Market Overview: EV E-Transmission Fluids, Synthetic Conversion, and Base Oil Expansion Drive Automotive Transmission Fluid Market

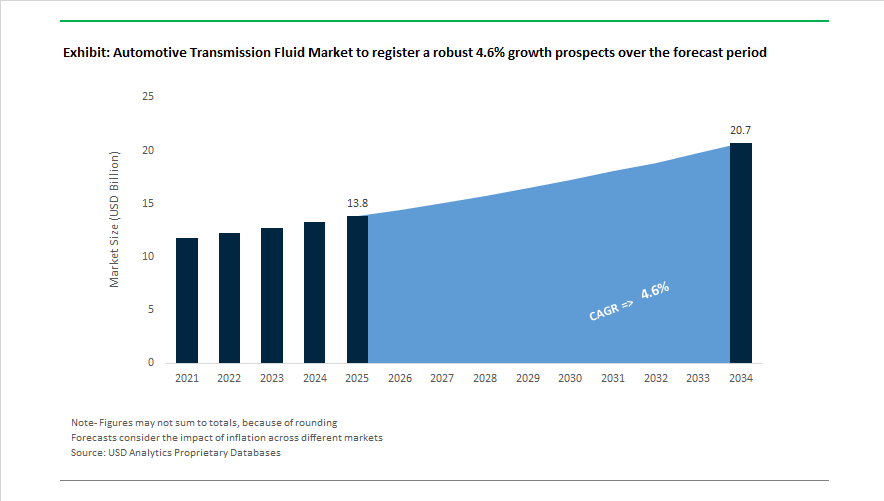

The automotive transmission fluid market is valued at $13.8 billion in 2025 and is projected to reach $20.7 billion by 2034, advancing at a 4.6% CAGR. Market expansion is linked to increasing demand for fully synthetic ATF, low-viscosity transmission fluids, EV e-transmission fluids, CVT fluids, PAO-based lubricants, PAG gear oils, and high-oxidation-stability automotive lubricants. The technology shift toward electrified drivetrains began accelerating in March 2024, when Lubrication Engineers introduced the SYNPAG series for EV gears using PAG chemistry for superior thermal conductivity and film strength. In the same year, ABRO Industries launched oxidation-resistant gear and transmission oils aimed at high-mileage fleets, while Punch Powertrain secured a major VT3 CVT supply contract in June 2024, reinforcing demand for specialized CVT transmission fluids in Asia. Also in 2024, BASF opened a new production facility in Shanghai for premium synthetic transmission fluids, strengthening localized supply chains.

Electrification and synthetic fluid conversion intensified during late 2024–August 2025. TotalEnergies expanded its Quartz EV Fluid portfolio into India in late 2024, addressing copper compatibility and static charge management in hybrid and electric drivetrains. In April 2025, Castrol introduced Castrol ON EV Transmission Fluid W2 and W5, engineered for wet e-motors with low electrical conductivity to prevent arcing and enhanced cooling for integrated electronics. Synthetic base oil supply strengthened when Chevron Phillips Chemical completed a low-viscosity PAO expansion in Belgium in August 2025, ensuring availability of high-performance base stocks for fuel-efficient ATFs. In the same month, Shell India initiated a strategic push to migrate customers from mineral to premium synthetic transmission fluids suited for extended drain intervals under high-temperature conditions.

Portfolio consolidation and heavy-duty integration shaped the outlook in December 2025–January 2026. Advanced Lubrication Specialties launched Sunoco Ultra Full Synthetic Multi-Vehicle ATF in December 2025, offering compatibility with nearly all passenger vehicle automatic and CVT systems to reduce service center inventory complexity. Valvoline expanded its technical collaboration with Cummins during 2025, targeting long-drain integrated fluids for automated manual transmissions in heavy-duty fleets. Castrol introduced its MHP lubricant range in July 2025, with chemistry adaptable to hybrid transmission demands involving frequent thermal cycling. In January 2026, Chevron confirmed preparations for PC-12 heavy-duty standards, a shift influencing transmission fluid chemistry compatibility with next-generation emission systems.

Trends and Opportunities Reshaping Competitive Strategy in the Automotive Transmission Fluid Market

Market Trend: Dedicated Low-Viscosity Fluids Purpose-Built for Integrated EV e-Drive Systems

The transition from multi-loop lubrication architectures to single-fluid immersive cooling is redefining product requirements across the Automotive Transmission Fluid Market. Modern electric vehicle drivetrains integrate the electric motor, reduction gears, and power electronics inside one shared housing, demanding fluids that deliver dielectric insulation, thermal dissipation, copper corrosion control, oxidation stability, and gear protection simultaneously.

In November 2025, Shell Lubricants introduced Shell EV-Plus Thermal Fluid, a milestone that demonstrated a single-circuit system capable of simultaneously cooling a battery pack while lubricating the e-drive unit. For OEMs, this simplifies system design, lowers bill-of-materials (BOM) costs, reduces cooling loop components, and supports lightweight architectures critical for range optimization.

Technical partnerships are accelerating capability adoption. A September 2025 Shell–RML Group study showed that advanced GTL-based e-fluids enabled a 34 kWh battery to reach 10–80% charge in under 10 minutes, managing heat loads that are five times higher than the thermal stress of standard slow-charging BEVs.

Electrical resistivity is emerging as a new performance axis. Industry data from 2025 indicates that next-generation e-ATFs are engineered to withstand voltages above 800V, specifically addressing rotor winding insulation gaps and preventing dielectric breakdown in high-speed EV propulsion platforms.

Market Trend: OEM Shift Toward "Fill-for-Life" Sealed Transmissions and Extended Drain Intervals

OEM powertrain strategies are converging around sealed transmissions, where fluids are no longer treated as consumables but as permanent performance enablers. By mid-2025, Toyota and Ford expanded sealed automatic transmission architectures across their global portfolios, shifting maintenance requirements from mileage-based checks to “severe-use conditional inspections,” effectively pushing the standard change interval toward 150,000 miles.

The system economics are compelling. Chevron and Havoline’s 2025 lubrication guides emphasize 40% higher oxidation resistance in new-generation Group III+ and IV synthetic ATFs, preventing sludge accumulation that historically drove premature fluid swaps. Government environmental reports forecast that extended-drain ATF adoption could reduce global automotive waste-oil volume by 15–20% over the next decade.

For fleet operators and subscription-mobility platforms, this adoption directly reduces lifetime maintenance cost – a factor increasingly weighted in fleet TCO contracts, particularly across high-utilization ride-hailing vehicles in North America and India.

Market Opportunity: High-Torque Hybrid Transmission Fluids as the Next Margin Pool

As Hybrid Electric Vehicles (HEVs) scale, the market is bifurcating into factory-fill OEM contracts and service-fill aftermarket demand, with the latter poised to become the largest profit engine. Infineum (December 2025) reported that 16% of global vehicle production (~12M units) now utilizes Dual-Clutch Transmissions (DCTs). As these vehicles age, the aftermarket is projected to overtake OEM factory-fill revenue streams for the first time in 2025.

Hybrid transmission lubrication requires dual-duty characteristics: protection against electric-motor-driven torque spikes and friction-consistent behavior required by clutch-based shifting hardware. Castrol TRANSMAX hybrid DCT fluids (launched 2024) address this by combining precise friction curve control with thermal conductivity suited for flooded DCT systems, which now represent 80% of all DCT installations.

A parallel technical avenue sits in life-extension additives. In October 2024, JATCO’s friction-restoring CVT additive system was validated to extend the usable life of aging hybrid transmissions without hardware dismantling, unlocking a scalable aftermarket service model for Tier-2 garages and dealership service networks.

Market Opportunity: Ultra-Low-Viscosity ATFs Enabling CAFE-Compliant Efficiency Targets

Regulatory pull is shaping a new competitive landscape for transmission fluid formulation. The U.S. NHTSA CAFE Final Rule (2024–2026) requires OEM fleet averages to reach 49 mpg by 2026, converting lubricant viscosity into a compliance-critical technology lever.

Academic data cited in 2025 MDPI Lubricants confirms that transitioning from 15W-40 baselines to 0W-16 or 0W-12 ultra-low-viscosity ATFs can improve urban cycle fuel economy by up to 5% in ICE-based vehicle platforms. The chemistry enabler is Molybdenum-based friction modifiers, which reduce boundary friction by ~30%, maintaining durability in high-pressure gear meshes even at reduced viscosity.

OEM procurement has already responded. Premium-grade low-friction ATF contracts are being integrated into multi-year sourcing frameworks between Tier-1 lubricant formulators and drivetrain OEMs, particularly across U.S., Korean, and Japanese automakers that face the steepest regulatory compliance exposure.

Automotive Transmission Fluid Market Share and Segmentation Insights

Fluid Type Market Share: ATF Dominates Volumes While EV Transmission Fluids Redefine Future Growth

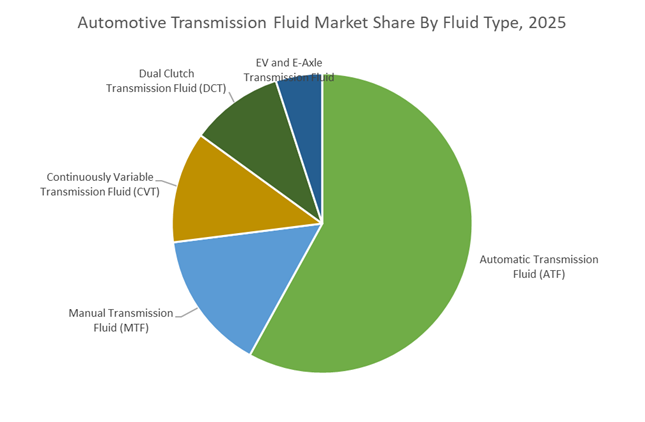

In 2025, automatic transmission fluid (ATF) accounts for 58% of global automotive transmission fluid demand, reflecting the near-complete phase-out of manual gearboxes in North America and strong adoption of torque-converter automatics across China and India. ATF remains the backbone of passenger vehicle lubrication, supporting multi-speed automatic platforms with increasingly tight friction and durability requirements. Manual transmission fluid (MTF) is in structural decline, confined largely to entry-level economy cars, select commercial vehicles, and legacy European models. EV and e-axle transmission fluids represent the most strategically critical segment, growing rapidly despite a smaller base, as electrified drivetrains require specialized dielectric performance and advanced thermal management for motors and reduction gears. CVT and DCT fluids have stabilized, with CVTs dominant in Japanese hybrids and DCTs favored by VW Group and Korean OEMs for fuel efficiency, reinforcing segmentation across drivetrain architectures.

Base Oil Market Share: Synthetic Fluids Cross 50% as Modern Transmissions Demand Higher Performance

By base oil type, synthetic transmission fluids capture 52% market share in 2025, marking a structural inflection point as modern 6+ speed automatics, CVTs, DCTs, and EV drivetrains increasingly depend on low-viscosity, high-thermal-stability formulations derived from Group III and Group IV base oils. This shift is directly tied to OEM mandates for improved fuel economy, extended drain intervals, and enhanced oxidation resistance. Mineral oil based fluids continue retreating, now concentrated in parts of Africa, Southeast Asia, and legacy commercial fleets, where higher friction losses and weak cold-flow performance limit compliance with current efficiency standards. Semi-synthetics act as transitional solutions, while bio-based transmission fluids remain niche, constrained by cost and oxidative stability, serving mainly green fleet certifications and select Western European mandates. Notably, no major automaker currently supports bio-based fluids for factory-fill applications.

Automotive Transmission Fluid Market Competitive Landscape

The automotive transmission fluid (ATF) market in 2026 is being reshaped by electrification, ultra-low-viscosity requirements, extended drain intervals, and the convergence of lubrication with thermal management. Leading suppliers are moving beyond conventional automatic transmission fluids toward multifunctional e-fluids that cool batteries, motors, and gearboxes simultaneously. Strategic priorities now center on gas-to-liquid base oils, PAO chemistry, AI-designed friction modifiers, and circular re-refined fluids. OEM compliance for hybrid drivelines, wet e-motors, and dual-clutch transmissions is accelerating innovation, while Asia-Pacific manufacturing expansion and aftermarket simplification are redefining competitive positioning across passenger vehicles, LCVs, and heavy-duty fleets.

Direct liquid cooling leadership and GTL-powered ATF innovation by Shell plc

Shell enters 2026 as the global lubricants leader for the 19th consecutive year, leveraging GTL technology to dominate high-purity synthetic ATFs. Its EV-Plus Thermal Fluid, launched in late 2025, enables all-in-one cooling for batteries, motors, and transmissions, supporting sub-10-minute fast charging. The Shell Spirax portfolio remains core to heavy-duty and passenger segments, including Spirax S4 GX 75W-90 engineered for India’s LCV market. Shell strengthened its South Asian footprint through the full acquisition of Raj Petro Specialities in July 2025. Strategically, Shell is pivoting toward active immersion cooling for high-performance EV platforms and next-generation thermal density applications.

Advanced base oil scale and hybrid driveline protection from ExxonMobil

ExxonMobil is positioning itself as the backbone supplier of next-generation ATFs through its 2025–2026 Singapore Resid Upgrade Project, adding 20,000 barrels per day of premium base stocks and introducing EHC 340 MAX™ globally. The company integrates SpectraSyn™ PAO chemistry directly into Mobil 1™ Synthetic ATF, delivering viscosity stability from −40°C to 150°C. Focused on the Asia-Pacific growth corridor, ExxonMobil has harmonized its global base stock slate to simplify OEM-grade formulations. Its 2026 ATFs are optimized for hybrid drivelines, specifically protecting copper windings in wet e-motors embedded within modern transmission architectures.

Motorsport-validated low-friction ATFs and EV fluid partnerships by BP p.l.c. / Castrol

Castrol is transforming into a full thermal management partner under BP’s strategic review initiated in February 2025. Its Castrol TRANSMAX range remains a global aftermarket benchmark, with 2026 variants targeting friction reduction in 8-speed and 10-speed automatics. Castrol secured an exclusive partnership with Audi’s 2026 Formula 1 entry, developing bespoke Castrol ON EV fluids aligned with new FIA regulations. Leveraging motorsport validation, Castrol delivers ultra-low-friction ATFs that improve fuel economy by up to 1.5% in commercial fleets, reinforcing its reputation for liquid engineering excellence across ICE, hybrid, and electric mobility platforms.

Circular transmission fluids and driveline-neutral strategy from TotalEnergies SE

TotalEnergies leads in circular ATF solutions through its Quartz EV3R program, producing OEM-compliant transmission fluids from re-refined base oils using a Reduce, Reuse, Regenerate model. The FLUIDMATIC SYN and FLUIDE XLD FE lines support extended drain intervals up to 300,000 km in European buses and trucks. In August 2025, TotalEnergies partnered with XING Mobility to integrate immersion-cooled battery systems with its FLUIDMATIC portfolio. Under its 2026 Multi-Energy strategy, the company is repositioning its fluids as driveline-neutral, ensuring compatibility across internal combustion, hybrid, and full EV architectures.

AI-designed friction modifiers and additive architecture from BASF SE

BASF serves as the architect of ATF chemistry, supplying critical additives and friction modifiers that enable global brands to meet tightening 2026 OEM standards. Following its Winning Ways strategy update in late 2025, BASF is scaling plasticizers and performance additives to prevent seal leakage in aging transmissions. A Global Digital Hub opened in Hyderabad in Q1 2026 applies AI-driven molecular modeling to design long-life friction modifiers exceeding 150,000-mile service requirements. BASF also expanded its Pudong facility to support China’s DCT production surge, while Verbund integration enables up to 30% lower-carbon ATF additives via biomass-balanced intermediates.

High-mileage ATFs and data-driven aftermarket optimization by Valvoline Global Operations

Valvoline is targeting simplified maintenance and high-mileage vehicles following its acquisition by Aramco. Its MaxLife™ ATF remains the world’s first high-mileage transmission fluid, now enhanced with advanced seal conditioners and friction modifiers for aging drivetrains. Leveraging Aramco’s UHVI base oils, Valvoline is delivering premium synthetic ATFs at competitive price points in 2026. The company launched Restore & Protect in 2025, a novel ATF that actively removes solenoid and valve deposits during operation. Integration with the Valvoline Instant Oil Change network provides real-time service data, accelerating R&D for next-generation aftermarket transmission fluids.

United States Automotive Transmission Fluid Market: Ultra-Low-Viscosity Leadership and EV-Ready Fluid Architectures

The United States continues to set the pace for ULV automatic transmission fluid specifications, anchored by the long evolution of DEXRON®-VI and the rapid pivot toward Ford MERCON® ULV products for 9- and 10-speed gearboxes. By late 2025, OEM and aftermarket suppliers were clearly prioritizing ultra-low viscosity fluids with exceptional shear stability to support fuel economy compliance under upcoming CAFE standards. This has accelerated the phase-out of Group I and Group II base oils in favor of Group III+ and PAO synthetics across the U.S. market.

Independent formulators are also reshaping the competitive landscape. In December 2025, Advanced Lubrication Specialties introduced the Sunoco® Ultra Full Synthetic Multi-Vehicle ATF, designed to cover nearly all non-commercial automatic transmissions. This reflects a broader trend toward inventory-simplifying, friction-balanced fluids that address both CVTs and stepped automatics. Parallel to this, U.S. lubricant majors have fast-tracked dielectric transmission fluids for wet e-motors, where direct fluid contact with electrical components is critical for heat dissipation in integrated e-axles.

India Automotive Transmission Fluid Market: Localization, Policy-Driven Standardization, and EV Collaboration

India’s transmission fluid market is being reshaped by manufacturing localization and policy alignment. Under the “Make in India” framework, ZF India’s 2025 partnership with a domestic commercial vehicle OEM to supply EcoMid and EcoTronic transmissions has materially increased localized demand for heavy-duty, high-torque transmission fluids. These developments are reinforcing India’s role as a factory-fill hub rather than a pure aftermarket destination.

Policy has become a central driver. The Ministry of Petroleum and Natural Gas finalized its Auto Fuel Vision and Policy 2025 roadmap, mandating standardized high-performance lubricants to improve vehicle efficiency and emissions performance. At the same time, EV-focused collaborations are gaining momentum. Gulf Oil Lubricants India deepened partnerships with electric commercial vehicle manufacturers such as Altigreen in late 2025, supplying custom e-fluids tailored for compact EV thermal management. This trajectory is reinforced by ZF Friedrichshafen’s capacity expansion in Coimbatore, positioning India as a global transmission production hub with rising demand for advanced synthetic fluids.

China Automotive Transmission Fluid Market: CVT Scale-Up, NEV Localization, and Green Manufacturing Zones

China represents the world’s most dynamic convergence of CVT adoption and New Energy Vehicle localization. The 2024 award of the VT3 CVT contract to Punch Powertrain and the subsequent start of manufacturing in 2025 created immediate demand for CVT-specific fluids engineered for belt durability and friction control. Annual volumes exceeding 100,000 units underscore the scale effect shaping fluid formulation strategies in China.

NEV policies are equally transformative. Aggressive localization of e-axles has driven domestic producers, including Sinopec, to scale sulfur-free driveline lubricants for EV transmissions by 2026. Regulatory pressure is intensifying through the Ministry of Ecology and Environment’s “Blue Sky” audits, which have consolidated ATF production into state-monitored Green Chemical Zones. These zones mandate biodegradable, low-VOC formulations, accelerating China’s shift toward environmentally compliant transmission fluids aligned with export and domestic sustainability targets.

Germany Automotive Transmission Fluid Market: Carbon-Neutral Fluids and High-Voltage EV Compatibility

Germany’s transmission fluid market is increasingly defined by carbon-neutral production and high-voltage research. In January 2025, Chemetall, part of BASF, announced that its primary German metal-treatment and lubricant sites now operate on 100% renewable electricity. This has positioned Germany as a benchmark for low-carbon fluid manufacturing within Europe’s automotive value chain.

On the technology front, German suppliers are pioneering low-conductivity e-fluids tailored for luxury EV platforms expected from 2026 onward. These fluids must remain chemically stable while in proximity to high-voltage components and advanced copper and polymer materials used in electric drive units. Beyond passenger vehicles, collaboration between Afton Chemical and German industrial partners in late 2025 highlighted convergence between automotive and industrial gear oils, with next-generation additives exceeding new ISO thermal and oxidation stability thresholds.

South Korea Automotive Transmission Fluid Market: Additive Innovation and Energy-Storage Adjacency

South Korea’s influence in the transmission fluid ecosystem is increasingly additive-driven rather than volume-driven. In late 2025, LG Electronics successfully scaled its PuroTec™ glass-matrix additive platform for use in high-performance lubricant masterbatches. This technology delivers sustained antioxidant functionality in synthetic ATFs, enhancing oxidation resistance and service life under severe operating conditions.

Beyond automotive applications, South Korea is leveraging transmission-fluid-adjacent chemistries for long-duration energy storage. National investments in grid-scale battery systems are utilizing similar thermal management fluids, creating a technology bridge between automotive transmission fluids and stationary energy infrastructure. This cross-sector synergy positions South Korea as a niche innovation hub for advanced fluid additives.

Strategic Direction of the Automotive Transmission Fluid Industry by Country

Automotive Transmission Fluid Market County Level Snapshot

|

Country

|

Strategic Focus

|

Implication for Transmission Fluids

|

|

United States

|

ULV specifications and EV e-fluids

|

Shift to Group III+/PAO synthetics and dielectric fluids

|

|

India

|

Localization and policy-driven standardization

|

Growth in factory-fill and EV-specific formulations

|

|

China

|

CVT scale-up and NEV localization

|

Rising demand for CVT fluids and low-VOC driveline oils

|

|

Germany

|

Carbon-neutral production and HV research

|

Premium low-conductivity fluids for luxury EVs

|

|

South Korea

|

Additive innovation and storage synergy

|

Longer-life, antioxidant-enhanced synthetic ATFs

|

Automotive Transmission Fluid Market Report Scope

Automotive Transmission Fluid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.8 Billion

|

|

Market Size (2034)

|

$20.7 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Fluid Type (Automatic Transmission Fluid, Manual Transmission Fluid, Continuously Variable Transmission Fluid, Dual Clutch Transmission Fluid, EV and E Axle Transmission Fluid), By Base Oil Type (Mineral Oil Based, Synthetic Oil Based, Semi Synthetic, Bio Based), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric and Hybrid Vehicles, Off Road Equipment), By Sales Channel (Original Equipment Manufacturer, Aftermarket), By Performance Specification (Low Viscosity Fluids, Ultra Low Viscosity Fluids, High Viscosity Fluids)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell plc, Exxon Mobil Corporation, BP plc, Chevron Corporation, TotalEnergies SE, Sinopec Group, Idemitsu Kosan Co Ltd, Fuchs SE, Afton Chemical Corporation, Lubrizol Corporation, Valvoline Global Operations, Petronas Lubricants International, Allison Transmission Holdings, S Oil Corporation, Phillips 66

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Automotive Transmission Fluid Market Segmentation

By Fluid Type

- Automatic Transmission Fluid

- Manual Transmission Fluid

- Continuously Variable Transmission Fluid

- Dual Clutch Transmission Fluid

- EV and E Axle Transmission Fluid

By Base Oil Type

- Mineral Oil Based

- Synthetic Oil Based

- Semi Synthetic

- Bio Based

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Electric and Hybrid Vehicles

- Off Road Equipment

By Sales Channel

- Original Equipment Manufacturer

- Aftermarket

By Performance Specification

- Low Viscosity Fluids

- Ultra Low Viscosity Fluids

- High Viscosity Fluids

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Automotive Transmission Fluid Industry

- Shell plc

- Exxon Mobil Corporation

- BP plc

- Chevron Corporation

- TotalEnergies SE

- Sinopec Group

- Idemitsu Kosan Co Ltd

- Fuchs SE

- Afton Chemical Corporation

- Lubrizol Corporation

- Valvoline Global Operations

- Petronas Lubricants International

- Allison Transmission Holdings

- S Oil Corporation

- Phillips 66

*- List not Exhaustive