companies: Includes analysis and profiles of 15+ key players across pumps, converters, and material suppliers (e.g., AptarGroup, Quadpack, Albéa, Pum-Tech, Silgan).

Methodology

Our approach combines primary interviews with packaging engineers, brand marketing and procurement leads, materials scientists, and supply-chain managers across target regions, plus rigorous secondary research from corporate disclosures, patent databases, trade events, and validated shipment data; market sizing uses a hybrid bottom-up/top-down model that reconciles installed production capacity, SKU-level penetration by category, and channel dynamics (retail vs. e-commerce). Technology adoption curves were informed by pilot deployments and supplier roadmaps, while lifecycle and recyclability assessments applied industry-standard LCA inputs and local recycling-stream assumptions. Sensitivity scenarios test impacts from PCR availability, mono-material conversions, and regional policy shifts—producing investment-grade forecasts and prioritized tactical recommendations.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

2. Airless Packaging Market Landscape & Outlook (2025–2034)

2.1. Introduction to Airless Packaging Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers and Barriers (Premiumization, Active Ingredient Protection)

2.4. Regulatory and Sustainability Pressures (Recyclability, PCR, Refillable Systems)

2.5. Channel Dynamics: Retail, E-commerce and Regional Demand Patterns

3. Innovations Reshaping the Airless Packaging Market

3.1. Trend: Mono-material and Refillable System Design

3.2. Trend: Precision Dosing and Vacuum-Piston Mechanisms

3.3. Opportunity: Penetration into Pharma and OTC Therapeutics

3.4. Opportunity: Dermocosmetic and Mass-Market Premiumization

4. Strategic Investments and Capacity Expansion

4.1. Mergers, Acquisitions, and Regional Consolidation

4.2. Local-for-Local Manufacturing and Capacity Builds

4.3. R&D in Sustainable Materials and PCR Integration

4.4. Commercialization of New Formats and Lines

5. Market Share and Segmentation Insights: Airless Packaging Market

5.1. By Packaging Type

5.1.1. Bottles & Jars

5.1.2. Tubes

5.1.3. Pouches

5.1.4. Other Formats

5.2. By Dispensing System

5.2.1. Pump

5.2.2. Dropper

5.2.3. Other Dispensers

5.3. By Material

5.3.1. Plastic

5.3.2. Glass

5.3.3. Others

5.4. By End-Use Industry

5.4.1. Personal Care & Cosmetics

5.4.2. Healthcare & Pharmaceutical

5.4.3. Food & Beverage

5.4.4. Other Applications

5.5. By Value Chain Role (Converters, Pump OEMs, Brand Owners)

5.1.1, 5.1.2 … vary according to provided segmentation in text

6. Country Analysis and Outlook of Airless Packaging Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Airless Packaging Market Size Outlook by Region (2025–2034)

7.1. North America Airless Packaging Market Size Outlook to 2034

7.1.1. By Packaging Type

7.1.2. By Dispensing System

7.1.3. By Material

7.1.4. By End-Use Industry

7.2. Europe Airless Packaging Market Size Outlook to 2034

7.2.1. By Packaging Type

7.2.2. By Dispensing System

7.2.3. By Material

7.2.4. By End-Use Industry

7.3. Asia Pacific Airless Packaging Market Size Outlook to 2034

7.3.1. By Packaging Type

7.3.2. By Dispensing System

7.3.3. By Material

7.3.4. By End-Use Industry

7.4. South America Airless Packaging Market Size Outlook to 2034

7.4.1. By Packaging Type

7.4.2. By Dispensing System

7.4.3. By Material

7.4.4. By End-Use Industry

7.5. Middle East and Africa Airless Packaging Market Size Outlook to 2034

7.5.1. By Packaging Type

7.5.2. By Dispensing System

7.5.3. By Material

7.5.4. By End-Use Industry

7.1.1, 7.1.2 … vary according to provided segmentation in text

8. Company Profiles: Leading Players in the Airless Packaging Market

8.1. AptarGroup, Inc.

8.2. Berry Global Group, Inc.

8.3. Silgan Holdings Inc.

8.4. Albéa S.A.

8.5. Mondi plc

8.6. HCP Packaging

8.7. Quadpack Industries S.L.

8.8. Lumson S.p.A.

8.9. Fusion Packaging

8.10. Comar, LLC

8.11. Raepak Ltd.

8.12. Yonwoo Corporation

8.13. RPC Group Plc

8.14. Coster Group S.p.A.

8.15. Libo Cosmetics Co., Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Airless Packaging Market Segmentation

By Packaging Type

Bottles & Jars

Tubes

Pouches

Other Formats

By Dispensing System

Pump

Dropper

Other Dispensers

By Material

Plastic

Glass

Others

By End-Use Industry

Personal Care & Cosmetics

Healthcare & Pharmaceutical

Food & Beverage

Other Applications

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Airless systems dramatically reduce oxygen and microbial ingress, preserving labile actives (vitamin C, retinoids, peptides) and enabling preservative-reduction strategies. For brands, this translates into longer in-use stability, stronger efficacy claims, and differentiation in premium segments where potency and “clean” formulations are marketed.

Mono-material pumps and cartridges eliminate mixed-material assemblies that block recycling; when the entire unit shares a single polymer family (e.g., PP or PE), it can enter existing recycling streams. Refillable outer housings paired with replaceable inner cartridges reduce waste volumes while preserving the hermetic, dosing benefits of airless tech.

Prioritize validated compatibility (extractables/leachables), dosing accuracy, and regulatory compliance for sterile pathways. Airless formats must pass container-closure integrity testing and stability studies; RTU/RTF-compatible cartridges and pharma-grade materials accelerate qualification and reduce contamination risk in clinical and commercial fill-finish.

Right-sizing, robust outer cartons with protective inserts, and securing inner cartridges against actuator movement reduce compression and actuator failures. Local-for-local manufacturing and closer inventory nodes also shorten transit, lowering breakage risk and supporting sustainable last-mile fulfillment.

Start with highest-volume SKUs: convert to mono-material constructions, increase PCR content in non-critical components, and pilot refill programs where consumer economics support repurchase. Simultaneously engage recyclers and run localized take-back pilots to verify circularity claims and close the loop operationally.