Bronopol Market Overview: Water Treatment Expansion, Oil & Gas Microbial Control, and Personal Care Preservation Push Market to $2.3 Billion by 2034

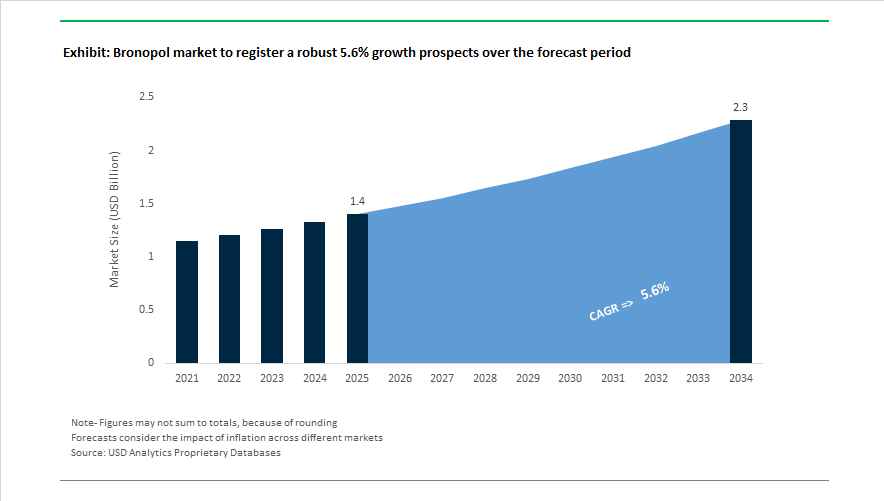

The global Bronopol market is valued at USD 1.4 billion in 2025 and is forecast to reach USD 2.3 billion by 2034, registering a steady CAGR of 5.6% between 2025 and 2034. Market expansion is fundamentally driven by accelerating demand for industrial water treatment biocides, oil & gas corrosion inhibitors, cosmetic preservatives, and agrochemical antimicrobial additives. According to World Health Organization, nearly 1.7 billion people relied on feces-contaminated water sources as of late 2024, forcing municipalities and industrial operators to scale deployment of Bronopol-based microbial control solutions across purification plants, cooling systems, and wastewater infrastructure.

Operational demand remains strongest in North America, which contributes roughly 40% of global Bronopol revenue, largely due to oil & gas applications targeting Sulfate-Reducing Bacteria (SRB). Industry benchmarks show that 150 ppm shock dosing reduces SRB counts by over 90% within 48 hours, preventing corrosion-related equipment failures costing millions of dollars. Simultaneously, the $500+ billion global cosmetics and personal care industry continues to rely on Bronopol for rinse-off formulations due to its high efficacy at ultra-low concentrations, despite rising “preservative-free” claims. Growth is further reinforced by a 2% rebound in global fertilizer usage during 2024, boosting Bronopol adoption in agrochemical bactericides, while U.S. oil and gas revenues exceeding USD 330 billion are sustaining demand for microbiostats in HVAC and open-recirculating cooling systems. For buyers, Bronopol’s value proposition centers on cost-efficient antimicrobial performance, infrastructure protection, regulatory compliance, and formulation stability across industrial, consumer, and agricultural markets.

Bronopol Market Analysis: Supply Chain Localization, Sustainability Chemistry, and Capacity Investments Redefine Competitive Dynamics

The Bronopol market entered a structural transition phase beginning in January 2025, when BASF expanded its ISCC EU-certified biomass-balanced methanol portfolio, strengthening sustainability credentials for downstream antimicrobial products. This momentum accelerated in February 2025, as new U.S. tariffs on brominated compounds disrupted global sourcing routes, prompting manufacturers to realign supply chains and prioritize domestic production. Sustainability gained further traction in May 2025, after The Carbon Trust verified several BASF intermediates with Product Carbon Footprints significantly below market averages, enabling Bronopol suppliers to position low-carbon biocides toward ESG-driven industrial procurement programs.

Pharmaceutical-grade infrastructure also expanded rapidly. In June 2025, BASF launched a GMP Solution Center in Michigan to supply high-purity excipients and bioprocessing ingredients, reinforcing Bronopol’s penetration into regulated life science applications. Meanwhile, LANXESS advanced its localization strategy with a production expansion at its Bushy Park facility in South Carolina in September 2025, improving supply reliability for U.S. pharmaceutical and industrial customers. This was followed by a 50% capacity increase and technical upgrade at Rhein Chemie’s Qingdao site in November 2025, strengthening APAC delivery capabilities for specialty preservatives and microbial control additives. Portfolio optimization also reshaped the landscape in October 2025, when BASF divested its decorative paints business to Sherwin-Williams, allowing greater strategic focus on Industrial Solutions and Nutrition & Care segments where Bronopol plays a critical formulation role.

The sustainability narrative intensified in January 2026, as LANXESS reported leading positions in MSCI ESG and ISS ESG ratings, signaling deeper commitment to environmentally responsible production of consumer protection chemicals. Shortly after, in February 2026, BASF announced a major 1,4-butanediol (BDO) value-chain reinforcement at Ludwigshafen, securing upstream supply of key precursors required for complex organic biocides, including Bronopol. Collectively, these developments reveal three defining market shifts: accelerated local-for-local manufacturing, rising adoption of low-carbon and biomass-balanced intermediates, and expanding pharmaceutical-grade capacity. For industry professionals, this marks Bronopol’s evolution from a conventional industrial biocide into a strategic antimicrobial platform aligned with ESG compliance, supply resilience, and high-purity application growth.

Regulatory Crackdowns and Industrial Usage Realignment Driving Trends and Opportunities in the Bronopol Market

Regulatory Phase-Out in Consumer Care and NDSRI Compliance Deadlines Accelerate Reformulation

Bronopol is undergoing a structural demand shift driven by global regulatory pressure on nitrosamine-prone and formaldehyde-releasing preservatives. Effective September 1, 2025, the EU 7th CMR Omnibus Regulation expands the prohibited substances list and restricts bronopol in leave-on formats due to sensitization and endocrine-disruption concerns. Although bronopol remains permitted in rinse-off products, major multinational brands are proactively removing it from shampoos and cleansers to align with Clean Beauty standards and retailer safety lists. The urgency is amplified by the U.S. FDA’s August 1, 2025 NDSRI compliance deadline, which requires manufacturers to mitigate nitrosamine formation. Because bronopol can react with secondary amines, formulators are transitioning toward nitrosamine-inhibited blends or switching to organic-acid-based biocides in personal care. These enforcement timelines are reshaping procurement and favoring suppliers capable of offering reformulation support and impurity-risk modeling.

Capacity Rationalization and Portfolio Restructuring Shift Bronopol Toward Industrial Applications

The competitive landscape is pivoting away from consumer care reliance and moving toward high-margin industrial applications where bronopol’s efficacy profile is strategically advantageous. Throughout 2024 and 2025, LANXESS executed its FORWARD efficiency initiative targeting long-term cost reductions and exit from non-core polymer books. As part of the transition, resource allocation has been redirected toward Consumer Protection divisions, where bronopol is being positioned as a premier industrial preservative for sanitation, HVAC cooling towers, and water treatment. The operational blueprint includes regional capacity reinforcement, such as the September 2025 expansion of its Bushy Park production site in the United States, aimed at improving supply resilience under inflationary freight costs and tariff volatility. This “local-for-local” production model is gaining momentum across the market as buyers seek security against early-2025 logistical disruptions that strained bronopol availability.

Bronopol as a Critical In-Can Preservative in High-Humidity Paint and Coating Markets

The transition toward waterborne and Low-VOC coating systems has increased risk of microbial spoilage in manufacturing and storage. Bronopol has become integral to formulation strategies in humid regions such as Southeast Asia and the Southern United States, where can temperatures routinely exceed 30°C. Paint and coatings producers are using bronopol in synergistic blends with BIT to deliver rapid microbial kill rates and prevent aesthetic defects like gas formation and color shifts. Technical bulletins from 2025 highlight the value proposition for coatings OEMs: bronopol performs effectively at ultra-low dosage rates, as little as 0.01 percent, allowing manufacturers to offset rising pigment and surfactant costs without compromising product stability.

High-pH Biocide Advantages Position Bronopol for Oil and Gas Drilling and Well Integrity Programs

Within oilfield chemistry, bronopol is gaining renewed relevance due to its durability in water-based drilling mud systems, which increasingly incorporate biodegradable materials such as sugarcane bagasse to improve rheology. These additives are nutrient-rich and highly prone to microbial attack, requiring biocides that remain active across variable pH environments. Bronopol’s ability to maintain efficacy between pH 5.0 and 9.0 enables extended protection of viscosifiers and shale inhibitors during storage, particularly at remote drilling pads where maintenance intervals are long. Its indirect function as a corrosion inhibitor, by suppressing sulfate-reducing bacteria, further ties bronopol to wellbore integrity initiatives. As operators increase chemical spend to protect downhole assets, bronopol is emerging as a cost-aligned alternative to premium high-temperature biocides.

Bronopol Market Share and Segmentation Insights

Market Share by Form: Crystalline Powder Leads Volume While Liquids Enable Safer Processing

Crystalline powder holds 54% of bronopol demand in 2025, favored for its high active content, long shelf life, and dosing precision across industrial water treatment and oil and gas applications where bulk handling is standard. Granules and pellets rank second, offering reduced dusting and improved worker safety, making them preferred in personal care and pharmaceutical manufacturing environments with automated metering systems. Liquid solutions are the smallest but fastest-growing format, eliminating dissolution steps and reducing operator exposure, with increasing adoption in closed-system production for cosmetics and water-based coatings, despite higher logistics costs and lower active concentration.

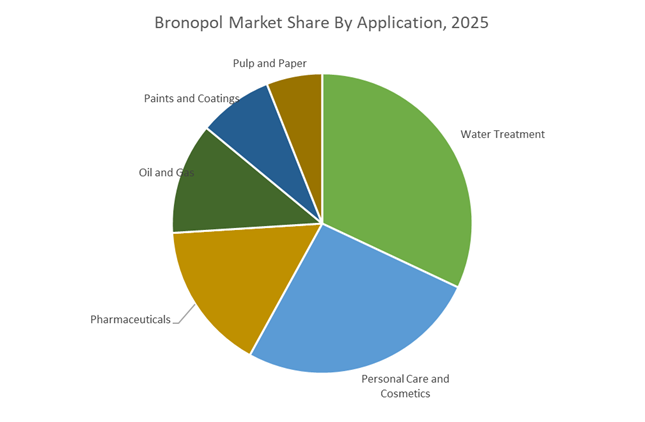

Market Share by Application: Water Treatment Anchors Volume as Cosmetics Drive Value Growth

Water treatment accounts for 32% of bronopol consumption in 2025, leveraging its broad-spectrum efficacy against bacteria, fungi, and algae in cooling towers, air washers, and paper mill circuits, with demand tracking industrial output. Personal care and cosmetics represent the second-largest and fastest-growing application, using bronopol as a formaldehyde-releasing preservative in shampoos, lotions, and wet wipes, particularly across Asia-Pacific and Latin America where regulatory pressure is less restrictive. Pharmaceuticals utilize bronopol in ophthalmic solutions and topical formulations under stringent pharmacopeial standards. Oil and gas forms a volatile niche, applying bronopol to control sulfate-reducing bacteria in drilling and produced water systems. Paints and coatings adopt bronopol as an in-can preservative amid tightening isothiazolinone regulations, while pulp and paper remains a mature segment facing gradual substitution by oxidizing biocides.

Competitive Landscape of the Bronopol Market

The global Bronopol market in 2026 is defined by tightening biocide regulations, rising demand for low-toxicity preservatives, and the shift toward mass-balanced, renewable-feedstock formulations across personal care, industrial water treatment, oil & gas, and paints and coatings. Competition centers on ultra-high-purity Bronopol grades, multifunctional preservative blends, digitalized supply chains, and regulatory stewardship. Leading manufacturers are differentiating through predictive analytics, low-concentration efficacy (0.01% to 0.05% ), hybrid biocide systems, and localized technical support, positioning Bronopol as a cost-effective alternative to parabens while meeting evolving ECHA and sustainability requirements.

Verbund-driven ultra-pure Bronopol leadership from BASF SE

BASF competes through its Care Chemicals division, leveraging its Verbund integration to supply ultra-high-purity Bronopol for sensitive medical, water treatment, and pulp applications. Its Myacide® AS and Myacide® G1 grades remain the 2026 global benchmark for rapid bacterial knockdown in industrial systems. Early-2026 management restructuring accelerated BASF’s Green Transformation strategy, moving its biocide portfolio toward mass-balanced renewable feedstocks. Using its Global Digital Hub in Hyderabad, BASF applies predictive analytics to manage bromine price volatility and optimize logistics. Strategically, BASF is advancing low-dose efficacy formulations, positioning Bronopol as a safer, economical paraben alternative in medical skincare.

Regulatory-first alkaline-stable Bronopol from LANXESS AG

LANXESS dominates through its Consumer Protection platform, with Bronopol-based Preventol® P series engineered for alkaline systems where conventional preservatives fail, maintaining stability up to pH 9.0. After achieving its FORWARD! €150 million savings target in late 2025, LANXESS reinvested in 2026 toward digital design for biocide delivery and ion-exchange systems. Its deep toxicology database provides a competitive edge under ECHA scrutiny of halogenated compounds. Expansion of the Bushy Park US hub now supports North American oil and gas logistics, reinforcing LANXESS’s position as a compliance-driven supplier of high-performance Bronopol preservatives.

Clean-beauty preservative cocktails pioneered by Sharon Laboratories

Sharon Laboratories has emerged in 2026 as a global innovator in multifunctional Bronopol systems for premium personal care. Its Sharon™ Biomix platform uses synergistic carriers to boost efficacy against Gram-negative bacteria while minimizing skin irritation. The company’s “Preservative Plus” strategy blends Bronopol with skin-soothing and antioxidant components, aligning with clean beauty trends. Following its BWA Water Additives acquisition, Sharon now operates a dual-track model serving both luxury cosmetics and industrial desalination. Sharomix™ 601 remains a top-selling wet-wipe preservative in 2026, prized for maintaining antimicrobial activity in high-organic-load formulations.

Heavy-industry Bronopol applications scaled by The Dow Chemical Company

Dow anchors the North American Bronopol market through large-scale deployment in oilfield biocides, HVAC systems, and construction materials. In 2026, Dow’s Bronopol is critical in fracturing fluids, preventing microbial degradation of friction reducers and hydrogen sulfide formation. Its Transform to Outperform initiative introduced fully automated batch processing to lift specialty chemical productivity. Dow integrates Bronopol with polymer and coatings expertise to deliver “system-in-a-box” mold prevention for energy-efficient insulation. With over 89% of R&D aligned to sustainability goals, Dow is advancing closed-loop biocide delivery systems to reduce worker exposure and improve industrial safety.

Digital challenge testing and hybrid preservation from Thor Group

Thor Group leads as an independent specialist in technical preservation, supplying ACTICIDE® Bronopol solutions for paints, coatings, and industrial fluids. ACTICIDE® L 30 is a 2026 staple for in-can protection against spoilage organisms. Thor’s Digital Lab enables customers to run simulated microbial risk assessments and receive optimized Bronopol dosages within minutes. The company excels in hybrid chemistries, combining Bronopol with non-halogenated organic acids to support transitions away from legacy biocides. With production in Germany, Mexico, and China, Thor delivers localized microbiological audits through its global “local touch” service model.

Cost-efficient crystalline Bronopol scale from Zhejiang Zhongxin Fluoride Materials

Zhongxin represents China’s new-generation Bronopol producers, leveraging fluorine-bromine integration to reduce production costs through advanced byproduct utilization. In 2025/2026, the company scaled its integrated platform and secured key European export certifications, becoming a Tier-2 supplier for global distributors seeking supply diversification. Zhongxin specializes in 99.9% crystalline Bronopol, favored in 2026 for its lightweight shipping profile and extended shelf life. Its precision manufacturing investments target low-byproduct synthesis pathways, specifically reducing formaldehyde release during Bronopol decomposition, positioning Zhongxin as a competitive, high-purity supplier for international industrial and personal care markets.

China Bronopol Market: Process Upgrading and Industrial Water Protection Demand

China’s bronopol industry is transitioning from volume-driven manufacturing to process-intensive, compliance-led production aligned with advanced industrial demand. A major inflection point occurred in late 2025 when the Nanjing Jiangbei New Material Technology Park commissioned a new high-efficiency bronopol synthesis line. This unit applies advanced catalytic bromination technology, improving yield by 12% while materially reducing hazardous nitromethane-derived byproducts. The upgrade reflects a broader national push to align specialty biocide manufacturing with tighter environmental and safety expectations, particularly in export-oriented clusters.

Demand growth is increasingly linked to high-tech and food security applications rather than commoditized preservation. The Ministry of Industry and Information Technology formally prioritized bronopol as a preferred non-oxidizing biocide for closed-loop circulating water systems in semiconductor fabrication plants, where microbial slime can trigger micro-corrosion and yield losses. In parallel, aquaculture has emerged as a structurally important downstream segment. Under the 2025 Fisheries Development Plan, shrimp and high-value aquatic farms in the Pearl River Delta expanded bronopol usage as a safer substitute for legacy bactericides, supporting export compliance for North American and European seafood markets. On the regulatory front, “Blue Sky” environmental audits throughout 2025 forced Shandong-based producers to migrate toward closed-cycle production systems, stabilizing long-term supply while eliminating informal capacity.

United States Bronopol Market: Energy Infrastructure Use and Preservation Reformulation

In the United States, bronopol demand is shaped by oil and gas infrastructure recovery, evolving workplace safety standards, and reformulation trends in personal care. The EPA’s extension of Workplace Chemical Protection Program compliance for laboratory and specialty chemicals during late 2024 and 2025 has influenced how antimicrobial producers manage nitromethane precursor handling, increasing investment in engineering controls and operator training rather than capacity expansion.

Industrial demand strengthened sharply alongside record U.S. natural gas output in 2025. Bronopol consumption rose in the Permian Basin as operators intensified bacterial corrosion control in hydraulic fracturing systems and midstream pipelines, where sulfate-reducing bacteria pose material integrity risks. At the formulation level, major personal care and material science suppliers such as Ashland and Dow accelerated bronopol adoption as a secondary preservative in green-label cosmetics, avoiding fluorinated chemistries amid PFAS restrictions. Regulatory oversight continues to tighten. The EPA’s September 2025 update to Aquatic Life Benchmarks retained bronopol as an approved biocide but imposed stricter runoff management obligations for municipal and industrial water users, reinforcing compliance-driven demand for controlled dosing systems.

India Bronopol Market: Export-Grade Crystallization and Clean Manufacturing Alignment

India’s bronopol market is increasingly export-oriented, supported by pharmaceutical policy incentives and environmental reform in traditional industries. Under the Production Linked Incentive Scheme for pharmaceuticals during 2025–2026, specialty chemical manufacturers in Gujarat expanded export-only units for high-purity bronopol crystals, targeting a 14% increase in shipments to regulated markets in Europe and North America. These investments emphasize crystallization control, impurity profiling, and documentation readiness rather than commodity volume.

Cost dynamics remain a defining feature. In early 2025, the Indian Specialty Chemical Price Index recorded an 11.04% increase in bronopol prices, driven by higher imported bromine costs and a market shift toward high-tensile crystalline grades required by pharmaceutical and industrial buyers. Beyond pharma, domestic policy is reshaping downstream demand. The Ministry of Textiles’ 2025 “Clean Leather Production” initiative promoted bronopol-based preservatives as alternatives to heavy-metal biocides in the Chennai leather clusters, aligning environmental compliance with export competitiveness for finished leather goods.

European Union (Germany / Belgium) Bronopol Market: Classification Discipline and Zero-Discharge Manufacturing

The European bronopol market is defined by regulatory precision, data transparency, and emission control rather than incremental demand growth. In March 2025, the European Chemicals Agency issued the 22nd Adaptation to Technical Progress under Annex VI of the CLP Regulation, mandating updated hazard classification, labeling, and safety data sheets for bronopol mixtures by May 1, 2026. This has triggered portfolio reviews among formulators supplying cleaning, detergent, and industrial water treatment segments.

Regulatory infrastructure has also evolved. By December 2025, all bronopol REACH dossiers were migrated to the ECHA CHEM database, increasing downstream visibility into impurity profiles and potential substitution assessments. The Poison Centre Notification mandate effective January 2025 further requires Unique Formula Identifier codes for all hazardous mixtures containing bronopol, adding compliance complexity for distributors. On the production side, European manufacturers such as BASF implemented advanced wastewater treatment upgrades at Verbund sites during 2025 to meet Industrial Emissions Directive expectations, ensuring zero-detectable bronopol discharge into regional waterways and reinforcing Europe’s position as a benchmark market for responsible biocide manufacturing.

Comparative Snapshot of the Bronopol Industry by Country

Bronopol Market County Level Snapshot

|

Country / Region

|

Primary Demand Driver

|

Strategic Focus

|

|

China

|

Semiconductor water systems, aquaculture

|

Yield optimization, closed-cycle compliance, export stability

|

|

United States

|

Oil and gas corrosion control, cosmetics

|

Infrastructure protection, PFAS-free reformulation

|

|

India

|

Pharmaceutical exports, leather processing

|

High-purity crystallization, cost-competitive exports

|

|

European Union

|

Cleaning, detergents, industrial water

|

Classification compliance, zero-discharge manufacturing

|

Bronopol Market Report Scope

Bronopol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Form (Crystalline Powder, Granules and Pellets, Liquid Solutions), By Purity Grade (Technical Grade, Pharmaceutical and Cosmetic Grade, Electronic Grade), By Application (Water Treatment, Oil and Gas, Personal Care and Cosmetics, Pharmaceuticals, Pulp and Paper, Paints and Coatings), By End Use Industry (Healthcare and Pharmaceuticals, Consumer Goods, Industrial Water Management, Energy, Agriculture and Aquaculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Ashland, LANXESS, Sharon Laboratories, Symbolic Pharma, Shanghai Rich Chemicals, Fujian Shaowu Yongfei Chemical, Navin Fluorine International, Wuhan Fortuna Chemical, Gayathri Chemicals and Agencies, Sai Supreme Chemicals, Mani Agro Chemicals, BQ Technology, Sushil Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bronopol Market Segmentation

By Form

- Crystalline Powder

- Granules and Pellets

- Liquid Solutions

By Purity Grade

- Technical Grade

- Pharmaceutical and Cosmetic Grade

- Electronic Grade

By Application

- Water Treatment

- Oil and Gas

- Personal Care and Cosmetics

- Pharmaceuticals

- Pulp and Paper

- Paints and Coatings

By End Use Industry

- Healthcare and Pharmaceuticals

- Consumer Goods

- Industrial Water Management

- Energy

- Agriculture and Aquaculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bronopol Industry

- BASF

- Dow

- Ashland

- LANXESS

- Sharon Laboratories

- Symbolic Pharma

- Shanghai Rich Chemicals

- Fujian Shaowu Yongfei Chemical

- Navin Fluorine International

- Wuhan Fortuna Chemical

- Gayathri Chemicals and Agencies

- Sai Supreme Chemicals

- Mani Agro Chemicals

- BQ Technology

- Sushil Corporation

*- List not Exhaustive