Biomedical Metal Market 2026 Strategic Outlook: Biomechanics-First Design, Porous Architectures, and Additive Manufacturing Scale-Up

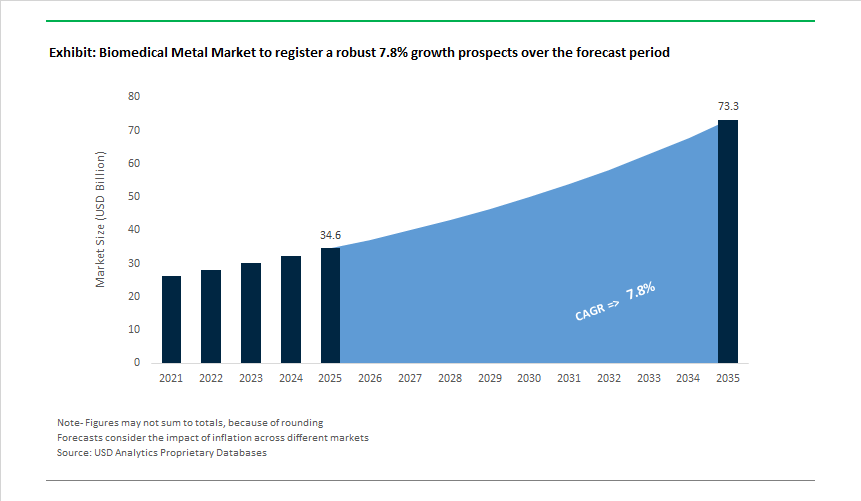

The Biomedical Metal Market, valued at USD 34.6 billion in 2025 and projected to reach USD 73.3 billion by 2035 at a CAGR of 7.8%, is undergoing a foundational shift driven by low-modulus titanium alloys, high-porosity porous metals, antimicrobial surface chemistries, and the rapid scale-up of additively manufactured (3D-printed) implants. For manufacturers with decades of experience, the competitive edge now hinges on delivering metals that balance biomechanical compatibility, biological fixation, and validated infection-prevention performance, while maintaining scalable, regulatory-aligned production systems for next-generation orthopedic and spinal devices.

Long-term demand increasingly favors biomechanics-first material design, with clinicians prioritizing implants that minimize stress shielding by narrowing the elastic modulus gap between metals and natural bone. New low-modulus titanium alloys engineered toward 4-6 GPa-much closer to cortical bone’s 10-30 GPa-enable improved load transfer and reduce aseptic loosening risk, a challenge that has persisted for decades in high-demand orthopedic patients. At the same time, porous tantalum and titanium scaffolds are setting new performance benchmarks, with architectures reaching 80% porosity and pore sizes >200 µm, enabling superior vascularization and osseointegration required for long-term fixation across complex reconstructions.

Infection prevention is becoming a material-level differentiator rather than a post-operative protocol. Silver-coated titanium and emerging NO-releasing surfaces demonstrate >85% in-vitro bacterial kill rates, offering hospitals and surgeons quantifiable reductions in implant-related infection risk-one of the highest-cost complications in modern orthopedics. On the other hand, the maturity of additive manufacturing has shifted from experimental to industrial scale: since 2021, leading contract manufacturers have delivered over 50,000 patient-specific 3D-printed titanium implants, proving readiness for mass customization, complex lattice structures, and revision implants that traditional machining cannot economically achieve. The commercialization environment is equally shaped by regulatory evidence, with FDA clearances, long-term outcomes, and surface treatment validations now serving as primary purchasing drivers for health systems and global OEM partners.

Low-Modulus Titanium, Porous Metals, and Antimicrobial Surfaces Reshape Implant Material Demand

- Biomechanics-driven innovation: Low-modulus titanium alloys and engineered porous metal architectures are central to improving physiological load distribution and enhancing long-term osseointegration.

- Porosity as a performance standard: Pore sizes >200 µm and porosity levels up to 80% correlate strongly with enhanced vascularization and bone in-growth in orthopedic and spinal applications.

- Material-enabled infection control: Antimicrobial surface chemistries-silver or gas-releasing coatings-offer measurable infection mitigation, serving as true differentiators in high-risk implant categories.

- Additive manufacturing at scale: The delivery of 50,000+ AM titanium implants confirms industrial scalability for complex geometries, custom implants, and rapid-turnaround surgical solutions.

- Regulatory rigor as a market catalyst: FDA clearances, breakthrough designations, and published clinical outcomes remain the strongest adoption levers for hospitals and procurement teams

Market Analysis: Consolidation, Surface Technology Acquisitions, and Additive Manufacturing Acceleration

The biomedical metal sector has experienced notable consolidation, strategic tech acquisitions, and product launches through 2024-2025 that materially impact supply, clinical adoption, and innovation pipelines. In March 2025, Medtronic’s acquisition of Nanovis’ nano-surface technology strengthened its spinal portfolio by integrating surface modifications that accelerate bone growth on metal implants - a direct competitive response to clinical demands for faster fusion and improved early stability. Earlier in July 2024, Stryker’s acquisition of Artelon expanded its soft-tissue repair and ligament reconstruction capabilities, complementing its metal fixation product lines and enabling bundled solutions that combine metallic fixation hardware with synthetic soft-tissue augmentation. Over the past two years, industry players have emphasised surface and coating innovations: a Communications Materials publication in July 2024 described a heat-treatment method to generate localized nitric oxide (NO) release from implant surfaces, offering a drug-free antibacterial strategy that could reduce reliance on systemic antibiotics and lower infection rates.

Additive manufacturing and regulatory progress continue to underpin market expansion and product differentiation. Reports of over 50,000 titanium 3D-printed medical implants delivered since 2021 (publicized in September 2024) validate contract manufacturer capabilities and the clinical acceptance of complex porous geometries, enabling companies to commercialize patient-specific spinal, trauma, and joint devices with porous bone-mimetic surfaces. Product clearances and launches in 2025 further reflect this trend: Johnson & Johnson (DePuy Synthes) launched the INHANCE INTACT™ Total Shoulder Replacement System in October 2025, designed for tissue-sparing procedures with optimized metal components for day-one mobility, while Maxx Orthopedics received US FDA 510(k) clearance in September 2025 for a titanium-based revision knee system employing surface-hardening to address metal allergy concerns. Finally, December 2025 saw Zimmer Biomet acquire Monogram Technologies, aligning metal implant platforms with autonomous joint replacement robotics - an integration that signals the growing interSection of implant metallurgy, surface science, and surgical automation.

Biomedical Metal Market: Trends and Opportunities

Additively Manufactured Porous Titanium Redefining Long-Term Implant Fixation

Additive manufacturing has moved decisively from experimental use into scaled, regulated production for biomedical metals, with laser powder bed fusion (L-PBF) porous titanium emerging as the dominant platform for load-bearing implants. The strategic value lies in biomechanics rather than novelty: trabecular titanium lattices with 55–80% porosity closely replicate cancellous bone stiffness, materially reducing stress shielding and improving secondary stability over time. This transition is visible in production data. In October 2025, Amnovis shipped its 100,000th 3D-printed implant and indicated that 2025 volumes alone would match roughly half of its cumulative output from the prior four years—an inflection point that signals industrial, not pilot-scale, adoption.

Process innovation is accelerating scale economics. Amnovis’ validation of a heat-treatment-free titanium workflow that meets ASTM requirements eliminates post-print thermal cycles, preserving engineered lattice microstructures while reducing lead times and energy intensity—key constraints for hospital-grade manufacturing. Clinical durability data further de-risks adoption: a 15-year longitudinal study published in June 2025 reported zero failures for Direct Metal Laser Sintered dental implants, with 200–400 µm pore sizes sustaining osseointegration over more than a decade. OEM benchmarks reinforce this direction. Zimmer Biomet’s OsseoTi platform achieves ~70% porosity and ~475-micron pores, engineered to support vascularization while delivering strength between cancellous and cortical bone—illustrating how porous titanium has become a precision-tuned material system rather than a generic implant substrate.

Bioresorbable Magnesium Alloys Advancing “Disappearing Metal” Orthopedics

Bioresorbable metals are transitioning from niche innovation to clinically validated solutions, with magnesium (Mg) alloys leading due to a Young’s modulus (10–23 GPa) that closely matches natural bone. The clinical and economic logic is compelling: implants that degrade in vivo eliminate secondary removal surgeries, reduce complication risk, and lower lifetime treatment costs—particularly relevant in pediatrics and trauma. A major regulatory milestone was reached in July 2025 when Syntellix AG secured approval from China’s NMPA for its MAGNEZIX® bioabsorbable metallic implants, opening access to the world’s largest orthopedic market.

Clinical evidence has reached critical mass. By late 2025, more than 50 peer-reviewed publications had validated MAGNEZIX® (MgYREZr alloy system) as clinically superior to titanium in selected fracture fixation applications, demonstrating controlled degradation with complete replacement by host bone within 12–24 months. Commercial rollout mirrors this maturity: Syntellix now holds approvals in over 70 countries, covering roughly two-thirds of the global population, and formally launched Chinese operations in November 2025 to target high-volume hospital networks. Pediatric orthopedics represents a structurally attractive sub-segment. July 2025 research highlighted magnesium’s ability to avoid growth-related complications inherent to permanent titanium or stainless steel hardware, positioning resorbable Mg alloys as a default choice for younger patients as regulatory comfort continues to expand.

Antimicrobial Metal Surfaces Addressing Persistent Implant Infection Risk

Periprosthetic joint infection remains one of the most expensive and clinically challenging failure modes in orthopedic and trauma surgery, creating a funded opportunity for antimicrobial biomedical metals that operate independently of antibiotics. The current innovation cycle is centered on ion-mediated antimicrobial action, where controlled release of silver, copper, zinc, or gallium ions disrupts bacterial membranes while preserving host cell compatibility. In October 2025, researchers at Flinders University reported a dual-function bioceramic scaffold incorporating silver-gallium liquid metal nanoparticles that significantly suppressed MRSA colonization while promoting bone regeneration—illustrating how antimicrobial function can be integrated without sacrificing osteoconductivity.

Commercial validation is advancing in parallel. A 2025 study confirmed that HyProtect™ silver multilayer (SML) coatings achieved >99.2% reduction in viable bacteria on titanium and cobalt-chromium-molybdenum alloys. Importantly, three-year follow-up data demonstrated sustained osseointegration with ultrathin SML coatings, alleviating historical concerns that antimicrobial layers might inhibit bone bonding. This momentum aligns with a broader regulatory and clinical shift away from antibiotic-loaded cements toward localized, sustained ion release, as healthcare systems seek durable defenses against multi-drug resistant pathogens without accelerating antimicrobial resistance.

Advanced Cobalt- and Platinum-Based Alloys Powering Next-Generation Cardiovascular Stents

Interventional cardiology is placing new mechanical demands on metallic biomaterials as procedures extend to smaller, more calcified, and anatomically complex vessels. Cobalt-chromium (CoCr) and platinum-chromium (PtCr) alloys are gaining share due to their superior radial strength, fatigue resistance, and radiopacity compared with legacy 316L stainless steel. In August 2025, real-world data from the SOLSTICE Registry showed that an ultra-thin strut CoCr stent achieved a 99.7% device success rate in complex PCI cases, underscoring how CoCr enables strut thicknesses below 75 µm without compromising vessel scaffolding—critical for rapid endothelialization and lower restenosis risk.

PtCr alloys are extending functionality further. Boston Scientific’s SYNERGY MEGATRON™ platform leverages platinum content to deliver exceptional fluoroscopic visibility and controlled over-expansion from 3.5 mm to 6.0 mm, addressing large proximal vessels without structural trade-offs. Clinical strategy is also evolving. Updated 2024–2025 data from the EVOLVE Short DAPT Trial confirmed that advanced PtCr stents support three-month dual antiplatelet therapy, expanding eligibility among high-bleeding-risk patients previously excluded from metallic stenting. Bench testing consistently shows lower elastic recoil and higher radial strength versus stainless steel, enabling thinner, more navigable profiles—positioning advanced CoCr and PtCr alloys as central to the next phase of minimally invasive cardiovascular care.

Biomedical Metal Market Share Analysis

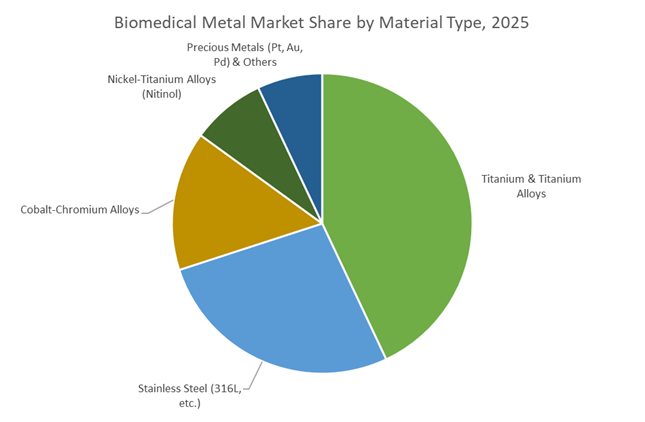

Market Share by Material Type: Titanium and Titanium Alloys Define the Commercial Gold Standard

Titanium and titanium alloys account for an estimated 43% share of the global biomedical metal market, reflecting their entrenched position as the material of choice for permanent, load-bearing implant applications. This dominance is structurally driven by titanium’s unmatched biophysical compatibility with human bone, a factor that directly influences long-term implant success rates and clinical adoption. Compared with stainless steel and cobalt-chromium alloys, titanium—particularly Ti-6Al-4V ELI (Grade 23)—offers a significantly lower elastic modulus, reducing stress shielding and preserving surrounding bone density over time. This mechanical alignment with natural bone has become a decisive procurement criterion for orthopedic surgeons and hospital purchasing committees focused on implant longevity and revision avoidance. Titanium’s superior strength-to-weight ratio further reinforces its market leadership, enabling high mechanical performance at nearly half the density of traditional implant metals, which directly improves patient comfort in hip, knee, and trauma reconstructions. Beyond mechanical performance, titanium’s spontaneous formation of a stable titanium oxide surface enables reliable osseointegration, allowing implants to achieve direct structural bonding with bone without inflammatory responses. This biological advantage has no true substitute among competing metals and underpins titanium’s widespread regulatory acceptance. Market share is further consolidated by titanium’s dominance in additive manufacturing for medical implants, where porous lattice structures manufactured via 3D printing allow customized geometries, faster bone ingrowth, and modulus tailoring. As personalized medicine, complex reconstructions, and revision-resistant implants gain clinical priority, titanium alloys remain the economic and clinical backbone of the biomedical metals market.

Market Share by Application: Orthopedic Implants Anchor Long-Term Demand for Biomedical Metals

The orthopedic segment represents approximately 35% of total biomedical metal demand, making it the largest and most structurally resilient application area within the market. This leadership position is anchored in the sheer volume and mechanical intensity of orthopedic procedures, particularly hip, knee, and spinal surgeries that require materials capable of enduring millions of load cycles over decades. Titanium alloys dominate this segment because of their proven high-cycle fatigue resistance, which supports long implant lifecycles exceeding 20 years in joint replacements—an increasingly critical metric as global populations age and revision surgeries become costlier for healthcare systems. Orthopedic demand is also reinforced by titanium’s exceptional bio-corrosion resistance in physiological environments, where minimal ion release reduces the risk of metallosis, inflammatory reactions, and premature implant failure. Within spinal applications, the market is evolving toward low-modulus beta titanium alloys, which better replicate the flexibility of the human spine and reduce adjacent segment degeneration compared to rigid cobalt-chromium systems. This shift reflects a broader clinical emphasis on motion preservation rather than pure rigidity. While permanent implants drive the majority of value, orthopedics also sustains steady demand for stainless steel in temporary fixation devices and surgical instruments, underscoring the segment’s material diversity. However, it is titanium’s ability to combine durability, biological safety, and mechanical harmony with the human body that keeps orthopedics at the center of biomedical metal consumption and ensures its continued leadership in overall market share.

Competitive Landscape Defined By Porous Metals, Surface IP, and AM Capabilities in Biomedical Metal Market

The competitive field in biomedical metals is concentrated among leading orthopaedic and medical-device OEMs that combine proprietary porous technologies, surface treatments, additive manufacturing capabilities, and digital/robotic integrations. Market leaders differentiate on porous biomaterials (tantalum, porous Ti), low-modulus alloy R&D, antimicrobial surface chemistries, FDA/regulatory track records, and scale in 3D-printed implant supply. Below is a concise overview followed by company-specific positioning.

Fragmentation in niche specialties (spinal, trauma, joint revision, cardiovascular) persists, but major players are consolidating via acquisitions and technology integrations that expand metal platform breadth (porous matrices, coatings, AM capability) and digital surgery tie-ins (robotics and navigation). Key purchase considerations remain biological fixation performance, implant mechanical compatibility, infection-resistance, and supply reliability for custom and off-the-shelf portfolios.

Zimmer Biomet - Pioneering Porous Metal Fixation and Integrating Robotics Into Metal Implant Platforms

Zimmer Biomet’s Trabecular Metal® (elemental tantalum) represents a market-leading porous biomaterial with up to 80% porosity, engineered for exceptional biological fixation and vascularization. The company is investing heavily in digital ecosystems-integrating robotics (e.g., ROSA-like systems) and OrthoGrid planning tools-to drive precise placement and improved outcomes for metal orthopedic implants. Zimmer Biomet’s Monogram Technologies acquisition (Dec 2025) strengthens its position in autonomous joint replacement and signals a strategic push to marry advanced metals with surgical automation. Their iodine-treated hip system (FDA Breakthrough Designation) further underscores a focus on surface innovation to improve long-term biological response.

Stryker - Broad Alloy Portfolio and Robotics-Enabled Precision For Metal Joint and Trauma Devices

Stryker’s strength lies in its deployment of titanium and cobalt-chromium alloys across joint replacement and trauma lines, emphasizing high wear resistance and fatigue strength for load-bearing implants. Stryker’s Mako robotic-arm platform enhances implant alignment and reproducibility for metal arthroplasties, while substantial R&D investment (~USD 1.5B FY24) fuels development of porous titanium coatings and surface treatments. Strategic moves-such as acquiring mfPHD for modular OR systems-reflect a broader ecosystem play to optimize surgical environments for metal implant procedures.

Johnson & Johnson (Depuy Synthes) - Scale in 3D-Printed Porous Ti Devices and Legacy Fixation Systems

DePuy Synthes combines an extensive trauma and fixation heritage (stainless steel 316L, Ti alloys) with modern 3D-printed porous titanium interbody and implant platforms (CONDUIT™), designed to mimic cancellous bone and promote fusion. Recent product introductions in 2025 (e.g., VOLT™ plating systems) and tissue-sparing shoulder systems highlight the company’s dual strategy: leverage legacy metal fixation reliability while scaling porous, AM-enabled devices for spinal and fusion indications. DePuy’s VELYS™ robotic navigation further integrates metal implant delivery with perioperative planning.

Smith & Nephew - AM-Led Porous Ti Matrices (CONCELOC®) For Enhanced Fixation and Immediate Stability

Smith & Nephew’s CONCELOC® porous titanium, produced via additive manufacturing, achieves near-surface porosities up to ~80% in Ti-6Al-4V and provides a high coefficient of friction (≈0.95) to minimize micromotion-key for immediate post-operative stability. The company’s AM focus enables complex geometries and patient-matched constructs for hip and knee reconstructions, positioning Smith & Nephew as a specialist in porous metal matrices and advanced surface topographies that drive osseointegration.

Medtronic - Spinal and Neurovascular Metal Platforms With Advanced Surface Tech and MRI-Compatible Materials

Medtronic’s metal portfolio emphasizes spinal implants and neurovascular devices built on proprietary titanium alloys and specialized coatings that support long-term biocompatibility and structural integrity. The acquisition of Nanovis’ nano-surface technology (Mar 2025) enhances Medtronic’s ability to accelerate bone growth on metal surfaces-improving fusion rates. Medtronic also invests in Nitinol for shape-memory and superelastic devices and prioritizes MRI-compatible, low-artifact metals for implantable cardiac and neuromodulation systems.

The United States continues to dominate the biomedical metal market through a powerful combination of regulatory agility, advanced manufacturing, and deep capital investment in medical-grade alloys. Federal focus in 2025 is strongly centered on additive manufacturing–ready metals, particularly titanium alloys, cobalt-chromium, and Nitinol, which are critical for next-generation orthopedic implants and cardiovascular devices. Regulatory clearance pathways have become a strategic enabler, allowing faster commercialization of hypersensitivity-safe titanium systems and surface-engineered implants. At the same time, defense–healthcare convergence is accelerating demand for lightweight, shape-memory alloys used in field-deployable medical solutions. On the supply side, capacity expansions by specialty alloy producers such as Carpenter Technology Corporation underscore the growing requirement for ultra-clean metal powders tailored for 3D printing. Collectively, these dynamics position the U.S. as the global benchmark for high-performance, innovation-driven biomedical metals.

South Korea’s National Push for Medical Alloy Localization and Device Integration

South Korea is rapidly emerging as a strategic biomedical metals hub by embedding implant-grade alloy development into its long-term medical device industrial policy. The government’s “game-changer” initiative explicitly links advanced metals with surgical robotics and dental implant ecosystems, creating downstream pull for high-purity titanium and cobalt-based alloys. Localization targets are reshaping procurement strategies, with domestic producers increasingly substituting imported biomedical substrates to enhance national medical security. The tangible outcomes of prior programs-hundreds of regulatory approvals and strong commercial traction-have validated this approach. South Korea’s strength lies in tightly coupling biomedical metal development with finished medical device manufacturing, enabling faster iteration cycles and export-ready product platforms.

China’s New Materials Roadmap and Ultra-Purity Metal Scale-Up

China’s biomedical metal market is transitioning from cost-driven production to high-end material sovereignty. National policy now prioritizes ultra-pure non-ferrous metals, rare earth alloys, and high-strength stainless steels tailored for neurosurgical and cardiovascular applications. Circular economy mandates are simultaneously expanding recycled alloy recovery, creating secondary supply streams for medical-grade metals while reducing import exposure. Under the New Materials framework, dedicated R&D centers are accelerating breakthroughs in tantalum and specialty stainless steels used in high-risk surgical environments. This dual focus on purity and scale positions China as both a volume supplier and an increasingly capable producer of advanced biomedical alloys.

India’s PLI 1.2-Driven Shift Toward Biocompatible Specialty Alloys

India’s biomedical metal market is undergoing a structural upgrade as the country pivots from commodity steelmaking to high-value, medical-grade alloys. The Production Linked Incentive (PLI) scheme for specialty steel has unlocked large-scale investment into biocompatible stainless steels and titanium alloys suitable for implants and surgical instruments. Strategic indigenization milestones achieved by Mishra Dhatu Nigam Limited highlight India’s growing capability in producing aerospace- and medical-grade alloys domestically. Parallel investments by JSW Steel and Tata Steel into specialized production lines are strengthening supply availability for the fast-growing orthopedic implant market. India’s trajectory is defined by cost-efficient manufacturing combined with rising compliance to global medical standards.

Germany’s Regulatory Optimization and Sustainable Biomedical Metallurgy

Germany remains Europe’s innovation nucleus for biomedical metals, benefiting from strong regulatory institutions and advanced metallurgical expertise. Planned reforms to the EU Medical Device Regulation are expected to ease approval bottlenecks for custom and small-batch metallic implants, a segment where German manufacturers excel. Investment momentum in life sciences is feeding into the development of advanced biocompatible coatings and corrosion-resistant alloys. Industrial leaders such as Heraeus Medical and Fort Wayne Metals (via German operations) are integrating AI-driven design with nitinol and cobalt-chrome wire production, enhancing precision and consistency. Sustainability is an additional differentiator, with increasing emphasis on low-carbon metallurgy aligned with EU climate objectives.

Japan’s Materials DX Strategy Addressing an Aging Population

Japan’s biomedical metal market is shaped by demographic imperatives and digital transformation. The Materials DX Platform is enabling data-driven discovery of bio-active alloys, particularly titanium–zirconium systems optimized for osseointegration in elderly patients. Advanced simulation tools are shortening development timelines and improving clinical predictability of new alloys. Regulatory outreach by the PMDA is also enhancing Japan’s global integration, facilitating faster international adoption of breakthrough metallic therapies through fast-track pathways. Japan’s competitive edge lies in precision metallurgy, long-term reliability, and alignment with aging-society healthcare needs rather than volume expansion.

National Strategic Development Matrix: Biomedical Metal Market (2025)

Biomedical Metal Market Development Matrix by Country

|

Country

|

Primary Strategic Driver

|

Key 2025 Development

|

Core Biomedical Metal Focus

|

|

United States

|

Additive manufacturing & MedTech innovation

|

FDA clearances and alloy powder capacity expansion

|

Titanium alloys, Nitinol, 3D-printed implants

|

|

South Korea

|

Medical device localization

|

Game-changer medical device funding

|

Dental implants, surgical robotics metals

|

|

China

|

New Materials sovereignty

|

Ultra-pure non-ferrous metal scale-up

|

Tantalum, specialty stainless steel

|

|

India

|

PLI-led indigenization

|

Specialty steel investments for healthcare

|

Biocompatible steel, titanium components

|

|

Germany

|

EU MDR optimization & sustainability

|

AI-driven wire and coating innovation

|

Nitinol, cobalt-chrome, green metallurgy

|

|

Japan

|

Materials DX & aging population

|

AI-simulated bio-active alloy discovery

|

Titanium–zirconium, osseointegrative alloys

|

Biomedical Metal Market Report Scope

Biomedical Metal Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.6 Billion

|

|

Market Size (2035)

|

$73.3 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Material Type (Titanium & Titanium Alloys, Stainless Steel, Cobalt-Chromium Alloys, Nickel-Titanium Alloys, Precious Metals, Other Metals), By Application (Orthopedic, Cardiovascular, Dental, Craniomaxillofacial, Neurological, Surgical Instruments), By Final Product Form (Powders, Wrought Products, Cast Products, Forged Products), By Manufacturing Process (Machining, Casting, Forging, Additive Manufacturing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Carpenter Technology Corporation, ATI Inc., AMETEK Inc., Fort Wayne Metals, G&S Titanium, QuesTek Innovations LLC, DSM-Firmenich AG, Johnson Matthey PLC, Zimmer Biomet Holdings Inc., Stryker Corporation, Smith & Nephew plc, Medtronic plc, Orthofix Medical Inc., Aperam S.A., The Japan Steel Works Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biomedical Metal Market Segmentation

By Material Type

- Titanium and Titanium Alloys

- Stainless Steel

- Cobalt-Chromium Alloys

- Nickel-Titanium Alloys

- Precious Metals

- Other Metals

By Application

- Orthopedic

- Cardiovascular

- Dental

- Craniomaxillofacial

- Neurological

- Surgical Instruments

By Final Product Form

- Powders

- Wrought Products

- Cast Products

- Forged Products

By Manufacturing Process

- Machining

- Casting

- Forging

- Additive Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Biomedical Metal Market

- Carpenter Technology Corporation

- ATI Inc.

- AMETEK, Inc.

- Fort Wayne Metals Research Products Corp.

- G&S Titanium

- QuesTek Innovations LLC

- DSM-Firmenich AG

- Johnson Matthey PLC

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Smith & Nephew plc

- Medtronic plc

- Orthofix Medical Inc.

- Aperam S.A.

- The Japan Steel Works, Ltd.

*- List not Exhaustive