Market Overview: Blue Hydrogen Is Emerging as the Fastest-Deployable Path To Industrial-Scale Decarbonization

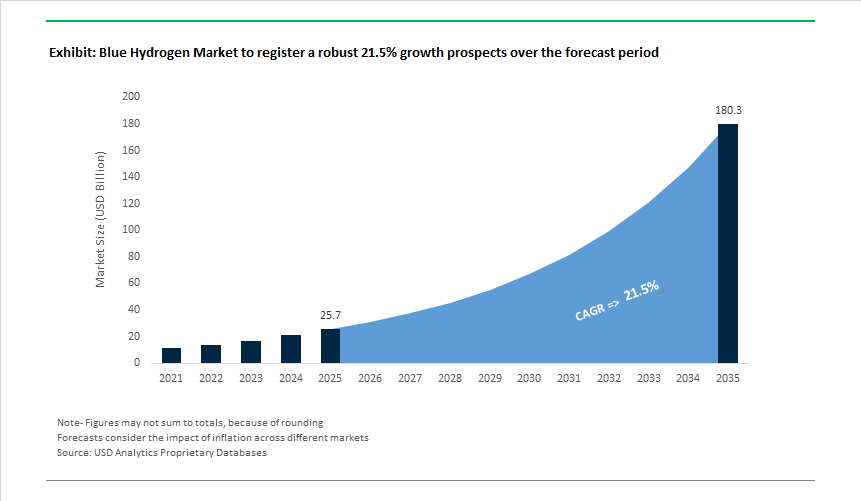

The Blue Hydrogen Market is valued at USD 25.7 billion in 2025 and is projected to reach USD 180.2 billion by 2035, expanding at a 21.5% CAGR as governments, energy majors, and heavy industries prioritize near-term carbon abatement without dismantling existing gas-based infrastructure. Today, blue hydrogen is no longer framed as a transitional afterthought; it is being positioned as a scale-ready decarbonization platform for sectors where electrification or green hydrogen remains technically or economically constrained.

The market’s momentum is being driven by a pragmatic reality: industrial hydrogen demand already exists at scale, particularly in refining, ammonia, methanol, steel processing, and chemicals. Blue hydrogen allows these sectors to cut lifecycle emissions sharply by pairing proven hydrogen production routes with high-efficiency carbon capture and storage (CCS), rather than waiting for green hydrogen supply chains to mature. As a result, blue hydrogen projects are increasingly aligned with industrial cluster strategies, where shared CO₂ transport and storage infrastructure materially lowers cost per ton of avoided emissions.

Technology maturity is a central advantage. Steam Methane Reforming (SMR) continues to underpin roughly 60-65% of blue hydrogen capacity, reflecting decades of operational experience, existing asset bases, and relatively straightforward CCS retrofitting. However, the strategic direction is shifting toward Auto Thermal Reforming (ATR) for large-scale newbuild projects, as ATR enables higher single-train capacities, more concentrated CO₂ streams, and capture rates consistently targeting 90-98%, which are rapidly becoming the benchmark for low-carbon hydrogen certification. In this context, blue hydrogen is evolving from “grey-plus-CCS” into a certification-driven product class where carbon intensity thresholds determine market access.

Economics remain tightly linked to feedstock and policy. Natural gas accounts for approximately 65-70% of operating expenditure, making long-term gas sourcing, price hedging, and regional cost advantages decisive for project bankability. CCS integration introduces an energy penalty-typically 20-25% higher energy demand for SMR-based systems-which further reinforces the need for process optimization, waste-heat recovery, and scale efficiencies. Despite this, blue hydrogen remains cost-competitive versus green hydrogen in most regions through the mid-2030s, particularly where carbon pricing, offtake contracts, and shared CCS infrastructure are in place.

Policy frameworks are now accelerating final investment decisions. Incentives such as the U.S. 45Q tax credit, along with European Contracts for Difference (CfDs) and industrial decarbonization funds, are converting blue hydrogen from a technically viable option into a financeable asset class. In 2025 alone, policy support enabled more than 1.5 million tonnes per annum of blue hydrogen capacity to reach FID, signaling a shift from pilot projects to multi-billion-dollar industrial deployments.

Market Analysis: Rapid Global Project Acceleration, Ccs Milestones, Atr Scale-Up & Blue Ammonia Trade Expansion

Momentum across the Blue Hydrogen industry accelerated over the past two years, driven by government incentives, refinery decarbonization plans, and large-scale CCS infrastructure buildout. In February 2024, the UK recorded a major investment announcement for the country’s first large-scale Blue Hydrogen facility at the Stanlow refinery, advancing heavy industry decarbonization in one of Europe’s most emissions-intensive clusters. By September 2024, Mitsubishi Corporation and ExxonMobil formalized a partnership at the Baytown Hydrogen Project in the United States, emphasizing over 1 million tons of low-carbon ammonia exports, reinforcing Blue Ammonia's role in transpacific decarbonization corridors.

In March 2025, the sector witnessed multiple strategic advancements: Uniper and Kyuden International signed an MoU to build a hydrogen-ammonia trading network between Europe and Japan, while Aramco acquired a 50% stake in the Blue Hydrogen Industrial Gases Company (BHIG) to expand a regional low-carbon hydrogen network in Saudi Arabia.

Technology advancements further strengthened the market. Topsoe announced in February 2025 its new SynCOR™ SMR platform, which can achieve up to 99% CO₂ capture with reduced heat penalties, representing a breakthrough in high-capture SMR systems. In April 2025, CF Industries reached FID on the 1.4 Mt/year Blue Ammonia Blue Point Complex in Louisiana-one of the largest Blue Ammonia plants globally. Finally, by October 2025, ExxonMobil’s Baytown complex achieved a major EPC milestone, confirming its trajectory toward becoming the world’s largest low-carbon hydrogen facility, with >98% CO₂ capture via Denbury’s CCS network.

Blue Hydrogen Market Trends and Opportunities

Trend 1: Strategic Co-location with Ammonia Export Infrastructure for Global Trade

Blue hydrogen is increasingly commercialized in the form of blue ammonia, solving the logistical constraints of hydrogen transport while enabling immediate access to power, shipping, and industrial demand centers.

World-scale export hubs are now operationally defined, not conceptual. In September 2024, ADNOC committed $2 billion to port and conversion infrastructure at Al Ruwais to support 1 mtpa of blue ammonia, explicitly targeting Japanese and European utilities conducting live co-firing and grid-integration trials. These early cargoes are strategically important—they validate end-use compatibility and underpin long-term offtake contracts that de-risk upstream hydrogen production.

Market consolidation signals maturity. In November 2025, Woodside Energy’s $2.35 billion acquisition of OCI’s Beaumont blue ammonia project marked a pivot from pilot-scale positioning to balance-sheet-backed export platforms. The U.S. Gulf Coast’s access to low-cost gas, existing SMR assets, CO₂ sequestration sites, and deepwater ports gives it a structural advantage over greenfield hydrogen exporters.

Shipping economics are reinforcing ammonia dominance. By mid-decade, industry projections indicate that ~60%+ of hydrogen trade will move as ammonia, not liquid hydrogen. This is driving investment in Very Large Ammonia Carriers (VLACs), with fleet expansion emerging as a gating factor for transcontinental hydrogen trade rather than upstream production capacity.

Trend 2: Shift Toward Near-Zero-Emission Blue Hydrogen via High-Capture CCUS

The definition of “blue” hydrogen is tightening. Projects designed around 60–80% CO₂ capture are rapidly becoming non-bankable, replaced by architectures targeting 95%+ capture with residual emissions neutralized on-site.

Capture-rate escalation is now a competitive differentiator. The Net-Zero Hydrogen Energy Complex in Alberta is engineered to exceed 95% CO₂ capture, with remaining emissions balanced through hydrogen-fired power generation. This configuration establishes a reference model for lifecycle-compliant blue hydrogen in jurisdictions with stringent carbon accounting.

Modularity is accelerating brownfield adoption. In 2025, U.S. federal funding supported the integration of modular solvent-based capture systems capable of retrofitting existing SMRs and gas turbines. These units are designed as repeatable templates rather than bespoke installations—critical for scaling blue hydrogen across hundreds of existing industrial assets globally.

Energy-penalty optimization is reshaping cost curves. Process-level heat integration demonstrated in 2025 shows that advanced capture plants can meet 100% of reboiler steam demand internally, eliminating the historical efficiency penalty that undermined blue hydrogen competitiveness. This materially improves project resilience in carbon-priced markets.

Opportunity 1: Monetization Under the U.S. 45V Clean Hydrogen Tax Credit

The finalization of Section 45V in January 2025 transformed blue hydrogen economics from policy-exposed to policy-bankable, provided projects meet strict lifecycle thresholds.

Lifecycle carbon intensity now determines revenue, not labels. Blue hydrogen projects emitting below 4 kg CO₂e/kg H₂ qualify for credits ranging from $0.60 to $3.00/kg, with the highest tier reserved for sub-0.45 kg CO₂e performance. For capital-intensive CCUS systems, this incentive materially shortens payback periods and unlocks lower-cost project finance.

Regulatory clarity reduces development risk. The acceptance of Energy Attribute Certificates (EACs) and the ability to lock in a Provisional Emissions Rate (PER) at FEED stage allow developers to de-risk Final Investment Decisions before construction. This is catalyzing a wave of blue hydrogen FIDs across the Gulf Coast and Appalachian basins.

Opportunity 2: Rapid Decarbonization via Retrofitting Existing Grey Hydrogen Assets

Retrofitting existing SMR-based hydrogen units remains the fastest and lowest-risk growth pathway for blue hydrogen deployment.

Brownfield economics are compelling. Converting an existing grey hydrogen plant with post-combustion capture typically requires 30–40% less capital per unit of capacity than greenfield electrolysis projects, while avoiding electrolyzer supply bottlenecks and grid-connection delays.

Industrial clusters amplify scale. Shared CO₂ transport and storage networks—such as those forming in the UK’s Teesside and Humber regions—enable multiple refineries and chemical plants to transition simultaneously. This cluster model reduces per-tonne capture costs and accelerates compliance with tightening carbon regulations.

Regulatory pressure is accelerating adoption. Rising ETS prices and the enforcement trajectory of the EU Carbon Border Adjustment Mechanism (CBAM) are converting decarbonization from a reputational choice into a cost-avoidance imperative. For refineries and fertilizer plants, blue hydrogen retrofits represent the most immediate hedge against carbon-adjusted trade penalties.

Market Share Analysis: Blue Hydrogen Market

Market Share by Technology: SMR + CCUS Dominates Through Cost-Qualified Scale and Policy Alignment

Steam Methane Reforming combined with Carbon Capture, Utilization, and Storage (SMR + CCUS) accounts for around 60% of global blue hydrogen deployment because it is the only technology that simultaneously satisfies industrial-scale volume requirements, low-carbon regulatory thresholds, and near-term cost competitiveness. In 2025, the technology crossed a decisive credibility milestone when Air Products demonstrated 95% CO₂ capture rates at its Louisiana Clean Energy Complex, capturing more than five million tons of CO₂ annually—well within eligibility limits for incentives such as the U.S. 45V clean hydrogen tax credit. From a buyer’s perspective, this level of capture resolves the long-standing emissions credibility gap between blue and green hydrogen. Equally important is hydrogen quality: SMR-based systems engineered by Linde consistently deliver 99.97% hydrogen purity, eliminating downstream purification costs for refinery catalysts and fuel-cell applications. Scalability remains the decisive economic lever—industry benchmarks from Shell indicate that SMR trains can be deployed at ten times the capacity of current electrolyzer projects, enabling world-scale hydrogen supply without massive land or grid expansion. When combined with 30–50% lower levelized hydrogen costs versus green alternatives, as quantified by Johnson Matthey, SMR + CCUS emerges not as a transitional option but as the default industrial decarbonization pathway through the late 2020s.

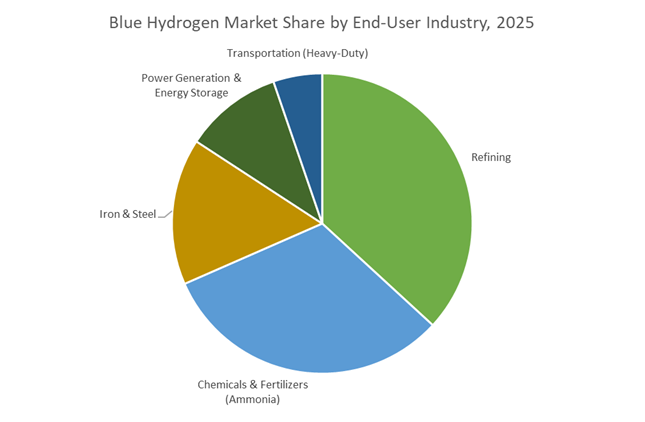

Market Share by End-User Industry: Refining Leads Adoption Through Immediate Substitution Economics

Oil refining represents roughly 35% of blue hydrogen demand because it offers the fastest, lowest-friction route to emissions reduction in sectors already structurally dependent on hydrogen. Refineries consume over 40% of global captive hydrogen volumes, primarily for hydrocracking and desulfurization, making blue hydrogen a direct drop-in replacement for grey hydrogen rather than a speculative fuel switch. In 2025, this substitution logic translated into large-scale contracts, with operators such as TotalEnergies and Air Liquide deploying blue hydrogen at facilities like La Mède to achieve annual emissions reductions of ~130,000 tons, a concrete metric increasingly required by ESG-driven capital committees. European hubs including Antwerp and Leuna have already secured 25% or more of long-term hydrogen supply from low-carbon sources, signaling that early adopters are locking in cost and compliance advantages ahead of tightening carbon pricing. Beyond core refining, producers are leveraging scale to serve adjacent markets: refinery-linked blue hydrogen plants now supply 30-ton-per-day liquid hydrogen units for heavy-duty transport, creating dual-revenue demand stability. This combination of immediate compliance value, contract-backed volumes, and cross-sector integration explains why refining remains the anchor end-use sustaining blue hydrogen’s market leadership in 2025.

Competitive Landscape: Leadership Driven by CCS Scalability, ATR/SMR Technology, and Industrial Cluster Integration

Competition in the Blue Hydrogen industry is defined by the ability to scale CCS, secure long-term feedstock, deploy SMR/ATR technologies efficiently, and integrate low-carbon hydrogen into refinery and petrochemical clusters. Companies that combine technology licensing, infrastructure ownership, and global export capability retain the strongest strategic position.

Linde - Global CCS-Integrated Hydrogen Pioneer with Gulf Coast Network Dominance

Linde is building one of the world’s largest Blue Hydrogen facilities in Beaumont, Texas, backed by a USD 1.8 billion investment, with plans to sequester 1.7 million tons of CO₂ annually starting in 2025. Its competitive strength lies in integrating hydrogen production into an expansive Gulf Coast pipeline network that supplies refiners, petrochemical producers, and industrial gas consumers. Linde’s portfolio includes SMR and ATR technologies with proprietary CCS integration solutions, while partnerships such as its 24 MW project with Yara reinforce its global hydrogen EPC leadership.

Exxonmobil - ATR Scale Leadership and Export-Driven Blue Ammonia Strategy

ExxonMobil’s Baytown Complex is poised to become the world’s largest low-carbon hydrogen facility, capable of producing up to 1 Bcf/day. Its strategy leverages ATR technology to produce high-concentration CO₂ streams, enabling >98% capture through Denbury’s CCS network. Collaboration with Mitsubishi Corporation expands the site’s role as a major Blue Ammonia export hub, producing >1 million tons/year for Asia-Pacific markets. ExxonMobil is positioning Baytown as a global benchmark for large-scale, export-ready Blue Hydrogen infrastructure.

Shell - Industrial Decarbonization Anchor for UK and European Hydrogen Clusters

Shell is pursuing Blue Hydrogen projects such as Acorn CCS and H2Teesside, anchoring industrial decarbonization in the UK by supplying low-carbon hydrogen to refineries, chemicals, and power assets. Shell’s Net Zero strategy forecasts CCS-enabled hydrogen supplying ~40% of its hydrogen mix by 2050, reinforcing Blue Hydrogen’s long-term role alongside green hydrogen. Its advantage is integration of existing refinery infrastructure, lowering CAPEX and enabling faster regional deployment.

BP - Cluster-Based SMR+CCS Developer Driving UK’s Largest Blue Hydrogen Initiative

BP’s flagship H2Teesside project aims to provide 15% of the UK’s 2030 low-carbon hydrogen target, demonstrating its strategic impact on national hydrogen policy. BP focuses on a disciplined portfolio of ~5-7 hydrogen and CCS projects that combine SMR with advanced CCS retrofits. Its strong pipeline connectivity and provision of Blue Hydrogen to industrial customers, transport fueling, and grid applications positions BP as a key enabler of hydrogen-led decarbonization.

Air Products - Global Hydrogen Logistics Leader with POX Technology and Middle East Expansion

Air Products maintains a unique advantage with its extensive North American hydrogen pipeline network and flexible POX (Partial Oxidation) technology suitable for heavy hydrocarbons, coal, and natural gas feedstocks. The company has invested >$15 billion in clean energy projects, including the BHIG joint venture in Saudi Arabia (now 50% acquired by Aramco). Its strength lies in controlling the entire hydrogen value chain-from production to liquefaction, cryogenic transport, and Blue Ammonia export capabilities.

The United States has consolidated its position as the global epicenter of blue hydrogen investment, underpinned by unmatched fiscal incentives and low-cost shale gas availability. The convergence of Section 45Q carbon sequestration credits and Section 45V clean hydrogen production credits under the Inflation Reduction Act (IRA) has fundamentally reshaped project bankability. In 2025, developers are increasingly “stacking” these incentives—capturing up to $85/tonne of permanently sequestered CO₂ while simultaneously qualifying for hydrogen production credits—making U.S. blue hydrogen the lowest-risk, highest-IRR pathway among low-carbon hydrogen options.

This policy framework has enabled world-scale Final Investment Decisions (FIDs). ExxonMobil’s Baytown, Texas project—moving toward FID in 2025—targets 1 billion cubic feet per day of blue hydrogen with a 98% CO₂ capture rate, positioning it as the largest low-carbon hydrogen facility globally. The project’s credibility was reinforced by ADNOC acquiring a 35% equity stake, signaling deep transatlantic capital alignment. Complementing this, CF Industries, alongside JERA and Mitsui, reached FID on the Blue Point Complex in Louisiana, a $2+ billion ATR-based facility producing 1.4 million tonnes of blue ammonia annually, cementing the U.S. Gulf Coast as the world’s most mature blue hydrogen and ammonia hub.

United Kingdom: Cluster-Based Decarbonization and Track-2 Momentum

The United Kingdom is pursuing a structurally differentiated blue hydrogen strategy centered on industrial cluster decarbonization rather than standalone mega-projects. Through its Track-1 and Track-2 CCUS cluster sequencing, the UK is embedding blue hydrogen directly into steel, chemicals, refining, and power-generation zones. The July 2025 Hydrogen Strategy Update confirmed over £500 million for CO₂ transport and storage infrastructure, anchoring long-term confidence for hydrogen-linked industrial investments.

The HyNet North West cluster—anchored by EET Hydrogen—is progressing toward first production in 2026–2027, with a stated ambition of 4 GW of hydrogen capacity by 2030. Simultaneously, Viking CCS and Acorn CCS were elevated to Track-2 priority, with specific blue hydrogen emitters expected to be confirmed by late 2025. Critically, the UK’s Low Carbon Hydrogen Business Model (LCHBM)—a CfD-style revenue stabilization mechanism—has insulated developers from gas price volatility and CO₂ storage cost risk, making the UK one of the most policy-derisked blue hydrogen markets globally.

Canada: Net-Zero Blue Hydrogen Anchored in Alberta Geology

Canada’s blue hydrogen strategy is built around a “low-carbon intensity first” doctrine, leveraging world-class CO₂ storage geology to deliver net-zero lifecycle emissions. Alberta has emerged as the nucleus of this strategy. Air Products’ C$1.6 billion Edmonton Net-Zero Hydrogen Energy Complex is nearing completion in 2025, integrating ATR technology with a hydrogen-fueled power plant to neutralize residual emissions. This “Blue, but Better” model has become a global reference for net-zero blue hydrogen design.

On the policy front, the Clean Hydrogen Investment Tax Credit (ITC)—enabled by Bill C-59—became fully operational in 2025, offering up to 40% refundable credits for projects meeting stringent carbon intensity thresholds. Provincial support further strengthens the ecosystem: Alberta committed $57 million across hydrogen initiatives to accelerate blending into natural gas grids and industrial use. Collectively, these measures position Canada as a premium supplier of low-CI blue hydrogen and ammonia to export-oriented markets seeking compliance with emerging carbon border regimes.

Saudi Arabia: Blue Ammonia Export Leadership and Certification Power

Saudi Arabia is redefining blue hydrogen through export-scale blue ammonia, capitalizing on its gas reserves and integrated petrochemical infrastructure. In July 2025, Saudi Aramco and SABIC achieved the world’s first independent certification for blue hydrogen and blue ammonia, a critical milestone that unlocks premium offtake into Japan and South Korea—markets that demand verified low-carbon credentials.

Feedstock security is anchored by the $11 billion Jafurah gas development, while Aramco’s 50% stake in the Blue Hydrogen Industrial Gases Company (BHIG) formalizes operational control across the value chain. Strategically, Saudi Arabia finalized long-term offtake MOUs with EnBW (Germany) and Marubeni (Japan) in early 2025, targeting 200,000 tonnes per year of blue ammonia exports by 2030. This positions the Kingdom not merely as a producer, but as a price-setting exporter in the emerging low-carbon ammonia trade.

United Arab Emirates: Dual-Track Domestic Scaling and Global Equity Stakes

The UAE is executing a dual-track blue hydrogen strategy, combining domestic industrial scale with equity participation in overseas mega-projects. At home, ADNOC’s TA’ZIZ Industrial Chemicals Zone in Ruwais advanced a $1.7 billion methanol and blue ammonia project in February 2025. The facility is designed to integrate into a CCS network capable of capturing 10 million tonnes of CO₂ annually by 2030, positioning TA’ZIZ as one of the world’s most carbon-efficient industrial hubs.

Internationally, ADNOC’s 35% ownership in ExxonMobil’s Baytown project secures strategic exposure to U.S. hydrogen markets and IRA-linked cash flows. Beyond blue hydrogen, the UAE is hedging technology risk through innovation: in 2025, ADNOC launched a methane pyrolysis (turquoise hydrogen) pilot with Levidian, producing hydrogen and solid graphene without CO₂ emissions—signaling long-term optionality beyond reforming-based pathways.

Norway: CCS-Centric Recalibration and Regional Hub Economics

Norway’s blue hydrogen strategy in 2025 reflects a pragmatic recalibration. Following the withdrawal of Equinor and Shell from the Norway–Germany hydrogen pipeline project in late 2024, the focus has shifted toward regional, high-value industrial hubs anchored by world-class CCS infrastructure. This pivot reduces capital intensity while preserving Norway’s strategic relevance in European decarbonization.

The Barents Blue ammonia project in Hammerfest—led by Equinor and Vår Energi—advanced CCS planning in 2025, centering on the Polaris storage license to achieve >95% capture rates. Crucially, the Northern Lights CCS project (Equinor, Shell, TotalEnergies) became commercially operational in 2025, providing open-access CO₂ transport and storage. This “open-source CCS” model is now the backbone for multiple blue hydrogen and ammonia projects across Northern Europe.

2025 Strategic Matrix: Blue Hydrogen National Milestones

Blue Hydrogen Strategic Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Technology Focus

|

|

United States

|

IRA tax credit synergy

|

Exxon Baytown FID; 35% ADNOC stake

|

ATR/SMR with ~98% CO₂ capture

|

|

United Kingdom

|

Industrial clusters

|

July 2025 Hydrogen Strategy update

|

Track-1 & Track-2 CCUS hubs

|

|

Canada

|

Low-CI sovereignty

|

C$1.6B Air Products net-zero complex

|

ATR + hydrogen-fueled power

|

|

Saudi Arabia

|

Export leadership

|

World-first blue ammonia certification

|

Jafurah gas + blue NH₃

|

|

United Arab Emirates

|

Industrial scaling + equity

|

$1.7B TA’ZIZ ammonia project

|

Blue NH₃ + turquoise H₂

|

|

Norway

|

CCS-led hub economics

|

Northern Lights CCS operational

|

Open-access CO₂ storage

|

Blue Hydrogen Market Report Scope

Blue Hydrogen Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.7 Billion

|

|

Market Size (2035)

|

$180.2 Billion

|

|

Market Growth Rate

|

21.5%

|

|

Segments

|

By Technology (SMR with CCUS, ATR with CCUS, Gas POX with CCUS, Methane Pyrolysis, SMR–ATR Hybrid Systems), By End-User Industry (Refining, Chemicals & Petrochemicals, Iron & Steel, Power Generation, Transportation), By Distribution Mode (Pipeline, Cryogenic Liquid Tankers, Ammonia Carriers, LOHC)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Air Products and Chemicals Inc., Linde plc, Saudi Aramco, Equinor ASA, Shell plc, Air Liquide S.A., ExxonMobil Corporation, Mitsubishi Heavy Industries, Johnson Matthey, Cummins Inc., Technip Energies, CF Industries Holdings Inc., JERA Co. Inc., PetroChina Company Limited, Wood Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Blue Hydrogen Market Segmentation

By Technology

- Steam Methane Reforming (SMR) with CCUS

- Auto-Thermal Reforming (ATR) with CCUS

- Gas Partial Oxidation (POX) with CCUS

- Methane Pyrolysis (Turquoise Hydrogen)

- SMR-ATR Hybrid Systems

By End-User Industry

- Refining

- Chemicals & Petrochemicals

- Iron & Steel

- Power Generation

- Transportation

By Distribution Mode

- Pipeline (Gaseous)

- Cryogenic Liquid Tankers

- Ammonia Carriers

- Liquid Organic Hydrogen Carriers (LOHC)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Blue Hydrogen Market

- Air Products and Chemicals, Inc.

- Linde plc

- Saudi Aramco

- Equinor ASA

- Shell plc

- Air Liquide S.A.

- ExxonMobil Corporation

- Mitsubishi Heavy Industries

- Johnson Matthey

- Cummins Inc.

- Technip Energies

- CF Industries Holdings, Inc.

- JERA Co., Inc.

- PetroChina Company Limited

- Wood Group

*- List not Exhaustive