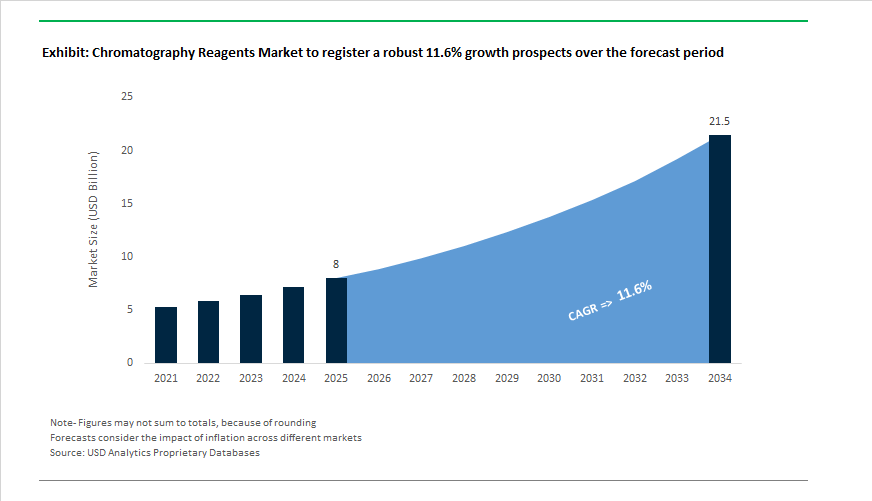

Chromatography Reagents Market Outlook 2025–2034: $8 Billion to $21.5 Billion at 11.6% CAGR Fueled by Biopharma Purification and Regulated Testing Expansion

The global Chromatography Reagents Market is projected to expand from $8 billion in 2025 to $21.5 billion by 2034, registering a strong CAGR of 11.6%. Growth is being driven by escalating demand for high-purity chromatography solvents, affinity resins, ion-exchange reagents, size-exclusion media, and certified reference materials across pharmaceutical, biopharmaceutical, environmental, food safety, and geochemical laboratories. Increasing regulatory scrutiny in drug manufacturing, biologics purification, and clinical diagnostics is intensifying reliance on validated chromatography reagents compatible with advanced HPLC, UHPLC, GC, LC-MS, and SFC platforms.

Market consolidation accelerated in 2024–2026, reshaping competitive positioning in chromatography consumables and reagent portfolios. In November 2024, Agilent Technologies restructured into three market-centric divisions, strengthening distribution channels for chromatography consumables under Agilent CrossLab. In 2024, Sartorius completed the acquisition of Novasep’s chromatography division, integrating high-performance resin and downstream purification technologies into its bioprocessing portfolio. In October 2025, Merck KGaA signed an agreement to acquire JSR Life Sciences’ chromatography business, including the Amsphere™ A3 Protein A resin platform targeting monoclonal antibody purification. In February 2026, Waters Corporation finalized a landmark $10 billion-plus combination with BD’s Biosciences and Diagnostic Solutions businesses, significantly expanding its regulated testing reagent footprint. These transactions reflect a clear strategic pivot toward biologics purification, high-volume diagnostic reagents, and vertically integrated chromatography ecosystems.

Product innovation remains central to competitive differentiation. In September 2025, Agilent introduced the Altura line of inert HPLC columns engineered to reduce non-specific adsorption of oligonucleotides and therapeutic peptides, directly enhancing the performance of high-purity chromatography reagents. In the same month, Phenomenex expanded its Biozen dSEC-1 size exclusion chromatography columns optimized for aggregate analysis of midsize biotherapeutics using inert silica-based matrices. Waters launched its proprietary Charged Aerosol Detector in November 2025, designed for seamless integration with the Empower Chromatography Data System to accurately quantify non-UV absorbing analytes such as lipids and excipients. Shimadzu debuted new i-Series integrated HPLC systems in September 2025 featuring automatic reagent clog detection and solvent contamination diagnostics, reducing reagent waste and improving laboratory efficiency. These innovations directly reinforce reagent utilization rates in complex analytical workflows.

Sustainability, traceability, and analytical standardization are emerging as structural growth pillars. Thermo Fisher Scientific introduced CertiQ GC Secondary Reference Standards in August 2025, traceable to NIST and USP/EP primary standards and packaged with moisture-controlled AcroSeal™ technology to preserve reagent integrity. In September 2025, Agilent earned top-level My Green Lab certification for its refurbishment centers, supporting its Sustainable Science initiative and ACT Eco-Label transparency for chromatography solvents and reagents. Shimadzu consolidated European reagent kit operations in April 2025, forming Shimadzu Chemistry and Diagnostics SAS to accelerate LC-MS and MALDI-MS reagent distribution. In February 2026, AnalytiChem launched high-purity Certified Reference Materials for critical minerals analysis, supporting lithium, cobalt, and rare earth research. These developments indicate sustained double-digit growth potential through 2034, anchored in biologics purification demand, diagnostic reagent expansion, and laboratory automation-driven reagent optimization.

Chromatography Reagents Market Trends and Opportunities

Rapid Expansion of LC-MS Grade Reagents Driven by High-Resolution Trace Analytics and Biotherapeutic Characterization

One of the most defining trends in the chromatography reagents market is the surging adoption of LC-MS-grade reagents engineered for sub-parts-per-billion metal ion purity and minimal non-volatile residues. This is closely linked to the global shift toward High-Resolution Mass Spectrometry (HRMS) and LC-MS/MS workflows, which have become the gold standard for impurity profiling and biomarker discovery across pharmaceutical, biopharmaceutical, food safety, and environmental testing laboratories.

In 2025, the mass spectrometry segment is poised for major expansion as regulatory bodies mandate ultra-sensitive detection of contaminants such as N-Nitrosamines, PFAS, endocrine disruptors, and extractables/leachables. Because LC-MS systems are acutely sensitive to baseline noise and ion suppression, laboratories are increasingly sourcing certified LC-MS-grade solvents, ultrapure mobile phase additives, and trace-level reagents to ensure repeatable molecular identification, structural elucidation, and validated impurity profiling.

Biopharmaceuticals are a major adoption catalyst, especially due to their reliance on Multi-Attribute Monitoring (MAM) platforms. MAM techniques combine HRMS and LC-MS/MS to monitor multiple CQAs in a single analytical run, requiring consistent purity-validated reagents across multi-site QC laboratories to meet global compliance requirements.

Regulatory-Driven Shift Toward Green Chromatography Reagents and Solvent Substitutes

A second critical trend is the accelerated move toward green chromatography reagents due to environmental regulatory reform, worker-safety mandates, and corporate ESG reporting pressures.

Under the Toxic Substances Control Act (TSCA), the U.S. EPA finalized a ban on most commercial uses of Methylene Chloride (DCM) in April 2024, requiring laboratories to transition toward alternative solvents. By late 2025, ethyl acetate/ethanol systems, heptanes, and dimethyl carbonate (DMC) have emerged as the primary substitutes, in alignment with Green Analytical Chemistry (GAC) principles. Corporate investments further validate this trend. In April 2025, Amcor and Anaïs Ventures led a US$14 million funding round in Bloom Biorenewables to accelerate bio-based molecular solvent technologies, illustrating a broader shift toward bio-derived substitutes replacing acetonitrile (ACN) and other legacy petro-based materials. Beyond cost and emissions, sustainability is increasingly linked to procurement eligibility, driven by the EU 2025 Circular Economy and hazardous waste reduction mandates, which are compelling laboratories to reengineer their entire reagent sourcing strategies.

Specialized Chromatography Reagents for Cell & Gene Therapy (CGT) Potency and Identity Testing

The most significant high-margin commercial opportunity lies in reagents used for cell and gene therapy (CGT) potency assays, identity verification, and quality control analytics. With rapid commercialization of CAR-T and TCR-T therapies, regulators are enforcing lifecycle-based potency validation across every lot release.

By 2025, the potency testing segment is expanding at double-digit rates, fueled by CGT programs requiring HPLC-based glycan profiling, charge-variant analysis for viral vectors, and mechanism-of-action reflective analytics. Because safety, dose consistency, and molecular-level identity must be proven before shipment, HPLC and Mass Spectrometry remain the fastest-growing analytical methods, pushing labs to secure pre-validated, globally compliant reagents.

Automated Purification Kits for mRNA and Plasmid DNA – Transition from Bulk Solvents to Plug-and-Play Reagent Kits

Automation is redefining reagent consumption models. The market is shifting from manual solvent-based workflows to GMP-compliant automated purification platforms, unlocking exponential reagent demand in pre-packed columns, buffer kits, and turnkey purification bundles.

A major inflection point occurred in June 2023, when GenScript Biotech launched the AmMag Quatro, a fully automated magnetic bead system capable of processing 24 samples within two hours. By 2025, automation-ready solutions are becoming the market standard. The Automated Nucleic Acid Extraction Market itself is projected to exceed US$6.5 billion in 2025, and a large share of this growth is attributable to Product-in-a-Box chromatography kits that include pre-formulated reagents, enzymes, and validated columns. These enable manufacturers to meet ICH Q6B molecular purity guidelines, minimize contamination events, and ensure reproducibility across decentralized manufacturing sites.

Chromatography Reagents Market Share and Segmentation Insights

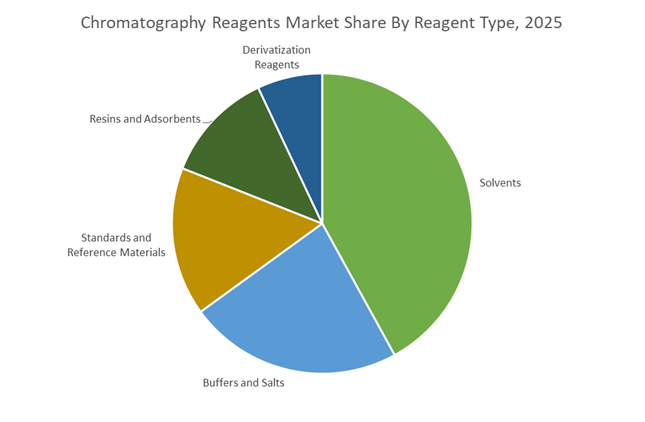

Reagent Type Dynamics: Solvents Lead Volume Demand as Bioprocessing Elevates Resin Consumption

Solvents dominate the Chromatography Reagents Market with 42% share in 2025, underpinned by their indispensable role as mobile phases in HPLC and GC workflows using acetonitrile, methanol, and ultrapure water. Despite laboratory efforts to minimize solvent usage, global sample throughput sustains strong revenue contribution. Buffers and salts follow closely, supporting pH stability and peak resolution in reverse-phase chromatography, particularly for biologics and biosimilars. Standards and reference materials form a high-value segment, driven by stringent pharmacopeial requirements and precision testing across pharmaceuticals, food safety, and forensic toxicology. Resins and adsorbents are experiencing rising demand from preparative chromatography, fueled by continuous manufacturing and monoclonal antibody production requiring Protein A and ion-exchange media. Derivatization reagents remain niche, serving specialized GC-MS applications such as amino acid profiling and pesticide residue analysis.

Application Breakdown: Pharma and Biotech Lead While Clinical Diagnostics Accelerates Reagent Uptake

Pharmaceutical and biotechnology applications capture about 38% of market share, positioning chromatography as the backbone of drug development, from early-stage impurity profiling to final QC release testing. Expanding pipelines for biologics, mRNA platforms, and small-molecule therapeutics continue to intensify reagent consumption. Clinical research and diagnostics represent the fastest-growing segment, propelled by LC-MS/MS adoption in hospitals for newborn screening, therapeutic drug monitoring, and vitamin assays. Food and beverage testing maintains steady demand amid heightened scrutiny of pesticide residues, mycotoxins, and adulterants. Environmental testing growth is reinforced by regulatory mandates targeting PFAS and trace pharmaceuticals in water systems. Academic and industrial research remains foundational, contributing lower revenue but serving as the innovation incubator for emerging chromatographic techniques and next-generation reagent formulations.

Competitive Landscape of the Chromatography Reagents Market

The Chromatography Reagents Market is led by vertically integrated analytical giants and life science specialists advancing bioprocessing resins, LC-MS mobile phases, green solvents, and smart reagent management systems. Competitive differentiation centers on GLP/GMP-ready consumables, AI-enabled method development, PFAS-free reagent kits, and scalable purification media for biologics and gene therapies. Market leaders are investing heavily in sustainability, digital chromatography workflows, and Asia-Pacific expansion to support pharmaceutical quality control, protein characterization, and next-generation therapeutics, reinforcing the shift toward high-performance, compliant, and automation-ready chromatography ecosystems.

Thermo Fisher delivers end-to-end chromatography ecosystems with smart reagent integration

Thermo Fisher Scientific is a global powerhouse in chromatography reagents, combining high-purity chemicals with its Vanquish and Dionex instrument platforms. Its extensive portfolio includes Hypersil GOLD columns, silylation reagents, and CX1-pH gradient buffers for advanced protein characterization. In June 2025, Thermo launched the Vanquish Charged Aerosol Detector P Series, paired with specialized reagent kits enabling near-universal detection of non-volatile compounds. A key strategic focus is integrating Chromeleon CDS with smart reagent tracking to automate inventory and reduce waste. Thermo’s unmatched vertical integration across reagents, columns, hardware, and software ensures exceptional reproducibility in regulated GLP and GMP laboratories.

Merck accelerates green chromatography with bio-renewable solvents and bioprocessing resins

Operating as MilliporeSigma in North America, Merck leads green chemistry and chromatography resins for biopharmaceutical manufacturing. In late 2025, Merck announced the acquisition of JSR Life Sciences’ chromatography business, expected to close mid-2026, strengthening its position in advanced filtration and next-generation therapy purification. The company is investing over €1.5 billion through 2026 to expand Life Science operations in Ireland and China. Recent innovations include expanding the Cyrene™ solvent line, a bio-renewable alternative to NMP and DMF for mobile phases. Merck projects 3.0 to 3.5% revenue growth in 2026, driven by Process Solutions supplying large-scale pharma resins.

Agilent sets analytical accuracy benchmarks with sustainable LC and GC reagent platforms

Agilent Technologies is the gold standard for analytical accuracy across gas and liquid chromatography, offering InfinityLab solvents and Altura inert HPLC columns optimized for sensitive biotherapeutic testing. In 2025, Agilent introduced the InfinityLab Pro iQ Series, providing real-time reagent status feedback to prevent dry runs and protect sample integrity. Sustainability is central to its strategy, with MyGreenLab ACT EcoLabel 2.0 certification achieved across the Infinity III LC series and consumables. In December 2025, Agilent opened a major India Refurbishment Center, supporting circular economy practices and affordable innovation across Asia-Pacific chromatography laboratories.

Waters expands regulated testing dominance with AI-driven UPLC reagent optimization

Waters Corporation focuses on high-value pharmaceutical and clinical diagnostics testing, dominating the UPLC reagent segment with specialized mobile phase additives that enhance LC-MS sensitivity. In 2025, Waters finalized a transformational combination with Becton Dickinson’s Biosciences and Diagnostic Solutions unit, doubling its total addressable market to roughly USD 40 billion. Its Waters Connect platform now features AI-powered method development kits that automatically select optimal reagent-column combinations for unknown analytes. With exceptional brand loyalty among global pharma manufacturers, Waters remains a default analytical standard for regulatory filings, reinforcing its leadership in compliant chromatography reagent workflows.

Shimadzu advances PFAS-free and intelligent chromatography for Asia-Pacific testing labs

Shimadzu is a pioneer in ultra-fast chromatography with strong penetration in Asian food safety and environmental testing markets. The company recently launched its i-Series with an intelligent Column Management Platform using RFID-tagged reagents and columns to eliminate setup errors. Key offerings include the Ghost Trap DS reagent and filter system that removes mobile-phase impurities to prevent ghost peaks. Shimadzu also leads PFAS analysis, supplying PFAS-free reagent kits aligned with tightening global regulations. Business expansion continues through the Shimadzu Tokyo Innovation Plaza, where custom chromatography reagents are co-developed with biotech startups.

Bio-Rad strengthens biopharma purification with ceramic hydroxyapatite and secure workflows

Bio-Rad Laboratories is a dominant player in protein purification and life science research, anchored by NGC™ chromatography systems and Affinity Resins for monoclonal antibodies and viral vectors. Its CHT™ Ceramic Hydroxyapatite media remains a world-leading reagent for high-resolution purification of antibody-drug conjugates. In 2026, Bio-Rad enhanced ChromLab Software with User Management and Security Edition, enabling 21 CFR Part 11 compliance for biopharma manufacturing. Strategically, Bio-Rad emphasizes its “Concept to Cure” workflow, offering transition kits that allow seamless scaling from 10 ml lab experiments to 100 L process chromatography using identical reagent chemistries.

United States Chromatography Reagents Market: Biopharma Consolidation, PFAS Testing Surge, and Sustainable LC-MS Innovation

The United States Chromatography Reagents Market remains the global growth engine for high-performance liquid chromatography reagents, mass spectrometry-grade solvents, and analytical reference standards. A major catalyst has been industry consolidation. In February 2026, Waters Corporation finalized its $16.8 billion acquisition of BD’s Biosciences and Diagnostic Solutions business, expanding its footprint in single-cell multiomics and clinical flow cytometry, which represented over 59% of its 2025 pharmaceutical-related net sales. This integration materially increases demand for ultra-high-purity LC-MS reagents, buffers, and specialty solvent systems.

In January 2026, Thermo Fisher Scientific reported $44.56 billion in full-year 2025 revenue, with chromatography and laboratory products contributing to 4% year-over-year growth. At HPLC 2025, Agilent Technologies introduced the InfinityLab Pro iQ Series featuring oil-free pumps and MyGreenLab ACT EcoLabel certification, signaling a shift toward sustainable chromatography reagents and eco-optimized solvent systems. U.S. suppliers are also transitioning from helium to hydrogen carrier gases in gas chromatography due to global helium shortages, reshaping reagent formulations and lab infrastructure. Additionally, heightened EPA mandates on PFAS in drinking water have driven rapid adoption of PFAS-specific chromatography reagents for environmental testing, positioning the U.S. as the epicenter of regulatory-driven analytical chemistry demand.

Germany Chromatography Reagents Market: Bioprocessing Resins, GMP Reform, and Continuous Chromatography Adoption

Germany anchors the European Chromatography Reagents Market through its dominance in bioprocessing resins, monoclonal antibody purification, and high-purity buffer systems. In October 2025, Merck KGaA announced a definitive agreement to acquire the chromatography business of JSR Life Sciences, integrating Amsphere A3 and A+ Protein A resins into its portfolio. This move strengthens Germany’s position in next-generation antibody purification and downstream bioprocessing reagents.

In January 2026, Merck reported a strategic pivot toward its Life Science division, prioritizing chromatography resins and buffers aligned with infectious disease and oncology pipelines. Implementation of Commission Implementing Regulation EU 2025/2091 in July 2026 introduces stricter GMP benchmarks for reagents used in medicinal production, increasing demand for validated, pharmaceutical-grade chromatography solvents and columns. German CDMOs are deploying continuous chromatography systems capable of reducing solvent consumption by up to 80% compared to batch processing. Meanwhile, initiatives led by CLIB - Cluster Industrial Biotechnology are advancing bio-based solvent and buffer production, reinforcing Germany’s leadership in sustainable analytical reagents and SFC-grade materials for green hydrogen and e-SAF applications.

China Chromatography Reagents Market: Specialty Chemical Localization and LC-MS Grade Solvent Expansion

China’s Chromatography Reagents Market is rapidly transitioning toward high-end specialty analytical chemicals, targeting 90% self-sufficiency in critical laboratory intermediates by 2026. In September 2025, the Ministry of Industry and Information Technology of China issued the Work Plan for Steady Growth in the Petrochemical and Chemical Industry 2025 to 2026, aiming for over 5% annual industry value-added growth and emphasizing electronic chemicals and high-end polyolefins. These materials serve as feedstocks for next-generation polymer-based chromatography columns and reagent packaging systems.

Expansion at Huizhou Dayawan Petrochemical Industrial Park includes dedicated production lines for LC-MS grade acetonitrile and methanol, reducing reliance on North American imports and stabilizing domestic solvent supply chains. Updated Good Laboratory Practice standards from the National Medical Products Administration for 2026 mandate stricter batch consistency for imported and domestic chromatography reagents. Chinese firms are also developing AI-driven impurity detection software to streamline chromatographic quality control of large-scale solvent production. Coordinated fiscal incentives from seven ministries support green technology adoption and digital manufacturing for analytical chemicals, positioning China as a high-volume yet increasingly high-purity supplier within the global chromatography reagents market.

India Chromatography Reagents Market: PLI Incentives, Generic Export Growth, and USP-Grade Standard Expansion

India’s Chromatography Reagents Market is benefiting from structural expansion in pharmaceutical exports and government-backed advanced chemistry incentives. In December 2025, Agilent Technologies opened its first India Refurbishment Center, improving access to high-performance chromatography equipment and associated reagents for emerging laboratories. The Indian pharmaceutical sector’s cumulative $22 billion FDI inflow as of 2024 has directly increased demand for USP-grade chromatography standards and validated analytical reagents.

In 2025, Thermo Fisher Scientific introduced CertiQ secondary GC standards in India, offering traceability to United States Pharmacopeia lots at lower cost, supporting domestic generic manufacturers. The Production Linked Incentive Scheme for Advanced Chemistry version 2.0 has catalyzed giga-scale investments in high-purity intermediates and laboratory solvent manufacturing. A 15% revenue jump for firms such as Akums Drugs in Q3 FY26, driven by EU-approved generics, has elevated demand for analytical method validation reagents. Telangana’s positioning as a TechBio Powerhouse under BioAsia 2026 further strengthens regional manufacturing of bioprocessing buffers and filtration media, enhancing India’s export competitiveness in standardized chromatography reagents.

Japan Chromatography Reagents Market: UHPLC Compatibility, Digital Twin Labs, and Chiral Stationary Phase Dominance

Japan continues to lead the Chromatography Reagents Market through innovation in high-resolution detectors, UHPLC-compatible solvents, and chiral stationary phase production. In January 2025, Shimadzu Corporation launched the Brevis GC-2050, a compact gas chromatograph engineered for reduced reagent consumption and real-time CO2 visualization. In August 2025, Shimadzu introduced the LCMS-8065XE equipped with proprietary UF Technologies for ultra-fast PFAS detection, reinforcing Japan’s strength in healthcare and environmental chromatography reagents.

Japan is advancing Digital Twin laboratory management systems, with WuXi Biologics deploying the PatroLab simulation platform to model chromatography runs and optimize reagent consumption prior to physical analysis. Japanese manufacturers are aligning with Green Transformation strategies, producing analyzers such as the TOC-1000e S for ultrapure semiconductor water testing, which requires ultra-high-sensitivity reagents. A renewed 15-year collaboration between Agilent Technologies and Monash University in late 2025 supports bio-based stationary phase research across Asia. Japan also maintains global leadership in chiral stationary phases, holding a dominant share in HPLC column and stereoisomeric drug reagent kits, reinforcing its strategic position in precision analytical chemistry.

Chromatography Reagents Market Report Scope

Chromatography Reagents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8 Billion

|

|

Market Size (2034)

|

$21.5 Billion

|

|

Market Growth Rate

|

11.6%

|

|

Segments

|

By Reagent Type (Solvents, Buffers and Salts, Derivatization Reagents, Resins and Adsorbents, Standards and Reference Materials), By Technique (Liquid Chromatography, Gas Chromatography, Supercritical Fluid Chromatography, Thin-Layer Chromatography), By Application (Pharmaceutical and Biotechnology, Food and Beverage, Environmental Testing, Clinical Research and Diagnostics, Academic and Industrial Research)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermo Fisher Scientific Inc., Merck KGaA, Agilent Technologies, Inc., Waters Corporation, Shimadzu Corporation, Bio-Rad Laboratories, Inc., Sartorius AG, Avantor, Inc., Honeywell International Inc., PerkinElmer, Inc., Restek Corporation, Tosoh Corporation, Repligen Corporation, Trajan Scientific and Medical, Phenomenex, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chromatography Reagents Market Segmentation

By Reagent Type

- Solvents

- Acetonitrile

- Methanol

- Water (HPLC and LC-MS Grade)

- Ethanol

- Isopropanol

- Buffers and Salts

- Ammonium Acetate

- Phosphate Buffers

- Formic Acid

- Trifluoroacetic Acid

- Derivatization Reagents

- Silylation Reagents

- Acylation Reagents

- Alkylation Reagents

- Resins and Adsorbents

- Protein A Resins

- Ion-Exchange Resins

- Silica Gel

- Alumina

- Standards and Reference Materials

- Analytical Standards

- Isotopically Labeled Standards

By Technique

- Liquid Chromatography

- Gas Chromatography

- Supercritical Fluid Chromatography

- Thin-Layer Chromatography

By Application

- Pharmaceutical and Biotechnology

- Food and Beverage

- Environmental Testing

- Clinical Research and Diagnostics

- Academic and Industrial Research

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chromatography Reagents Industry

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Agilent Technologies, Inc.

- Waters Corporation

- Shimadzu Corporation

- Bio-Rad Laboratories, Inc.

- Sartorius AG

- Avantor, Inc.

- Honeywell International Inc.

- PerkinElmer, Inc.

- Restek Corporation

- Tosoh Corporation

- Repligen Corporation

- Trajan Scientific and Medical

- Phenomenex, Inc.

*- List not Exhaustive