Dicyclopentadiene Market to Reach $2.2 Billion by 2034 at 6% CAGR Driven by High-Purity Expansion and Circular Resin Innovation

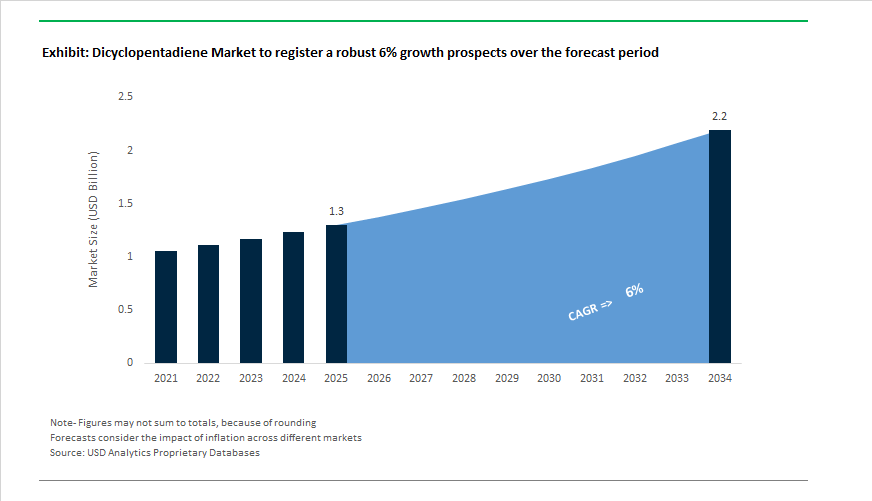

The Dicyclopentadiene (DCPD) Market is projected to grow from $1.3 billion in 2025 to $2.2 billion by 2034, registering a CAGR of 6%. DCPD remains a critical C5 hydrocarbon intermediate derived from steam cracking of naphtha and gas oils, serving as a backbone for unsaturated polyester resins (UPR), hydrocarbon resins, EPDM elastomers, and cyclic olefin polymers. Demand acceleration is being shaped by infrastructure expansion in Asia, lightweight composite adoption in automotive manufacturing, and the structural shift toward styrene-free and PFAS-free resin systems. Regulatory tightening on volatile organic compound emissions and hazardous air pollutants is simultaneously reshaping production standards across major Gulf Coast and East Asian cracking hubs.

Regulatory enforcement intensified in late 2024, when the U.S. EPA finalized updates to the Hazardous Organic NESHAP standards for synthetic organic chemical manufacturing. Through 2025, DCPD producers were required to implement enhanced leak detection and repair programs and reduce VOC emissions at major Gulf Coast facilities. Capacity expansions followed. In 2025, ExxonMobil completed a 20% DCPD capacity expansion at its Baton Rouge, Louisiana facility to address supply tightness in North American adhesives and coatings markets after 2024 logistics disruptions. In parallel, Eneos Corporation finalized its DCPD resin expansion in Japan between 2024 and 2025, supporting the country’s transition toward lightweight composites as Toyota and Honda accelerate solid-state EV platforms. Bio-based innovation also intensified between 2024 and 2025, with Arlanxeo and ExxonMobil ramping up production of bio-based EPDM grades using renewable sugarcane-derived bio-ethylene, enabling 50–70% bio-based content in finished elastomers and aligning with ZDHC and ESG mandates.

Structural investments escalated in 2025 and 2026. Braskem scaled proprietary metathesis technology in 2025 to produce ultra-high-performance DCPD resins for Reaction Injection Molding, targeting wind turbine nacelles and agricultural machinery components. The Indian government’s Green Corridor and Smart Cities Mission triggered a surge in UPR consumption during 2025–2026, pushing domestic players such as Deepak Nitrite and Matangi Industries to increase procurement of DCPD-UPR grades for corrosion-resistant piping and infrastructure composites. In China, CNPC and BASF confirmed plans to construct a 100,000 metric ton per annum DCPD plant expected to be operational by late 2026, reinforcing Asia-Pacific’s dominance in high-performance resin manufacturing for automotive and electronics sectors. Strategic portfolio shifts also emerged. In January 2026, LyondellBasell advanced its European divestment plan under a broader $1.3 billion Cash Improvement Plan while evaluating debottlenecking of its Channelview, Texas polybutadiene unit to expand elastomer output using DCPD intermediates. In February 2026, Kolon Industries announced a pivot toward ultra-high purity DCPD above 99%, targeting 3D printing filaments and cyclic olefin polymers for medical syringes and pharmaceutical packaging. Concurrently, the industry accelerated commercialization of styrene-free DCPD resins during 2025, responding to EU regulatory scrutiny and indoor air quality concerns in construction and solid-surface applications.

Trends and Opportunities in the Global Dicyclopentadiene (DCPD) Market

Rising Use of DCPD-Modified Unsaturated Polyester Resins in Marine and Infrastructure Applications

- DCPD-modified unsaturated polyester resins are gaining strong traction in marine, construction, and industrial infrastructure due to their superior durability and lower environmental footprint compared with conventional orthophthalic resins. These formulations typically require styrene levels below 35% to achieve workable viscosities, significantly reducing volatile organic compound emissions during fabrication. Following updated low-VOC formulation guidance issued in July 2024 by the European Chemicals Agency, adoption of DCPD-based UPR systems has accelerated in applications such as boat hulls, large corrosion-resistant storage tanks, and wastewater treatment components, where workplace exposure limits are increasingly stringent.

- Performance data from 2024 and 2025 further supports this transition. DCPD-modified resins exhibit hydrophobic behavior and markedly lower water absorption than traditional polyester systems, improving long-term dimensional stability and resistance to blistering. These characteristics have positioned DCPD-based UPR as the preferred material for rehabilitation panels used in aging bridges and coastal infrastructure, as well as fiber-reinforced components operating in the aggressive chemical environments of chlor-alkali plants. As infrastructure spending rises globally, demand for these low-emission, high-durability composites is expected to remain structurally strong.

High-Purity DCPD Enabling Growth of pDCPD via ROMP and RIM Technologies

- The expansion of polydicyclopentadiene applications is directly tied to the availability of ultra-high-purity DCPD, typically exceeding 99%. High-purity feedstock is essential for ring-opening metathesis polymerization, which relies on ruthenium-based Grubbs catalysts that are highly sensitive to impurities and moisture. Technical briefings released in January 2025 by Exothermic Molding highlight that pDCPD systems now deliver exceptional impact strength and stiffness at relatively low densities, enabling consolidation of multiple metal parts into a single molded component.

- This capability is driving substitution of metals in heavy equipment housings, agricultural machinery panels, and electric vehicle battery enclosures. In parallel, a major chemical producer announced in 2024 a breakthrough catalytic purification process that increases DCPD purity while cutting energy consumption by approximately 20%. Such advances are critical because even trace isomeric contamination can deactivate catalysts used in reaction injection molding, which remains the dominant high-throughput manufacturing route for large, aerodynamically complex pDCPD parts.

High-Energy-Density Feedstock Pathways for Sustainable Aviation Fuel

- DCPD is attracting attention as a non-food, high-energy-density feedstock for advanced aviation fuels. Research conducted during 2024 and 2025 by the Australian National University used machine-learning-driven screening to identify polycyclic hydrocarbons derived from DCPD as promising candidates for high-energy-density fuels. Through controlled oligomerization and hydrogenation, DCPD derivatives can meet ASTM D7566 and D4054 specifications, offering higher heats of combustion and lower freeze points than conventional Jet A-1.

- These attributes align closely with policy-driven market creation. Under the United States SAF Grand Challenge, which targets domestic production of 3 billion gallons of sustainable aviation fuel by 2030, DCPD is being evaluated as a blendstock to enhance range and payload capacity without increasing fuel volume. Its high carbon-to-hydrogen ratio also supports niche demand in high-performance military and racing fuels, positioning DCPD as a strategic molecule within next-generation aviation energy systems.

Building Blocks for High-Refractive-Index Polymers in AR and VR Optics

- Beyond fuels and composites, DCPD is emerging as a valuable building block for advanced optical polymers. Studies published in Macromolecules in October 2025 demonstrate that incorporating DCPD into polymer backbones via photoinitiated ROMP enables precise tuning of refractive indices above 1.60. These high-refractive-index materials are critical for light-guiding films, waveguides, and compact lenses used in augmented and virtual reality devices, where optical performance must be balanced with lightweight design and manufacturability.

- Additive manufacturing is amplifying this opportunity. Research reported in late 2024 and 2025 shows that stereolithographic 3D printing of pDCPD using latent ruthenium catalysts can produce complex optical components with microscale features and high surface fidelity. This capability opens a high-margin pathway for DCPD in high-brightness LED encapsulants, customized optical elements, and next-generation AR and VR architectures. As immersive electronics scale, DCPD-based optical polymers are poised to move from laboratory validation to commercial production.

Dicyclopentadiene (DCPD) Market Share and Segmentation Insights

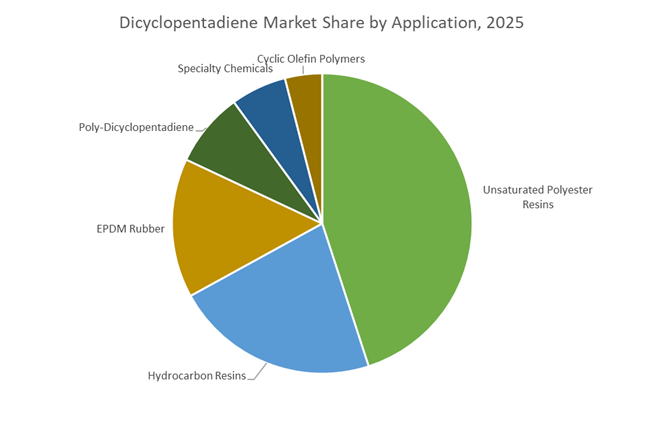

Market Share by Application : Unsaturated Polyester Resins Lead While Poly-DCPD and COPs Drive High-Value Growth

Unsaturated polyester resins (UPR) account for 45% of global DCPD consumption in 2025, establishing Dicyclopentadiene as a core modifier for construction composites, marine laminates, and transportation panels. DCPD-modified UPR delivers higher heat distortion temperature, improved chemical resistance, and reduced styrene emissions compared with conventional orthophthalic systems, accelerating adoption in fiberglass-reinforced plastics and polymer concrete. Hydrocarbon resins derived from DCPD represent a major secondary segment, supporting hot-melt adhesives, pressure-sensitive adhesives, printing inks, and rubber compounding through enhanced tackification and compatibility. EPDM rubber relies on DCPD-derived ENB as a critical third monomer, enabling sulfur vulcanization for automotive seals and roofing membranes. Poly-DCPD continues expanding via reaction injection molding for large impact-resistant parts, while specialty chemicals remain niche. Cyclic olefin polymers (COP/COC) form a premium segment for medical devices and pharmaceutical packaging, valued for optical clarity and moisture barrier performance.

Market Share by End-Use Industry : Construction Anchors Volume as Automotive and Electronics Accelerate Adoption

Building and construction holds 30% market share, driven by DCPD-based unsaturated polyester resins in FRP panels, bathroom fixtures, and polymer concrete, alongside EPDM roofing membranes and construction sealants. Automotive follows as a major consumer, using DCPD in EPDM hoses and weatherstrips, sheet molding compounds (SMC) for lightweight body panels, and poly-DCPD for durable exterior components that support vehicle weight reduction. The marine sector depends heavily on DCPD-modified resins for hulls, decks, and gel coats where long-term water resistance is essential. Electrical and electronics applications are growing steadily, leveraging DCPD-derived laminates and encapsulants for dielectric stability and thermal performance. Packaging utilizes DCPD hydrocarbon resins in labels, tapes, and flexible packaging adhesives. Aerospace and defense remain a specialized but high-value segment, specifying poly-DCPD composites and advanced resins for radomes and structural components requiring impact resistance and dimensional stability under extreme conditions.

Competitive Landscape of the Dicyclopentadiene (DCPD) Market

The global Dicyclopentadiene market is led by integrated petrochemical majors and high-purity specialists supplying polyester-grade and electronic-grade DCPD for reaction injection molding (RIM), hydrocarbon resins, EPDM elastomers, and advanced composites across automotive, construction, wind energy, and electronics.

Shell drives high-purity DCPD through global C5 cracker integration

Shell Chemicals anchors the premium segment of the DCPD market by leveraging its vast global ethylene cracker network to capture C5 fractions with unmatched reliability. The company supplies high-purity DCPD (>99%) optimized for Reaction Injection Molding (RIM), enabling lightweight, high-impact automotive body panels. Shell’s “Value over Volume” strategy prioritizes specialty grades for medical and electronic applications, moving away from commodity polyester supply. In 2025–2026, Shell invested in digital twin technology across its steam crackers, improving C5 yield optimization and cutting energy intensity by roughly 10%. This combination of supply security, process digitization, and specialty focus positions Shell as a benchmark producer in the global DCPD value chain.

Dow integrates resin-grade DCPD into low-VOC construction systems

Dow leads the North American DCPD market through deep integration into hydrocarbon resins and coatings systems. Its DOW™ DCPD Resin Grade (73%–83% Endo-DCPD) is engineered for architectural paints and interior coatings, while also supporting EPDM elastomers used in EV weather-stripping and sealing applications. In early 2026, Dow introduced low-VOC DCPD formulations aligned with European Green Deal indoor air quality requirements, strengthening its position in sustainable construction materials. Backed by its “Transform to Outperform” initiative, Dow is optimizing production with AI while developing drop-in solutions for adhesives and sealants, making it a critical supplier for performance-driven DCPD applications.

ExxonMobil scales ultra-low-color DCPD for advanced adhesives

ExxonMobil Chemical is executing one of the industry’s largest DCPD capacity expansions, completing a 20% upgrade at its Baton Rouge facility in 2025 and reaching full output in early 2026. This expansion supports the fast-growing hydrocarbon resin market, projected to exceed 4.5% annual growth in North America. ExxonMobil differentiates through proprietary catalyst technology that produces ultra-low-color DCPD, essential for transparent adhesives and specialty optical films. With world-class polymer R&D, the company frequently co-develops customized resin grades with tier-one automotive OEMs, reinforcing its leadership in high-performance coatings, structural adhesives, and next-generation composite systems.

Braskem advances renewable DCPD for marine and wind composites

Braskem dominates Latin America’s DCPD supply while expanding exports to the U.S. and Europe, supported by long-term feedstock agreements with Petrobras that stabilize margins amid oil price volatility. In 2026, Braskem began piloting “Green C5” pathways, using bio-based feedstocks to produce partially renewable DCPD for premium composite markets. The company is a major supplier of DCPD-based unsaturated polyester resins (UPR) for marine vessels and wind turbine blades, where corrosion resistance and structural durability are critical. With 2025 revenues exceeding $77 billion, Braskem’s specialty chemicals segment continues to gain momentum, particularly in sustainable energy infrastructure.

Kolon targets mobility and aerospace with specialty DCPD resins

Kolon Industries is a high-value materials leader in Asia-Pacific, positioning DCPD as a strategic building block for mobility, aerospace, and battery technologies. In 2026, Kolon launched high-purity HDCP aimed at missile fuel intermediates (JP-10 synthesis) while also expanding DCPD-derived hydrocarbon resins for EV tire performance, improving grip and rolling resistance. Under its “Pioneering Sustainable Materials” roadmap, Kolon is investing in hydrogen systems and advanced battery separator coatings. The opening of a new Vietnam distribution hub in early 2026 further strengthens its regional footprint, supporting electronics manufacturing growth across Southeast Asia.

Maruzen delivers ultra-clean HDCP for optical and medical polymers

Maruzen Petrochemical is recognized for producing some of the world’s purest DCPD, offering HDCP with typical purity of 99.7% and ultra-low color (Hazen Unit ~5), critical for optical-grade resins. Through proprietary C5 dimerization and refining, Maruzen supplies Japan’s cyclic olefin polymer (COP) ecosystem, enabling smartphone components and medical devices that demand zero discoloration. In 2026, the company expanded packaging formats to custom 193 kg drums and tanks, supporting specialty chemical customers in Europe and India. Maruzen’s technical precision and niche purity leadership secure its role in premium electronics and healthcare applications.

China: Policy-Backed Scale-Up and EV-Oriented Materials Strategy

China’s dicyclopentadiene ecosystem is being reshaped by a tightly coordinated policy and capacity expansion agenda that links petrochemical scale with advanced manufacturing outcomes. The 2025–2026 work plan jointly issued by the Ministry of Industry and Information Technology and the NDRC targets sustained growth in chemical added value, with explicit prioritization of high-purity DCPD above 99%. This focus aligns with national aerospace and high-end manufacturing objectives under the Made in China 2025 framework, where resin consistency and thermal stability are critical inputs.

On the supply side, integration of large C5 separation units into new steam crackers across Zhejiang and Guangdong has positioned China to reach projected DCPD capacity of roughly 1.5 million tons by 2025. This scale is not purely volumetric. Under the 2026 New Energy Vehicle strategy, DCPD-based Reaction Injection Molding has been incentivized for large body panels to reduce curb weight by double-digit percentages versus steel. Parallel digitalization efforts underscore the quality pivot. In late 2024 and early 2025, Zibo Luhua Hongjin New Material implemented AI-driven controls on DCPD resin lines, cutting specific energy consumption by 15%. The combined effect is a China market characterized by rapid scale, specification tightening, and direct pull from EV lightweighting programs.

United States: Feedstock Advantage and Infrastructure-Driven Specialty Demand

The United States continues to benefit from shale-derived feedstock flexibility, with a 2025 shift toward upgrading heavier NGL fractions to support higher-value DCPD intermediates. Major integrated producers such as ExxonMobil and Dow have highlighted DCPD’s role in advanced circularity initiatives, particularly for unsaturated polyester resins used in durable infrastructure and industrial composites.

Demand-side momentum is being reinforced by public investment. As Infrastructure Investment and Jobs Act projects move into execution through early 2026, domestic consumption of DCPD-modified concrete and corrosion-resistant fiberglass piping has increased, reflecting material substitution in municipal water upgrades. Defense specifications add another layer of resilience. In 2025, the U.S. Department of Defense expanded procurement of DCPD-based composites for specialized aircraft platforms due to favorable strength-to-weight and heat resistance characteristics. Specialty chemical expansion in Texas further supports the quality trend, with Texmark Chemicals increasing high-purity DCPD distillation capacity to serve cyclic olefin copolymer applications in medical diagnostics. Overall, the U.S. market emphasizes feedstock leverage, infrastructure durability, and defense-grade performance.

Japan: Carbon Neutrality Forcing Green DCPD Pathways

Japan’s DCPD strategy is being reframed by its GX2040 Vision and the 7th Basic Energy Plan, approved in February 2025. These policies accelerate the transition toward green and circular feedstocks, compelling producers to decouple DCPD growth from fossil intensity. In July 2025, ENEOS Corporation and Mitsubishi Chemical completed a chemical recycling facility that converts plastic waste into cracker-ready oil, enabling recycled-carbon DCPD streams.

Beyond sustainability, Japan is differentiating through chemistry innovation. ENEOS announced a high-performance ligand in mid-2025 that uses DCPD-based precursors to improve yields in nickel-catalyzed coupling reactions relevant to pharmaceuticals and electronics. Looking ahead, hydrogen infrastructure pilots by Maruzen Petrochemical and Zeon Corporation in 2026 are testing DCPD resins for hydrogen tank liners, leveraging low gas permeability. Japan’s market is thus defined by green feedstocks, specialty chemistry, and early hydrogen economy applications.

South Korea: Automotive Materials Integration and Low-Carbon Export Readiness

South Korea’s DCPD landscape is evolving through corporate consolidation and export-oriented decarbonization. In January 2025, Kolon Industries integrated its automotive materials operations to synchronize DCPD-based resin production with downstream components such as tire cords and interior parts. This alignment supports faster material qualification cycles for OEM programs.

At the same time, Kolon’s investment in a high-tech tire cord facility in Vietnam reflects a regional supply chain expansion strategy that leverages recycled equipment to improve capital efficiency. Environmental competitiveness is becoming central. Petrochemical majors in the Yeosu cluster rolled out carbon capture and utilization pilots on C5 separation units in late 2025, aiming to supply low-carbon DCPD to EU markets facing tightening carbon thresholds. South Korea’s trajectory combines automotive demand alignment with export-focused carbon reduction.

Germany: Specialty Chemicals Focus and Portfolio Rationalization

Germany’s DCPD market is being shaped by strategic exits from commodity polymers and renewed emphasis on specialty intermediates. In April 2025, LANXESS AG completed the sale of its urethane systems business to UBE Corporation, marking a full pivot toward specialty chemicals including DCPD-based advanced intermediates. Rising energy costs have accelerated rationalization, with LANXESS closing its hexane oxidation unit in Krefeld-Uerdingen to redeploy capital into higher-margin bromine and DCPD-derived fragrance and flavor ingredients.

Innovation remains active in adjacent segments. Evonik Industries reported improved EBITDA momentum through 2025–2026 driven by niche coating additives and next-generation biosurfactants that utilize cyclic hydrocarbon backbones. Germany’s DCPD narrative is therefore less about scale and more about value density, margin resilience, and application specialization.

India: Self-Reliance Imperative and Renewable Energy Linkages

India remains structurally short of domestic DCPD supply, a gap formally acknowledged in a 2025 Ministry of Petroleum and Natural Gas report recommending world-scale extraction units to achieve self-reliance by 2030. This recognition has elevated DCPD from a byproduct consideration to a strategic intermediate within the Atmanirbhar Bharat agenda, particularly for composites, resins, and specialty elastomers.

Energy intensity is a key constraint. In October 2025, ENEOS and NTPC Green Energy Limited signed an MOU to explore green methanol and hydrogen derivatives, including the use of renewable power for energy-intensive C5 separation in emerging chemical hubs. This linkage between renewable energy and petrochemical extraction positions India to pursue DCPD capacity growth without proportionate emissions escalation.

Comparative Snapshot: Dicyclopentadiene Industry by Region

Dicyclopentadiene Market Country Level Snapshot

|

Region

|

Primary Strategic Driver

|

Core Applications

|

Structural Direction

|

|

China

|

Policy-backed capacity and EV lightweighting

|

RIM panels, hydrocarbon resins

|

Large-scale, high-purity domestic supply

|

|

United States

|

Feedstock advantage and infrastructure spend

|

UPR, composites, pipes

|

Specialty demand with circularity

|

|

Japan

|

Carbon neutrality and recycling

|

Green DCPD, hydrogen liners

|

Low-carbon, innovation-led

|

|

South Korea

|

Automotive integration and exports

|

Resins, tire cords

|

Decarbonized export readiness

|

|

Germany

|

Portfolio rationalization

|

Specialty intermediates

|

Margin-focused specialization

|

|

India

|

Self-reliance and renewables

|

Emerging composites

|

Capacity build with green energy

|

Dicyclopentadiene (DCPD) Market Report Scope

Dicyclopentadiene Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2.2 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Purity Grade (High Purity, Resin Grade, Unsaturated Polyester Resin Grade), By Application (Unsaturated Polyester Resins, Hydrocarbon Resins, EPDM Rubber, Cyclic Olefin Polymers, Poly-Dicyclopentadiene, Specialty Chemicals), By End-Use Industry (Automotive, Building and Construction, Marine, Electrical and Electronics, Aerospace and Defense, Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Zeon Corporation, LyondellBasell Industries Holdings B.V., Shell Chemicals, Dow Inc., Exxon Mobil Corporation, Chevron Phillips Chemical Company LLC, Texmark Chemicals, Inc., Kolon Industries, Inc., ENEOS Corporation, Maruzen Petrochemical Co., Ltd., Braskem S.A., China Petrochemical Corporation, Zibo Luhua Hongjin New Material Co., Ltd., NOVA Chemicals Corporation, Henghe Design Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dicyclopentadiene Market Segmentation

By Purity Grade

- High Purity

- Resin Grade

- Unsaturated Polyester Resin Grade

By Application

- Unsaturated Polyester Resins

- Hydrocarbon Resins

- EPDM Rubber

- Cyclic Olefin Polymers

- Poly-Dicyclopentadiene

- Specialty Chemicals

By End-Use Industry

- Automotive

- Building and Construction

- Marine

- Electrical and Electronics

- Aerospace and Defense

- Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dicyclopentadiene Industry

- Zeon Corporation

- LyondellBasell Industries Holdings B.V.

- Shell Chemicals

- Dow Inc.

- Exxon Mobil Corporation

- Chevron Phillips Chemical Company LLC

- Texmark Chemicals, Inc.

- Kolon Industries, Inc.

- ENEOS Corporation

- Maruzen Petrochemical Co., Ltd.

- Braskem S.A.

- China Petrochemical Corporation

- Zibo Luhua Hongjin New Material Co., Ltd.

- NOVA Chemicals Corporation

- Henghe Design Co., Ltd.

*- List not Exhaustive