Coatings Raw Materials Market Size, Specialty Chemical Innovation, and Circular Feedstock Transition

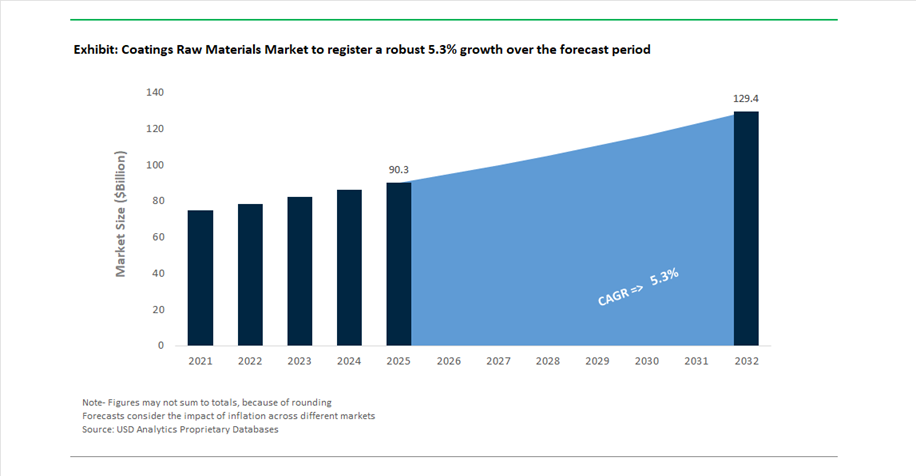

The global coatings raw materials market was valued at $90.3 billion in 2025 and is projected to grow at a CAGR of 5.3% between 2025 and 2032, reaching $129.6 billion by 2032. This growth is driven by rising demand across architectural coatings, automotive OEM and refinish, industrial coatings, packaging, and high-performance specialty applications, where raw materials such as resins, pigments, additives, solvents, and fillers determine overall coating performance, durability, and sustainability.

A major structural shift in the market is the transition toward circular, bio-based, and low-carbon raw materials, as manufacturers respond to increasingly stringent environmental regulations and decarbonization targets. Traditional petrochemical-derived inputs are gradually being complemented or replaced by recycled feedstocks, renewable intermediates, and mass-balanced materials, enabling coatings producers to reduce lifecycle emissions while maintaining performance characteristics. This transition is particularly critical in automotive, construction, and packaging sectors, where sustainability has become a key procurement criterion.

Technological advancements are also redefining raw material innovation. The development of high-performance resins, specialty crosslinkers, functional additives, and advanced pigments is enabling coatings with enhanced properties such as UV resistance, corrosion protection, thermal stability, and aesthetic versatility. In parallel, the integration of digital tools and AI-driven process optimization is improving production efficiency, supply chain resilience, and product customization capabilities across the coatings value chain.

Emerging applications such as electric vehicles (EVs), 3D printing, and advanced infrastructure materials are further driving demand for specialized raw materials. These applications require coatings with superior adhesion, lightweight characteristics, and resistance to extreme environmental conditions, reinforcing the importance of continuous innovation in raw material chemistry.

AI-Driven Chemical Optimization, Strategic Capacity Expansion, and Sustainable Material Innovation Reshaping the Supply Chain

The coatings raw materials market is undergoing rapid transformation through digitalization, strategic acquisitions, and sustainability-focused innovation initiatives. In January 2026, Dow launched its “Transform to Outperform” initiative, targeting a $2 billion improvement in operational EBITDA through the use of AI and automation to optimize production and distribution of coating resins and solvents. This initiative reflects the growing importance of data-driven manufacturing and supply chain efficiency in a volatile chemical market.

Strategic acquisitions are strengthening global production networks for critical raw materials. Covestro’s acquisition of Vencorex production sites (August 2025, expected closure in H1 2026) significantly enhances its capacity for HDI derivatives, essential for producing high-performance, weather-resistant polyurethane coatings. Additionally, Covestro’s €1.17 billion partnership with XRG (December 2025) provides financial flexibility to accelerate R&D in circular resins and digitalized supply chains, reinforcing its long-term sustainability strategy.

Sustainability-led innovation is a defining theme across the market. Solvay’s circular silica strategy (January 2026) involves converting production to ISCC+ certified waste-based raw materials, enabling over half of its regional capacity to shift toward circular inputs. Similarly, Eastman’s Kingsport methanolysis facility, which doubled recycled content production in 2025, is advancing molecular recycling technologies that provide sustainable intermediates for coatings without compromising performance.

Material innovation is also expanding into high-growth specialty segments. Arkema’s 2026 strategic roadmap emphasizes bio-attributed resins and advanced materials such as Kynar® PVDF and Rilsan® polyamides, targeting applications in EV battery coatings and 3D printing. Meanwhile, Evonik’s focus on specialty crosslinkers and advanced additives reflects increasing demand for high-performance coatings in technologically demanding applications, despite pricing pressures in commodity segments.

Collaborative innovation is further accelerating the development of next-generation materials. Clariant’s joint venture with FUHUA (November 2025) focuses on halogen-free flame retardant additives, addressing growing safety requirements in architectural coatings and EV-related applications. At the same time, BASF Coatings’ “DRIVING THE PROXY” collection (October 2025) showcases how renewable and recycled raw materials are being integrated directly into coating formulations, leveraging advanced pigment technologies to enhance both sustainability and visual performance.

Bio-Based Feedstock Traceability Becomes a Core Compliance Requirement

The raw materials segment of the coatings industry is undergoing a structural shift toward supply chain transparency, driven by the enforcement phase of the EU Deforestation Regulation (EUDR) 2023/1115. With applicability now active for most operators and full compliance deadlines extending into mid-2026 for smaller enterprises, the regulation directly impacts a wide spectrum of bio-based inputs—including soybean oil-derived alkyds, tall oil derivatives, natural rubber additives, and palm-based surfactants.

The defining feature of EUDR is its geolocation-based due diligence requirement, which mandates that companies provide precise coordinates of the land where raw materials were sourced. This fundamentally alters procurement models, shifting them from transactional sourcing to traceable, digitally verifiable supply chains. For coatings manufacturers, this introduces new operational layers involving satellite monitoring, blockchain-based traceability systems, and supplier-level environmental audits.

The regulation’s retroactive cutoff date—prohibiting materials linked to deforestation post-December 2020—has immediate implications for feedstock availability. Certain high-risk sourcing regions for palm oil and soy have already been categorized under stricter inspection regimes, resulting in higher rejection rates and longer import clearance cycles. This is forcing formulators to diversify sourcing strategies, including a pivot toward regionally certified or synthetic alternatives.

Financial exposure is also non-trivial. Penalties of at least 4% of EU turnover for non-compliance elevate EUDR from a sustainability initiative to a material financial risk. Consequently, procurement and regulatory functions are becoming tightly integrated, with raw material selection increasingly influenced by compliance feasibility rather than cost alone.

Energy-Constrained Production Reshaping Global Supply Chains

China’s “Dual Control” policy on energy consumption has entered a decisive enforcement phase, significantly influencing the global supply of key coating raw materials such as titanium dioxide (TiO₂) and petrochemical resins. The policy, aligned with the final stage of the 14th Five-Year Plan, targets both energy intensity and total consumption, creating structural pressure on energy-intensive chemical manufacturing.

One of the most immediate impacts has been the systematic shutdown of inefficient sulfate-process TiO₂ plants, which historically dominated lower-cost production. The transition toward cleaner chloride-process facilities, while environmentally favorable, is capital-intensive and time-consuming, resulting in short-term supply tightness and price volatility.

Simultaneously, regional mandates—such as reduced coal consumption in the Yangtze River Delta—are accelerating the integration of alternative energy sources into chemical production. Newly commissioned resin plants are increasingly designed as “green factories,” incorporating solar and wind-powered thermal systems to meet regulatory benchmarks. This transition is not seamless; during facility upgrades, supply disruptions of 10%–15% have been observed for specialty monomers and intermediates, particularly affecting high-performance coatings segments.

The broader implication is a reconfiguration of global supply chains. Buyers are increasingly adopting a multi-origin sourcing strategy, reducing dependence on single-country supply hubs. This includes nearshoring initiatives in Southeast Asia, India, and Eastern Europe, as well as strategic inventory buffering for critical raw materials. The result is a shift from cost-optimized sourcing to resilience-oriented procurement.

Emergence of Isocyanate-Free Resin Chemistry as a Regulatory and Performance Breakthrough

Non-Isocyanate Polyurethane (NIPU) resins are transitioning from laboratory-scale innovation to commercial viability, driven by tightening regulatory restrictions on isocyanates under frameworks such as REACH and occupational safety mandates. These resins are synthesized through the reaction of cyclic carbonates with amines, forming hydroxyurethane linkages without the need for toxic isocyanate intermediates.

Recent advancements have addressed historical performance gaps, with next-generation NIPU systems achieving mechanical strength and thermal properties comparable to conventional polyurethane coatings. This parity is critical, as it enables substitution without compromising end-use performance in demanding applications such as industrial coatings and automotive finishes.

From an environmental perspective, the advantages are substantial. Solvent-free NIPU formulations can reduce VOC emissions by up to 90%, aligning with the strictest regulatory thresholds in Europe and North America. Additionally, innovations in catalysis have lowered curing temperatures below 80°C, reducing energy consumption in industrial coating lines by approximately 20%.

Feedstock flexibility further enhances their strategic value. The ability to incorporate renewable inputs such as cashew nut shell liquid (CNSL) or soybean derivatives enables partial decoupling from petrochemical supply chains while improving carbon footprint metrics. As regulatory pressure on toxic intermediates intensifies, NIPU chemistry is positioned as a next-generation platform technology rather than a niche alternative.

Circular Economy Integration at the Binder Level

The integration of recycled materials into coatings is evolving beyond packaging into core formulation components, particularly through the adoption of post-consumer recyclate (PCR) resins. Advances in chemical recycling technologies now enable the depolymerization of PET and HDPE waste into high-purity intermediates suitable for polyester and alkyd binder production.

This shift is being driven by both regulatory and corporate sustainability commitments. Major coatings manufacturers have set targets to incorporate at least 25% PCR content in binders and packaging by the 2025–2026 timeframe, creating a rapid scale-up in demand for recycled feedstocks.

From a performance standpoint, earlier limitations related to inconsistency and quality variability have largely been mitigated. Modern PCR-derived resins achieve up to 98% consistency in key parameters such as viscosity and color, enabling their use in premium architectural coatings rather than being confined to low-end applications.

The environmental impact is also quantifiable. The use of PCR-based polyester resins can reduce the cradle-to-gate carbon footprint of coating binders by up to 40%, making them a critical lever for companies targeting Scope 3 emissions reductions.

This development signals a deeper transformation in the coatings value chain, where circularity is no longer an auxiliary consideration but a core design parameter in raw material selection and formulation strategy.

Resins & Binders Dominate Coatings Raw Materials Market with 38% Share as the Core Film-Forming Backbone

Raw Material Type Analysis: High-Value Resin Systems Drive Performance and Cost Structure

Resins and binders hold a leading 38.0% share of the coatings raw materials market in 2025, serving as the fundamental film-forming backbone that determines coating performance across all applications. These materials—ranging from acrylics, epoxies, polyurethanes, alkyds, and polyesters—govern critical properties such as adhesion, chemical resistance, durability, flexibility, and mechanical strength. Accounting for 20–60% of total formulation weight and priced 2x–5x higher than pigments, resins represent the largest cost component for coating manufacturers. Acrylic resins alone contribute approximately 35% of resin demand, driven by architectural and automotive coatings, while epoxies and polyurethanes dominate protective and high-performance coatings segments. A key 2025 trend is the shift toward bio-based resins, including bio-acrylics, plant-derived polyols, and glycerin-based epoxies, supporting sustainability goals and reducing carbon footprint. This evolution reinforces resins’ critical role in the global coatings raw materials market.

Architectural & Decorative Sector Leads with 42% Share Driven by Massive Global Paint Consumption

End-Use Sector Analysis: High-Volume Paint Production Fuels Raw Material Demand

The architectural and decorative segment accounts for 42.0% of the coatings raw materials market in 2025, driven by the immense scale of global paint production exceeding 40 billion liters annually. This segment encompasses interior and exterior wall paints, primers, decorative finishes, and protective coatings for residential and commercial buildings, making it the largest consumer of raw materials. A typical architectural paint formulation includes 20–30% acrylic resin, 10–20% pigments (primarily titanium dioxide), 10–20% fillers (calcium carbonate, talc), and 3–8% additives, creating substantial demand across the coatings supply chain. A major industry focus is titanium dioxide (TiO₂) optimization, as this high-cost pigment accounts for a significant portion of formulation expenses. Manufacturers are increasingly adopting advanced dispersion technologies and extender systems to maintain opacity while reducing TiO₂ usage. These dynamics position architectural coatings as the primary demand driver in the global coatings raw materials market.

Coatings Raw Materials Market Competitive Landscape Shaped by Sustainable Resins, Additives, and Feedstock Integration

The coatings raw materials market is led by vertically integrated chemical giants focusing on sustainable resins, specialty additives, and circular economy solutions. Competition is driven by feedstock flexibility, low-VOC innovations, regional capacity expansion, and advanced materials for automotive, packaging, and industrial coatings applications.

BASF Strengthens Global Resin Supply Chain with Low-VOC and Integrated Feedstock Strategy

BASF SE’s Dispersions & Resins division remains central to the global coatings raw materials market, supported by €60 billion in 2025 group sales and strong vertical integration into acrylic monomers. The company expanded dispersion production capacity across Durban, Ludwigshafen, and Dilovasi in 2026 to secure EMEA supply continuity. Its launch of Joncryl® HPB high-performance barrier resins targets sustainable packaging and functional coatings with near-zero VOC emissions. The early operationalization of its Zhanjiang Verbund site enhances cost-efficient supply for the rapidly growing Asian coatings market. BASF’s “Winning Ways” strategy enables faster, localized responses to market volatility and demand shifts. Its integrated production model and innovation in eco-friendly coating resins reinforce leadership in architectural and industrial coatings raw materials.

Covestro Advances Circular Polyurethane Dispersions and Smart Textile Coatings

Covestro AG continues to prioritize innovation in coatings and adhesives despite EBITDA pressures, reporting €12.9 billion in 2025 sales and maintaining strong R&D investment in circular economy solutions. The acquisition of Pontacol in 2026 expands its thermoplastic adhesive films portfolio for automotive and technical textiles applications. At Techtextil 2026, Covestro introduced advanced Impranil® polyurethane dispersions with enhanced conductivity and flexibility, targeting smart textile coatings and sensor-integrated protective apparel. The company is progressing toward climate neutrality for Scope 1 and 2 emissions by 2035, supported by bio-based TPU and recycled aniline for MDI production. Its Desmopan® AIR and FLY TPU grades enable lightweight, high-performance applications through supercritical fluid foam processing. Covestro’s focus on sustainable polyurethane coatings and advanced materials strengthens its position in next-generation functional coatings markets.

Dow Enhances Specialty Coatings Materials with Digital Carbon Tracking and Cost Optimization

Dow Inc.’s Performance Materials & Coatings segment is executing its “Transform to Outperform” strategy, targeting $2 billion in EBITDA improvements with significant cost savings expected by the end of 2026. The company implemented price increases on polyethylene and monomers to manage supply constraints and geopolitical risks, maintaining strong margins in volatile markets. Its DOWANOL™ Glycol Ethers sustainability ledger enables coatings manufacturers to track Scope 3 carbon emissions in real time, enhancing transparency in solvent usage. Dow is reallocating capital away from high-cost upstream assets toward high-margin specialty surfactants and rheology modifiers. Its feedstock flexibility and global asset footprint ensure operational resilience during supply chain disruptions. The company’s focus on digital tools, specialty chemicals, and sustainable solvents positions it strongly in industrial and architectural coatings raw materials.

Arkema Leads Photocure Resin Innovation and Bio-Attributed Coating Solutions

Arkema’s Coating Solutions segment continues to expand through portfolio realignment, separating primary materials from high-growth specialty materials businesses in 2026. The company achieved over 70% global ISCC+ certification for bio-attributed resins, enabling mass-balance solutions for sustainable coatings production. Arkema holds a leading position in Sartomer® photocure resins and ranks among the top global coating resin suppliers, with strong emphasis on UV, LED, and EB curing technologies. Its collaboration with Senior advances high-performance binders and separator coatings for electric vehicle batteries. Arkema also showcased advanced fire-retardant and cooling-compatible coating materials for sustainable data centers in 2026. The company’s innovation in energy-efficient curing technologies and green resins strengthens its competitive advantage. Its strategic alignment with EV and digital infrastructure markets supports long-term growth.

Evonik Expands High-Performance Additives Portfolio with Strong Distribution Network

Evonik Industries AG maintains a strong position in coating additives, supported by a 2026 EBITDA outlook of €1.7–€2.0 billion and stabilized demand in its Custom Solutions segment. The company strengthened its North American distribution network by partnering with Palmer Holland and Andicor, enhancing technical service capabilities. Its TEGO® additives and silica-based matting agents are widely used in high-performance automotive coatings and electronic finishes. Evonik continues to invest in crosslinkers and advanced materials for 3D printing, supporting next-generation coating applications. Its sustainability roadmap links dividend policy to financial performance, emphasizing return on capital efficiency. The company’s 37% cash conversion rate supports targeted R&D in specialty additives. Evonik’s focus on functional additives and surface performance optimization reinforces its leadership in premium coatings formulations.

Solvay Optimizes Specialty Chemical Portfolio with Sustainable Coating Intermediates

Solvay is restructuring its specialty chemicals portfolio to prioritize high-margin coating intermediates and sustainable production processes. The company optimized its soda ash capacity in Europe, shifting focus toward sodium bicarbonate and premium raw materials for coatings and surface treatments. Its deep integration in hydrogen peroxide and soda ash value chains supports critical applications in glass coatings and industrial processes. Solvay achieved its 2030 emission reduction targets ahead of schedule, reducing CO2 emissions by 29% since 2021 through energy transition initiatives. The company’s “Essential Chemistry” strategy emphasizes carbon-neutral production and biomass energy utilization across key European sites. Its focus on sustainable intermediates and process optimization enhances long-term competitiveness. Solvay’s integrated and environmentally aligned approach positions it strongly in the evolving coatings raw materials market.

China Coatings Raw Materials Market: High-Purity Feedstocks and Green Manufacturing Driving Global Scale

China continues to dominate the coatings raw materials market, combining massive production scale with rapid transition toward high-purity and sustainable feedstocks. The revised GB 4806.10-2025 standard (effective 2026) has significantly expanded approved materials for food-contact coatings, driving demand for ultra-low-migration resins and additives.

The EV boom is a major catalyst, with 35% expansion in high-purity NMP production supporting lithium-ion battery coatings. Infrastructure stimulus of $140 billion (2025) is boosting demand for epoxy resins and polyurethane precursors for rail and bridge coatings. At the same time, volatility in TiO₂ pricing is accelerating innovation in alternative opacity-enhancing fillers. China is also advancing circularity through bio-based polyols derived from agricultural waste, targeting a 30% reduction in PU carbon footprint. AI-driven production at mega-sites like Jiaxing further reinforces China’s leadership in intelligent, sustainable raw material manufacturing.

India Coatings Raw Materials Market: Specialty Chemical Expansion and PLI Incentives Driving Localization

India is rapidly transforming into a global hub for specialty coating raw materials, supported by strong government incentives and industrial consolidation. Under PLI Scheme 1.2, over $1.43 billion in investments is being directed toward specialty steel coatings, increasing demand for advanced polyester and acrylic resins.

Market consolidation—such as JSW Paints’ acquisition of AkzoNobel India—is reshaping procurement strategies, favoring domestic suppliers. Housing programs like PMAY are driving demand for decorative emulsion resins and inorganic pigments, while the entry of Birla Opus is accelerating production of zero-VOC additives and antimicrobial agents. Additionally, localized R&D hubs are developing heat-reflective pigments tailored for India’s climate, and improved logistics are boosting demand for specialty additives in rural markets. These factors position India as a high-growth, self-reliant raw material market.

United States Coatings Raw Materials Market: Functional Coating Demand and Regulatory Shift Driving Innovation

The United States market is evolving toward high-performance and environmentally compliant raw materials, supported by federal funding and reshoring initiatives. The CHIPS Act is driving demand for ultra-high-purity dielectric resins and electronics-grade solvents used in semiconductor fabrication.

Regulatory changes under TSCA Section 6 are accelerating the transition away from hazardous solvents, leading to a 22% increase in oxygenated and bio-based solvents. Infrastructure projects under the IIJA are boosting demand for epoxy-glass flake precursors for long-life protective coatings. Additionally, innovation in bio-based alkyd resins derived from soybean oil is expanding eco-friendly product portfolios, while supply chain realignments—such as PPG’s silica business divestment—are reshaping the availability of key additives.

Germany Coatings Raw Materials Market: Bio-Circular Resins and REACH 2.0 Compliance Leading Sustainability

Germany remains the global benchmark for green chemistry and sustainable raw materials, driven by strict regulatory frameworks and advanced R&D. The commercialization of bio-circular resins is reducing CO₂ emissions by up to 50%, while proactive compliance with REACH 2.0 is accelerating the shift toward PFAS-free and isocyanate-free systems.

Technological innovation is strong across multiple fronts. The adoption of UV-LED curing systems is increasing demand for specialized photo-initiators, while Digital Product Passports (DPP) are enabling full traceability of raw materials. Germany is also advancing permeation-resistant resins for hydrogen infrastructure and pioneering lignin-based solvents as renewable alternatives to petrochemical products. These developments reinforce Germany’s leadership in sustainable coatings raw materials.

Japan Coatings Raw Materials Market: Nanotechnology Precision and Semiconductor Demand Driving High-End Innovation

Japan’s coatings raw materials market is defined by extreme precision and high-purity requirements, particularly in electronics and advanced manufacturing. The development of ultra-high-purity PGMEA (<1 ppb impurities) is critical for next-generation semiconductor nodes (2nm and 3nm).

Innovation is also expanding into EV and medical applications. The use of thermally conductive fillers (boron nitride, alumina) is enhancing battery coatings, while regulatory changes are boosting demand for biocompatible nanomaterials in medical devices. Japan is also advancing supercritical CO₂ solvent technologies for extracting high-purity resins, and investing in photocatalytic nanocoating precursors for self-cleaning infrastructure. These factors position Japan as a leader in high-value, precision raw materials.

Brazil Coatings Raw Materials Market: Biofuel Integration and Agribusiness Demand Driving Regional Growth

Brazil’s coatings raw materials market is shaped by its strong agribusiness and renewable energy sectors. The “Fuel of the Future” law is driving demand for biofuel-resistant epoxy and phenolic resins used in storage tanks and pipelines.

Agricultural expansion is increasing demand for pesticide-resistant coating agents in protective gear, while industrial investments—such as the ArcelorMittal Vega expansion (640,000 tonnes)—are boosting demand for ZM coating precursors. The sale of BASF’s decorative paint business has restructured supply chains for acrylic emulsions, while sustainable fashion trends are driving adoption of plant-based coating agents from soybean and castor oil. Additionally, federal investments in clean-tech are supporting bio-attributed PU resins on recycled substrates, positioning Brazil as a leader in bio-based coating raw materials.

Coatings Raw Materials Market Report Scope

Coatings Raw Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$90.3 Billion

|

|

Market Size (2032)

|

$129.6 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Raw Material (Resins and Binders, Pigments and Fillers, Inorganic Pigments, Organic Pigments, Extenders and Fillers, Solvents, Additives), By Resin (Acrylics, Epoxies, Polyurethanes (PU), Alkyds, Specialty Resins), By Pigment Grade (Titanium Dioxide (TiO2), Specialty Pigments), By Formulation Technology (Water-borne Feedstocks, Solvent-borne Feedstocks, Powder Coating Raw Materials, Radiation Curable), By End-Use Sector (Architectural and Decorative, Automotive and Transportation, General Industrial, Protective and Marine, Packaging and Inks)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, The Dow Chemical Company, Evonik Industries AG, Arkema S.A., Eastman Chemical Company, Covestro AG, Huntsman Corporation, Allnex GMBH, Wacker Chemie AG, The Chemours Company, Venator Materials PLC, Celanese Corporation, DIC Corporation, Synthomer PLC, Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coatings Raw Materials Market Segmentation

By Raw Material

- Resins and Binders

- Pigments and Fillers

- Inorganic Pigments

- Organic Pigments

- Extenders and Fillers

- Solvents

- Additives

By Resin

- Acrylics

- Epoxies

- Polyurethanes (PU)

- Alkyds

- Specialty Resins

By Pigment Grade

- Titanium Dioxide (TiO2)

- Specialty Pigments

By Formulation Technology

- Water-borne Feedstocks

- Solvent-borne Feedstocks

- Powder Coating Raw Materials

- Radiation Curable

By End-Use Sector

- Architectural and Decorative

- Automotive and Transportation

- General Industrial

- Protective and Marine

- Packaging and Inks

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Coatings Raw Materials Market

- BASF SE

- The Dow Chemical Company

- Evonik Industries AG

- Arkema S.A.

- Eastman Chemical Company

- Covestro AG

- Huntsman Corporation

- Allnex GMBH

- Wacker Chemie AG

- The Chemours Company

- Venator Materials PLC

- Celanese Corporation

- DIC Corporation

- Synthomer PLC

- Clariant AG

*- List not Exhaustive