Bulletproof Glass Market Overview: Lightweight Ballistic Glazing, Multi-Hit Survivability & Smart-Glass Integration Driving Global Demand

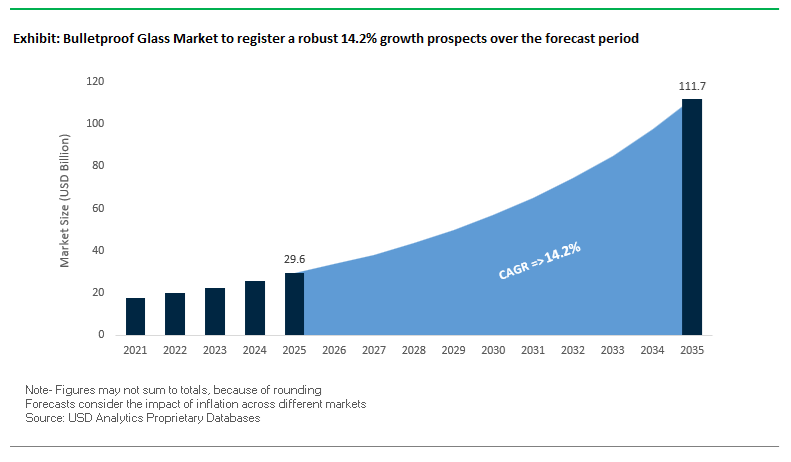

The Transparent Armor (Bulletproof Glass) Market, valued at USD 29.6 billion in 2025 and projected to surge to USD 111.7 billion by 2035 at an exceptional 14.2% CAGR, is entering a high-growth phase shaped by next-generation lightweight materials, rising multi-hit ballistic requirements, and the integration of smart, sensor-ready glazing systems. Modern platforms—from military vehicles and law enforcement fleets to luxury armored SUVs and critical-infrastructure facilities—now require ballistic transparencies that deliver superior protection without compromising visibility, fuel efficiency, or system interoperability. As a result, procurement teams and OEMs are shifting toward Glass-Clad Polycarbonate (GCP) laminates, which offer up to 40% weight reduction compared with legacy all-glass configurations at the same STANAG 4569 Level 3 rating, unlocking major benefits in vehicle performance, payload flexibility, and EV range optimization.

Beyond ballistic stopping power, the market is being redefined by functional integration requirements. Transparent armor must now incorporate 5G and GNSS-transparent antenna films, electrochromic tinting, defogging and de-icing elements, and sensor-ready conductive layers, enabling both defense and commercial vehicles to support advanced situational awareness and connectivity. Decision-makers must also evaluate multi-hit survivability, optical distortion limits, laminate thickness, spall control, and compliance with standards such as U.S. Army ATPD 2352, NATO STANAG 4569, and civilian A12/CEN B7+ certifications. As global security environments evolve, the transparent armor market is rapidly transitioning from conventional ballistic glass to lightweight, multi-functional protective glazing systems, setting new benchmarks for survivability and system integration through 2035.

Market Analysis: Material Innovations, Smart-Glass Integration & Geopolitical Contracting

The transparent armor market accelerated in 2025 with clustered advances in polymer backers, composite backings and smart integrations. In October 2025, Saint-Gobain Sekurit publicly demonstrated a transparent film-type antenna developed with LG Electronics, signaling that armored vehicle glazing is now a platform for 5G/GNSS connectivity-an important differentiator for executive and security fleets that require constant, resilient comms. That same month Avient (Dyneema®) launched HB330/HB332 UD materials; while targeted primarily at opaque armor, those ultra-high-performance UHMWPE backers influence GCP composite designs and help drive the 40% lightweighting gains observed in modern bulletproof glass systems.

Defense and vehicle upgrades further underpinned demand: in September 2025 the U.S. Army’s Bradley A4 modernization contract (BAE Systems, contract modification) required advanced transparent armor and survivability kits, reinforcing military procurement as a steady growth pillar. Earlier in March 2025, a major European government report introduced ballistic-façade code recommendations for climate-resilient buildings, creating a sustained architectural glazing market for certified ballistic glass. Simultaneously, February 2025 announcements from luxury automakers confirming optional multi-hit ballistic glazing for flagship EVs show the consumer premium segment is adopting transparent armor as part of security packages.

Material science and nanotechnology activity in mid-2025 (August) indicated promising routes to thinner, scratch-resistant and stronger bulletproof glass via specialized coatings and nanocomposite interlayers; these advances aim to reduce thickness while retaining optical clarity and multi-hit resilience. Complementing polymer and nano work, aerospace-grade aliphatic urethane adhesive interlayers (used by PPG Aerospace and others) have migrated into transparent armor, improving service life across temperature and humidity extremes-a decisive advantage for military and marine glazing.

Key Trends Transforming Transparent Armor Adoption

Trend 1: Security Mandates Accelerate the Shift from Laminated Glass to Polycarbonate–Ceramic Ballistic Glazing in Critical Infrastructure

Governments and private institutions are increasingly codifying ballistic protection requirements, making high-performance transparent armor a mandatory infrastructure feature rather than an optional upgrade. In the U.S., agencies operating under Interagency Security Committee (ISC) guidelines must deploy glazing that meets minimum ballistic classifications—often UL 752 Level 3 or higher—in public-facing federal buildings. These standards respond to a heightened risk environment, requiring glazing capable of resisting handgun and rifle threats without catastrophic failure.

Insurance carriers have become a parallel regulatory force. Many major insurers now condition full coverage for bank branches, luxury retail, and high-risk commercial spaces on the installation of advanced multi-layer ballistic glazing with high-retention interlayers. These insurance-driven mandates have created a measurable shift away from basic laminated glass toward composite systems combining hard ceramics, chemically strengthened glass, and polycarbonate spall liners.

Across Europe, anti-terrorism initiatives are accelerating this transition further. Updated standards governing transport hubs and government buildings now require transparent armor capable of resisting fragmentation-grenade (FRAG) hazards, automatic-rifle fire, and blast overpressure—placing explicit performance expectations on glazing systems previously focused only on shatter resistance. As a result, the market is moving decisively toward high-rigidity composite systems that deliver multi-hit protection with predictable failure mechanics and superior occupant survivability.

Trend 2: Lightweight Ballistic Glazing Becomes a Core Design Requirement for Electric Vehicles and VIP Armored Platforms

The rapid electrification of luxury mobility and the expanding global demand for VIP armored vehicles are pushing transparent armor manufacturers to develop lightweight, thinner ballistic glass that meets stringent rifle-level protection without compromising vehicle efficiency. In electric vehicles (EVs), heavy traditional bullet-resistant glass can reduce driving range significantly due to increased mass. OEMs across luxury EV and armored EV segments now specify ballistic glazing systems that deliver 30%–40% weight reduction relative to legacy all-glass solutions.

Polycarbonate–ceramic laminates are emerging as a dominant architecture. These systems achieve BR6 performance (resistance to 7.62 mm rifle fire) at thicknesses of just 50–60 mm, compared to older laminated constructions that required substantially more thickness and mass. The resulting performance-to-weight advantage is driving rapid adoption in VIP transport and armored SUVs designed for discrete executive protection.

Breakthroughs in polyurethane and PVB interlayers are equally influential. New generations of high-energy-absorption PVB formulations deliver up to 15% more kinetic energy dissipation than standard interlayers, enabling manufacturers to reduce the number of glass plies while maintaining identical ballistic classifications. This innovation directly correlates with thinner, lighter, and optically superior glazing—critical attributes for premium automotive OEMs and EV platforms constrained by stringent energy-efficiency and design requirements.

High-Value Opportunities Driving Next-Generation Bulletproof Glass Innovation

Opportunity 1: Transparent Armor for UAV and Robotic Sensor Protection in Defense and Law Enforcement

The rapid proliferation of UAVs, UGVs, and autonomous robotic platforms in reconnaissance, perimeter security, and EOD operations is creating a specialized but fast-growing market for lightweight transparent armor designed for sensor survivability. Military and law-enforcement agencies are increasingly specifying protective glazing for optical payloads—cameras, thermal imagers, and LIDAR sensors—that must remain operational under small-arms fire and fragmentation threats.

To meet these requirements, manufacturers are developing high-hardness materials such as synthetic sapphire (Mohs 9) and ALON (Mohs 8) for small-format windows and domes. These materials provide exceptional abrasion, sand erosion, and impact resistance while maintaining precise optical clarity—an essential characteristic to avoid beam deviation exceeding 0.5 milliradians, which can disrupt targeting, mapping, or navigation systems.

In ground robotics, transparent armor must also resist fragmentation from near-field explosive events, tested under standards such as MIL-STD-662F. This creates demand for laminated composites engineered specifically for blast-fragment retention at minimal thickness. As autonomous defense robotics expand globally, this segment presents a sustained, technology-driven growth opportunity for ballistic glazing suppliers specializing in low-mass, high-optical-performance solutions.

Opportunity 2: Smart Transparent Armor with Integrated Heating, HUD Compatibility, and Electrochromic Privacy Control

Transparent armor is transitioning from a passive ballistic barrier to a multifunctional system capable of enhancing vehicle operability, pilot situational awareness, and occupant privacy. This shift opens premium market opportunities in armored aviation, luxury security vehicles, and military cockpits.

One of the fastest-growing features is integrated transparent heating films, typically using Indium Tin Oxide (ITO). These conductive coatings allow uniform low-voltage surface heating for rapid de-icing and anti-fogging—mission-critical capabilities for aircraft and armored vehicles operating in cold or humid environments.

Simultaneously, high-end platforms are demanding ballistic glazing that supports Head-Up Display (HUD) projection. This requires precision lamination to eliminate ghosting and ensure the inner surface meets strict optical flatness while still resisting ballistic threats.

Electrochromic (EC) and liquid crystal layers represent the next frontier. These systems allow ballistic glass to shift from ~80% visible transparency to full opacity within seconds, offering glare control, interior privacy, and tactical concealment. For VIP transport and specialized military platforms, EC-equipped ballistic glazing provides both enhanced survivability and enhanced comfort—making it a high-margin, strategically important opportunity for transparent armor manufacturers.

Bulletproof Glass Market Share Analysis

Market Share by Material Type: Glass-Clad Polycarbonate (GCP) Leads with 51.2% Share

Glass-Clad Polycarbonate (GCP) dominates the Bulletproof Glass Market with a commanding 51.2% share in 2025, underscoring its position as the industry’s most commercially scalable and performance-balanced solution for ballistic protection. GCP’s leadership is driven by its unique combination of multi-hit resistance, reduced weight, high flexural strength, and cost-effectiveness, making it the preferred choice for commercial armored vehicles, government buildings, retail storefronts, embassies, and security-sensitive infrastructures. Unlike traditional laminated glass, GCP offers superior impact dissipation and spall control, enabling it to withstand high-velocity rifle rounds while maintaining manageable system thickness for easier installation and retrofitting. This strong market share also reflects global demand trends: rising urban security requirements, expanding adoption of armored SUVs, and heightened risk preparedness in commercial and public buildings. Surrounding material categories reinforce how the market is stratified by performance and cost needs—traditional laminated glass (glass/PVB) remains essential for handgun-level protection and high optical clarity; acrylic and monolithic polymers serve lightweight, cost-sensitive installations; and advanced composites and ceramic solutions (ALON, sapphire, GPU) are reserved for mission-critical defense, aerospace, and VIP transport applications where maximum protection at minimal weight is non-negotiable. The segmentation highlights GCP’s strategic role as the workhorse of the global ballistic glazing industry.

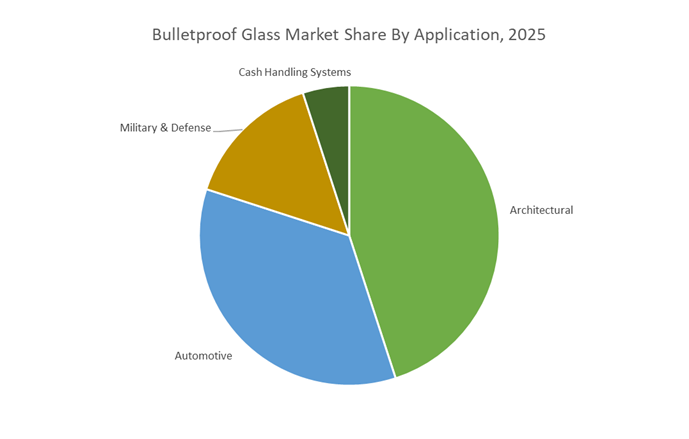

Market Share by Application/End-Use: Architectural Sector Leads with 45.9% Share

Architectural applications account for the largest share at 45.9% in 2025, reflecting the rising prioritization of ballistic-resistant building envelopes across commercial, governmental, and high-risk environments. This dominance stems from increased global investment in physical security infrastructure, where ballistic glazing is integrated into facades, entry points, security lobbies, guard stations, and critical-operation centers to mitigate threats ranging from armed attacks to forced entry. The segment benefits from strong construction activity in emerging economies, retrofitting of high-value assets in developed regions, and stricter safety standards adopted by corporations, financial institutions, and public-sector agencies. Architectural installations also require extensive customization—balancing optical clarity, building aesthetics, threat level requirements, and integration with blast and forced-entry standards—making ballistic glazing an essential component of modern security architecture. Beyond buildings, the broader application landscape reflects diversified market pull: armored automotive applications drive technological integration in lightweight multi-layer glass systems that influence vehicle performance and fuel efficiency; military and defense users advance R&D toward ultra-light ceramic-reinforced transparent armor; and cash-handling systems maintain stable demand due to stringent banking and retail security protocols. Collectively, the end-use segmentation illustrates how architectural adoption forms the volume backbone of the market, while automotive and defense applications push the innovation frontier.

Country Analysis: Global Bulletproof Glass Market Innovation Hubs

United States: Lightweight Transparent Armor Production Accelerated by Defense Modernization and Domestic Sourcing Shifts

The United States continues to dominate the bulletproof glass and transparent armor market, driven by the scale of Army fleet modernization and stringent protective requirements for military and homeland security missions. The U.S. Army’s $356.6 million AMPV contract modification (March 2025) reinforces long-term demand for high-performance transparent armor that meets MIL-SPEC ballistic resistance while achieving aggressive weight-reduction targets. These modernization programs require suppliers to advance laminated glass/ceramic hybrids, acrylic-polycarbonate composites, and anti-spall interlayer technologies that enhance visibility and survivability in armored vehicles.

Trade policy developments are reshaping sourcing strategies. The July 2025 U.S. antidumping ruling, which proposed duties up to 311% on float glass imports from China and Malaysia, is accelerating a shift toward domestic and allied supply chains for base glass used in ballistic laminates. This shift boosts U.S. investments in specialty float glass, low-iron substrates, and laminated ballistic glazing lines. Meanwhile, architectural security demand is tightening due to rising adoption of UL 752 and ASTM forced-entry dual-certification, requiring glazing systems that protect against both ballistic threats and physical intrusion. U.S. manufacturers are responding with multi-layered transparent armor solutions that integrate polyurethane or PVB interlayers for zero-spall performance, making the U.S. a global leader in integrated protective glazing.

European Union: EN 1063-Driven Multi-Functional Ballistic Glazing and Security-Retrofit Growth

The European Union’s bulletproof glass market is defined by rigorous certification requirements (EN 1063) and the rapid evolution of multi-functional transparent armor solutions. At Glass Performance Days (GPD) 2025, European engineers emphasized a shift toward glazing that achieves high ballistic resistance, solar control, thermal insulation, and acoustic damping within a single laminated structure. This trend is driving EU suppliers to develop hybrid interlayer stacks, high-strength glass-ceramic laminates, and energy-efficient ballistic façades for commercial and government applications.

European defense contractors such as Rheinmetall AG continue integrating advanced transparent armor into land systems, strictly aligning designs with STANAG ballistic protection levels. On the civilian side, regulatory pressure is driving strong demand for ballistic glazing retrofits in banks, embassies, airports, and critical infrastructure. These applications often require custom sizing, variable curvature, or oversized laminated panels, reinforcing the region’s specialization in precision-engineered ballistic glass fabrication.

Corporate realignment is strengthening the specialty glazing ecosystem. Saint-Gobain’s 2025 “Lead & Grow” strategy focuses on high-value specialty glass—including security glazing—bolstering European leadership in architectural ballistic solutions, laminated façades, and police/military protective window systems. The EU remains a global pioneer in multi-functional, energy-efficient armored glazing.

China: High-End Manufacturing and Infrastructure Security Catalyzing Domestic Ballistic Glass Demand

China is rapidly scaling its capacity for advanced ballistic glass manufacturing, supported by national smart manufacturing initiatives and a growing emphasis on securing critical infrastructure. At the China Glass 2025 Exhibition, producers showcased deep integration of AI-driven production lines, IoT-enabled glass furnaces, and intelligent defect detection, improving consistency in float glass quality—a foundational requirement for ballistic laminate production. This technological capability positions China as a leading producer of high-end glass substrates, alumina-reinforced glass, and optical-strengthened specialty glass used in transparent armor.

Government programs are heavily expanding demand for secure glazing. Investments in banking facilities, government compounds, transport hubs, and high-security buildings are driving large-scale adoption of bulletproof and forced-entry-resistant windows. At the same time, Chinese material science labs are developing high-alumina second-generation glasses and anti-halo photoelectric materials, enhancing the underlying strength of ballistic laminates while enabling thinner, lighter protective solutions. Despite these advancements, Chinese exports face heightened global trade barriers, pushing manufacturers to concentrate more heavily on high-security domestic markets and regionally aligned supply chains.

Japan: Precision Glass Engineering and Automotive-Integrated Transparent Armor Innovation

Japan remains a global leader in precision glass fabrication, laminated composites, and high-performance coatings, which are increasingly leveraged in the development of advanced bulletproof glass systems. AGC Inc., a dominant force in global glass technologies, continues to refine glass-resin lamination, composite bonding, and surface engineering techniques essential for producing lightweight transparent armor with excellent optical clarity. These innovations enable Japanese manufacturers to produce thin, high-strength ballistic laminates capable of meeting strict resistance requirements while maintaining superior visibility.

Japan’s automotive sector is also shaping new integration paths for security glazing. Technologies such as p-polarized reflection coatings, in-mold forming, and advanced windshield composites position AGC and other suppliers to incorporate active and passive security functions directly into vehicle glazing—especially for VIP transport, defense vehicles, and luxury brands seeking ballistic-rated options. Japan’s continued emphasis on manufacturing precision, optical integrity, and material innovation secures its role as a strategic hub for next-generation transparent armor systems.

Competitive Landscape: Aerospace-Grade Interlayers, GCP Lightweighting & Integrated Connectivity Leaders

The competitive field for bulletproof glass is populated by traditional flat-glass giants, specialty interlayer suppliers, high-performance laminated glazing manufacturers and vehicle armor integrators. Differentiation hinges on adhesive/interlayer chemistry, composite backing materials (UHMWPE/Dyneema, aramid backers, PC), smart-film integration capability, certification experience (ATPD 2352, STANAG 4569, AEP-55) and the ability to deliver multi-hit validated products at scale.

PPG Industries, Inc. - Aerospace-grade transparencies and high-performance adhesive interlayers for certified transparent armor

PPG leverages decades of aerospace transparency development to supply Securitect® Transparent Armor for military, marine and architectural applications. Its proprietary aliphatic urethane adhesive interlayers-rooted in aerospace R&D-deliver superior optical clarity, environmental durability and service life in extreme climates. PPG’s product suite is certified to STANAG 4569 and ATPD 2352, positioning it as a go-to supplier when rigorous defense specifications and long-term optical performance are required.

Saint-Gobain (Sekurit) - Automotive glazing leader integrating transparent antennas and functional films into ballistic glass

Saint-Gobain Sekurit combines world-class laminated glass know-how with electronics partnerships (e.g., with LG) to embed transparent film-type antennas and other smart functionalities into vehicle glazing. This capability is critical for armored luxury and executive transport that require 5G/GNSS connectivity without degrading ballistic protection. Saint-Gobain’s strength lies in marrying certified ballistic laminates (EuroNorm/EN and STANAG-level capabilities) with advanced functional films for modern vehicle ecosystems.

AGC Inc. - Flat glass and composite glazing specialist scaling armored windshields and architectural laminated solutions

AGC applies flat-glass manufacturing scale and composite lamination techniques (including resin and PC backer systems) to produce Lamisafe and other high-security glazing products. Its acquisition of NordGlass expanded windshield and specialized glazing capacity, enabling AGC to address automotive armored glazing and architectural ballistic panels with high throughput and consistent quality-important for OEM and retrofit markets.

Armormax - Lightweight armored conversions and region-focused vehicle protection services

Armormax specializes in discreet, lightweight armored vehicle conversions using proprietary synthetic fibers and composite systems that preserve OEM aesthetics and performance. The company’s November 2025 expansion into Senegal targets rising regional demand for VIP and governmental protective mobility. Armormax’s portfolio emphasizes minimal weight penalty, preserving vehicle dynamics-an attractive proposition for luxury and diplomatic vehicle fleets.

Eastman Chemical Company - Interlayer technology and high-performance PVB/ionomer formulations for multi-hit lamination

Eastman supplies critical interlayers (PVB, ionomers like Saflex and Trosifol) used to bond glass and polycarbonate layers into certified ballistic laminates. Its R&D focuses on multi-hit capability and blast resistance enhancements, improving fragment retention and post-impact integrity. Eastman’s materials are central to achieving STANAG and ATPD certifications and are widely used across architectural, vehicular and marine transparent armor programs.

Bulletproof Glass Market Report Scope

Bulletproof Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.6 Billion

|

|

Market Size (2035)

|

$111.7 Billion

|

|

Market Growth Rate

|

14.2%

|

|

Segments

|

By Material Type (Glass-Clad Polycarbonate, Traditional Laminated Glass, Acrylic/Solid Polymer, Glass-Clad Polyurethane, Ceramic Transparent Armor), By Protection Level (UL 752, EN 1063, VPAM, STANAG 4569), By Application/End-Use (Automotive, Architectural, Military & Defense, Cash Handling Systems), By Security Feature (Spall-Free Glazing, Multi-Hit Performance Glazing, Forced-Entry/Burglary-Resistant Glazing, Switchable/Smart Glazing, Lightweight Armor)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AGC Inc., Saint-Gobain S.A., PPG Industries Inc., AGP Group, Ravenscroft G.A.P. Security Inc., I.A.R. Incorporated, Isoclima S.p.A., Taiwan Glass Industry Corporation, DuPont de Nemours Inc., Eastman Chemical Company, Total Security Solutions LLC, Apogee Enterprises Inc., Guardian Glass, Plasan Sasa Ltd., Hofstetter G.A.P. Security

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bulletproof Glass Market Segmentation

By Material Type

- Glass-Clad Polycarbonate (GCP)

- Traditional Laminated Glass

- Acrylic / Solid Polymer

- Glass-Clad Polyurethane (GPU)

- Ceramic Transparent Armor

By Protection Level

- UL 752 Levels 1–3 (Handgun Protection)

- UL 752 Levels 4–8 (Rifle Threat Protection)

- EN 1063 BR Ratings (BR1 to BR7)

- VPAM VR Ratings (Vehicle Ballistic Protection)

- STANAG 4569 (Military Vehicle Protection)

By Application / End-Use

- Automotive

- Architectural

- Military & Defense

- Cash Handling Systems

By Security Feature

- Spall-Free Glazing

- Multi-Hit Performance Glazing

- Forced-Entry / Burglary-Resistant Glazing

- Switchable / Smart Glazing

- Lighter-Weight Armor

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Bulletproof Glass Market

- AGC Inc.

- Saint-Gobain S.A.

- PPG Industries, Inc.

- AGP Group

- Ravenscroft G.A.P. Security Inc.

- I.A.R. Incorporated

- Isoclima S.p.A.

- Taiwan Glass Industry Corporation

- DuPont de Nemours, Inc.

- Eastman Chemical Company

- Total Security Solutions, LLC

- Apogee Enterprises, Inc.

- Guardian Glass

- Plasan Sasa Ltd.

- Hofstetter G.A.P. Security

*- List not Exhaustive