Architectural Metal Coatings Market Size and Growth Driven by Sustainable Facade Solutions and High-Performance Materials

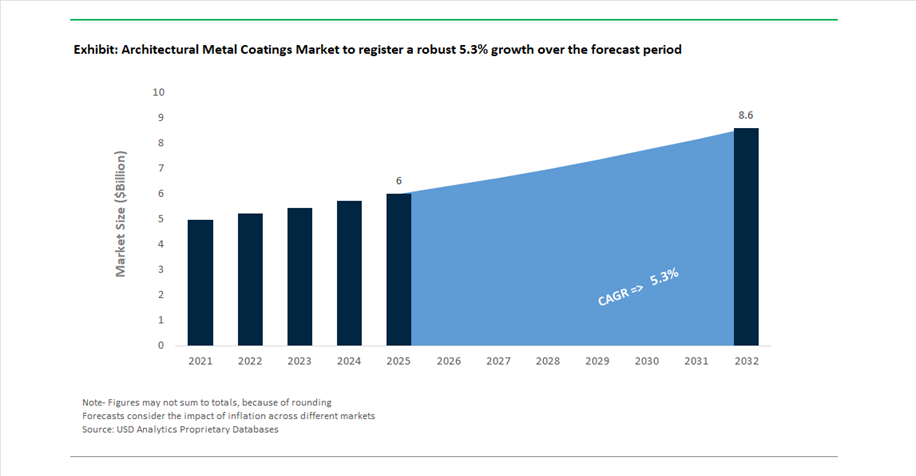

The Architectural Metal Coatings Market is projected to grow from USD 6 billion in 2025 to USD 8.61 billion by 2032, registering a CAGR of 5.3%. This growth is driven by the increasing adoption of advanced protective coatings for aluminum and steel structures, particularly in high-rise buildings, commercial complexes, and modern infrastructure projects. As urban skylines evolve, the demand for coatings that provide long-term durability, weather resistance, and aesthetic consistency is intensifying.

Architectural metal coatings are critical for protecting building envelopes against UV radiation, corrosion, moisture ingress, and temperature fluctuations, ensuring structural longevity and reducing maintenance costs. High-performance systems such as polyvinylidene fluoride (PVDF), polyester, and fluoropolymer coatings are widely used due to their superior color retention, gloss stability, and resistance to environmental degradation. These properties are essential for maintaining the visual and structural integrity of curtain walls, roofing systems, window frames, and façade panels over extended lifecycles.

A major market driver is the global shift toward sustainable and energy-efficient construction, where coatings play a key role in improving thermal performance and environmental compliance. Innovations such as cool-roof coatings, solar-reflective pigments, and energy-generating façade systems are gaining traction as developers pursue Net Zero building targets and green certifications. Additionally, the integration of low-VOC and bio-based coating technologies is aligning the market with evolving environmental regulations and ESG commitments.

The market is also benefiting from increasing investments in commercial construction, infrastructure modernization, and smart building technologies, particularly in emerging economies. Competitive dynamics are shaped by material innovation, strategic collaborations, and capacity expansion, positioning architectural metal coatings as a critical component of next-generation building design and performance

Low-Carbon Innovation, Strategic M&A, and Advanced Facade Technologies Transforming Market Dynamics

The architectural metal coatings market is undergoing significant transformation driven by sustainability-focused innovation, strategic consolidation, and advancements in façade technologies. A major development occurred in March 2026, when AkzoNobel and Axalta announced a merger of equals, creating a global coatings leader with enhanced capabilities in architectural metal coatings and high-performance resin systems. This consolidation integrates AkzoNobel’s Interpon and Sikkens brands with Axalta’s advanced coating technologies, accelerating innovation in durable and sustainable metallic finishes.

Sustainability initiatives are at the forefront of market evolution. In September 2025, AkzoNobel, Arkema, and BASF partnered to develop low-carbon powder coatings using bio-based resins and mass-balance certified materials. This collaboration aims to provide architects and developers with environmentally responsible coating solutions for aluminum window frames, curtain walls, and structural metal components. Complementing this, AkzoNobel’s October 2025 agreement to supply coatings for solar-absorbing wall technology highlights the convergence of coatings with energy generation systems, enabling building facades to contribute to thermal energy capture and efficiency.

Technological advancements are enhancing both performance and energy efficiency. PPG’s DURANAR® and CORAFLON® innovations, showcased at the AIA Conference on Architecture, introduce cool-surface pigment technologies that improve the solar reflectance index (SRI) of metal roofing and cladding, helping mitigate urban heat island effects. Similarly, Jotun’s next-generation powder coatings are designed for extreme environmental conditions (C5VH/CX ratings), offering superior corrosion protection for architectural and energy infrastructure applications.

Market growth is further supported by strong demand for premium finishes and design flexibility. Valspar’s “Warm Eucalyptus” color launch (August 2025) reflects the increasing importance of aesthetic customization in architectural metal applications, while maintaining high-performance standards. Additionally, Nippon Paint’s “Design-to-Factory” (D2F) strategy is improving project timelines by reducing lead times for complex architectural coatings, particularly in high-end commercial and industrial projects.

AAMA 2605 Specification Mandates Elevating Durability and Aesthetic Benchmarks

The architectural metal coatings industry is witnessing a decisive shift toward higher performance specifications as AAMA 2605 standards become the baseline requirement for commercial projects, particularly for structures exceeding four stories. This transition reflects a growing emphasis on long-term durability, color stability, and environmental resistance in high-value architectural applications. Lower-tier systems such as AAMA 2603 and 2604 are increasingly excluded from premium tenders, consolidating demand around high-performance fluoropolymer-based coatings.

Under current AAMA 2605 protocols, coatings must demonstrate exceptional color retention, with a maximum allowable color shift of 5 ΔE units after ten years of South Florida weathering exposure. This requirement has accelerated the phase-out of conventional polyester systems that cannot meet these stringent benchmarks. PVDF coatings, particularly those with 70% fluoropolymer content, are emerging as the dominant solution, consistently maintaining chalk ratings of 8 or higher over extended exposure periods, ensuring long-term facade integrity.

Gloss retention is another critical performance parameter. Advanced FEVE resin systems are demonstrating the ability to retain over 80% of their original gloss after a decade of high ultraviolet exposure, significantly outperforming silicone-modified polyester alternatives. In addition, updated erosion resistance requirements mandate a minimum of 40 liters per mil in sand abrasion testing, ensuring coatings can withstand harsh environmental conditions such as coastal winds and desert particulates.

These elevated performance criteria are reshaping procurement strategies across the construction industry, favoring coating systems that deliver superior lifecycle performance, reduced maintenance costs, and enhanced aesthetic longevity.

Chromate-Free Pretreatment Technologies Driving Sustainable Metal Finishing

The global transition toward chromate-free pretreatment systems is fundamentally transforming architectural metal coating processes. Regulatory frameworks, particularly under EU REACH, have moved into strict enforcement phases that effectively eliminate the use of hexavalent chromium in metal finishing operations. This shift is driving widespread adoption of alternative pretreatment chemistries based on zirconium and titanium compounds.

The environmental impact of this transition is substantial. Eliminating chromate-based systems can reduce hazardous sludge generation by up to 90% in aluminum extrusion facilities, significantly lowering waste disposal costs and environmental liabilities. At the same time, modern chromate-free conversion coatings are delivering comparable, and in some cases superior, performance. These systems have demonstrated the ability to withstand more than 3,000 hours of acetic acid salt spray testing, meeting the durability requirements of high-performance standards such as Qualicoat Seaside.

Operational efficiency is also improving. Chromate-free processes typically operate at lower temperatures than traditional chromating systems, resulting in energy savings of approximately 15% during pretreatment operations. This contributes to reduced operational costs and aligns with broader sustainability goals within the coatings and construction industries.

By 2026, more than 85% of architectural metal coaters in North America and Europe have transitioned away from hexavalent chromium-based systems, reflecting a near-complete industry shift toward environmentally compliant technologies.

Data Center Infrastructure Driving Demand for Low-Gloss, High-Performance Metal Coatings

The rapid expansion of data center infrastructure, fueled by artificial intelligence and cloud computing growth, is creating a specialized demand segment for architectural metal coatings. These facilities require coatings that balance aesthetic precision with functional performance, particularly for cabinet cladding and exterior facade panels.

One of the key requirements in this segment is gloss control. Super-matte coatings with gloss levels below 10 units are increasingly specified to minimize light reflection and prevent interference with sensitive optical and laser-based monitoring systems within server environments. At the same time, these coatings must maintain a high level of distinctness of image to support branding and visual consistency in high-profile data center projects.

Thermal management is another critical factor. Infrared-reflective coatings are being deployed on data center facades to reduce surface temperatures by up to 15°C, directly lowering cooling loads and improving energy efficiency. This is particularly important given the high energy consumption associated with data center operations.

Durability requirements are equally stringent. Coatings used on server enclosures and structural components must achieve pencil hardness ratings between H and 2H to withstand frequent mechanical handling and maintenance activities. Additionally, there is growing demand for electrostatic dissipative coatings that prevent static buildup, protecting sensitive electronic equipment from potential damage.

Anti-Graffiti Coatings Creating Sustainable Solutions for Urban Infrastructure Protection

The expansion of urban transit systems and high-density developments is driving increased demand for anti-graffiti coatings on architectural metal surfaces. Materials such as aluminum composite panels and perforated steel used in transit stations and public buildings are frequent targets for vandalism, creating ongoing maintenance challenges for operators.

Permanent anti-graffiti coatings are emerging as a preferred solution, offering long-term protection integrated directly into the architectural finish. These coatings, often based on silicone-modified or fluoropolymer chemistries, can withstand more than 24 cycles of aggressive solvent cleaning without loss of gloss or surface integrity. This represents a significant improvement over traditional sacrificial coatings, which typically fail after one or two cleaning cycles.

From an economic perspective, the adoption of permanent anti-graffiti systems can reduce facade maintenance costs by up to 60%, as they eliminate the need for repainting or abrasive cleaning methods. Environmental benefits are also notable. These coatings enable graffiti removal using mild, biodegradable cleaning agents, reducing water consumption and chemical usage by approximately 40% compared to conventional maintenance practices.

In addition to vandalism resistance, these coatings provide enhanced UV protection, adding an extra protective layer that shields underlying finishes from degradation in urban environments characterized by high pollution and heat exposure. As cities continue to invest in sustainable infrastructure, anti-graffiti architectural metal coatings are becoming a standard specification, combining durability, cost efficiency, and environmental performance.

Architectural Metal Coatings Market Share and Segmentation Insights

Market Share by Coating Technology: Powder Coatings Lead with Sustainability-Driven Adoption (48%)

Powder coatings dominate the architectural metal coatings market with a commanding 48% market share in 2025, underpinned by a structural shift toward low-VOC, environmentally compliant coating technologies. As global construction stakeholders increasingly align with green building certifications such as LEED and BREEAM, powder coatings have emerged as the preferred solution for exterior architectural applications including aluminum facades, curtain wall systems, and window frames. Their near-zero VOC emissions, combined with superior transfer efficiency exceeding 95% through reclaim systems, position them as both a regulatory-compliant and cost-efficient technology. Additionally, powder coatings deliver exceptional durability metrics such as high resistance to UV-induced chalking, color fading, and environmental degradation, making them the default coating technology for high-rise building cladding and roofing systems. While liquid coatings such as PVDF, polyester, and silicone-based systems continue to serve high-performance niches, particularly in extreme weather environments, the overall market momentum is clearly shifting toward powder-based solutions due to lifecycle cost advantages and sustainability mandates.

Market Share by Structural Application: Roofing and Cladding Segment Captures 38% Share Amid High Exposure Demand

Roofing and cladding represent the largest structural application segment in the architectural metal coatings market, accounting for 38% of total demand in 2025. This dominance is primarily driven by the extensive surface area these components occupy across commercial, industrial, and residential building envelopes, making them the highest-volume consumers of architectural coatings. More critically, roofing and cladding systems are directly exposed to harsh environmental conditions, necessitating coatings with superior weathering performance, including long-term UV resistance, corrosion protection, and color retention over 20 to 40-year lifecycle warranties. As a result, high-performance coating technologies such as PVDF liquid coatings and super-durable polyester powder coatings are widely specified for these applications. The segment’s growth is further supported by the global expansion of urban infrastructure and high-rise construction, particularly in Asia-Pacific and the Middle East, where façade aesthetics and long-term durability are key procurement criteria. Consequently, roofing and cladding continue to anchor demand in the architectural metal coatings market, reinforcing their position as the most critical application segment.

Architectural Metal Coatings Market Competitive Landscape Driven by PVDF Technology and Sustainable Powder Innovations

The architectural metal coatings market is driven by PVDF coatings, super durable powder coatings, and low-VOC waterborne formulations. Leading players are focusing on coil coatings, aluminum extrusions, and curtain wall systems to deliver long lifecycle performance, energy efficiency, and regulatory-compliant solutions across commercial construction and infrastructure projects.

AkzoNobel leads architectural metal coatings with low-energy curing and merger-driven scale

AkzoNobel is a global leader in architectural metal coatings, strengthened by its $25 billion merger with Axalta in 2026, targeting $600 million in synergies across coil and extrusion coatings. The company reported €1.44 billion in adjusted EBITDA in 2025 with a 14.2% margin, reflecting strong operational efficiency. Its Interpon D1036 Low-E powder coating cures at temperatures 30°C lower than standard systems, reducing energy consumption by up to 20% in metal coating processes. The company maintains leadership in super durable powder coatings for aluminum extrusions, meeting Qualicoat Class 1 and 2 standards for high-rise construction. Product innovation focuses on energy-efficient coatings and sustainable architectural applications.

PPG Industries dominates PVDF architectural coatings with long-life façade protection systems

PPG Industries holds a leading position in architectural metal coatings through its advanced PVDF coating technologies. Its DURANAR® coatings use 70% PVDF resins to provide up to 50 years of durability for metal façades in extreme UV and coastal environments. The company transitioned its portfolio to low-VOC water-based formulations to comply with global environmental regulations while maintaining performance. Adoption of electrostatic application technology has reduced overspray by 40% in large-scale metal panel production. Strategic investments exceeding $380 million are focused on smart coatings with infrared-reflective pigments to reduce building cooling loads. Product development emphasizes durability, sustainability, and energy efficiency.

Sherwin-Williams expands coil coatings leadership with green-certified and high-productivity systems

Sherwin-Williams leverages its Valspar® and Fluropon® brands to dominate the coil coatings segment, supplying finishes for over 60% of metal roofing in North America. Its Fluropon Pure line is compliant with Living Building Challenge Red List standards, supporting green building certifications for hospitals and schools. The company announced a major capacity expansion in Kentucky in 2026 to meet rising demand for polyester and fluoropolymer coatings. Its Direct-to-Metal acrylic coatings reduce application steps by 33%, improving contractor productivity in labor-constrained environments. Product development focuses on sustainable coatings and high-efficiency application systems.

Axalta strengthens architectural metal coatings with super durable powders and UV-curable technologies

Axalta Coating Systems is a key player in architectural metal coatings, supported by strong financial performance with $1.13 billion adjusted EBITDA and a 22% margin in 2025. The company’s Alesta SD powder coatings deliver high durability and antimicrobial protection for metal surfaces, including medical device housings. Its UV-curable powder technology enables rapid curing on temperature-sensitive metal substrates, reducing manufacturing energy consumption by 15%. Strategic focus includes expanding mobility and industrial coatings into architectural metal applications. Product innovation centers on performance coatings and sustainable manufacturing processes.

Nippon Paint drives APAC architectural metal coatings growth with AI innovation and infrastructure focus

Nippon Paint Holdings leads growth in the APAC architectural metal coatings market, under its 2026 strategy. The company dominates infrastructure coatings for bridges and industrial plants, supported by strong demand in China, India, and Southeast Asia. Its AOC division is prioritizing sustainable coatings, with 59% of its development portfolio focused on environmentally friendly solutions. AI-driven innovation initiatives aim to develop heat-insulating and low-emission coating technologies. The company also leads in anti-corrosive silyl coatings for maritime and industrial infrastructure. Product development focuses on durability, sustainability, and large-scale infrastructure applications.

United States Architectural Metal Coatings Market: PFAS-Free Transition and High-Performance PVDF Innovation Driving Growth

The United States architectural metal coatings market is undergoing a major transformation, led by sustainability mandates and high-performance material innovation. A significant shift toward PFAS-free fluoropolymer alternatives is already underway, with nearly 80% of coating portfolios transitioning to non-fluorinated systems to comply with tightening environmental regulations. This is reshaping the competitive landscape, especially in coil and extrusion coating segments.

Technological advancements are also redefining product performance. The development of cool-roof metal coatings (SRI >110) is improving energy efficiency in large infrastructure such as data centers, reducing HVAC loads significantly. Additionally, the introduction of antiviral-infused metal coatings for high-touch surfaces like airport infrastructure is expanding application scope. Investments in next-generation PVDF coatings with 40-year color retention are further enhancing durability in extreme climates. The growing use of coated metal in EV battery gigafactories highlights the increasing importance of coatings that can withstand thermal cycling and industrial stress.

China Architectural Metal Coatings Market: High-Volume Production and Green Building Compliance Accelerating Adoption

China dominates the architectural metal coatings market in terms of scale, supported by massive production of pre-painted galvanized steel (PPGI) and strong regulatory push toward sustainability. Updated green building standards mandate low-VOC waterborne coatings, accelerating the shift away from solvent-based systems.

Innovation is a key growth driver, with photocatalytic TiO₂-coated aluminum facades being deployed to reduce urban air pollution by neutralizing NOx emissions. Infrastructure expansion, particularly under the Belt and Road Initiative, is driving demand for graphene-enhanced anti-corrosion coatings for bridges and marine structures. Additionally, advancements in aesthetic coatings such as wood-grain and liquid-granite finishes are expanding architectural design possibilities. Strict environmental tax enforcement is also accelerating the adoption of powder coatings, reinforcing China’s leadership in both volume and innovation.

Germany Architectural Metal Coatings Market: Circular Economy Leadership and Low-Temperature Cure Technologies

Germany sets the global benchmark for sustainable architectural metal coatings through its strong focus on circular economy principles and advanced material science. The introduction of low-temperature cure (LTC) powder coatings (≈130°C) is enabling coating of hybrid materials without thermal degradation, expanding application flexibility.

Regulatory frameworks such as the EU Circular Economy Act are mandating recycling-compatible coatings, ensuring that coated metals can be reprocessed without contamination. Innovations in bio-based resins derived from lignin and castor oil are significantly reducing carbon footprints. Additionally, infrastructure projects are driving demand for infrared-reflective coatings in metal cladding systems to improve building energy efficiency. The use of scratch-resistant and anti-graffiti coatings in public transport further highlights Germany’s leadership in high-performance, sustainable coating technologies.

Saudi Arabia Architectural Metal Coatings Market: Mega-Project Demand and Desert-Grade Coatings Driving Expansion

Saudi Arabia’s architectural metal coatings market is experiencing rapid growth, fueled by Vision 2030 and large-scale infrastructure projects such as NEOM. These developments are generating strong demand for PVDF-based coatings capable of withstanding extreme desert conditions, including sand abrasion and high temperatures.

Innovations in “desert-grade” coatings are maintaining reflectivity even under dust accumulation, improving energy efficiency. Regulatory mandates are also shaping the market, with requirements for heat-reflective roofing coatings and intumescent fire-retardant systems in high-rise buildings. The localization of production, including new powder coating facilities, is strengthening supply chains. Additionally, antimicrobial-coated aluminum panels are being widely used in metro systems and healthcare infrastructure, highlighting the growing role of multifunctional coatings.

India Architectural Metal Coatings Market: Infrastructure Boom and Transition to PVDF Systems Driving Growth

India’s architectural metal coatings market is rapidly evolving, supported by large-scale infrastructure investments and government incentives. The shift from basic polyester coatings to super-durable PVDF and polyurethane systems is enhancing performance, particularly in high-corrosion coastal environments.

Major infrastructure projects, including airport expansions and high-speed rail networks, are driving demand for anti-graffiti and high-gloss metal coatings. The Production Linked Incentive (PLI) scheme is strengthening domestic manufacturing of specialty resins, reducing reliance on imports. Additionally, the development of food-safe antimicrobial coatings for storage and agricultural applications is expanding market scope. Investments by leading players in dedicated production lines are further boosting capacity, positioning India as a key growth market.

Japan Architectural Metal Coatings Market: Nanotechnology Innovation and Seismic-Resilient Coatings Leadership

Japan’s architectural metal coatings market is defined by its leadership in nanotechnology and advanced material engineering. The widespread adoption of self-cleaning hydrophilic coatings is reducing maintenance requirements for high-rise buildings, particularly in dense urban environments.

Technological innovation is also focused on seismic-resilient coatings, with high-elongation materials capable of bridging cracks during earthquakes without delamination. The development of soft-touch antimicrobial coatings is addressing safety needs in aging population infrastructure. Additionally, innovations such as micro-texture coatings that physically disrupt pathogens are redefining antimicrobial performance. Integration of antiviral coatings in smart window systems further highlights Japan’s leadership in multifunctional coating technologies.

Brazil Architectural Metal Coatings Market: Mineral Resource Advantage and Anti-Corrosive Coatings Driving Growth

Brazil’s architectural metal coatings market benefits from strong raw material availability and expanding infrastructure investments. The country’s leadership in titanium dioxide production enables cost-effective manufacturing of high-performance coatings.

Infrastructure development programs are driving demand for anti-corrosion and anti-carbonation coatings for bridges and transport systems. Innovations in bio-based resins derived from sugarcane waste are supporting sustainability initiatives. The agricultural sector is also a key driver, with increasing use of zinc-rich antimicrobial coatings for machinery and storage structures. Additionally, eco-labeling requirements are encouraging the adoption of low-solvent coatings, reinforcing Brazil’s position as a major player in sustainable architectural metal coatings.

United Kingdom Architectural Metal Coatings Market: Graphene Integration and Regulatory Evolution Driving Innovation

The United Kingdom architectural metal coatings market is evolving through strong innovation in advanced materials and regulatory divergence post-Brexit. The adoption of graphene-enhanced coatings is significantly improving corrosion resistance, particularly in coastal infrastructure and modular construction.

Regulatory frameworks under the Building Safety Act are enforcing stricter fire safety standards, including mandatory use of A1/A2 fire-rated coatings in residential buildings. The expansion of EV charging infrastructure is driving demand for antiviral powder coatings on public interfaces. Additionally, innovations in heritage preservation coatings are enabling protection of historic metal structures without altering their appearance. The UK’s focus on advanced materials and regulatory flexibility positions it as a leader in next-generation architectural metal coatings.

Architectural Metal Coatings Market Report Scope

Architectural Metal Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2032)

|

$8.6 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Resin Chemistry (Fluoropolymers, Polyester, Polyurethane, Epoxy, Silicone-Modified Polymers, Acrylic), By Coating Technology (Liquid Coatings, Powder Coatings, UV-Cured and Radiation Curable Systems, Anodizing and Conversion Coatings), By End-Use Sector (Commercial, Residential, Industrial, Public Infrastructure), By Structural Application (Roofing and Cladding, Wall Panels and Facades, Doors and Windows, Fascia, Soffits and Gutters, Interior Architectural Metalwork), By Performance Property (Corrosion and Chemical Resistance, UV and Weathering Resistance, Aesthetic and Decorative, Functional Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Beckers Group, BASF SE, Jotun A/S, Hempel A/S, Tiger Coatings GmbH & Co. KG, KCC Corporation, Arkema S.A., Asian Paints Limited, Tnemec Company, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Architectural Metal Coatings Market Segmentation

By Resin Chemistry

- Fluoropolymers

- Polyester

- Polyurethane

- Epoxy

- Silicone-Modified Polymers

- Acrylic

By Coating Technology

- Liquid Coatings

- Powder Coatings

- UV-Cured and Radiation Curable Systems

- Anodizing and Conversion Coatings

By End-Use Sector

- Commercial

- Residential

- Industrial

- Public Infrastructure

By Structural Application

- Roofing and Cladding

- Wall Panels and Facades

- Doors and Windows

- Fascia, Soffits and Gutters

- Interior Architectural Metalwork

By Performance Property

- Corrosion and Chemical Resistance

- UV and Weathering Resistance

- Aesthetic and Decorative

- Functional Coatings

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Architectural Metal Coatings Market

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V

- Axalta Coating Systems Ltd

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Beckers Group

- BASF SE

- Jotun A/S

- Hempel A/S

- Tiger Coatings GmbH & Co. KG

- KCC Corporation

- Arkema S.A.

- Asian Paints Limited

- Tnemec Company, Inc.

*- List not Exhaustive

Table of Contents: Architectural Metal Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Architectural Metal Coatings Market Landscape & Outlook (2025–2032)

2.1. Introduction to Architectural Metal Coatings Market

2.2. Market Valuation and Growth Projections (2025–2032)

2.3. Demand Drivers: Urban Infrastructure, High-Rise Construction, and Facade Systems

2.4. Regulatory Landscape: AAMA Standards, VOC Compliance, and Environmental Regulations

2.5. Sustainability Trends: Energy-Efficient Coatings and Low-Carbon Materials

3. Innovations Reshaping the Architectural Metal Coatings Market

3.1. Trend: PVDF, Fluoropolymer, and High-Durability Coating Systems

3.2. Trend: Chromate-Free Pretreatment and Sustainable Metal Finishing Technologies

3.3. Opportunity: Cool Roof Coatings, Solar-Reflective Pigments, and Energy-Generating Facades

3.4. Opportunity: Anti-Graffiti, Infrared-Reflective, and Functional Smart Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. R&D and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Architectural Metal Coatings Market

5.1. By Resin Chemistry

5.1.1. Fluoropolymers

5.1.2. Polyester

5.1.3. Polyurethane

5.1.4. Epoxy

5.1.5. Silicone-Modified Polymers

5.1.6. Acrylic

5.2. By Coating Technology

5.2.1. Liquid Coatings

5.2.2. Powder Coatings

5.2.3. UV-Cured and Radiation Curable Systems

5.2.4. Anodizing and Conversion Coatings

5.3. By End-Use Sector

5.3.1. Commercial

5.3.2. Residential

5.3.3. Industrial

5.3.4. Public Infrastructure

5.4. By Structural Application

5.4.1. Roofing and Cladding

5.4.2. Wall Panels and Facades

5.4.3. Doors and Windows

5.4.4. Fascia, Soffits and Gutters

5.4.5. Interior Architectural Metalwork

5.5. By Performance Property

5.5.1. Corrosion and Chemical Resistance

5.5.2. UV and Weathering Resistance

5.5.3. Aesthetic and Decorative

5.5.4. Functional Coatings

6. Country Analysis and Outlook of Architectural Metal Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Architectural Metal Coatings Market Size Outlook by Region (2025–2032)

7.1. North America Architectural Metal Coatings Market Size Outlook to 2032

7.1.1. By Resin Chemistry

7.1.2. By Coating Technology

7.1.3. By End-Use Sector

7.1.4. By Structural Application

7.1.5. By Performance Property

7.2. Europe Architectural Metal Coatings Market Size Outlook to 2032

7.2.1. By Resin Chemistry

7.2.2. By Coating Technology

7.2.3. By End-Use Sector

7.2.4. By Structural Application

7.2.5. By Performance Property

7.3. Asia Pacific Architectural Metal Coatings Market Size Outlook to 2032

7.3.1. By Resin Chemistry

7.3.2. By Coating Technology

7.3.3. By End-Use Sector

7.3.4. By Structural Application

7.3.5. By Performance Property

7.4. South America Architectural Metal Coatings Market Size Outlook to 2032

7.4.1. By Resin Chemistry

7.4.2. By Coating Technology

7.4.3. By End-Use Sector

7.4.4. By Structural Application

7.4.5. By Performance Property

7.5. Middle East and Africa Architectural Metal Coatings Market Size Outlook to 2032

7.5.1. By Resin Chemistry

7.5.2. By Coating Technology

7.5.3. By End-Use Sector

7.5.4. By Structural Application

7.5.5. By Performance Property

8. Company Profiles: Leading Players in the Architectural Metal Coatings Market

8.1. PPG Industries, Inc.

8.2. The Sherwin-Williams Company

8.3. Akzo Nobel N.V

8.4. Axalta Coating Systems Ltd

8.5. Nippon Paint Holdings Co., Ltd.

8.6. Kansai Paint Co., Ltd.

8.7. Beckers Group

8.8. BASF SE

8.9. Jotun A/S

8.10. Hempel A/S

8.11. Tiger Coatings GmbH & Co. KG

8.12. KCC Corporation

8.13. Arkema S.A.

8.14. Asian Paints Limited

8.15. Tnemec Company, Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures