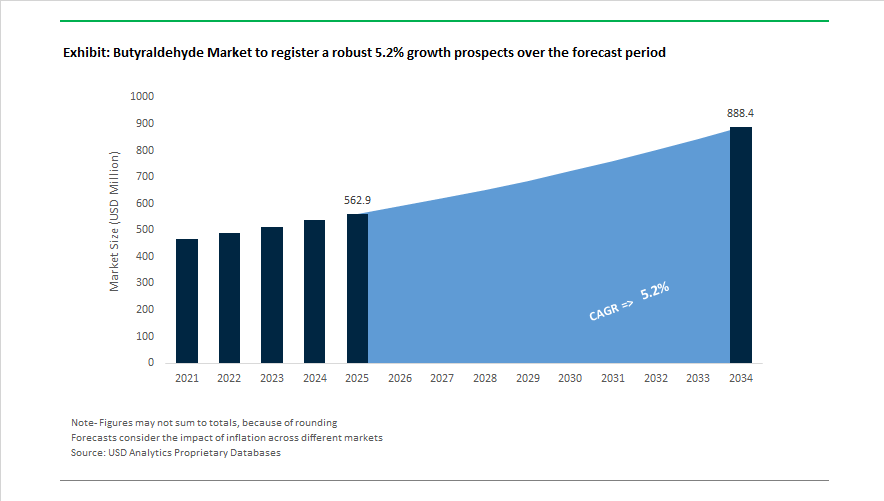

The butyraldehyde market is forecast to expand from USD 562.9 Million in 2025 to USD 888.3 Million by 2034, reflecting a CAGR of 5.2% driven by rising consumption of oxo-alcohols, plasticizer intermediates, coatings resins, and specialty chemical building blocks. Market stability improved in March 2024 when OQ Chemicals declared force majeure at its German operations due to feedstock disruption, then restored full production by May 2024 after process optimization. Financial restructuring followed in September 2024 when the company extended its debt maturity to December 2026, ensuring operational continuity across its global aldehyde network. Consolidation accelerated in October 2024 as Perstorp Group acquired OQ Chemicals Nederland, strengthening upstream oxo-chemicals integration in Northern Europe.

Capacity expansion and vertical integration defined regional growth trajectories during 2024 and 2025. In May 2024, DuPont completed a USD 300 million expansion that increased US butyraldehyde output by 50% to serve pharmaceutical and agrochemical intermediates. January 2024 collaboration between LG Chem and SABIC focused on optimizing hydroformylation routes in Asia to supply plasticizers and synthetic resins. In March 2024, INEOS Styrolution acquired a German production site to vertically integrate supply of butyraldehyde derivatives for specialty resins. Project Propel at OQ Chemicals Bay City site in 2024 further enhanced domestic aldehyde integration in North America.

Market dynamics in 2025 and 2026 are shaped by pricing shifts, sustainability, and regulatory transitions. October 2025 marked the inauguration of a BASF production line in Türkiye utilizing butyraldehyde derivatives for low-VOC dispersions powered by renewable electricity. Between 2025 and 2026, BASF advanced construction at its Zhanjiang Verbund site in China, adding C4 oxo alcohol capacity. January 2026 price adjustments by Eastman Chemical Company reflected cost pressure across the oxo value chain, while its 2025 to 2026 structural cost reductions aim to maintain competitiveness. China’s 2026 restriction on conventional phthalates is accelerating demand for 2-ethylhexanol derived from butyraldehyde, reshaping plasticizer chemistry.

The Butyraldehyde market is experiencing a structural reset driven by production instability and high-cost pressures in Europe. In May 2024, OQ Chemicals lifted a force majeure on n-Butyraldehyde and Isobutyraldehyde from its Oberhausen and Marl sites after a February 2024 disruption caused by a synthesis gas plant failure. This event exposed the fragility of Europe’s integrated oxo-alcohol value chain, signaling long-term vulnerability in hydroformylation capacity. By late 2025, EU chemical production remained materially below long-term baselines, compelling downstream buyers to diversify sourcing. Propylene feedstock economics remain a critical handicap: natural gas prices in Europe were still nearly triple those in the United States as of mid-2025, eroding competitiveness in energy-intensive oxo processes and accelerating reliance on Asian and U.S. imports. The decline in trade surplus and loss of regional hydroformylation self-sufficiency have reshaped procurement behavior, making supply-chain risk mapping and contract diversification a core task for large chemical buyers.

Sustainability mandates in fragrances, coatings, and specialty chemicals are driving interest in renewable butyraldehyde. New enzymatic routes are being commercialized that convert sugars and cellulose directly into n-butyraldehyde using engineered microorganisms. Easel Biotechnologies, supported by patents valid through 2032, has advanced gas-stripping fermentation systems that deliver commercially relevant yield increases and enable a lower-carbon footprint compared to fossil-based oxo synthesis. Fragrance manufacturers, including leaders like Firmenich, have signaled heightened demand for bio-derived aldehydes to support “natural” product positioning and premium pricing. This trend is catalyzing investments in biocatalysis partnerships and tech-transfer pipelines that allow chemical suppliers to reposition butyraldehyde within ESG-compliant raw material portfolios.

Automotive interior quality standards are pushing demand for Low-VOC dashboards, headliners, and upholstery. n-Butyraldehyde is the essential precursor for 2-Ethylhexanol (2-EH), which is required to manufacture key plasticizers such as DINP and DIDP used in interior polymer systems. China, reporting a 39.6% year-over-year surge in February 2025 vehicle production, is magnifying global 2-EH demand. Major producers such as BASF and LG Chem are optimizing aldol condensation and hydrogenation units to maximize conversion efficiency and secure high-purity feedstock streams. This conversion optimization supports automotive OEMs targeting lower odor emissions, anti-fogging cabin coatings, and passenger-wellness aligned product claims.

The Butyraldehyde market is indirectly tied to the global EV boom because it sits upstream of gamma-butyrolactone (GBL) and N-Methyl-2-Pyrrolidone (NMP), both mission-critical solvents in battery electrode coating. NMP, synthesized via butyraldehyde-derived GBL, accounts for the vast majority of solvent use in cathode-active material coating processes. With more than 14 million electric vehicles sold globally in 2024-2025 and Asia-Pacific alone delivering over 8 million units, electronic-grade NMP (purity ≥ 99.9 percent) continues to face constraint. The battery industry is simultaneously advancing closed-loop solvent recovery infrastructure, forming a multi-billion-dollar in-house purification market that reduces solvent loss and aligns manufacturers with tightening VOC-emission regulations in Europe and North America. This circularity model reinforces long-term butyraldehyde relevance in energy-transition supply chains, even as regional feedstock substitution and bio-routes diversify production pathways.

n-Butyraldehyde accounts for 72% of global butyraldehyde consumption in 2025, reinforcing its position as the primary oxo intermediate produced via propylene hydroformylation. It serves as the backbone for n-butanol, 2-ethylhexanol, and n-butyric acid, which are further converted into acrylates, acetate esters, amino resins, and major plasticizers such as DOP and DOTP. These derivatives underpin coatings, PVC formulations, adhesives, and solvents, tightly linking n-butyraldehyde demand to automotive production, construction coatings, and consumer goods manufacturing. Isobutyraldehyde represents a smaller but strategically important share, feeding isobutanol, neopentyl glycol, and isobutyric acid value chains. Neopentyl glycol supports polyester resins and synthetic lubricants, while isobutanol supplies alkyd coatings and specialty solvents. This segment remains stable, driven by specialty chemical applications requiring higher functionality and performance consistency.

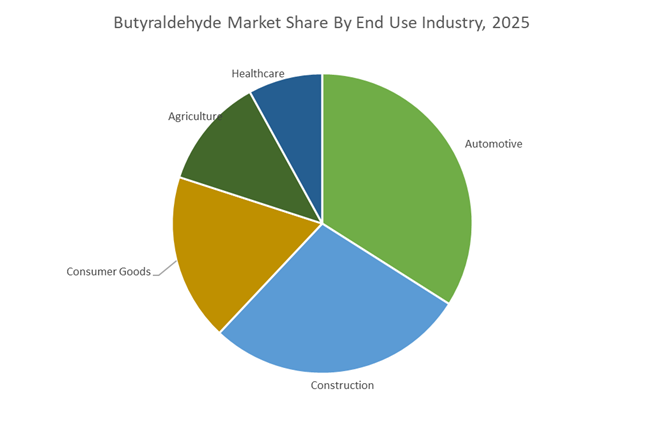

Automotive represents 34% of butyraldehyde-derived demand in 2025, driven by 2-ethylhexanol-based PVC plasticizers and n-butanol coatings used in interior trim, wire harnesses, refinish paints, and underbody protection. EV adoption and lightweighting trends are sustaining consumption of high-performance plastics and coatings. Construction forms the second-largest segment, utilizing n-butanol and 2-ethylhexanol in architectural paints, sealants, and wood adhesives, alongside butyraldehyde-based amino resins for laminates and panels, with infrastructure spending acting as a primary growth lever. Consumer goods absorb significant volumes through packaging plastics, synthetic leather, footwear, and household cleaners, while cosmetics rely on n-butyl acetate as a key solvent. Agriculture remains a specialized outlet for herbicide synthesis and feed preservatives, and healthcare represents a smaller, high-purity segment supplying API intermediates and vitamin precursors.

The global Butyraldehyde market in 2026 is defined by strong demand from 2-ethylhexanol (2-EH), polyvinyl butyral (PVB), plasticizers, specialty resins, and agrochemical intermediates, alongside increasing emphasis on mass-balance sustainability, bio-based oxo alcohols, and low-VOC derivatives. Competitive dynamics are shaped by oxo-process efficiency, n-to-iso selectivity ratios, backward integration into propylene, and geographic production flexibility. Leading producers leverage proprietary hydroformylation technologies, AI-enabled yield optimization, and circular feedstock integration to enhance carbon efficiency while serving high-growth sectors such as EV glazing, renewable infrastructure coatings, and advanced polymer systems.

BASF remains the global leader in the oxo-alcohol value chain, managing the entire pathway from propylene to butyraldehyde and downstream alcohol derivatives. In 2026, its Mass-Balance Sustainability strategy under Ccycled® prioritizes replacing fossil feedstocks with pyrolysis oil and renewable inputs in butyraldehyde production. High-capacity oxo plants in Ludwigshafen, Freeport, and Nanjing allow BASF to shift volumes to offset logistics bottlenecks and energy volatility. A key supplier for PVB resins used in EV safety glass and architectural glazing, BASF leverages AI to optimize n-butyraldehyde yields over isobutyraldehyde, aligning production with surging global 2-EH demand.

Dow enters 2026 focused on MobilityScience™, targeting automotive lightweighting and infrastructure electrification. Through its Transform to Outperform initiative, the company is deploying AI and automation across oxo-intermediate operations to enhance productivity and simplify delivery systems. Dow produces high-purity n- and iso-butyraldehyde using proprietary LP Oxo™ technology, delivering high efficiency and lower carbon intensity. Butyraldehyde derivatives feed EVOAIR™ polyolefin elastomers that replace traditional interior materials in vehicles. At K 2025, Dow showcased REVOLOOP™ recycled plastics resins integrating oxo-derived plasticizers into post-consumer cable jackets, reinforcing its position in circular economy applications.

Oxea has repositioned itself as a focused Oxo Performance specialist following its 2025 rebrand and recapitalization. The Propel project at Bay City expanded high-purity propionaldehyde and butyraldehyde capacity, supporting US coatings and construction markets. As a leader in C3 to C9 synthetic fatty acids, Oxea leverages its intermediate platform to produce butyraldehyde-based acids for high-performance lubricants. In 2026, improved financial leverage with a reduced debt-to-EBITDA ratio enables reinvestment into low-VOC derivatives aligned with European Green Deal compliance. Oxea’s strategy emphasizes operational excellence and specialty innovation over commodity exposure.

Eastman maintains a competitive advantage through its BISBI rhodium-catalyzed hydroformylation technology, achieving an industry-leading n-to-iso ratio above 25:1 and over 96% n-butyraldehyde selectivity. As a global oxo technology licensor, Eastman influences new capacity additions worldwide. In early 2026, the company implemented price adjustments for N-propyl and N-butyl alcohols to manage raw material volatility. Its Chemical Intermediates segment produces more than 25 oxo-derived derivatives, including plasticizers supporting electronics designed for disassembly-on-demand recycling. The debut of Naia™ Lyte further demonstrates Eastman’s integration of sustainable fiber solutions with advanced aldehyde chemistry platforms.

Now integrated within PETRONAS Chemicals Group, Perstorp has built a global East-West supply chain linking Swedish manufacturing with Malaysian feedstocks. By 2026, its ISCC PLUS-certified synthetic esters and polyols lead in traceable mass-balance transparency, allowing customers to quantify renewable content in specialty resins. The Infinite Loop initiative advances circular butyraldehyde production using recycled CO2 and renewable hydrogen, targeting near-zero carbon coatings. Perstorp dominates specialty resins for renewable energy infrastructure, including wind turbine blade finishes requiring durability, chemical resistance, and long service life under extreme environmental exposure.

Mitsubishi Chemical Group advances its KAITEKI sustainability vision through bio-based butyraldehyde pilot programs, aiming to transition toward bio-propylene feedstocks by 2030. In 2026, the company supplies aldehyde derivatives critical to agrochemical synthesis, supporting next-generation crop protection technologies for constrained arable land. Mitsubishi integrates oxo chemistry with its PMMA and polycarbonate chains, enabling high-performance coatings for smartphone, laptop, and electronics displays. Expansion across ASEAN strengthens its presence in paints, adhesives, and infrastructure applications, positioning Mitsubishi as a regional powerhouse linking specialty polymers with advanced aldehyde intermediates.

China’s butyraldehyde industry is being reshaped by explicit policy direction, integrated infrastructure, and digital manufacturing mandates. In September 2025, the Ministry of Industry and Information Technology released the Work Plan for Stabilizing Growth 2025–2026, targeting average annual petrochemical growth above 5% and prioritizing domestic localization of critical intermediates such as butyraldehyde. This policy has reinforced investments across oxo-alcohol value chains where n-butyraldehyde is essential for brake fluids, plasticizers, and stabilizers.

Infrastructure momentum is centered on large-scale integration. By October 2024, BASF inaugurated the first Central Operations Building at its Zhanjiang Verbund site, enabling coordinated ramp-up of oxo-alcohol lines that rely on n-butyraldehyde as a core precursor. Downstream pull is intensifying as well. Late 2025 saw the commissioning of new HDPE plants with 500,000 metric tons annual capacity, lifting captive consumption of butyraldehyde-derived stabilizers for construction and automotive applications. Specialty additives are another growth vector. The Nanjing Jiangbei New Material Technology Park expanded its advanced additives plant in May 2024 with commissioning slated for late 2025, using butyraldehyde in controlled radical polymerization dispersants. Sustainability and digitalization are now embedded. Formic acid from the Nanjing Verbund achieved a validated “Lower than Market” cradle-to-gate footprint through May 2026, setting a benchmark across the aldehyde chain, while the Work Plan mandates AI-driven process optimization to reduce waste and energy intensity in aldehyde production.

Germany’s butyraldehyde landscape is defined by corporate restructuring, downstream integration, and energy efficiency. On May 19, 2025, OQ Chemicals officially rebranded to Oxea following its acquisition by Strategic Value Partners, signaling a renewed focus on innovation and asset optimization in oxo-chemicals. This strategic reset has reinforced the role of German sites as anchors for high-value aldehyde derivatives.

Downstream investments are securing long-term feedstock demand. In March 2025, Oxea announced a major heptanoic acid production investment at its world-scale Oberhausen facility, locking in sustained consumption of butyraldehyde streams. Supply stability improved after early-2024 disruptions, with full operations resuming in May 2024 and restoring European availability of isobutyraldehyde for neopentyl glycol production. Sustainability measures are increasingly material. Through a partnership with Energieversorgung Oberhausen, industrial waste heat recycling was implemented across 2024–2025, materially reducing the energy intensity of butyraldehyde production. Product portfolios are also shifting toward bio-balanced offerings, highlighted by the July 2024 launch of OxBalance Neopentyl Glycol Diheptanoate for cosmetics, produced using biomass-balanced isobutyraldehyde to align with European Green Deal preferences.

The United States butyraldehyde industry is anchored in large-scale Gulf Coast assets and infrastructure-led efficiency. In April 2024, Project “Propel” reached mechanical completion at Bay City, Texas, enabling infrastructure for a world-scale methyl methacrylate plant that leverages butyraldehyde intermediates for high-performance automotive coatings. This milestone underscored the strategic importance of aldehyde availability for downstream acrylics and coatings.

Capacity and quality upgrades continued through 2025. Oxea’s Bay City site expanded supply of high-purity aldehydes to serve rising demand from pharmaceutical and fragrance manufacturers that require tight impurity control. Sustainability credentials are now a competitive differentiator. The site achieved ISCC PLUS certification in June 2024, enabling production of circular and bio-circular butyraldehyde derivatives for North American customers. Logistics efficiency has also improved. In 2025, federal funding under the Infrastructure for Rebuilding America program targeted chemical transport corridors, easing movement across butyraldehyde-intensive regions along the Gulf Coast and reducing delivery risk for downstream users.

India’s butyraldehyde market reflects a transition from import reliance toward value chain ambition. A July 2025 strategy by NITI Aayog set a clear objective to raise India’s share of the global chemicals value chain to 5–6% by 2030, explicitly incentivizing oxo-aldehydes to achieve net-zero importer status. This policy signal is reshaping investment priorities across aldehyde and derivative manufacturing.

Demand dynamics remain robust. Between 2023 and 2024, butyraldehyde import shipments rose 13.53% by volume, driven by rapid expansion in specialty chemicals, resins, and pharmaceuticals. Gujarat has emerged as a focal point, where increased production of Grignard reagents and pharmaceutical intermediates has lifted localized demand for n-butyraldehyde, as noted in 2025 industry updates. Sustainability-linked investment is gaining traction as well. Major producers reported strong early fiscal 2025–2026 performance in Industrial Solutions, supported by steady consumption of butyraldehyde-derived stabilizers for the domestic rubber sector and aligned with broader green transformation initiatives.

|

Country / Region |

Primary Growth Lever |

Strategic Direction |

|---|---|---|

|

China |

Policy-led localization, integrated Verbund sites |

AI-driven optimization, sustainability validation, captive downstream use |

|

Germany |

Oxea-led restructuring, downstream acids |

Bio-balanced products, energy-efficient production |

|

United States |

Gulf Coast scale, certified circularity |

High-purity capacity, logistics efficiency |

|

India |

Value chain upgrading, pharma demand |

Import substitution, oxo-aldehyde incentives |

|

Parameter |

Details |

|

Market Size (2025) |

$562.9 Million |

|

Market Size (2034) |

$888.3 Million |

|

Market Growth Rate |

5.2% |

|

Segments |

By Product Type (n-Butyraldehyde, Isobutyraldehyde), By Manufacturing Process (Oxo Process, Acetaldehyde Dehydrogenation), By Application (Chemical Intermediates, Resins and Plasticizers, Solvents and Additives, Specialty Chemicals), By End Use Industry (Automotive, Construction, Agriculture, Healthcare, Consumer Goods) |

|

Study Period |

2019- 2025 and 2026-2034 |

|

Units |

Revenue (USD) |

|

Qualitative Analysis |

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking |

|

Companies |

Oxea, BASF SE, Eastman Chemical Company, Dow, Mitsubishi Chemical Group, Perstorp, Sinopec, Wanhua Chemical Group, INEOS Group, Formosa Plastics Corporation, Petronas Chemicals Group, Grupa Azoty, Elekeiroz, Navin Fluorine International, Beijing Yunbang Biosciences |

|

Countries |

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa |

*- List not Exhaustive

Table of Contents: Butyraldehyde Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Butyraldehyde Market Landscape and Outlook (2025–2034)

2.1. Introduction to Butyraldehyde and Oxo Chemistry

2.2. Market Valuation and Growth Outlook (2025–2034)

2.3. Oxo-Alcohol Integration, Plasticizer Shifts, and Capacity Realignments

2.4. European Capacity Stress and Feedstock Economics

2.5. Bio-Based Aldehydes and Battery Solvent Value Chains

3. Strategic Trends and Opportunities

3.1. Hydroformylation Optimization and n-to-iso Selectivity

3.2. Emergence of Bio-n-Butyraldehyde via Fermentation

3.3. High-Purity 2-Ethylhexanol for Automotive Interiors

3.4. GBL and NMP Demand from Lithium-Ion Battery Manufacturing

3.5. Circular Solvent Recovery and Mass-Balance Feedstocks

4. Competitive Landscape and Strategic Developments

4.1. Oxo Capacity Expansions and Vertical Integration

4.2. European Production Restructuring and Energy Cost Mitigation

4.3. Sustainability Platforms and Bio-Balanced Portfolios

4.4. AI-Enabled Yield Optimization and Process Digitalization

4.5. Strategic Acquisitions and Regional Supply Diversification

5. Market Share and Segmentation Insights: Butyraldehyde Market

5.1. By Product Type

5.1.1. n-Butyraldehyde

5.1.2. Isobutyraldehyde

5.2. By Manufacturing Process

5.2.1. Oxo Process

5.2.2. Acetaldehyde Dehydrogenation

5.3. By Application

5.3.1. Chemical Intermediates

5.3.2. Resins and Plasticizers

5.3.3. Solvents and Additives

5.3.4. Specialty Chemicals

5.4. By End Use Industry

5.4.1. Automotive

5.4.2. Construction

5.4.3. Agriculture

5.4.4. Healthcare

5.4.5. Consumer Goods

6. Country Analysis and Outlook of Butyraldehyde Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. China

6.10. India

6.11. Japan

6.12. South Korea

6.13. Australia

6.14. Brazil

6.15. Argentina

6.16. Middle East

6.17. Africa

7. Butyraldehyde Market Size Outlook by Region (2025–2034)

7.1. North America Butyraldehyde Market Size Outlook

7.1.1. By Product Type

7.1.2. By Manufacturing Process

7.1.3. By Application

7.1.4. By End Use Industry

7.2. Europe Butyraldehyde Market Size Outlook

7.2.1. By Product Type

7.2.2. By Manufacturing Process

7.2.3. By Application

7.2.4. By End Use Industry

7.3. Asia Pacific Butyraldehyde Market Size Outlook

7.3.1. By Product Type

7.3.2. By Manufacturing Process

7.3.3. By Application

7.3.4. By End Use Industry

7.4. South and Central America Butyraldehyde Market Size Outlook

7.4.1. By Product Type

7.4.2. By Manufacturing Process

7.4.3. By Application

7.4.4. By End Use Industry

7.5. Middle East and Africa Butyraldehyde Market Size Outlook

7.5.1. By Product Type

7.5.2. By Manufacturing Process

7.5.3. By Application

7.5.4. By End Use Industry

8. Company Profiles: Leading Players in the Butyraldehyde Market

8.1. Oxea

8.2. BASF SE

8.3. Eastman Chemical Company

8.4. Dow

8.5. Mitsubishi Chemical Group

8.6. Perstorp

8.7. Sinopec

8.8. Wanhua Chemical Group

8.9. INEOS Group

8.10. Formosa Plastics Corporation

8.11. Petronas Chemicals Group

8.12. Grupa Azoty

8.13. Elekeiroz

8.14. Navin Fluorine International

8.15. Beijing Yunbang Biosciences

9. Methodology

9.1. Research Scope

9.2. Primary and Secondary Research Framework

9.3. Market Sizing and Forecast Model

9.4. Assumptions and Limitations

9.5. Validation and Triangulation

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The Butyraldehyde Market is valued at USD 562.9 Million in 2025 and is forecast to reach USD 888.3 Million by 2034, expanding at a CAGR of 5.2%. Growth is anchored in rising consumption of oxo-alcohols, plasticizer intermediates, coatings resins, and battery-grade solvents linked to electric vehicle manufacturing.

n-Butyraldehyde accounts for about 72% of total demand in 2025 because it is the primary precursor for n-butanol, 2-ethylhexanol (2-EH), and butyric acid. These derivatives feed large-volume markets including PVC plasticizers, architectural coatings, adhesives, and automotive interior materials, making n-butyraldehyde the backbone of the oxo-chemicals value chain.

Butyraldehyde sits upstream of gamma-butyrolactone (GBL) and N-Methyl-2-Pyrrolidone (NMP), both critical solvents for lithium-ion cathode coating. As EV production accelerates globally, demand for electronic-grade NMP (≥99.9% purity) continues to rise, reinforcing long-term butyraldehyde relevance in battery materials, even as closed-loop solvent recovery systems expand.

Europe faces ongoing oxo-capacity stress due to energy costs and prior supply disruptions, pushing buyers toward US and Asian sourcing. China is localizing integrated oxo-alcohol production under industrial policy frameworks, while India is moving from import dependence toward value-chain upgrading for pharmaceuticals and specialty chemicals. Parallel to this, bio-based n-butyraldehyde via enzymatic fermentation is emerging for fragrance and specialty applications, supporting ESG-driven procurement.

Key producers shaping capacity, integration, and technology include BASF SE, Dow, Eastman Chemical Company, Oxea, Perstorp, and Mitsubishi Chemical Group. Competition centers on hydroformylation efficiency, n-to-iso selectivity, backward integration into propylene, mass-balance sustainability, and geographic production flexibility to serve automotive, construction, and battery-material customers.