Market Overview: C9 Resin Market Growth Driven by Tackifier Realignment, Hydrogenated Resin Rationalization, and Sustainable Modifier Innovation

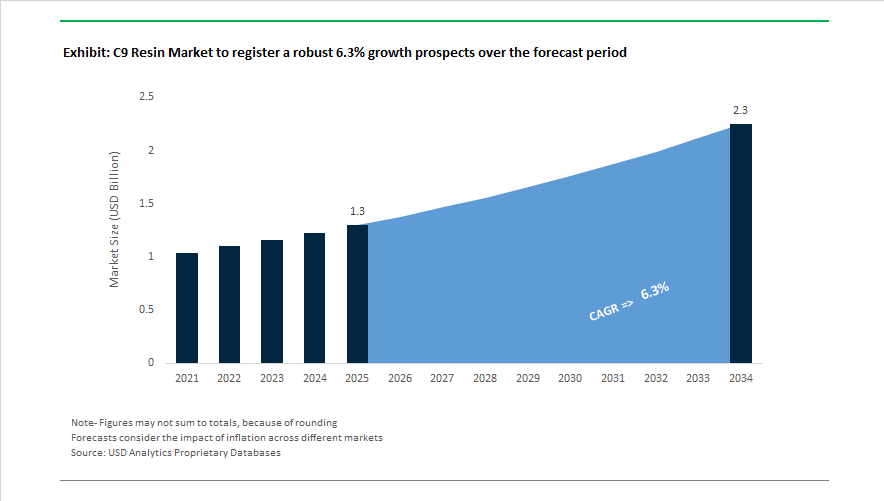

The C9 resin market is projected to grow from USD 1.3 billion in 2025 to USD 2.3 billion by 2034, registering a CAGR of 6.3% , supported by expanding use of aromatic hydrocarbon resins in adhesives, coatings, rubber compounding, and specialty packaging. Structural changes in distribution and supply chains began reshaping the market in May 2025 when Neville Chemical Company expanded its partnership with IMCD US to strengthen access to NEVTAC tackifying resins for U.S. adhesive and coating formulators. Capacity rationalization followed as Arakawa Chemical Industries completed the shutdown of hydrogenated hydrocarbon resin production in Germany during 2025, reflecting Europe’s high energy cost environment and a strategic shift toward more competitive regions. Upstream integration expanded in January 2025 when Rain Carbon Inc. announced a new coal tar distillation facility in India to strengthen aromatic feedstock supply for advanced resins serving infrastructure and industrial applications.

Product innovation and portfolio shifts accelerated during 2025. Neville Chemical Company introduced NEVOXY ECO sustainable epoxy modifiers in 2025, providing bio-hybrid alternatives that can partially displace traditional aromatic C9 modifiers in coatings and adhesives with lower VOC profiles. Between 2024 and 2025, Kolon Industries achieved milestones in hydrogenated C9 resins designed for hygiene and medical packaging, where ultra-light color and low odor characteristics are critical. July 2025 closure of a U.S. tackifier line by ExxonMobil shifted North American sourcing toward Asia, increasing import dependency. In February 2025, Rain Carbon entered sodium-ion battery research collaborations, expanding resin-related carbon chemistry into energy storage. Meanwhile, TotalEnergies Cray Valley in 2025 refocused on high-performance liquid resins to support rubber compounding and food-contact packaging.

Cost pressures and specialty demand trends influenced the market into 2026. January 2026 price increases from Eastman Chemical Company across oxo and ester derivatives signaled upstream cost escalation affecting resin and plasticizer chains. February 2026 reporting from Arakawa Chemical showed recovery in electronic materials resins tied to semiconductor packaging and display technologies, offsetting softness in traditional paper applications. Market intelligence in December 2025 pointed to range-bound APAC pricing for C5 and C9 petroleum resins amid high inventories and subdued Chinese construction demand. By 2025 and early 2026, industry movement toward PFAS-free and halogen-free adhesive formulations accelerated, with producers including Resonac and Eastman developing modified C9 resins optimized for adhesion to recycled plastics and bio-based substrates.

Sustainability-Driven Feedstock Reformulation, Hydrogenated Growth, and Infrastructure-Linked Demand Define Trends and Opportunities in the C9 Resin Market

Shift Toward Bio-Based and DCPD-Modified C9 Resins to Reduce Crude Dependency and Improve Polymer Performance

The C9 Resin Market is undergoing a decisive feedstock transition, driven by volatility in crude oil pricing and performance expectations in automotive, rubber, and coatings applications. In March 2024, resin manufacturers introduced commercially available bio-based C9 resins derived from bio-naphtha and tall oil. These products are engineered primarily for automotive OEMs and industrial coating manufacturers seeking demonstrable Scope 3 emissions reductions while maintaining softening points near 120°C, a critical parameter for rubber-to-road heat resistance and coating hardness.

In parallel, Dicyclopentadiene (DCPD) modification is emerging as a performance differentiator. DCPD-enhanced resins are now widely used for tire rubber compounding, particularly in tread formulations where rolling resistance and wet-grip compliance directly influence OEM sustainability and fuel-efficiency targets. Their thermal strength and color stability (Gardner < 1) align with high-spec manufacturing lines that require consistent optical clarity and low processing discoloration in 2025.

Global Capacity Consolidation and the Hydrogenated-C9 Shift Reflect a “Flight to Quality”

Producers are strategically rationalizing C9 capacity, prioritizing high-margin hydrogenated grades as global demand pivots away from commodity resins. Neville Chemical’s May 2025 expansion of its partnership with IMCD in the United States illustrates the shift toward integrated distribution models that bundle resin supply with formulation support and technical advisory.

Hydrogenated C9 Resins are gaining traction due to their high UV-resistance, water-white optical clarity, and suitability for high-sanitation product categories such as electronics assembly adhesives and medical packaging. Hydrogenation eliminates double-bond reactivity, creating resins that are chemically inert, oxidation-resistant, and compatible with Hot-Melt Adhesives (HMA), which continue to expand with rapid e-commerce packaging growth and smart-factory logistics requirements.

C9 Resins as Critical Tackifiers in Thermoplastic Road Marking Paints Used in Infrastructure and Safety Programs

Government-funded infrastructure acceleration is increasing material demand for C9 Resin–based binders in thermoplastic road marking paints. India, Qatar, and the United States are prioritizing high-retroreflective surface markings capable of supporting autonomous-vehicle lane-sensor recognition. C9-based tackifiers deliver fast-dry chemistry and strong bead-binding to prevent micro-bead embedment loss under high-load traffic.

Public expenditure trends, including approximately $1.6 trillion in U.S. infrastructure allocations by 2024, are reinforcing recurring revenue cycles for C9-enabled striping materials. Highways and airport runways require mandatory re-coating within defined maintenance intervals, strengthening multi-year procurement contracts for resin formulators.

Hydrogenated Low-Odor C9 Tackifiers Support Non-Woven Hygiene Adhesive Growth

Pressure-Sensitive Adhesives (PSA) used in disposable hygiene products—adult incontinence pads, feminine hygiene goods, and baby diapers—represent a rapidly expanding niche for hydrogenated C9 resins. Hygiene-grade PSA requires extremely low odor thresholds and high-bond permanence, particularly for elastic and core-stabilization bonding.

Producers are investing in odor-stripping purification technologies that remove volatile monomers and resin by-products to meet international brand-owner sensory specifications. Compatibility with SIS and SBS block copolymers makes C9 resins especially valuable for non-woven elastic attachments in Asia-Pacific markets, where demographic growth and rising disposable-income levels drive product premiumization.

C9 Resin Market Share and Segmentation Insights

Market Share by Resin Type: Non-Hydrogenated Grades Lead Volume While Hydrogenated C9 Accelerates in High-Performance Adhesives

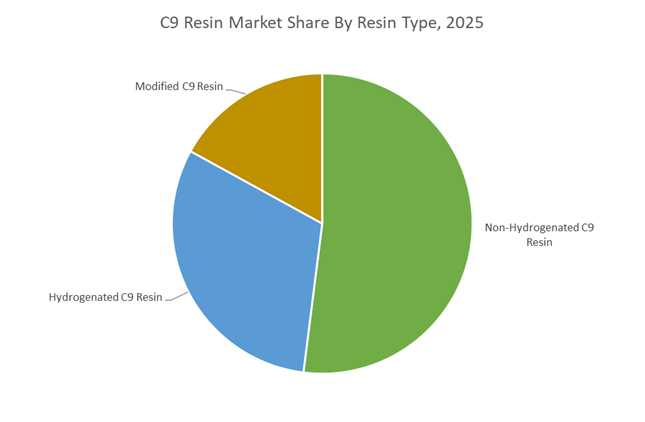

Non-hydrogenated C9 resin holds 52% of market share in 2025, driven by its low cost, broad compatibility, and deep color profile, making it suitable for rubber compounding, road marking paints, general-purpose inks, and low-grade adhesives, with volume concentrated in Asia-Pacific. Hydrogenated C9 resin is the fastest-growing segment, as saturation of unsaturated bonds produces water-white resins with superior UV resistance, thermal stability, and low odor. These properties are critical for hot-melt adhesives used in hygiene products, food-safe packaging, labels, and clear road markings, with demand accelerating alongside low-VOC regulations and premium packaging requirements. Modified C9 resin represents a specialty niche, where maleated, phenolated, or acrylated grades improve adhesion to metals, glass, and engineering plastics, enabling use in marine coatings, tire treads, and specialty sealants, commanding premium pricing despite lower volumes.

Market Share by End Use Industry: Packaging Anchors Demand as Hygiene Products Drive Premium Growth

Packaging accounts for 37% of C9 resin consumption in 2025, led by hydrogenated grades serving as tackifiers in hot-melt adhesives for carton sealing, tray forming, and flexible laminates, while non-hydrogenated resins support cost-sensitive corrugated packaging. Building and construction follow, utilizing C9 resins in road marking paints, roofing membranes, waterproofing compounds, and alkyd coatings, with infrastructure development in emerging economies sustaining baseline demand. Automotive and transportation consume C9 resins in tire building adhesives, rubber compounding, and sealants, with modified grades supporting adhesion to coated metals and lightweight substrates. Personal hygiene and medical represent the fastest-growing segment, relying on water-white hydrogenated C9 resins for diaper elastic attachment, core stabilization, and backsheet lamination, with aging populations and rising hygiene standards in developing markets accelerating adoption.

Competitive Landscape of the C9 Resin Market

The global C9 resin market in 2026 is shaped by strong demand from hot-melt adhesives, performance coatings, road marking paints, hygiene products, EV components, and packaging applications, alongside rapid adoption of hydrogenated C9 resins, mass-balanced feedstocks, and low-odor tackifiers. Competition centers on cracker-to-resin integration, hydrogenation technology, molecular weight control, and ISCC PLUS-certified sustainability platforms. Market leaders are leveraging vertical integration, advanced recycling, and application-led resin design to serve high-growth segments such as medical adhesives, smart infrastructure coatings, and automotive bonding, while Asian producers continue to expand capacity to capture the accelerating “clean resin” transition.

Cracker-integrated adhesion science leadership by ExxonMobil Chemical Company

ExxonMobil dominates the 2026 C9 resin market through unmatched cracker-to-resin integration, controlling C9 aromatic stream quality directly from its proprietary steam crackers. Its Escorez™ 2000 and hydrogenated Escorez™ 5000 series are industry benchmarks for high-clarity hot-melt adhesives used in premium packaging and medical tapes. In 2026, ExxonMobil is advancing “adhesion science leadership” by co-optimizing C9 resins with its Vistamaxx™ performance polymers for superior bonding efficiency. The company also reached new milestones in advanced recycling, supplying mass-balanced C9 resins that enable recycled-content claims without compromising adhesive strength, reinforcing its leadership in sustainable hydrocarbon resin solutions.

Crosslinkable resin innovation from Kolon Industries, Inc.

Kolon Industries enters 2026 as the world’s second-largest hydrocarbon resin producer, specializing in aromatic and hydrogenated C9 systems. Its HIKOTACK® and SUKOREZ® brands serve hygiene, packaging, and electronics markets, with SUKOREZ favored for its water-white color and near-zero odor. Kolon commercialized the world’s first crosslinkable hydrocarbon resin in late 2025, delivering superior thermal stability for automotive applications. The 2025/2026 Yeosu expansion cemented Kolon’s position as South Korea’s largest C5/C9 producer. Its integrated technology platform enables precise tuning of softening points and molecular weight distributions for advanced 6G and infrastructure requirements.

High-value performance coatings focus at Eastman Chemical Company

Eastman treats C9 resins as a core pillar of its innovation-driven growth strategy, emphasizing high-purity grades for transportation and building materials. Following portfolio rationalization, its 2026 focus is on value-added C9 resins for performance coatings, especially road marking paints requiring rapid drying and weather resistance for smart-city infrastructure. Eastman implemented off-list price increases in early 2026 to manage feedstock and energy inflation. Recent developments include Naia™ Lyte-compatible resin binders, illustrating Eastman’s ability to bridge traditional C9 chemistry with sustainable textile and specialty materials, strengthening its position in advanced coatings and engineered resin applications.

ISCC PLUS-certified specialty C9 resins from Cray Valley

Cray Valley, the specialty additives arm of TotalEnergies, focuses on low-molecular-weight, functionalized C9 resins that enhance rubber processing and ink performance. Its Cleartack® and Norsolene® brands are widely used in tires and high-speed digital printing, where pigment wetting is critical. With ISCC PLUS certification achieved at its Carling facility, Cray Valley now supplies bio-attributed C9 resins to European customers in 2026. The company’s low-carbon transition roadmap targets replacing up to 20% of hydrocarbon feedstocks with bio-sourced monomers, positioning Cray Valley as a leader in responsible innovation for specialty hydrocarbon resins.

Asian clean-resin expansion by Hanwha Solutions

Hanwha Solutions is rapidly scaling hydrogenated C9 and DCPD resin capacity, operating 150 KTA across three lines in early 2026. Its proprietary high-temperature polymerization and high-pressure hydrogenation technologies enable ultra-pure, low-toxicity resins used in EV vibration-damping compounds and automotive trim bonding. With full vertical integration from naphtha cracking to C9 fractionation and resin synthesis, Hanwha exports specialty C9 resins to over 120 countries while maintaining strong margins. The company is emerging as a key supplier to the Asian “clean resin” market, supporting electric mobility and functional polymer applications.

Hybrid tackifier engineering from Arakawa Chemical Industries, Ltd.

Arakawa Chemical is Japan’s leader in fine tackifier chemistry, combining rosin-based and petroleum-derived C9 systems to deliver hybrid adhesion solutions. Its ARKON® alicyclic hydrocarbon resins remain prestige products for medical adhesives and high-transparency film lamination in 2026. Guided by its KAITEKI chemistry philosophy, Arakawa is investing in solvent-free C9 production to reduce VOC emissions and advance circular economy goals. Expanded R&D hubs in Southeast Asia are enabling development of humidity-resistant C9 resins tailored for tropical construction markets, reinforcing Arakawa’s niche strength in precision adhesion engineering.

China’s Integrated Tire Manufacturing and Naphtha Cracker Optimization Reshaping the C9 Resin Value Chain

China remains the structural backbone of the global C9 resin industry, driven by vertically integrated petrochemical clusters and expanding downstream rubber and adhesive demand. In late 2024, Shanghai Huaqing Petroleum Development Group initiated a multi-phase tire manufacturing project in Yongzhou, designed to produce 21.1 million tire units annually. The “First Phase” alone spans 300 acres and targets 7.25 million units, directly anchoring local C9 tackifier resin supply chains used in rubber compounding and pressure-sensitive adhesives. This integrated tire manufacturing expansion materially strengthens captive demand for C9 hydrocarbon resins in high-performance elastomer blends.

Upstream, major state-owned refiners such as Sinopec Zhenhai and PetroChina Daqing have completed upgrades to naphtha crackers to optimize C9 aromatic fraction recovery as a byproduct of ethylene production. These feedstock integration initiatives enhance aromatic hydrocarbon yield efficiency, securing cost-competitive raw materials for C9 resin polymerization. In May 2025, a leading domestic producer deployed AI-based predictive control systems across hydrogenation lines, reducing energy consumption by 12% while stabilizing resin color consistency for premium export markets.

United States C9 Resin Market Strengthened by Shale-Derived Feedstock and Specialty Resin Innovation

The United States C9 resin market is characterized by regulatory modernization, shale-based feedstock integration, and high-value hydrogenated resin innovation. The Petroleum and Natural Gas Rules 2025 have streamlined hydrocarbon leasing frameworks, ensuring stable access to naphtha-derived feedstocks critical for aromatic C9 resin production. Gulf Coast petrochemical hubs in Texas and Louisiana have integrated shale-derived naphtha processing, lowering the cost basis for hydrocarbon resin manufacturing and reinforcing North America’s competitive export position.

Strategic distribution partnerships are expanding market reach. In May 2025, Neville Chemical Company expanded its agreement with IMCD to enhance availability of the NEVTAC series—specialized C9 tackifying resins—across adhesive and coatings markets. Simultaneously, industry leaders such as Eastman Chemical Company and ExxonMobil are intensifying R&D in hydrogenated C9 resins aligned with the domestic “clean label” packaging movement, emphasizing low odor, high thermal stability, and low VOC content.

India’s Regulatory Reforms and Smart Infrastructure Spending Catalyzing Domestic C9 Resin Expansion

India’s C9 resin market is entering a structurally transformative phase supported by regulatory clarity, petrochemical expansion targets, and infrastructure-led demand acceleration. The Oilfields (Regulation and Development) Amendment Act 2025 introduced 30-year long-term leases, providing stability for capital-intensive C9 resin production facilities that rely on long-cycle investment planning. The Ministry of Petroleum & Natural Gas has set a strategic objective to scale the national chemical and petrochemical sector from $220 billion to $300 billion by 2027, positioning high-performance hydrocarbon resins as a core growth pillar.

Demand-side growth is being propelled by urban infrastructure programs such as the Smart City Mission, which has increased consumption of C9 resin-based thermoplastic road markings, construction sealants, and waterproofing systems. Government-backed initiatives like Mission Anveshan are accelerating domestic hydrocarbon exploration to reduce import dependence, particularly given that petrochemical feedstocks account for approximately 12% of global oil demand. This import substitution strategy is structurally positive for India’s long-term C9 resin supply security.

South Korea’s Hydrogenated Resin Innovation and EV Integration Driving High-Performance C9 Demand

South Korea’s C9 resin industry is defined by technological sophistication, export efficiency, and electronics-grade resin development. Industry leaders such as LG Chem and Kolon Industries have introduced next-generation hydrogenated petroleum resins (H-Resins) engineered for optical clarity in LED assemblies and high-performance electronics encapsulation. These hydrogenated C9 resins offer superior color stability and ultra-low sulfur content, meeting stringent quality specifications for advanced applications.

Sustainability initiatives are gaining traction, with pilot-scale production of bio-mixed C9 resins incorporating renewable feedstocks while preserving the mechanical tack properties of traditional aromatic hydrocarbon resins. Automotive integration is another high-growth vector: as EV production scales, Korean producers have developed vibration-damping C9 compounds used in battery housing adhesives and interior trim bonding.

Germany’s Low-Emission C9 Resin Development Aligned with EU Eco-Label and Circular Economy Targets

Germany’s C9 resin market is shaped by stringent EU environmental regulations, high-value specialty applications, and circular economy mandates. In alignment with EU eco-label requirements, major chemical producers including BASF are prioritizing solvent-free, low-emission C9 resins for building and construction adhesives. Regulatory pressure is accelerating the shift toward low-VOC hydrocarbon resins tailored for indoor air quality compliance.

German manufacturers are also advancing C9 resin-modified elastomers for high-end sporting goods and medical devices, where biocompatibility, low migration, and mechanical resilience are critical. Circular economy initiatives are integrating recycled feedstock components into C9 polymerization processes to meet national 2030 decarbonization targets.

Vietnam’s FDI-Driven Petrochemical Integration Accelerating C9 Resin Blending and Export Support

Vietnam is emerging as a strategic Southeast Asian hub in the C9 resin value chain, supported by infrastructure expansion and rising foreign direct investment. In early 2024, Vinhomes JSC announced a $966 million investment in smart, green mega-urban projects, stimulating demand for C9-based waterproofing membranes, construction adhesives, and sealants.

Manufacturing migration from China and other regional markets has prompted multinational adhesive companies to relocate operations to Vietnam. This shift has catalyzed the establishment of local C9 resin blending and distribution hubs serving the furniture and footwear export industries. The Ministry of Industry and Trade has introduced tax holidays for petrochemical downstream projects, specifically targeting hydrocarbon resin production to strengthen domestic packaging capabilities.

FDI inflows into petrochemical zones have increased by approximately 15% year-over-year, with integration strategies linking C9 resin production to local naphtha supply from the Nghi Son Refinery. This localized feedstock-resin-application ecosystem enhances supply chain resilience and positions Vietnam as a competitive, export-oriented C9 hydrocarbon resin manufacturing base within Southeast Asia.

C9 Resin Market Report Scope

C9 Resin Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Resin Type (Non Hydrogenated C9 Resin, Hydrogenated C9 Resin, Modified C9 Resin), By Physical Form (Granules and Flakes, Liquid and Molten), By Softening Point (Low Softening Point, Medium Softening Point, High Softening Point), By Application (Adhesives and Sealants, Paints and Coatings, Printing Inks, Rubber Compounding, Construction), By End Use Industry (Automotive and Transportation, Building and Construction, Packaging, Personal Hygiene and Medical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, Eastman Chemical Company, Kolon Industries, Neville Chemical Company, Cray Valley, Arakawa Chemical Industries, RutgerS Group, Henghe Materials and Science Technology, Shandong Landun Petroleum Resin, Puyang Tiancheng Chemical, Shanghai Jinsen Hydrocarbon Resins, Zeon Corporation, Lesco Chemical, Puyang Ruisen Petroleum Resins, Zhejiang Lohas Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

C9 Resin Market Segmentation

By Resin Type

- Non Hydrogenated C9 Resin

- Hydrogenated C9 Resin

- Modified C9 Resin

By Physical Form

- Granules and Flakes

- Liquid and Molten

By Softening Point

- Low Softening Point

- Medium Softening Point

- High Softening Point

By Application

- Adhesives and Sealants

- Paints and Coatings

- Printing Inks

- Rubber Compounding

- Construction

By End Use Industry

- Automotive and Transportation

- Building and Construction

- Packaging

- Personal Hygiene and Medical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in C9 Resin Industry

- Exxon Mobil Corporation

- Eastman Chemical Company

- Kolon Industries

- Neville Chemical Company

- Cray Valley

- Arakawa Chemical Industries

- RutgerS Group

- Henghe Materials and Science Technology

- Shandong Landun Petroleum Resin

- Puyang Tiancheng Chemical

- Shanghai Jinsen Hydrocarbon Resins

- Zeon Corporation

- Lesco Chemical

- Puyang Ruisen Petroleum Resins

- Zhejiang Lohas Chemical

*- List not Exhaustive