Market Overview: Benzene Derivatives Market Value Growth, Aromatics Capacity Shifts, and Pricing Mechanism Reforms

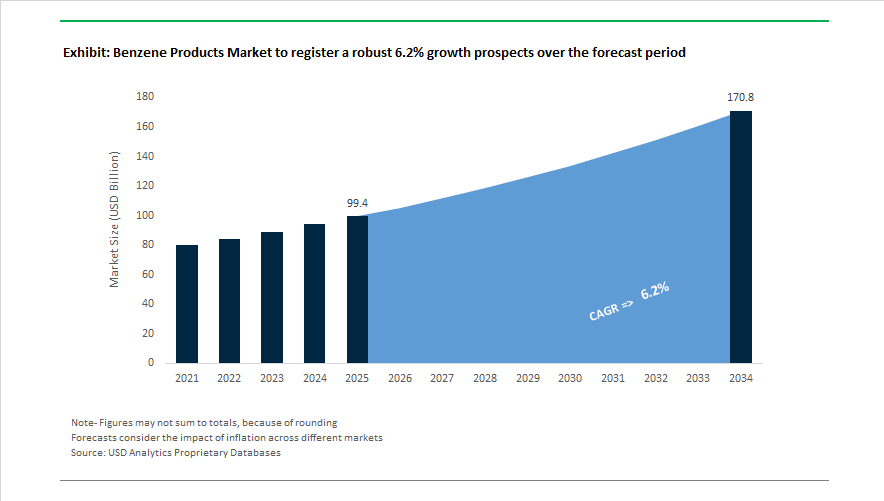

The benzene products market is advancing from USD 99.4 billion in 2025 to USD 170.8 billion by 2034, reflecting a CAGR of 6.2% , supported by steady demand for aromatics feedstocks used in polymers, resins, synthetic fibers, pharmaceuticals, and performance materials. Benzene remains a core petrochemical intermediate in styrene, phenol, cyclohexane, aniline, and alkylbenzene production, making supply chain stability a central concern for downstream industries such as automotive components, electronics, packaging, and healthcare materials. Structural supply adjustments began reshaping the market in 2024 and 2025. In January 2024, SABIC took Final Investment Decision on the Fujian petrochemical complex in China, targeting high-performance chemical output by late 2026. In September 2024, SI Group exited its Singapore production base to optimize regional manufacturing economics for benzene intermediates. Market imbalances became more visible in March 2025 when the U.S. Gulf Coast recorded a structural shortfall of nearly 100,000 tons of benzene imports per month, with elevated Asia–U.S. freight rates amplifying cost pressure for domestic styrene and phenol producers.

Capacity expansion shifted toward integrated mega-complexes while legacy assets faced rationalization. In April 2025, Saudi Aramco and Sinopec advanced expansion of the Yasref joint venture, adding a mixed-feed steam cracker and aromatics complex capable of producing 1.5 million metric tons of aromatics including benzene. In July 2025, PetroChina approved a $9.56 billion refinery and petrochemical complex in Dalian with a 200,000 barrel per day configuration designed to supply benzene and ethylene to downstream polymer chains. China’s domestic benzene output reached 23 million tons in 2025 with 10% annual growth, although industry sources indicate the expansion cycle is nearing a plateau heading into 2026. Structural optimization is continuing through new ethylene cracking capacity additions by Tangshan Dimu and North China Huajin during 2025 to 2026, emphasizing integrated production for supply stability. In contrast, South Korea and Japan announced cracker shutdowns across 2025 and 2026 that will remove roughly 500,000 tons of annual benzene capacity, reflecting consolidation toward efficient modern facilities.

Pricing transparency, regulatory oversight, and sustainability trends are altering benzene market fundamentals. In June 2025, China approved benzene futures and options trading on the Dalian Commodity Exchange, establishing a formal price discovery mechanism for the world’s largest consumer market following price volatility exceeding 30% earlier in the year. Regulatory scrutiny intensified in July 2025 when the U.S. FDA reiterated strict limits of 2 ppm benzene contamination in pharmaceutical production, prompting solvent substitution and tighter purification standards across drug manufacturing supply chains. Latin America faced structural risk in February 2026 when Brazilian industry groups warned of a regulatory gap in the REIQ regime that could accelerate benzene-related plant closures. Decarbonization pressures are also influencing derivative strategies. In 2025, Kuraray introduced a fully biomass-based EVAL resin, aligning with the broader green benzene and bio-naphtha feedstock movement aimed at lowering Scope 3 emissions in aromatics value chains.

Trends and Opportunities Transforming the Benzene Products Market

Market Trend: Styrene Strengthens on EV Growth While Cyclohexane Struggles in High-Cost Regions

A defining feature of the current Benzene Products Market is the widening performance gap between key downstream derivatives. Styrene demand is benefiting from a structural pull created by the electrification of mobility. Across 2025, Asia-Pacific ABS consumption rose meaningfully as Electric Vehicles utilized an estimated 20–25 kilograms of ABS per unit. These applications span interior trims, structural housing, lightweight dashboard systems, and battery compartmenting—areas where ABS provides weight reduction without compromising durability or aesthetics.

Cyclohexane, however, demonstrates the opposite trajectory. The European value chain has been unable to absorb capacity due to chronic cost disadvantages in power and feedstocks. ICIS expectations for 2025 characterize demand as stable but weak, reflecting the erosion of competitiveness in the EU’s nylon sector. European Cyclohexane and Caprolactam producers are facing heightened imports from vertically integrated Asian producers that operate at a significantly lower marginal cost and benefit from cluster-based operations.

Market Trend: European Decommissioning and U.S. Gulf Coast Integration Signal Permanent Structural Shift

Supply-side dynamics are undergoing a strategic reset. Europe is increasingly viewed as a high-cost region for benzene due to CBAM pressures, decarbonization mandates, and volatile utility pricing. In September 2025, Clariant confirmed decommissioning of a major Gendorf, Germany production unit. This event is emblematic of a broader 6% year-over-year decline in European benzene production as firms divest merchant benzene and exit carbon-intensive assets.

Conversely, the U.S. Gulf Coast is exhibiting expansionary and integration-driven investment. Air Liquide’s October 2025 announcement of a $50 million upgrade to its Texas hydrogen pipeline demonstrates the strategy of ensuring reliable supply to integrated complexes that convert benzene directly into polymers and specialty intermediates. By late 2025, regional pricing decoupling became pronounced; Europe averaged $660 per metric ton, nearly $50 lower than benchmark ranges in Asia and the United States, signaling a surplus condition and depressed margins for remaining EU operators.

Market Opportunity: PAN-Based Carbon Fiber as a High-Growth, High-Value Benzene Derivative Segment

A structural growth opportunity is emerging within Polyacrylonitrile (PAN)-based carbon fiber, which is chemically linked to benzene through the cumene–acrylonitrile chain. The global pivot toward lightweight mobility is expanding PAN demand beyond aerospace. In 2025, Type IV hydrogen tanks used in fuel-cell trucks are expected to push global carbon fiber requirements upward by approximately 42%. Wind energy investments are amplifying this effect, as longer turbine blades require high-modulus fiber reinforcement.

Additionally, civil construction is generating recurring long-term demand. Aging infrastructure in North America and the Nordics is increasingly rehabilitated with carbon-fiber-reinforced polymers (CFRP) to extend bridge lifespan, prevent corrosion, and reduce steel maintenance costs. This diversification makes PAN one of the most defensible and strategically attractive benzene-adjacent segments through 2030.

Market Opportunity: Renewable Benzene Production from Pyrolysis and Biomass Integration

Circularity is reshaping strategic capital allocation. "Renewable Benzene" produced from catalytic pyrolysis of post-consumer plastics is transitioning into commercial-scale development. In February 2025, an Energy & Fuels study confirmed catalytic pyrolysis of polypropylene in a double-fluidized-bed reactor can deliver a BTX cut of 22.3 weight%. This positions pyrolysis as a credible feedstock source capable of providing chemically identical benzene suitable for drop-in replacement in polymer manufacturing.

Corporate integration strategies are advancing rapidly as BASF, Dow, and SABIC invest in multi-feedstock benzene hubs capable of switching between naphtha, bio-oil, and pyrolysis oils. These flexible-feed platforms hedge against crude price volatility, while simultaneously helping multinational brand owners comply with packaging mandates requiring validated recycled content.

Benzene Products Market Share and Segmentation Insights

Market Share by Production Technology: Catalytic Reforming Anchors Supply While Coal and Cracker Routes Shape Regional Dynamics

Catalytic reforming accounts for 38% of global benzene production in 2025, maintaining its leadership due to reliable access to light naphtha streams in refining hubs across North America and the Middle East. This route is preferred for producing high-purity benzene required for key derivatives such as ethylbenzene and cumene, which feed styrene monomer and phenol value chains. Steam cracking represents the second-largest source, where benzene is recovered as a by-product of ethylene production, making its output closely linked to global olefins capacity expansion and naphtha cracking margins. Coal-based aromatics hold substantial share, particularly in China, where coal-to-chemicals investments support feedstock diversification and energy security, although environmental compliance costs remain a constraint. Toluene hydrodealkylation provides supply flexibility during periods of strong benzene pricing, while toluene disproportionation enables integrated refinery-petrochemical complexes to optimize benzene and mixed xylene output based on downstream aromatics demand.

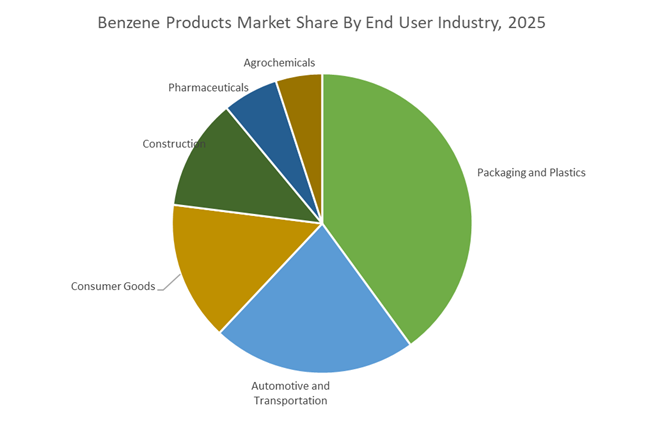

Market Share by End User Industry: Packaging and Engineering Polymers Drive Structural Benzene Consumption

Packaging and plastics lead benzene derivative consumption with a 40% share in 2025, underpinned by strong demand for styrene-based polymers including polystyrene, expandable polystyrene, and ABS, alongside phenol-derived polycarbonate resins. Applications span rigid food packaging, protective packaging, and consumer containers, reinforcing benzene’s centrality in the global polymer market. Automotive and transportation represent a major secondary segment, consuming benzene through caprolactam and adipic acid for nylon used in under-hood components and airbags, as well as styrenic materials for interior trims and dashboards, with lightweighting trends supporting structural growth. Consumer goods, including appliances and electronics housings, rely heavily on ABS and polycarbonate. Construction demand is tied to insulation materials such as EPS and XPS, adhesives, and piping systems, correlating with infrastructure and renovation cycles. Pharmaceuticals and agrochemicals, while lower in volume, represent high-value segments, utilizing benzene as a critical intermediate in API synthesis and crop protection formulations, respectively.

Competitive Landscape Analysis of the Benzene Products Market

The benzene products market is increasingly shaped by vertical integration, low-carbon process innovation, and the strategic shift from commodity aromatics toward high-value downstream derivatives. Leading producers are leveraging refinery-petrochemical synergies, AI-enabled production optimization, and circular chemistry platforms to improve margins while meeting tightening sustainability mandates. Competitive advantage now depends on feedstock flexibility, catalytic efficiency, CCS integration, and the ability to supply ultra-pure benzene intermediates for polymers, pharmaceuticals, batteries, and advanced materials. Major players are also aligning benzene portfolios with EV supply chains, recyclable plastics, and bio-based pathways, positioning aromatics as a cornerstone of next-generation industrial value creation.

Sinopec Group dominates global benzene supply through unmatched scale and integration

Sinopec Group enters 2026 as the world’s largest benzene producer and the central driver of China’s aromatics self-sufficiency. Its core strength lies in operating the globe’s most extensive network of integrated refinery-petrochemical complexes, enabling real-time switching between fuels and chemicals based on margin dynamics. Sinopec is a leading supplier of ethylbenzene and cumene, serving Asia’s rapidly expanding polystyrene and polycarbonate industries. Under its 2025 to 2026 technology-led decarbonization program, the company reduced benzene distillation energy intensity by twelve% across major sites. In early 2026, Sinopec commercialized advanced catalytic reforming that boosts benzene yield while lowering CO₂ emissions per ton.

ExxonMobil advances high-purity aromatics with low-carbon integration

ExxonMobil leads the global high-purity benzene segment, supplying demanding downstream markets through proprietary processing technologies. By fully integrating Pioneer Natural Resources by 2026, ExxonMobil optimized Permian feedstocks for its Gulf Coast aromatics crackers, reinforcing North American cost leadership. The company accelerated its Low Carbon Solutions roadmap, embedding carbon capture and storage directly into primary benzene hubs and moving ahead of 2030 GHG intensity targets. Its Proxxima systems, scaled during 2025 and 2026, convert benzene intermediates into advanced carbon materials and resins. Strategically, ExxonMobil is pivoting toward differentiated performance chemicals, with over forty% of Product Solutions earnings projected from high-value benzene derivatives.

BASF optimizes benzene flows through Verbund integration and digital twins

BASF sets the industry benchmark for Verbund integration, treating benzene as a core node within a highly efficient circular chemical network. In Q1 2026, BASF launched its Global Digital Hub in Hyderabad, applying AI and digital twin technologies to optimize energy use and output across benzene and TDI production lines. The company specializes in ultra-pure benzene-derived intermediates for pharmaceuticals and agrochemicals, commanding premium margins in regulated markets. Ongoing investments in the Zhanjiang Verbund complex position China as a key sustainable aromatics hub by late 2026. BASF also debuted near-zero SVOC benzene-based interior coatings for hospitals and schools, addressing stringent indoor air quality standards.

Reliance Industries transforms benzene into next-generation materials via O2C leadership

Reliance Industries operates the world’s largest single-location refining complex at Jamnagar and is redefining benzene economics through its Oil-to-Chemicals 2.0 strategy. The company is repositioning benzene as feedstock for new materials, including carbon fiber for wind energy and advanced battery chemicals. In 2026, Reliance showcased its proprietary RCAT-HTL process that converts organic waste into renewable crude for green benzene production. Parallel construction of the Dhirubhai Ambani Green Energy Giga Complex integrates benzene derivatives into circular battery manufacturing and recycling. Reliance’s unmatched feedstock flexibility, processing over fifty crude grades, enables global arbitrage and sustains some of the world’s lowest benzene production costs.

Dow leverages benzene for recyclable polymers and net-zero ambitions

Dow utilizes benzene as a foundation for performance plastics and silicones supporting infrastructure and e-mobility. In January 2026, Dow launched its Transform to Outperform initiative, targeting $2 billion in EBITDA improvement by simplifying benzene-to-polymer operations and deploying AI-driven customer interfaces. Through its global Pack Studios, Dow co-develops recyclable, high-barrier packaging using benzene-derived polymers. The company earned multiple Edison Awards in 2025 and 2026, including recognition for its REVOLOOP recycled resin platform. Strategically, Dow’s Path2Zero program centers on Fort Saskatchewan, aiming to establish the world’s first net-zero ethylene and benzene derivative complex.

Shell aligns benzene portfolios with customer sustainability pathways

Shell has repositioned its benzene business around selective growth and sustainability services for high-end industrial customers. A global leader in styrene monomer and phenol, Shell’s 2026 portfolio increasingly emphasizes performance surfactants for detergents and personal care. The company is finalizing its shift toward bio-based and circular chemicals, supplying mass-balance certified benzene that enables customers to claim renewable content in finished plastics. Shell targets automotive and electronics applications, with benzene-derived polycarbonates engineered for EV battery housings and lightweight structures. Its customer sustainability pacing strategy pairs lower-carbon benzene derivatives with tailored ESG consulting, embedding Shell deeper into client decarbonization roadmaps.

China Benzene Products Market: Verbund-Led Scale and Specialty Aromatics Pivot

China’s benzene products industry is entering a structurally integrated phase driven by mega-scale Verbund investments and policy-led capacity rationalization. In November 2025, BASF commenced core operations at its €8.7 billion Zhanjiang Verbund site, anchored by a steam cracker with 1 million metric tons of ethylene capacity and integrated benzene recovery. This configuration directly feeds downstream methylene diphenyl diisocyanate and engineering plastics, signaling a shift from merchant benzene toward captive, value-added consumption. The integration reduces logistics intensity, improves yield control, and positions China to internalize benzene flows within high-performance materials.

Policy measures are reinforcing this transition. Under the 2025 National Refining Blueprint, Beijing initiated the decommissioning of refining units older than 20 years, representing nearly 40% of legacy capacity. The objective is to curb overcapacity and accelerate a move toward high-purity specialty aromatics. In parallel, China’s plan to add 40 million metric tons of ethylene capacity between 2025 and 2028 is designed to synchronize ethylene and benzene availability, making the domestic market self-sufficient for styrene monomer production and reducing reliance on North American imports. Collectively, Verbund integration and refinery modernization are reshaping China from a volume-driven benzene market into a specialty-oriented, internally balanced ecosystem.

India Benzene Products Market: Feedstock Rebalancing and Low-Carbon Aromatics Pathway

India’s benzene products industry is undergoing a policy-driven rebalancing toward higher-value derivatives and lower-carbon production. A July 2025 NITI Aayog report identified benzene as a critical feedstock disparity, noting that 87% of domestic benzene is currently channeled into basic derivatives such as alkylbenzene, compared with a global average of 25%. In response, the government is incentivizing a strategic shift toward ethylbenzene and cyclohexane to deepen downstream integration into polymers, fibers, and engineering materials.

Industry investment is aligning with this mandate. Reliance Industries Limited is fast-tracking its USD 10 billion New Energy and New Materials ecosystem at Jamnagar. By late 2025, the company integrated advanced carbon-capture technologies into its aromatics complex, enabling production of low-carbon benzene tailored for export markets with tightening sustainability requirements. Policy support is expanding capacity for value-added intermediates. Under the updated Production Linked Incentive Scheme 2.0, India has allocated over ₹1.5 lakh crore to high-value chemical clusters, explicitly targeting benzene-based intermediates for pharmaceutical and agrochemical applications. These measures are repositioning India from a basic-derivatives market toward specialty-led benzene utilization.

South Korea Benzene Products Market: Capacity Rationalization and Export-Led Stability

South Korea’s benzene products industry is navigating margin pressure through coordinated capacity restructuring while retaining its export leadership. In August 2025, the Ministry of Trade, Industry and Energy and ten major firms, including LG Chem and Lotte Chemical, signed a landmark agreement to reduce naphtha-cracking capacity by up to 3.7 million metric tons. This move aims to rebalance supply amid tightening margins and rising competition from Chinese integrated projects.

Consolidation discussions are reinforcing this strategy. In late 2025, Lotte Chemical and HD Hyundai Chemical entered formal talks to merge their Daesan-based crackers, a step intended to consolidate benzene supply and enhance cost competitiveness. Despite domestic restructuring, South Korea remains the world’s leading benzene exporter. In 2025, shipping volumes reached approximately 2.9 billion kilograms, primarily serving the U.S. Gulf Coast and Southeast Asia. This export hub status provides revenue stability while the industry transitions to a leaner domestic footprint.

United States Benzene Products Market: Safety-Driven Compliance and Shale-to-Aromatics Efficiency

The United States benzene products industry is being reshaped by heightened environmental enforcement and a strategic pivot toward high-value aromatics derived from advantaged shale feedstocks. In June 2025, a fire at the Shell Polymers Monaca facility led to an accidental benzene release, triggering an investigation by the U.S. Chemical Safety and Hazard Investigation Board. The incident resulted in renewed federal mandates for real-time benzene fenceline monitoring across ethane crackers, accelerating investments in continuous monitoring, vapor recovery, and closed-loop handling systems.

Strategically, U.S. producers are doubling down on feedstock advantage. ExxonMobil raised its 2030 earnings outlook in December 2025, emphasizing its Product Solutions portfolio with a focus on high-value aromatics sourced from Permian Basin feedstocks. The plan targets a substantial contribution from specialty products by 2030. At the process level, producers are deploying advanced catalytic reforming technologies to extract higher benzene yields from light tight oil, positioning the United States as a flexible swing supplier for global cyclohexane and downstream nylon markets.

European Union (Germany and Belgium) Benzene Products Market: Compliance-Led Upgrades and Circular Benzene

Germany and Belgium sit at the center of the European Union’s compliance-led transformation of the benzene products industry. Effective January 2026, the EU implemented stricter occupational exposure limits for benzene under REACH, prompting accelerated investments in closed-loop handling systems and vapor recovery units across the Antwerp-Rotterdam-Rhine-Ruhr cluster. These upgrades are reshaping operating economics while raising the compliance threshold for continued production.

Circular feedstocks are emerging as a strategic differentiator. In late 2025, Borealis AG and INEOS successfully scaled benzene production derived from chemically recycled plastic waste using pyrolysis oil. The output targets demand for circular styrene in automotive and durable goods, aligning benzene supply with Europe’s circular economy objectives and carbon accounting frameworks.

Country-Level Strategic Snapshot: Benzene Products Industry

Benzene Products Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

China

|

Verbund integration and specialty shift

|

Zhanjiang startup, refinery phase-out, ethylene-linked benzene self-sufficiency

|

|

India

|

Feedstock rebalancing and low-carbon exports

|

NITI Aayog roadmap, Jamnagar carbon capture, PLI-backed specialty clusters

|

|

South Korea

|

Capacity rationalization and export stability

|

Naphtha capacity cuts, Daesan merger talks, global export leadership

|

|

United States

|

Safety compliance and shale advantage

|

Fenceline monitoring mandates, Permian-based aromatics, catalytic reforming

|

|

EU (Germany/Belgium)

|

REACH compliance and circular feedstocks

|

OEL enforcement, closed-loop systems, pyrolysis-based circular benzene

|

Benzene Products Market Report Scope

Benzene Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$99.4 Billion

|

|

Market Size (2034)

|

$170.8 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Production Technology (Catalytic Reforming, Steam Cracking, Toluene Hydrodealkylation, Toluene Disproportionation, Coal Based Aromatics), By Purity Grade (Industrial Grade, Nitration Grade, Refined Grade, Electronic Grade), By Derivative Application (Ethylbenzene, Cumene, Cyclohexane, Nitrobenzene, Alkylbenzene, Chlorobenzene), By End User Industry (Automotive and Transportation, Construction, Packaging and Plastics, Pharmaceuticals, Agrochemicals, Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

China Petroleum and Chemical Corporation, Exxon Mobil Corporation, Saudi Basic Industries Corporation, BASF, Reliance Industries, Shell, LG Chem, Chevron Phillips Chemical, PetroChina, INEOS Group, TotalEnergies, LyondellBasell Industries, Mitsubishi Chemical Group, GS Caltex, Hengyi Petrochemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Benzene Products Market Segmentation

By Production Technology

- Catalytic Reforming

- Steam Cracking

- Toluene Hydrodealkylation

- Toluene Disproportionation

- Coal Based Aromatics

By Purity Grade

- Industrial Grade

- Nitration Grade

- Refined Grade

- Electronic Grade

By Derivative Application

- Ethylbenzene

- Cumene

- Cyclohexane

- Nitrobenzene

- Alkylbenzene

- Chlorobenzene

By End User Industry

- Automotive and Transportation

- Construction

- Packaging and Plastics

- Pharmaceuticals

- Agrochemicals

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Benzene Products Industry

- China Petroleum and Chemical Corporation

- Exxon Mobil Corporation

- Saudi Basic Industries Corporation

- BASF

- Reliance Industries

- Shell

- LG Chem

- Chevron Phillips Chemical

- PetroChina

- INEOS Group

- TotalEnergies

- LyondellBasell Industries

- Mitsubishi Chemical Group

- GS Caltex

- Hengyi Petrochemical

*- List not Exhaustive