Market Overview: Robotic Unloading, Digital Catalyst Traceability, and Refinery Capacity Expansion Drive Catalyst Handling Services Market

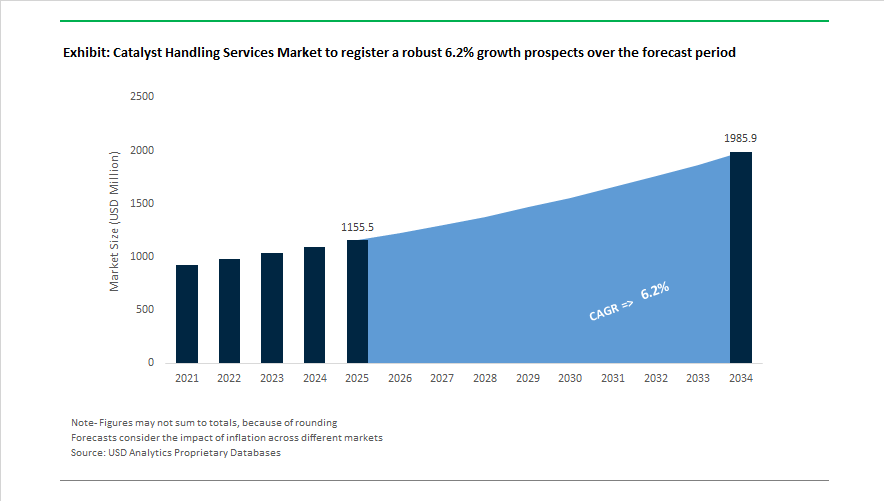

The Catalyst Handling Services Market is projected to expand from USD 1,155.5 Million in 2025 to USD 1,985.6 Million by 2034, registering a CAGR of 6.2% as refineries and petrochemical complexes prioritize automated reactor services, turnaround efficiency, and safety-driven operations. In 2024, Veolia initiated large-scale deployment of robotic catalyst unloading systems across European refinery projects, integrating IoT monitoring and AI-based safety protocols to minimize confined-space exposure. During the same year, Cat Tech International strengthened its North American footprint by acquiring Reactor Services Incorporated, improving its ability to manage inert and hazardous reactor environments along the Gulf Coast. Cat Tech Europe also completed a complex hydrocracker unload and reload project in 2024 using dense loading technology, improving catalyst distribution and reactor performance.

Automation and regional infrastructure growth intensified in 2025. India confirmed plans to raise refining capacity to 8 million barrels per day by 2025, creating significant demand for domestic catalyst loading and commissioning services across hydrocracking and vacuum gas oil units. In October 2025, CR3 Middle East received client recognition in Oman for accelerating catalyst loading schedules through advanced dense loading methods that shortened turnaround windows. In November 2025, CR3 Group signed a long-term cooperation agreement with Samsung E&A to support global EPC projects, strengthening Asia’s catalyst handling ecosystem. The same month, CR3 Thailand earned a Climate Action Leader Award for implementing regeneration-focused spent catalyst handling, reflecting a shift toward circularity and reduced waste disposal.

Digitalization and bio-catalyst specialization define the 2026 outlook. In February 2026, Topsoe highlighted digital monitoring and traceability at ME-CAT 2026, enabling predictive turnaround planning and performance tracking. Early 2026 also marked a safety milestone when CR3 India achieved five million LTI-free work hours, underscoring the sector’s safety culture in high-pressure reactor environments. Since 2025, firms including Veolia and Neste have expanded services to support bio-catalyst handling for renewable diesel and sustainable aviation fuel units, which require different operational protocols. Mourik’s 2024 to 2025 automated maintenance systems and lightweight unloading components further illustrate the transition from labor-intensive to technology-driven reactor service models.

Trends and Opportunities Transforming the Catalyst Handling Services Market

Shift Toward In-Situ Regeneration and Modular “Skidding” for Operational Continuity

A defining trend in the Catalyst Handling Services Market is the accelerated adoption of in-situ regeneration and modular skidding to avoid costly shutdowns and reduce dependency on frequent catalyst replacement cycles. Technical performance data across 2024–2025 confirms that mobile high-temperature regeneration units used on-site can extend catalyst lifespan by up to 20% , creating material EBIT improvements for petrochemical operators. For a standard 600 KTA Propane Dehydrogenation (PDH) facility, this can translate into earnings protection running into tens of millions annually by minimizing change-out frequency and extending reactor run lengths.

Operational decision-makers are also responding to the increased global price of platinum-group metals by deploying guard beds, partial redispersion techniques, and in-vessel attrition control for Pt/CeO₂ systems. The objective is to maximize recoverability of precious metals, where integrated regeneration programs now exceed 90% recovery in high-performance hydroprocessing units. As refineries transition toward lower-carbon fuel slates and petrochemical integration, the strategic focus is shifting away from volume-based catalyst procurement toward lifetime value optimization, where catalyst handling providers compete on turnaround speed, uptime impact, and metallurgical recovery efficiency.

Robotics, ROVs, and Digital Twins Driving a Zero-Entry Workforce Model

The Catalyst Handling Services Market is being redefined by zero-entry safety standards. In 2025, the deployment of screw-propelled robotic Amphirol systems (exemplified by the CAROL platform) became industrially validated, capable of continuous 24/7 operation at internal vessel temperatures of 80°C. This threshold is approximately double the safe temperature conditions for manual work crews, eliminating the need for human entry and thereby reducing insurance liability and fatality risk within confined reactor environments.

Digital twin technologies are also entering mainstream adoption, supported by regulator-backed assessments (e.g., U.S. NRC TLR-RES/DE-2025-09). These virtual replicas are now used in sequence planning prior to unloading, where thermal stress, bed compaction, and reactor metallurgy profiles are simulated to determine the safest loading pattern. The operational benefit is a measurable reduction in vessel wall stress and a corresponding improvement in the accuracy of dense-loading logistics, which directly impacts reactor throughput and fluid dynamics. For catalyst handling providers, digital twin-enabled scheduling is becoming a core differentiator in enterprise RFPs issued by refineries and midstream operators.

Handling Services for Blue Hydrogen, ATR Units, and Carbon Capture Sorbents

Blue Hydrogen development represents the strongest medium-term growth pocket for the Catalyst Handling Services Market. More than 1.5 MTPA of U.S. capacity reached Final Investment Decision in 2025, and large-scale projects such as ExxonMobil Baytown and Linde Gulf Coast ATR trains require ultra-sensitive catalyst loading environments. These catalysts often include sulfur-tolerant reforming systems and proprietary ADIP ULTRA-grade sorbents, which must be loaded and activated in oxygen-excluded atmospheres to ensure CO₂ capture efficiency approaching 99%.

Beyond catalyst longevity, carbon capture plants such as the $5 billion Project Labrador in Texas are generating demand for sorbent handling services that prevent material attrition during loading. Amine-based sorbents are mechanically fragile, and mishandling can reduce surface area and adsorption efficiency, resulting in multi-million-dollar yield loss. Providers deploying soft-loading pneumatic systems and inert-gas gloveboxes are capturing this emerging market segment, often operating under long-term service agreements due to continuous sorbent replenishment cycles.

Distributed Logistics and Portable Catalyst Handling for Modular GTL and Bio-Refineries

The Catalyst Handling Services Market is also moving toward decentralized models, driven by the global expansion of remote and small-scale chemical plants. Modular Gas-to-Liquids systems, such as those scaled by Infinium in 2025, convert flare gas and biogas into Sustainable Aviation Fuel (SAF) using compact catalytic reactors located far from traditional refinery clusters. These remote facilities lack permanent catalyst-extraction personnel, generating a lucrative niche for containerized handling systems that can be mobilized via truck and deployed for unloading, screening, and reactivation.

Another adjacent opportunity lies in the circular economy compliance landscape. Updated EU waste regulations now require recovered catalysts to be transported through certified chains-of-custody for metal reclamation. Catalyst handling firms are responding with “Logistics-as-a-Service” models where they not only unload catalysts on-site but also package, certify, and ship them to refining centers that enable metal recovery. This integrated workflow—extraction, safety management, regulatory compliance, transport, and recovery—positions service providers to move beyond transactional maintenance tasks toward recurring contractual value anchored in sustainability outcomes.

Catalyst Handling Services Market Share and Segmentation Insights

Market Share by Service Type: Catalyst Loading Leads While Regeneration Accelerates Under Circular Economy Pressure

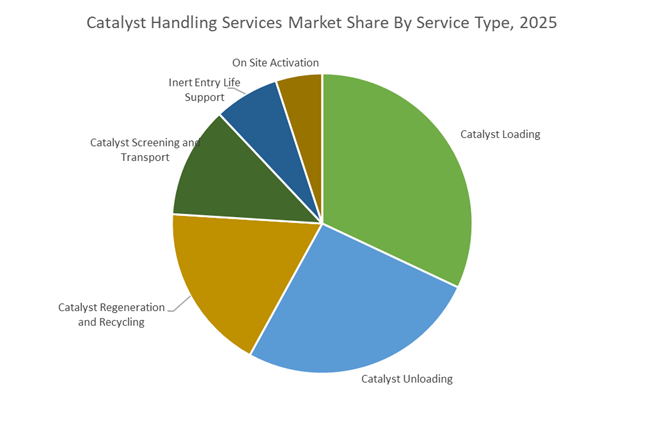

Catalyst loading accounts for 32% of global catalyst handling services demand in 2025, driven by the need for precise catalyst distribution to optimize reactor hydrodynamics, minimize pressure drop, and maximize on-stream efficiency. Dense loading methods such as sock loading and dense phase loading are increasingly specified in hydroprocessing and reforming units, tying demand closely to refinery turnaround schedules and petrochemical capacity additions. Catalyst unloading follows as the second-largest segment, reflecting the technical complexity of removing spent, coke-laden, and potentially pyrophoric catalysts under strict safety protocols. Catalyst regeneration and recycling is the fastest-growing service line, extending catalyst life and enabling recovery of high-value metals such as platinum, palladium, and rhodium, while reducing hazardous waste volumes. Screening and transport services support particle size control and compliant logistics, while inert entry life support and on-site activation remain specialized, safety-critical offerings required for confined-space reactor access and sulfiding or reduction of fresh catalyst charges.

Market Share by End Use Industry: Refining Dominates Volume as Petrochemicals Drive Growth Momentum

Petroleum refining represents 48% of catalyst handling services consumption in 2025, supported by routine changeouts across hydrotreaters, hydrocrackers, FCC units, catalytic reformers, and isomerization reactors. Refinery utilization rates, crude slate variability, and turnaround frequency directly influence service volumes, while IMO 2020 and tightening fuel sulfur specifications continue to elevate hydrodesulfurization catalyst activity. Petrochemicals form the second-largest and fastest-growing segment, fueled by catalyst-intensive steam crackers, aromatics units, and methanol-to-olefins plants, particularly across China’s coal-to-chemicals projects and US Gulf Coast ethane expansions where maintaining high on-stream factors is critical. Chemical manufacturing contributes steady, diversified demand through hydrogenation and oxidation processes, while environmental and emission control is expanding via SCR systems, VOC oxidation, and diesel particulate filter services. Pharmaceuticals and fine chemicals remain niche but high value, emphasizing precious metal recovery, GMP compliance, and frequent batch changeouts.

Competitive Landscape of the Catalyst Handling Services Market

The global catalyst handling services market in 2026 is being reshaped by robotic unloading, dense loading technology, digital bed verification, and lifecycle catalyst management. Competition increasingly centers on turnkey reactor services, inert atmosphere catalyst handling, FCC and hydroprocessing turnaround optimization, and spent catalyst recovery. Leading providers are differentiating through remote-operated systems, real-time loading analytics, precision temperature profiling, and zero-incident safety frameworks, helping refiners extend catalyst run length, reduce downtime, and improve ROI. Rising refinery modernization across Asia, the Middle East, and North America, combined with stricter safety and decarbonization mandates, is accelerating demand for advanced catalyst loading, unloading, screening, and activation services worldwide.

Robotic unloading and dense loading leadership from CR3 Group

CR3 Group leads the 2026 catalyst handling services market as a one-stop provider across Asia and the Middle East, combining robotics with turnkey reactor maintenance. Its Rover remotely operated vehicle sets a new safety benchmark by eliminating confined-space entry during catalyst unloading. The proprietary CR3 Dense Loader remains the gold standard for achieving uniform catalyst beds, preventing channeling and extending hydroprocessing run length. CR3 delivers blind-to-blind solutions covering mechanical works, internal repairs, catalyst activation, and startup support. Strategically, the company is scaling SMART Systems Integration, including its Catalyst Loading Tracker platform, enabling refinery managers to monitor real-time bed density and loading progress for optimized turnaround performance.

Safety-first dense catalyst systems powered by Mourik

Mourik enters 2026 as a global innovator in environmentally responsible catalyst handling, with strong operations across Europe and the Americas. Its MIDC dense loading system delivers high-precision reactor filling while minimizing catalyst attrition, a critical requirement for fixed-bed units. Mourik’s CatSpider remote-controlled suction arm dramatically reduces catalyst removal time in large reactors. In parallel, the company intensified its decarbonization partnership with Huntsman, deploying hydrogen-powered equipment and zero-emission job sites. Mourik’s strategy centers on uncompromising safety behavior, supported by AR-enabled training programs designed to eliminate incidents while improving turnaround efficiency and customer satisfaction.

GCC catalyst handling dominance driven by AnabeeB

AnabeeB is the dominant catalyst handling contractor in the GCC, serving Saudi Aramco and regional energy majors with advanced inert-atmosphere capabilities. The company expanded its vacuuming fleet through 2025–2026, adding high-capacity liquid-ring and dry-vane systems to support refinery expansions. AnabeeB specializes in pyrophoric catalyst handling under nitrogen blankets, using life-support systems and lockable safety helmets. It is a primary contractor for FCC and CCR units, integrating internal inspections with catalyst change-outs. Its 2026 strategy focuses on regional modernization, training local technicians in robotic handling while strengthening local-content delivery across Middle Eastern mega-refineries.

Global rapid-response catalyst lifecycle management by Cat Tech

Cat Tech differentiates itself as a pure-play catalyst handling specialist with global rapid-response teams and full lifecycle catalyst management. The company oversees materials from manufacturer dispatch through onsite loading to final disposal or precious metal reclamation. In late 2025, Cat Tech completed a record European refinery turnaround using High-Speed Gravity Unloading, cutting schedules by 48 hours. Its portable screening units enable real-time segregation of reusable catalyst from fines, reducing replacement costs. For 2026, Cat Tech is expanding spent catalyst handling, partnering with recyclers to recover platinum, palladium, and molybdenum, advancing waste valorization across refinery operations.

Precision loading and thermal intelligence from Daily Thermetrics (Catmasters)

Daily Thermetrics, through its Catmasters division, defines the 2026 precision loading segment with advanced thermal analytics. Its CatTracker® system delivers ultra-high-density temperature profiling, allowing operators to assess catalyst bed health during loading and activation. The newly introduced Hyperloader™ integrates dense loading with real-time temperature verification, ensuring perfect catalyst distribution aligned to reactor thermal profiles. Daily Thermetrics’ core strength lies in thermal intelligence, using spectroscopic analysis to validate catalyst quality before sealing reactors. Its 2026 focus is optimizing ROI, helping refiners extend catalyst life by up to 10–15% through superior temperature management and loading accuracy.

Southeast Asia clean fuels catalyst services from CR Asia

Operating under the CR3 transformation, CR Asia remains a key specialist in Southeast Asian catalyst change-outs, particularly for hydrocracking and reforming units supporting clean fuels mandates. In January 2026, it completed full integration into CR3 Group, consolidating digital assets and safety protocols. The company opened a new catalyst storage and logistics hub in Thailand, enabling rapid equipment deployment during emergency shutdowns. CR Asia maintains long-term multi-site contracts with Petronas and Shell, providing stable revenue and continuous operational data. Its strength lies in executing complex regional turnarounds while supporting lower-sulfur fuel production across ASEAN markets.

United States: Refinery Density, SAF Expansion, and AI-Driven Predictive Maintenance Elevate Catalyst Handling Demand

The United States catalyst handling services market is structurally anchored in its extensive refinery network and tightening environmental compliance landscape. As of January 2025, the U.S. Energy Information Administration reported 132 operable petroleum refineries with a combined atmospheric crude oil distillation capacity of approximately 18.42 million barrels per calendar day. This scale directly translates into recurring demand for hydrotreating catalyst unloading, hydrocracking catalyst change-outs, reactor dense loading, and turnaround management services across the Gulf Coast and Midwest refining corridors.

Regulatory modernization is intensifying service frequency. Updated 2024–2025 air quality standards from the U.S. Environmental Protection Agency and enhanced TSCA Section 5 reporting requirements have accelerated catalyst replacement cycles, especially for sulfur recovery and aromatics reforming units. Simultaneously, OSHA’s 2025 reinforcement of Process Safety Management (PSM) protocols has driven adoption of life-support systems and specialized breathing apparatus for pyrophoric catalyst handling in nitrogen-rich environments. Domestic providers such as Catalyst Handling Resources and Zep Inc. have expanded Gulf Coast service footprints to support a 68% rise in specialty chemical sales reported in late 2025. U.S. facilities are also pioneering AI-driven predictive analytics to monitor catalyst bed pressure drops and temperature profiles, reducing unplanned downtime by up to 15% . The pivot toward Sustainable Aviation Fuel (SAF) is another catalyst handling driver; Neste is scaling U.S.-based renewable diesel capacity to 6.8 million tons annually by 2027, requiring specialized bio-catalyst loading and regeneration expertise.

India: Refining Capacity Doubling, PESO Safety Mandates, and Tube Inserts Optimization Drive Service Intensity

India is emerging as one of the fastest-growing catalyst handling services markets, underpinned by aggressive refining expansion targets and evolving regulatory oversight. According to the Press Information Bureau, India aims to more than double its oil refining capacity to 8 million barrels per day by 2025–2026. This expansion translates into substantial growth in catalyst loading, unloading, screening, and regeneration contracts across public and private refineries.

In July 2025, Petroval showcased its proprietary Tube Inserts technology at the Global Refining & Petrochemicals Congress in Delhi, targeting enhanced reactor performance and optimized catalyst distribution in hydroprocessing units. Regulatory tightening under the GCR (Amendment) Rules 2025, overseen by the Petroleum & Explosive Safety Organisation, has introduced stricter guidelines for hazardous catalyst storage and handling within petrochemical complexes. To accommodate a projected 35% refining capacity increase by 2030, Indian state-run refineries are installing automated catalyst screening and segregation systems to minimize material loss during regeneration cycles. Adoption of BizSAFE- and MASE-aligned safety certifications reflects alignment with international operational standards in high-risk shutdown environments. Additionally, the government’s Mission Anveshan hydrocarbon exploration push is increasing demand for specialized reforming and synthesis gas catalyst handling across upstream and downstream installations.

Finland: Waterflood Catalyst Unloading and Sub-Zero Engineering Redefine Nordic Safety Benchmarks

Finland represents a specialized, innovation-driven segment within the Nordic catalyst handling services landscape. In 2025, Mourik completed a landmark project for a major Finnish petrochemical facility, deploying the “Waterflood” catalyst unloading technique to comply with the client’s strict “No Nitrogen” entry policy. This method provides a non-inert alternative for spent catalyst removal, reducing spontaneous combustion risk and setting a new safety benchmark for fixed-bed reactor servicing.

Cold-weather engineering remains a defining technical differentiator. Finnish contractors have developed winter-hardened vacuum trucks and specialized waterflood hoppers capable of operating in sub-zero temperatures without freezing or compromising catalyst structural integrity. Finland’s push toward bio-fermented C6 chains and circular fatty acid production has also created niche demand for handling sensitive bio-catalysts in low-carbon chemical plants. The Finnish case is increasingly referenced globally as a model for non-inert reactor entry and sustainable catalyst handling under extreme climatic conditions.

Saudi Arabia: Robotic Reactor Solutions and Vision 2030 Safety Mandates Transform Turnaround Services

Saudi Arabia’s catalyst handling services market is expanding in line with its integrated refinery-petrochemical complex strategy. Anabeeb remains a dominant regional player, leveraging collaborations with CR Asia and TubeMaster to deliver turnkey brownfield construction and turnaround solutions across GCC facilities.

By late 2024, major Saudi plants had deployed fully automated catalyst handling systems, reducing manual intervention in hazardous reactor environments. The introduction of “Rover” robotic solutions for unloading extra-large reactors has significantly enhanced throughput and minimized confined-space risk. Strategic investments in localized safety training centers align with Vision 2030 objectives, ensuring contractor compliance with high industrial safety standards while building domestic technical capacity. Large-scale turnaround schedules in hydrocracking and residue upgrading units continue to sustain robust demand for advanced catalyst dense loading and robotic unloading services.

Thailand: Blind-to-Blind Change-Outs and Regional Dense Loading Leadership Anchor APAC Operations

Thailand functions as a regional logistics and technical command center for catalyst handling services in Southeast Asia. CR3 Group achieved a technical milestone in late 2024 by completing a complex catalyst change-out using a “blind-to-blind” methodology, enabling earlier-than-expected unit restart and setting a world record for turnaround speed.

Robotic unloading has become standard practice across Southeast Asian hydrotreater projects, with the Rover remotely operated vehicle eliminating the need for personnel entry into inert atmospheres. CR3’s Dense Loading technology was deployed in Singapore for a 5.4-meter diameter diesel hydrotreater, exceeding uniformity parameters despite adverse weather. Thailand serves as the logistical base for the region’s largest fleet of catalyst handling equipment, supporting refinery shutdowns across Singapore, Vietnam, and Indonesia. This regional integration underpins Thailand’s leadership in high-efficiency, safety-driven catalyst loading operations.

China: Double-Helix Reactor Design and Segmented Radial Loading Enhance Cost-Effective Uniformity

China’s catalyst handling services market is scaling alongside a planned 5% increase in refining capacity through 2025, reinforcing its position as the world’s largest energy consumer. Technical research has shifted toward Data-Driven Intelligent Regulation for fixed-bed reactors, emphasizing the deployment of double-helix distributors to reduce radial density fluctuations in aromatics isomerization and reforming units.

For extra-large radial reactors exceeding 4 meters in diameter, Chinese service providers are implementing segmented radial loading combined with real-time ultrasonic density monitoring, achieving bed uniformity within ±1.2% . Benchmark studies indicate that domestic double-helix systems deliver performance comparable to Western radial sparger technologies while reducing equipment costs by approximately 20% . This cost-effectiveness, combined with intelligent monitoring, positions China as a competitive provider of advanced catalyst loading and unloading solutions within Asia-Pacific and emerging export markets.

Catalyst Handling Services Market Report Scope

Catalyst Handling Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1155.5 Million

|

|

Market Size (2034)

|

$1985.6 Million

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Service Type (Catalyst Loading, Catalyst Unloading, Catalyst Screening and Transport, Catalyst Regeneration and Recycling, Inert Entry Life Support, On Site Activation), By Technology Type (Robotic and Automated Handling, Conventional Handling, Semi Automated Systems), By Reactor Type (Hydroprocessing, Fluid Catalytic Cracking, Tubular Reforming, Ammonia and Methanol Converters, Alkylation and Isomerization), By End Use Industry (Petroleum Refining, Petrochemicals, Chemical Manufacturing, Pharmaceuticals and Fine Chemicals, Environmental and Emission Control)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Anabeeb, Mourik, Cat Tech International, Johnson Matthey, BASF SE, CR3, Technivac, Catalyst Handling Resources, Buchen ICS, Kanooz Industrial Services, Axens, Sinopec Shanghai Catalysts, Dickinson Group, Albemarle, Topsoe

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Catalyst Handling Services Market Segmentation

By Service Type

- Catalyst Loading

- Catalyst Unloading

- Catalyst Screening and Transport

- Catalyst Regeneration and Recycling

- Inert Entry Life Support

- On Site Activation

By Technology Type

- Robotic and Automated Handling

- Conventional Handling

- Semi Automated Systems

By Reactor Type

- Hydroprocessing

- Fluid Catalytic Cracking

- Tubular Reforming

- Ammonia and Methanol Converters

- Alkylation and Isomerization

By End Use Industry

- Petroleum Refining

- Petrochemicals

- Chemical Manufacturing

- Pharmaceuticals and Fine Chemicals

- Environmental and Emission Control

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Catalyst Handling Services Industry

- Anabeeb

- Mourik

- Cat Tech International

- Johnson Matthey

- BASF SE

- CR3

- Technivac

- Catalyst Handling Resources

- Buchen ICS

- Kanooz Industrial Services

- Axens

- Sinopec Shanghai Catalysts

- Dickinson Group

- Albemarle

- Topsoe

*- List not Exhaustive