Asia-Pacific Sludge Treatment Chemicals Market: Value Growth, Industry Analysis, and Forecast to 2034

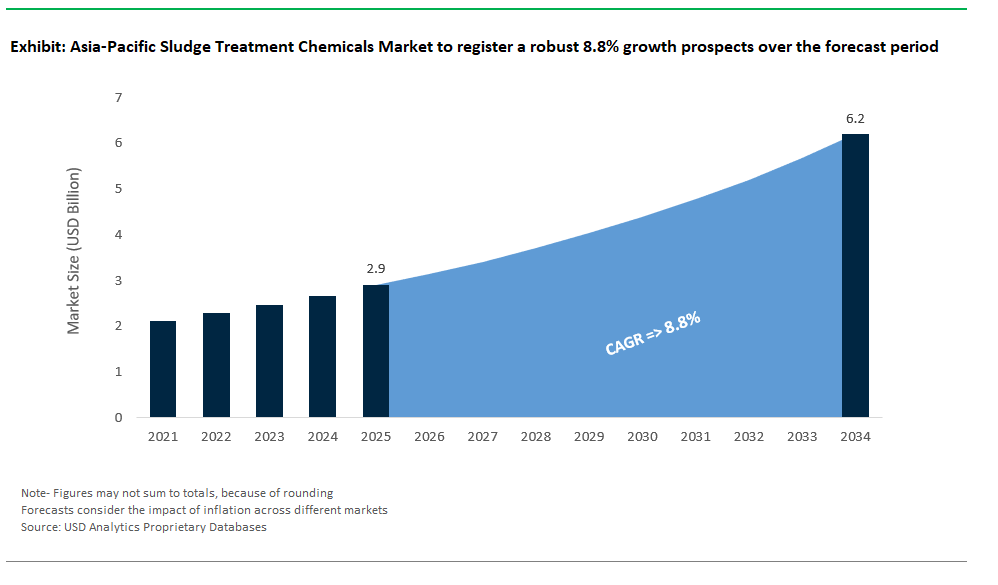

Asia-Pacific Sludge Treatment Chemicals Market Size is estimated at $2.9 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 8.8% to reach $6.2 Billion by 2034.

The Asia-Pacific sludge treatment chemicals market is changing from high-volume chemical use to smarter, performance-based applications. This shift is driven by new environmental regulations and different needs in municipal and industrial sectors. Cationic polyacrylamide (CPAM) is still the main polymer used for dewatering. Its charge densities vary by sludge type; they are typically 40–60% for municipal sludge and can go up to 80% for high-solids industrial sources. In India, the CPCB guidelines inform strategies for optimizing polymers based on EPS (extracellular polymeric substance) levels, which improves dewatering efficiency. Meanwhile, countries like Japan and Thailand are advancing the use of biodegradable coagulants made from natural sources like chitosan and plant-based starches. This aligns with their national green procurement rules. In Taiwan, the high-tech and pulp sectors are adopting hybrid polymer-silicate systems. These systems protect centrifuge equipment while meeting dryness standards set by their EPA-equivalent bodies. In China, the industrial sludge sector, especially from mining and electroplating, is increasingly using sulfide-based chemicals like sodium sulfide and ferrous sulfate. These chemicals help immobilize heavy metals, like lead and cadmium, ensuring that treated leachate stays under 1 mg/L to meet GB 5085.3 toxicity limits.

Seasonal and climate challenges are also influencing chemical innovation. In Southeast Asia, where monsoon-season sludge rewetting is an issue, hydrophobic polymer coatings have become popular. Trials have shown up to a 50% reduction in moisture rebound of dewatered cakes. This supports sustainable land application and transport efficiency. Policy changes across the region are further speeding up demand for multifunctional and environmentally safe chemical formulations. For example, China generated around 55 million tonnes of wet sludge in 2020 and is actively promoting thermal recovery, through incineration or gasification, to lessen reliance on landfills and reduce greenhouse gas emissions by 15–40%. India is also working towards progressive regulations, with the CPCB pushing for moisture contents below 20% in treated sludge. This makes it suitable for co-processing in cement kilns. As carbon intensity becomes a performance target, traditional lime stabilization, which releases around 0.8–1.2 tonnes of CO₂ per tonne of sludge, is gradually losing ground to lower-emission alternatives like anaerobic digestion and enzymatic conditioning. Multifunctional sludge treatment chemicals that combine dewatering, stabilization, heavy metal suppression, and odor control are gaining popularity. Vendors that can provide such integrated, compliance-ready solutions especially those that work with smart dosing systems are becoming key partners in the next phase of Asia-Pacific’s sludge management evolution.

Market Trend: Stricter Landfill Bans and Carbon Policies Drive Demand for Advanced Dewatering and Conditioning Chemistries

The Asia-Pacific sludge treatment chemicals market is experiencing a significant shift due to increasing regulatory pressure and rising disposal costs. With China banning landfill disposal of untreated sludge starting in 2025 and India’s Swachh Bharat 2.0 requiring 100% sludge processing by 2026, utilities and industries are quickly moving toward next-generation dewatering and stabilization chemistries. Traditional polyacrylamides (PAMs) are losing popularity compared to bio-based alternatives, such as tannin-grafted and chitosan-based flocculants, which provide better cake dryness while complying with Japan’s 2024 PFAS discharge limits. For example, Solenis’ Magnafloc® LT8000, used in Singapore’s Tuas Nexus thermal hydrolysis facility, achieved a 22% reduction in polymer demand compared to standard PAMs. This is increasingly important in regions like Guangdong Province, where landfill tipping fees have tripled since 2022 for sludge with under 20% dry solids (DS). Furthermore, the connection between sludge moisture and incineration energy is pushing deeper chemical innovations. A mere 1% increase in cake dryness can save $8 per ton of incineration fuel in Japan’s fluidized bed incinerators. The use of sludge conditioners that improve thermal hydrolysis, anaerobic digestion efficiency, and phosphorus recovery is rising. Suppliers are incorporating digital rheology tools (e.g., Ecolab’s 3D TRASAR™ Sludge) to fine-tune dosing in real-time. The region’s focus on net-zero wastewater operations clearly positions sludge chemistry as critical for both cutting carbon emissions and recovering resources.

Market Opportunity: Coal-to-Biomass Power Conversions Create $320 Million Niche for Heavy Metal Stabilizers

A rapidly growing niche in Asia-Pacific’s sludge treatment chemical market is emerging from the transition to biomass in thermal power generation. This transition creates complex sludge streams with high heavy metal content. With Japan requiring 20% biomass co-firing by 2030 and Thailand aiming for 5,000 MW of biomass power, fly ash and FGD sludge from these facilities increasingly contain cadmium, arsenic, and lead from contaminated agricultural waste like rice husk and palm kernel shells. This change has opened a market of over $320 million for chelating agents, EDTA-free binders, and geopolymer-based stabilizers designed to ensure compliance with new leaching standards like Vietnam’s TCVN 13229:2024, which limits arsenic to 0.5 mg/L TCLP. China’s 2024 Biomass Sludge Control Directive has also declared rice husk-derived sludge as hazardous if not stabilized. In response, suppliers are introducing region-specific formulations. BASF’s Trilon® M, a biodegradable chelator, is being tested in Chinese facilities to prevent secondary contamination risks. In India, NTPC’s pilot project for fly ash-sludge cogranulation with nano-silica additives (CSIR-NEERI 2024) has shown over 95% immobilization of lead and zinc. Suppliers like Kemira are providing sector-specific blends such as Superfloc® XD-100, which combines thiourea derivatives with PAC for treating palm oil mill sludge in Southeast Asia. Additionally, Veolia’s PHOS4® platform allows for dual-purpose treatment: recovering struvite from centrate while simultaneously binding heavy metals like zinc and nickel. As sludge valorization becomes a crucial part of the circular economy, the demand for chemical solutions that meet both landfill eligibility and resource recovery goals will continue to grow particularly in industrial areas without centralized hazardous waste facilities.

Competitive Landscape - Asia-Pacific Sludge Treatment Chemicals Market

The Asia-Pacific sludge treatment chemicals market includes a variety of global and regional players. Each company uses local manufacturing, technical services, and customized product lines to meet the region's unique sludge conditioning needs. Polyacrylamide-based flocculants, inorganic coagulants, and specialty additives lead the market. Vendors are increasingly combining chemistry with process improvement.

SNF Floerger is the top supplier due to its strong manufacturing presence in China and Australia. It also has a significant role in both municipal and industrial wastewater treatment plants. The company provides a complete range of cationic, anionic, and non-ionic PAMs that work well with belt presses, centrifuges, and DAF units. This solidifies its position as a leader in high-performance sludge dewatering.

Kemira Oyj adds to this market with a strong presence in China, Japan, Southeast Asia, and Australia/New Zealand, especially in industries like pulp and paper, chemicals, and oil and gas. Its mix of organic flocculants and ferric/alum-based coagulants, backed by application expertise, helps in managing challenging sludges. This is particularly useful in markets with varying influent characteristics.

BASF, with its Zetag® flocculant line and inorganic coagulants, serves both formulators and end users effectively. Its regional manufacturing facilities enhance its ability to supply both raw materials and ready-made solutions for dewatering and digestion tasks.

Nalco Water, part of Ecolab, provides sludge treatment programs that combine polymers and coagulants with real-time monitoring and process control. With service teams throughout the Asia-Pacific region, the company has become a reliable partner in optimization, especially where reducing operating costs is essential.

Solenis also focuses on improving performance, particularly in reducing polymer usage and enhancing cake dryness. Its products target high-volume sludge generators and are supported by a wide regional reach along with a complete wastewater product line.

Japanese companies like Kurita Water Industries understand the local sludge profiles, regulations, and conditions in Japan, China, and Southeast Asia. Kurita’s strength comes from its unique polymer formulations and hands-on technical support, especially in difficult sludge situations.

In the realm of integrated solutions, Veolia Water Technologies sets itself apart by combining its Hydrex® chemical line with mechanical dewatering systems and advanced process units such as thermal hydrolysis. The company plays a key role in large municipal projects across the region.

Ion Exchange and Thermax, both based in India, provide sludge management solutions to domestic and Southeast Asian markets. Ion Exchange combines conditioning chemicals with complete ETP/STP installations and advanced sludge handling options. Thermax pairs its polymer products with engineered systems like filter presses and dryers.

Moreover, Mitsubishi Chemical Corporation, through its Diaion™ brand, addresses niche sludge treatment applications involving ion exchange and adsorption. This is especially important for recovering heavy metals from industrial sludge or for specific conditioning before dewatering. This highlights the market's need for precise and high-purity separation solutions.

Asia-Pacific Sludge Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Polymers Dominate While Nutrient Additives Lead in Growth

In the Asia-Pacific sludge treatment chemicals market, polymers particularly flocculants remain the dominant category, accounting for approximately 42.4% of market share in 2025. Among these, cationic polyacrylamides (CPAMs) are most commonly used for municipal and industrial sludge dewatering, prized for their ability to enhance solid-liquid separation efficiency in mechanical dewatering systems like belt filter presses and centrifuges. Coagulants, such as ferric chloride and polyaluminum chloride, are often used in combination with polymers to condition sludge by improving particle agglomeration. The fastest-growing segment is nutrient additives, projected to grow at a 10.2% CAGR between 2025 and 2034, fueled by the growing adoption of anaerobic digestion in wastewater treatment plants across India and China. These additives improve microbial performance and biogas output in digesters. Additionally, disinfectants and odor control agents are seeing accelerated adoption due to the tightening of biosolids reuse regulations, especially for pathogen suppression before land application or composting. pH adjusters and conditioners (e.g., lime and magnesium hydroxide) are integral to stabilization processes, while defoamers help optimize thickening and digestion operations. Specialty formulations tailored for advanced treatment or ZLD (zero liquid discharge) applications continue to occupy a smaller but stable portion of the market.

By Sludge Treatment Stage: Dewatering Leads While Drying & Incineration Surge Ahead

Sludge dewatering is the largest application stage, commanding a 44.1% market share in the Asia-Pacific region by 2025. It is central to reducing sludge volume and weight, thereby cutting down transportation and disposal costs. Dewatering operations in this region heavily rely on polymers, which account for over 60% of the chemical usage at this stage. Technologies like belt filter presses, decanter centrifuges, and screw presses are prevalent across China, Japan, South Korea, and India. Sludge drying and incineration, though smaller in current share 16%, is the fastest-growing segment, expanding at 11.4% CAGR. This surge is driven by growing adoption of thermal drying and incineration systems particularly in Japan and South Korea where landfill disposal is either banned or heavily regulated. The push toward energy recovery from sludge incineration and thermal oxidation is further boosting chemical use for drying enhancement and ash conditioning. Stabilization continues to be critical for pathogen reduction and odor control, especially using lime or hydrogen peroxide. Sludge thickening, an essential pretreatment step, remains a consistent user of polymers, particularly in gravity thickeners and dissolved air flotation (DAF) units in municipal and industrial facilities.

.png)

Asia-Pacific Sludge Treatment Chemicals Market Report Scope

Asia-Pacific Sludge Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$6.2 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Type of Chemical (Polymers (Flocculants), Coagulants, pH Adjusters/Conditioners, Disinfectants/Odor Control Agents, Defoamers/Antifoaming Agents, Nutrient Additives, Other Specialty Chemicals), By Sludge Source/Application (Municipal Wastewater Treatment Sludge, Industrial Wastewater Treatment Sludge), By Sludge Treatment Stage (Sludge Thickening, Sludge Dewatering, Sludge Stabilization, Sludge Drying/Incineration), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kemira Oyj (Finland), SNF Floerger (France), Ecolab Inc. (U.S.), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), Solenis LLC (U.S.), Ion Exchange (India) Ltd. (India), Veolia Water Technologies (France), Thermax Limited (India), Nouryon (The Netherlands), Chembond Chemicals Limited (India), Bio-Chem Asia Pacific Sdn Bhd (Malaysia),

|

|

Countries

|

China, India, Japan, South Korea, Australia, South East Asia

|

Asia-Pacific Sludge Treatment Chemicals Market Segmentation

By Type of Chemical

- Polymers (Flocculants)

- Coagulants

- pH Adjusters/Conditioners

- Disinfectants/Odor Control Agents

- Defoamers/Antifoaming Agents

- Nutrient Additives

- Other Specialty Chemicals

By Sludge Source/Application

- Municipal Wastewater Treatment Sludge

- Primary Sludge

- Secondary Sludge (Waste Activated Sludge - WAS)

- Digested Sludge

- Industrial Wastewater Treatment Sludge

- Pulp and Paper Industry Sludge

- Food and Beverage Industry Sludge

- Chemical and Petrochemical Industry Sludge

- Oil and Gas Industry Sludge

- Mining and Metallurgy Industry Sludge

- Pharmaceutical Industry Sludge

- Textile Industry Sludge

- Electronics and Semiconductors Industry Sludge

- Other Industrial Sludges

By Sludge Treatment Stage

- Sludge Thickening

- Sludge Dewatering

- Sludge Stabilization

- Sludge Drying/Incineration

By Form of Chemical

- China

- India

- Japan

- South Korea

- Australia

- South East Asia

- Rest of Asia

Top Companies in Asia-Pacific Sludge Treatment Chemicals Market

- Kemira Oyj (Finland)

- SNF Floerger (France)

- Ecolab Inc. (U.S.)

- BASF SE (Germany)

- Kurita Water Industries Ltd. (Japan)

- Solenis LLC (U.S.)

- Ion Exchange (India) Ltd. (India)

- Veolia Water Technologies (France)

- Thermax Limited (India)

- Nouryon (The Netherlands)

- Chembond Chemicals Limited (India)

- Bio-Chem Asia Pacific Sdn Bhd (Malaysia)

* List Not Exhaustive

Research Coverage

The Asia-Pacific Sludge Treatment Chemicals Market report provides an in-depth analysis of the chemical solutions and technologies driving sludge treatment performance in municipal and industrial sectors. It explores major trends such as landfill bans, carbon reduction mandates, and thermal sludge valorization, while highlighting innovations in polymers, coagulants, nutrient additives, and advanced conditioning agents. The research evaluates how regulatory shifts, climate-driven operational challenges, and resource recovery initiatives shape demand for dewatering, stabilization, and drying enhancement chemistries.

Scope Includes:

- Segmentation By Type of Chemical: Polymers (Flocculants), Coagulants, pH Adjusters/Conditioners, Disinfectants/Odor Control Agents, Defoamers, Nutrient Additives, Specialty Chemicals

- Segmentation By Sludge Source/Application: Municipal Sludge (Primary, Secondary, Digested), Industrial Sludge (Pulp & Paper, Food & Beverage, Oil & Gas, Chemical, Electronics, Textile, Mining, Others)

- Segmentation By Sludge Treatment Stage: Sludge Thickening, Dewatering, Stabilization, Drying/Incineration

- Segmentation By Form: Liquid, Powder/Solid

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Key Regions & Markets: Covers 7+ APAC countries with granular insights into infrastructure policies, sludge handling regulations, and industry-specific chemical needs.

- Companies Covered: SNF Floerger, Kemira Oyj, Ecolab Inc., BASF SE, Solenis LLC, Kurita Water Industries, Veolia Water Technologies, Thermax, Ion Exchange India, Nouryon, Chembond Chemicals, Bio-Chem Asia Pacific.

Methodology

This study applies a mixed-method approach integrating primary interviews with plant operators, regulatory agencies, and chemical formulators, and secondary research from government publications, sludge management guidelines, and peer-reviewed studies. Market estimation employs a bottom-up model, aggregating sludge treatment capacities by municipal and industrial plants, and applying chemical dosing rates per ton of dry solids for each treatment stage. Top-down validation leverages regional chemical consumption data and import/export flows. Forecasting incorporates drivers such as ZLD mandates, carbon-neutral initiatives, energy recovery from sludge, and climate-linked seasonality. Data triangulation across multiple sources ensures accuracy, while scenario modeling assesses the impact of emerging technologies like anaerobic digestion enhancers and PFAS-compliant formulations on market dynamics.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements