Market Overview: Exponential Growth in Cold Chain Packaging Materials

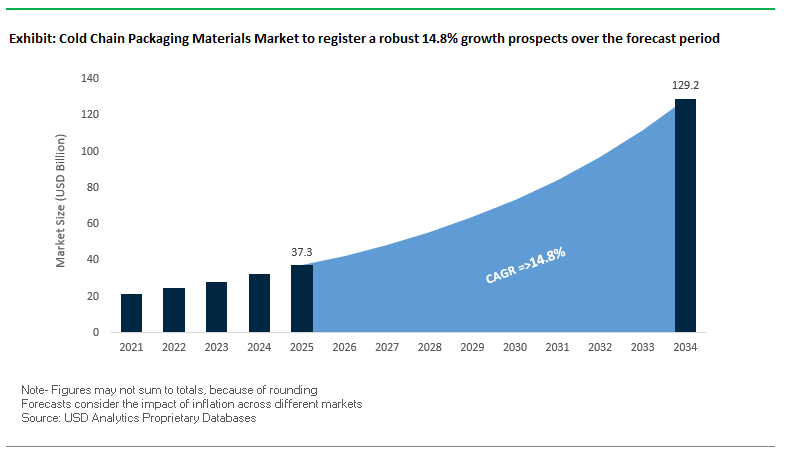

The global Cold Chain Packaging Materials Market is projected to grow from USD 37.3 billion in 2025 to USD 129.2 billion by 2034, advancing at a strong CAGR of 14.8%. This growth trajectory is driven by rising demand for pharmaceutical, biologics, and perishable food shipments that require consistent thermal protection. For industry professionals, the central question is not just “how to keep products cold,” but “how to guarantee temperature compliance with cost efficiency, sustainability, and visibility across global supply chains.Temperature-sensitive goods, particularly vaccines, biologics, and fresh produce, demand packaging solutions that prevent excursions while meeting regulatory standards. The industry is increasingly shaped by sustainability goals, with reusable systems gaining traction and innovative insulation materials like vacuum insulated panels (VIPs) and phase-change materials (PCMs) delivering over 120 hours of thermal protection. Furthermore, the balance between active systems (battery or thermoelectric-powered) and passive systems (insulated containers with refrigerants) is reshaping decision-making based on shipment duration and cost efficiency.

Key Insights:

- Temperature compliance remains the top performance indicator for cold chain packaging.

- Reusable packaging systems are accelerating adoption due to environmental and cost advantages.

- Innovations such as VIPs and PCMs extend thermal protection for long-haul, international shipping.

- Active systems dominate in precision shipments, while passive solutions remain cost-effective for shorter transits.

- Integration of IoT sensors for real-time tracking enhances visibility and reduces spoilage risks.

Market Analysis: Key Industry Developments Driving Growth

The Cold Chain Packaging Materials Market has witnessed transformative changes marked by sustainability-driven innovation and regulatory scrutiny. In September 2025, Steriline unveiled its robotic 3D Control and Picking Solution (3D CPS) at the Fachpack trade show, addressing aseptic packaging challenges in the pharmaceutical sector by reducing particle release during capping and crimping. Similarly, in July 2025, the UK Court of Appeal’s ruling against Aldi in favor of Thatchers underlined the growing importance of distinctive packaging design, even in cold chain packaging contexts, where brand identity and compliance intersect.

Earlier in June 2025, PMMI reported a packaging material shift, projecting reduced use of rigid plastics and glass in favor of flexible and paper-based formats, aligning with single-serve and sustainable packaging trends. Around the same time, May 2025 saw MRP Solutions recognized by the National Association of Container Distributors (NACD) as Supplier of the Year, emphasizing leadership in packaging excellence. Meanwhile, Teknor Apex’s March 2025 acquisition of Danimer Scientific highlighted strategic integration of PHA-based bioplastics into cold chain packaging portfolios, advancing the adoption of biodegradable materials.

Going back to 2024 and 2023, innovation momentum was already strong. In April 2024, CSafe launched its Silverpod MAX RE, a reusable pallet shipper capable of maintaining protection for over 120 hours, targeting sustainability-conscious clients. TekniPlex Healthcare expanded cleanroom capabilities in January 2024, while Cryopak’s Eco Gel launch in November 2023 showcased biodegradable gel packs resilient enough for multiple uses. Likewise, Thomas Scientific’s October 2023 acquisition of Quintana Associates strengthened its position in cleanroom and cold chain packaging. Ranpak’s March 2023 launch of RecyCold climaliner, a recyclable paper-based liner, reinforced the shift toward eco-friendly alternatives.

Transformative Trends and Lucrative Opportunities Driving the Cold Chain Packaging Materials Market

Rapid Adoption of Phase Change Materials (PCMs) for Parcel-Scale Pharmaceutical Shipping

The cold chain packaging market is experiencing accelerated adoption of Phase Change Materials (PCMs), particularly for parcel-scale pharmaceutical shipments. The rise of direct-to-patient models and specialty pharmacy distribution has increased demand for reliable thermal management solutions for biologics and cell & gene therapies with narrow thermal stability profiles. PCMs, engineered to maintain precise temperatures (e.g., 2–8°C or -20°C), offer a safer and more efficient alternative to traditional gel packs and dry ice, mitigating risks like freeze-shock and handling hazards. Cold Chain Technologies, a leading market player, has developed advanced refrigerant PCMs that are non-water-based and reusable, aligning with industry sustainability and cost-efficiency goals. This trend represents a high-value growth segment, particularly as the pharmaceutical industry increasingly relies on parcel-scale, temperature-sensitive logistics. Reports indicate that PCMs offer superior performance in controlled room temperature (CRT) shipping, ensuring product integrity throughout transit while reducing operational risk.

Material Science Innovation in Sustainable & Recyclable Insulation

Environmental and ESG mandates are accelerating the development of sustainable, high-performance insulation materials to replace expanded polystyrene (EPS) and polyurethane (PUR) foam. Biodegradable and recyclable solutions are gaining traction, driven by the environmental burden of single-use foam and rising consumer expectations. Companies such as Ranpak (with RecyCold® climaliner™) and EFP, LLC (through NatureKool acquisition) are pioneering paper-based and natural fiber insulation alternatives, offering comparable thermal performance while being curbside recyclable or compostable. Research highlights that bio-based foams from cornstarch and other plant-derived materials provide effective insulation with significantly reduced ecological impact. This trend creates a key growth avenue as retailers and pharmaceutical distributors demand environmentally responsible cold chain packaging, particularly for high-volume applications.

Development of Integrated IoT-Enabled Packaging for Condition Monitoring

The integration of IoT-enabled sensors in cold chain packaging represents a major opportunity for real-time, GPS-enabled condition monitoring. With high-value pharmaceuticals and perishable foods at stake, stakeholders require immutable, blockchain-verified proof of condition for regulatory compliance and chain-of-custody documentation. Companies like Sensitech and Elpro are leading innovation by embedding data loggers and sensors into packaging, enabling remote monitoring of temperature, humidity, and shock events. IoT-enabled packaging supports proactive intervention, such as rerouting shipments, and aligns with regulations like the U.S. FDA Drug Supply Chain Security Act (DSCSA). This trend creates new business models, including packaging-as-a-service, and opens revenue streams for cold chain providers while ensuring compliance and minimizing product loss.

Standardization of Packaging for Last-Mile Vaccine and Biologic Distribution in Emerging Markets

The global scaling of vaccine distribution has exposed critical gaps in last-mile cold chain logistics, particularly in regions with unreliable infrastructure. There is a growing opportunity to develop standardized, ultra-passive cooling containers capable of maintaining stable temperatures over long durations without electricity. Initiatives by WHO and Gavi highlight the need for cost-effective, durable solutions to prevent wastage, which currently accounts for over 50% of vaccines globally in low-income settings due to cold chain disruptions. Lessons from the COVID-19 pandemic, such as the distribution challenges of ultra-cold Pfizer-BioNTech vaccines, have demonstrated feasibility, while emphasizing cost reduction for routine use. This opportunity addresses an urgent market need, offering growth potential for packaging providers targeting emerging markets, global health organizations, and pharmaceutical companies seeking reliable, long-duration cold chain solutions.

Competitive Landscape: Leading Companies in Cold Chain Packaging Materials

The competitive environment in the global cold chain packaging materials market is characterized by a mix of specialized thermal packaging providers, global packaging leaders, and innovators focused on sustainability. Companies are investing in biodegradable solutions, reusable pallet shippers, and high-barrier films to strengthen their portfolios and capture a larger share of the rapidly expanding market.

Cold Chain Technologies Expands Life Sciences Focus

Cold Chain Technologies (CCT) remains a leading provider of insulated thermal packaging solutions for pharmaceuticals and biotech companies. Its October 2023 acquisition of Exeltainer expanded its global reach and added sustainable thermal packaging products to its portfolio. With reusable and single-use shippers, insulated boxes, and gel packs, CCT leverages its deep expertise in life sciences to meet the highest standards of temperature compliance.

Sonoco ThermoSafe Strengthens Sustainable Offerings

Sonoco ThermoSafe, a unit of Sonoco, is a global supplier of validated cold chain solutions for pharmaceuticals, vaccines, and biologics. The company emphasizes sustainable lightweighting and invests in continuous innovation to meet regulatory and customer requirements. Its global footprint and ability to provide customized solutions have made it a trusted partner for both small and large-scale clients.

Amcor PLC Accelerates Sustainability Goals

Amcor PLC plays a pivotal role in integrating sustainable materials into flexible and rigid plastic packaging. In July 2025, Amcor launched its Hector Child Resistant Closure (CRC) for medical cannabis and household cleaner packaging, balancing safety with sustainability. Its commitment to making all packaging recyclable or reusable by 2025 sets it apart as a sustainability leader in the cold chain packaging space.

Sealed Air Enhances High-Barrier Film Innovation

Sealed Air, through its Cryovac brand, delivers multi-layer high-barrier films critical for food and medical cleanroom packaging. Its strong R&D network underpins its focus on lightweighting and sustainability, while its global footprint enables comprehensive solutions across industries. Sealed Air continues to invest in technologies that improve safety and performance while reducing material consumption.

Cryopak Pioneers Biodegradable Solutions

Cryopak, a subsidiary of CryoPort Inc., provides gel packs, phase-change materials, and insulated containers for food, pharma, and biotech applications. Its November 2023 launch of Eco Gel reinforced its role in sustainable packaging innovation, introducing biodegradable gel packs designed for repeated use. The company’s strategic emphasis on eco-friendly solutions positions it well to capture the growing demand for sustainable cold chain shipping options.

Cold Chain Packaging Materials Market Share Insights

Insulated Containers Lead Market Share by Product Type in the Cold Chain Packaging Industry

Insulated containers command the largest share at 28% of the cold chain packaging market, reflecting their critical role as the primary vessel for transporting temperature-sensitive products across industries. Their versatility ranging from small parcel shippers for diagnostics to large insulated boxes for bulk food or pharmaceutical shipments makes them indispensable. Growth is underpinned by innovations in reusable designs, curbside-recyclable fiberboard insulation, and integration with advanced refrigerants. While refrigerants and pallet shippers are equally critical, insulated containers form the backbone of cold chain logistics by combining thermal protection with structural durability, making them the workhorse of both food and pharma supply chains. Their position is reinforced by increasing global trade in biologics, vaccines, and frozen foods, where failure in insulation is not an option.

Pharmaceuticals & Biotechnology Dominate Market Share by End-Use Industry in Cold Chain Packaging

Pharmaceuticals and biotechnology control 55% of the cold chain packaging market, cementing their role as the industry’s high-value anchor. Unlike food applications, where packaging is largely cost-driven, pharmaceutical shipments such as biologics, vaccines, and oncology drugs demand uncompromising temperature integrity, chain-of-custody verification, and compliance with stringent regulations (e.g., GDP and USP standards). This makes premium insulated containers, phase change materials (PCMs), and real-time temperature monitoring devices indispensable. The surge in global demand for personalized medicine, clinical trial logistics, and advanced therapies is further accelerating investment in cold chain infrastructure. While the food and beverage sector follows with volume-driven growth, it is the pharmaceutical and biotech sector that continues to define technological benchmarks, pushing suppliers toward smart packaging, IoT-enabled monitoring, and zero-failure performance standards.

United States Cold Chain Packaging Market Accelerates with Ultra-Low Temperature Solutions and IoT Integration

The U.S. cold chain packaging materials market is heavily regulated by the Food and Drug Administration (FDA), particularly for pharmaceuticals, biologics, and food products. The introduction of regulations for cell and gene therapies has intensified demand for specialized ultra-low temperature packaging materials. Corporate investments are focused on strategic partnerships, such as Cold Chain Technologies (CCT) collaborating with VPL Rx in August 2024 to integrate thermal packaging into specialty pharmacy shipping workflows, demonstrating an emphasis on supply chain efficiency and product safety.

Technological advancements are driving the adoption of reusable and high-performance passive packaging, including vacuum-insulated panels (VIPs) and optimized phase change materials (PCMs) that maintain precise temperatures without dry ice. The industry is also embracing sustainable materials, such as recycled plastics and fiber-based alternatives to expanded polystyrene (EPS). Integration of Internet of Things (IoT) sensors for real-time temperature monitoring is becoming standard, providing end-to-end visibility and proactive intervention capabilities. Demand is concentrated in pharmaceuticals, biotechnology, and food & beverage sectors, fueled by e-commerce and home delivery services for perishable goods.

Germany Cold Chain Packaging Market Focused on Sustainability, Compliance, and High-Performance Insulation

Germany’s cold chain packaging market is shaped by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, mandating fully recyclable or reusable packaging by 2030. German manufacturers emphasize high-quality assurance and compliance with Good Distribution Practice (GDP) guidelines, particularly in pharmaceuticals. Technological innovation is focused on machinery capable of handling sustainable materials and in-house production on advanced extrusion and converting equipment, ensuring quality and traceability.

The pharmaceutical and food sectors are the key drivers, with Germany’s position as the largest milk producer in Europe driving demand for specialized dairy packaging. R&D collaborations between companies and research institutions are leading to lighter, stronger, and more sustainable packaging solutions. The adoption of digital product passports and watermarks ensures material transparency and improves recycling efficiency, positioning Germany as a leader in both compliance and environmentally responsible cold chain packaging.

China Cold Chain Packaging Market Expands Through Green Initiatives and Domestic Manufacturing

China’s cold chain packaging materials market is driven by the government’s “dual carbon” strategy, promoting green industrial transformation and sustainable logistics. The cold-chain logistics sector expanded significantly in the first half of 2025, supported by investments in new-energy refrigerated trucks and cold storage facilities. Regulatory reforms, including the mandatory standard for “Limit of Harmful Substances of Coatings” effective June 1, 2026, are strengthening controls on hazardous materials and aligning domestic production with international standards.

Technological advancements in China focus on AI and “5G plus industrial internet” integration to optimize production efficiency and flexibility for complex packaging designs. Local companies are expanding capacity to reduce dependency on imported technology, catering to growing demand from pharmaceuticals, high-value agricultural exports like lychees and cherries, and the domestic e-commerce and fresh food sectors. China is also leading in packaging innovation, with numerous patents driving the development of advanced, environmentally friendly materials and high-performance cold chain solutions.

India Cold Chain Packaging Market Driven by Farm-to-Fork Infrastructure and Sustainable Solutions

India’s government initiatives, such as the “Pradhan Mantri Kisan Sampada Yojana (PMKSY),” aim to strengthen cold chain infrastructure from farm gates to retail outlets. As of March 2025, 52 projects were approved under the scheme to enhance value chain development. Corporate investments are focused on sustainable packaging solutions like Phase Change Material (PCM) cartridges by Tessol, offering fuel-free and eco-friendly thermal protection.

Technological adoption is increasing, with automated systems and cost-efficient solutions being developed for vaccines, frozen foods, and other perishable products. Strategic partnerships, such as the CIRCLE Alliance launched by Unilever, USAID, and EY in August 2024, are promoting packaging circularity and waste reduction. Demand is propelled by rapid growth in e-commerce, food & beverage, and pharmaceutical sectors, emphasizing reduced post-harvest losses and reliable cold chain solutions.

Brazil Cold Chain Packaging Market Advances with Robotics, Sustainability, and Ultra-Low Temperature Capabilities

Brazil’s cold chain packaging market is influenced by the National Solid Waste Policy and new sustainability laws, which require compliance with material purity and sterility standards. Technological advancements include robotics and AI for enhanced efficiency, defect detection, and real-time monitoring through smart additive packages and sensors. There is a strong emphasis on integrating circular economy principles into packaging design and manufacturing.

The food, beverage, pharmaceutical, and personal care sectors drive demand, with government initiatives promoting vaccine sovereignty and ultra-low-temperature storage upgrades. Companies are investing in advanced machinery to meet growing demand for sustainable, high-quality packaging technologies. Ongoing government regulations and voluntary commitments targeting 30% mandatory recycling in the current year and 50% by 2040 are further influencing material choice and cold chain innovation.

Japan Cold Chain Packaging Market Leads in Nanotechnology, Sensors, and High-Performance Shelf-Life Solutions

Japan’s cold chain packaging market leverages precision manufacturing and advanced technologies, with innovations that extend the shelf life of fresh produce up to 10 times without special packaging, reducing transport costs and CO2 emissions. Regulatory guidance under the “Plastic Resource Circulation Act” (April 2022) encourages environmentally conscious design and reduction of single-use plastics.

The Japanese market is pioneering the use of nanotechnology, smart films, and IoT sensors for real-time tracking of temperature-sensitive products. Innovation is focused on high-performance materials with superior barrier properties, dimensional stability, and resistance to deformation. Corporate collaborations with leaders such as Nichirei Corporation, as well as academic research into biopolymers and natural agents, are driving the development of sustainable, high-functioning cold chain packaging solutions for pharmaceuticals, food, and high-value logistics applications.

Cold Chain Packaging Materials Market Report Scope

Cold Chain Packaging Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.3 Billion

|

|

Market Size (2034)

|

$129.2 Billion

|

|

Market Growth Rate

|

14.8%

|

|

Segments

|

By Product Type (Insulated Containers, Insulated Pallet Shippers, Refrigerants, Gel Packs, Dry Ice, Phase Change Materials, Vacuum Insulated Panels, Temperature Monitoring Devices), By Material Type (Expanded Polystyrene, Polyurethane, Polyethylene, Paper & Paperboard, Others), By End-Use Industry (Pharmaceuticals & Biotechnology, Food & Beverages, Chemicals, Cosmetics & Personal Care, Others), By Temperature Range (Frozen, Chilled, Ambient)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cold Chain Technologies, Pelican Products, Inc. (Peli BioThermal), Sonoco ThermoSafe, Cryopak, Softbox Systems Ltd., Sofrigam, CSafe, Tower Cold Chain, Envirotainer AB, Inmark LLC, DGP Intelsius LLC, Nordic Cold Chain Solutions, CoolPac, TemperPack Technologies, Inc., Coldman Logistics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cold Chain Packaging Materials Market Segmentation

By Product Type

- Insulated Containers

- Insulated Pallet Shippers

- Refrigerants

- Gel Packs

- Dry Ice

- Phase Change Materials

- Vacuum Insulated Panels

- Temperature Monitoring Devices

By Material Type

- Expanded Polystyrene

- Polyurethane

- Polyethylene

- Paper & Paperboard

- Others

By End-Use Industry

- Pharmaceuticals & Biotechnology

- Food & Beverages

- Chemicals

- Cosmetics & Personal Care

- Others

By Temperature Range

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cold Chain Packaging Materials Market

- Cold Chain Technologies

- Pelican Products, Inc. (Peli BioThermal)

- Sonoco ThermoSafe

- Cryopak

- Softbox Systems Ltd.

- Sofrigam

- CSafe

- Tower Cold Chain

- Envirotainer AB

- Inmark LLC

- DGP Intelsius LLC

- Nordic Cold Chain Solutions

- CoolPac

- TemperPack Technologies, Inc.

- Coldman Logistics

* List Not Exhaustive

Methodology

The findings presented in this report on the Cold Chain Packaging Materials Market have been developed using a rigorous research framework by USDAnalytics, integrating both primary and secondary sources to deliver actionable intelligence for industry professionals. Primary research involved interviews with key stakeholders, including packaging manufacturers, logistics providers, pharmaceutical distributors, and food supply chain managers, to capture insights on technology adoption, regulatory compliance, and sustainability initiatives. Secondary research encompassed the review of corporate reports, patent filings, trade journals, regulatory guidelines, and press releases to evaluate material innovations, product launches, and competitive strategies. The research process analyzed trends in active and passive thermal protection systems, innovations in Phase Change Materials (PCMs), vacuum insulated panels (VIPs), reusable containers, and IoT-enabled packaging for real-time monitoring. Regional regulatory landscapes across North America, Europe, Asia-Pacific, and Latin America were examined to understand compliance requirements and sustainability mandates. Advanced analytical techniques, including market segmentation, performance benchmarking, and technology adoption assessment, were employed to identify growth opportunities in pharmaceutical, biotech, and food logistics sectors. The report also evaluates key players’ portfolios, highlighting strategies in sustainable materials, reusable systems, and high-barrier insulation solutions. By combining quantitative data, expert insights, and trend mapping, USDAnalytics provides a comprehensive perspective on emerging opportunities, technological advancements, and strategic priorities in the evolving cold chain packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.