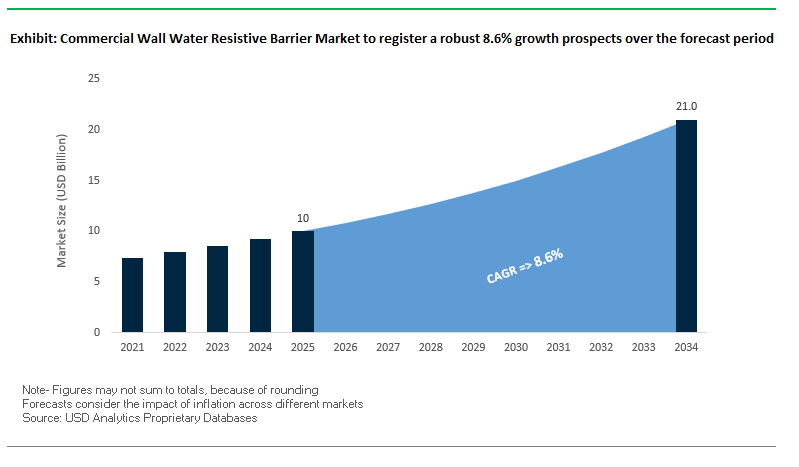

Market Overview: Global WRB Market Valued at $10 Billion in 2025

The Global Commercial Wall Water Resistive Barrier (WRB) Market is valued at USD 10 billion in 2025 and is forecasted to reach USD 21 billion by 2034, advancing at a robust CAGR of 8.6%. Unlike traditional building papers, WRBs have evolved into a strategic component of high-performance building envelopes, critical for moisture control, fire safety, and long-term structural integrity. For developers, architects, and contractors, WRBs are no longer an afterthought they are a compliance-driven and performance-enhancing necessity in commercial construction.

Adoption trends reflect a decisive move toward fluid-applied WRBs in North America and Europe, where seamless application ensures continuous protection against water intrusion. Building standards bodies have validated WRB safety with increasing numbers of assemblies passing the NFPA 285 fire propagation test, which is now a non-negotiable requirement in multi-story and high-rise projects. Another transformative driver is demand for high vapor-permeable systems, enabling assemblies to dry naturally and reducing risks of mold, decay, and costly litigation.

Commercial contractors and owners are also prioritizing single-source system providers manufacturers that deliver integrated WRBs, sealants, flashings, and insulation under one warranty. This approach simplifies installation, reduces compatibility issues, and ensures performance continuity across the entire envelope.

Key Insights for Industry Professionals:

- Market Size 2025: USD 10 Billion | Market Size 2034: USD 21 Billion | CAGR: 8.6%

- Fluid-applied WRBs replacing sheet goods in high-performance projects.

- NFPA 285 compliance boosting adoption in high-rise construction.

- Vapor-permeable barriers increasingly preferred for healthier buildings.

- System integration with flashings and sealants becoming a contractor priority.

- Sustainability and resilience driving innovation pipelines in North America and Europe.

Market Analysis: Strategic Developments Reshaping WRB Industry in 2025

The commercial wall WRB market in 2025 is marked by innovation, regulatory shifts, and cross-industry collaboration that directly address fire safety, sustainability, and efficiency.

In August 2025, a U.S.-based building products leader launched a fire-retardant WRB membrane for Type I and II structures, directly addressing safety regulations in dense urban high-rise construction. One month earlier, in July 2025, a European chemical major introduced a bio-based WRB formulation utilizing renewable polymers, signaling a clear shift toward petrochemical alternatives. Similarly, in May 2025, a partnership between an insulation giant and a WRB provider delivered a fully integrated system combining insulation, air, and vapor barriers, highlighting the move toward systemized building envelope solutions.

Technological upgrades also accelerated. In April 2025, a construction chemicals company launched a self-adhered WRB with advanced adhesive technology, designed for wider temperature applications and faster installation, cutting on-site labor costs. Reports in March 2025 highlighted the rising adoption of prefabricated panels with pre-installed WRBs, demonstrating the industry’s pivot toward off-site construction efficiencies. In February 2025, a specialty chemicals player expanded into flashings and drainage via acquisition, enhancing its comprehensive moisture management portfolio.

Policy interventions are also playing a key role. In January 2025, an Asian government introduced tax incentives for specifying energy-efficient WRBs, while a major skyscraper developer publicly announced adoption of a single-source WRB system for an entire façade, citing warranty and quality control benefits.

Key Market Trends and Strategic Opportunities in the Commercial Wall Water Resistive Barrier Market

Regulatory Shift Towards High-Performance, Breathable Membranes

The commercial WRB market is transitioning from basic water-resistant solutions to advanced, breathable polymeric membranes, driven by increasingly stringent building codes and energy efficiency mandates. ASHRAE Standard 90.1 now specifies continuous air barrier performance metrics, including a maximum air permeance of 0.02 L/(s·m²) at 75 Pa, a requirement traditional asphalt-saturated felt papers often fail to meet. High-performance WRBs are increasingly recognized as critical to building durability and energy efficiency, with the U.S. Department of Energy citing moisture intrusion as the “single greatest threat” to long-term building performance. Regulatory enforcement, as evidenced by Washington State’s active penalties for non-compliance in construction materials, further underscores that adherence to WRB standards is a non-negotiable requirement. In addition, agencies like the U.S. Army Corps of Engineers and the International Green Construction Code (IgCC) emphasize air-tightness in building envelopes, making WRB performance in controlling air leakage essential to overall energy and durability goals.

Integration with Air and Vapor Barrier Systems for Continuous Performance

A growing trend in commercial construction is the adoption of WRBs as part of fully integrated, seamless air and vapor barrier systems. Moving beyond standalone sheets, products like DuPont Tyvek Fluid Applied WB+™ use silyl-terminated polyether (STPE) technology to create a monolithic barrier, reducing traditional installation failures from taped seams. The Huber Zip System demonstrates the efficacy of integrated systems by combining sheathing and WRB into a single panel with specialized tapes that maintain long-term performance even after years of sun exposure. By addressing systemic failure points, these integrated solutions reduce the risk of moisture intrusion from improper installation or inadequate flashing, providing superior durability and reliability for high-value commercial projects.

Development of Drainage-Enhanced WRBs for Rainscreen Applications

The proliferation of ventilated rainscreen cladding systems presents a targeted opportunity for WRBs with integrated drainage technologies. Advanced WRBs now feature textured surfaces or three-dimensional filament matrices that provide vertical drainage planes, typically ranging from 1 mm to 6 mm, to manage incidental water behind cladding. These innovations ensure secondary moisture management, enhancing overall wall system performance. The growing adoption of aesthetic, high-performance rainscreens in commercial architecture guarantees sustained demand for drainage-enhanced WRBs, offering manufacturers a strategic avenue for growth and differentiation in the competitive market.

Adoption of Sustainable and Recyclable WRB Materials

Sustainability mandates and embodied carbon considerations are reshaping the WRB market, creating opportunities for bio-based and mono-material polymer solutions. Regulatory drivers, such as EPA and GSA initiatives, encourage low-carbon materials and require Environmental Product Declarations (EPDs) to guide procurement. Bio-based polymers derived from renewable feedstocks like tall oil or sugarcane can reduce carbon footprints while maintaining WRB performance. Mono-material WRBs, such as those using polyethylene, improve recyclability and support circular economy principles, offering manufacturers a pathway to meet upcoming waste diversion and federal sustainability mandates. The Federal Buy Clean Task Force amplifies this opportunity by incentivizing low-carbon materials in federally funded projects, creating a clear commercial incentive for WRB innovation and adoption.

Competitive Landscape: Global Leaders in WRB Solutions

The commercial WRB industry is consolidated around manufacturers with R&D depth, distribution scale, and building science expertise. Competitive strategies revolve around fire compliance, system integration, and sustainable chemistry.

DuPont de Nemours, Inc.: Tyvek® Leadership in High-Performance WRBs

DuPont remains a global benchmark in building envelope innovation, led by its Tyvek® brand. Its portfolio includes Tyvek® CommercialWrap® and Tyvek® Fluid Applied WB+, both engineered for vapor permeability, durability, and NFPA 285 compliance. DuPont’s strategy is to deliver integrated systems combining WRBs, flashing tapes, and sealants under a single warranty. Its R&D investment in fire-rated and fluid-applied solutions positions it as a leader in high-rise applications.

Sika AG: System Solutions with Low-VOC and Fluid-Applied WRBs

Sika leverages its construction chemicals expertise to deliver comprehensive building envelope solutions. Recent launches include solvent-free, low-VOC WRBs aligned with green building codes. Its Sika® RainBlock-WB provides a seamless barrier against air and water infiltration. Sika is expanding globally through acquisitions, integrating complementary façade and waterproofing products. Its strength lies in offering full-system WRB solutions from roofing to wall assemblies, appealing to architects prioritizing compatibility and compliance.

Henry Company LLC: Blueskin® Brand Driving Systemized Moisture Control

Henry Company has built a reputation for air and vapor barrier expertise, anchored by its Blueskin® brand. Its product line includes Blueskin VP100 self-adhered membranes and fluid-applied solutions, often packaged as part of complete building envelope systems. Henry’s strategy emphasizes ease of installation and code compliance, with products designed for both new commercial construction and retrofits. Its focus on building science-backed performance makes it a preferred partner for high-performance institutional projects.

Carlisle Companies Inc.: Integrated WRBs and Roofing Solutions

Carlisle offers WRB systems under its CCW and Vapor Barrier brands, spanning fluid-applied and self-adhered membranes. Its competitive edge lies in offering a single-source building envelope, integrating WRBs with roofing and insulation systems. Carlisle has invested in products designed for complex geometries and extreme climates, ensuring durability across diverse markets. Its ability to bundle WRBs with insulation and roofing makes it a strong choice for contractors seeking one-stop envelope solutions.

GAF Materials Corporation: Expanding Beyond Roofing into Wall Barriers

GAF, best known for roofing, has expanded into wall water resistive barriers as part of a holistic building envelope strategy. Its WRBs are engineered for tear resistance, water holdout, and vapor permeability, catering to both new construction and renovation projects. Leveraging its brand recognition and distribution network, GAF positions itself as a provider of roof-to-wall continuity solutions, ensuring integration across the full building envelope.

Commercial Wall Water Resistive Barrier Market Share Insights

Mechanically Attached Sheet Barriers Dominate Market Share by Product Type in Commercial Wall Water Resistive Barrier Industry

Mechanically attached sheet barriers account for nearly 50% of the commercial wall water resistive barrier market, making them the cost-effective workhorse of mid-rise and large-scale construction projects. Products like Tyvek® and similar housewraps are favored for their low material cost, rapid installation, and proven vapor-permeable performance that meets most code requirements. Their dominance is particularly evident in commercial office complexes, retail strip malls, and mixed-use developments where project budgets are tight and building assemblies remain relatively straightforward. Contractors prefer these systems for labor efficiency large rolls can cover extensive square footage quickly, reducing installation time. Furthermore, mechanically attached WRBs align well with rising demand for value-engineered solutions in high-volume construction, ensuring they remain the baseline standard even as fluid-applied and self-adhered membranes capture more specialized, performance-driven niches.

Commercial Buildings Drive Market Share by End-Use in Commercial Wall Water Resistive Barrier Industry

Commercial buildings represent 45% of market demand for water resistive barriers, underscoring their role as the volume driver across the sector. Office towers, retail centers, and large mixed-use complexes are constructed at enormous scale, making WRB selection pivotal in balancing performance with cost. Developers and contractors in this segment prioritize solutions that meet minimum building energy codes while maintaining cost-efficiency, which explains the prevalence of mechanically attached sheet barriers. However, growing emphasis on building envelope performance, especially in LEED-certified projects, is also pushing greater use of fluid-applied barriers in premium commercial projects with rainscreen cladding or curtain wall systems. As commercial real estate continues to urbanize in North America, Europe, and Asia, the sector will remain the primary consumer of WRBs, both in new construction and retrofit applications driven by tightening energy efficiency mandates.

United States: Stricter Building Codes and Energy-Efficient Commercial Wall Water Resistive Barriers

The commercial wall water resistive barrier market in the United States is undergoing a transformation, driven by evolving regulations and sustainability mandates. States like California are enforcing stringent building codes that emphasize advanced air and moisture control systems to improve energy efficiency and extend building lifecycles. The U.S. Environmental Protection Agency’s (EPA) ENERGY STAR program and the Inflation Reduction Act of 2022 are accelerating this trend by offering tax credits for energy-efficient building retrofits. As a result, high-performance WRB systems are increasingly being adopted in both new construction and retrofitting of older commercial properties.

Technological advancements are further shaping the U.S. market. DuPont’s Tyvek commercial wrap with self-sealing seams and Henry Company’s Blueskin VP 180/40 highlight the industry’s shift toward self-adhered and fluid-applied membranes. Demand is particularly strong in institutional buildings such as hospitals, schools, and LEED-certified green projects. Companies like Georgia-Pacific are simplifying installations through integrated systems like the DensElement® Barrier System, while corporate consolidations, such as Sika’s acquisition of MBCC Group, are strengthening portfolios with air, vapor, and waterproofing membranes. This innovation-driven and regulation-backed environment positions the U.S. as a leading hub for high-performance WRBs in commercial applications.

Germany: Circular Economy Regulations Fuel Demand for Sustainable WRBs

Germany’s commercial wall water resistive barrier market operates within one of the most stringent regulatory frameworks in Europe, shaped by the EU’s Packaging and Packaging Waste Regulation (PPWR), effective from February 2025. These regulations mandate waste reduction and recyclability, pushing WRB manufacturers to focus on eco-friendly solutions. Germany’s Packaging Act (Verpackungsgesetz) strengthens producer responsibility for the entire lifecycle of packaging and building products, incentivizing innovations that improve recyclability and promote a circular economy.

The market is also driven by sustainability initiatives and corporate innovation. For example, Gerresheimer AG launched a bio-based closure paired with a glass jar in 2024, showcasing how circular economy principles are extending into construction materials. With PPWR setting targets for recycled content and full recyclability by 2030, German WRB manufacturers are accelerating research into advanced materials and systems. This combination of regulatory pressure, technological innovation, and strong recycling infrastructure ensures Germany remains a leader in sustainable water resistive barrier development for commercial buildings.

China: Carbon Neutrality Goals Reshape the Commercial WRB Market

China’s commercial wall water resistive barrier market is being reshaped by governmental initiatives linked to the nation’s “dual carbon” goals of carbon peak and neutrality. These policies promote eco-friendly and reusable materials in construction, boosting demand for high-performance WRBs in commercial projects. Manufacturers are embracing advanced technologies like automation, 5G-enabled industrial internet, and AI to increase efficiency and flexibility in production, aligning with China’s “Made in China 2025” plan that targets 70% domestic content in high-tech materials by 2025.

Additionally, China’s regulatory push to reduce non-degradable plastics by 2025 is encouraging the development of sustainable WRB systems that minimize environmental impact. Rapid e-commerce growth further drives the need for secure, lightweight, and cost-effective packaging applications, indirectly supporting innovation in WRBs. By coupling government mandates with manufacturing strength, China is becoming a global hub for affordable yet technologically advanced water resistive barrier products that meet both domestic and international standards.

India: Urbanization and Government Incentives Accelerate WRB Adoption

India’s commercial wall water resistive barrier market is expanding rapidly under the government’s “Make in India” initiative and “Zero Effect Zero Defect” mission, both of which encourage high-quality domestic production. Incentives like the Production Linked Incentive (PLI) scheme, with an outlay of INR 10,900 crore for the food processing sector, are strengthening India’s manufacturing base and creating opportunities for WRB adoption across diverse industries. The Plastic Waste Management Rules, which phase out single-use plastics, have further spurred demand for eco-friendly, reusable, and high-performance WRBs in commercial projects.

The demand is reinforced by India’s fast-growing consumer base, urbanization, and the expansion of commercial complexes, IT parks, and business hubs. The healthcare and pharmaceutical industries are also fueling WRB growth as they require secure, tamper-evident, and high-quality barriers for facilities. Furthermore, the SATAT initiative promoting Compressed Bio-Gas (CBG) storage and transport underscores the country’s shift toward sustainable infrastructure. With rapid urbanization and a focus on quality manufacturing, India is positioning itself as a high-growth market for advanced WRB systems in the commercial building sector.

Brazil: Regulatory and Technological Shifts Drive WRB Innovation

Brazil’s commercial wall water resistive barrier market is shaped by the National Solid Waste Policy, which emphasizes circular economy principles and discourages plastic dependency. The January 2025 ban on the import of solid waste, including plastics, is forcing domestic manufacturers to adopt responsible waste management practices and invest in sustainable solutions. This aligns with Brazil’s broader regulatory framework promoting environmental responsibility, making WRBs that are reusable, durable, and recyclable increasingly attractive.

On the technological front, robotics and artificial intelligence (AI) are transforming Brazil’s packaging and construction materials industries. These innovations improve efficiency, enable defect detection, and streamline automated processes, creating high-quality WRB products. Additionally, Brazil’s National Agency of Sanitary Surveillance (ANVISA) has implemented stringent traceability requirements for food and beverage supply chains, further boosting demand for robust and reliable WRBs in commercial facilities. With sustainability, technology, and regulation converging, Brazil is rapidly emerging as a competitive market for next-generation commercial water resistive barrier systems.

Japan: Bio-Based and Recycled Materials Lead the Future of WRBs

Japan’s commercial wall water resistive barrier market stands out for its advanced recycling systems and strong regulatory environment. The Containers and Packaging Recycling Law assigns recycling responsibilities directly to businesses, ensuring a robust infrastructure for repurposing rigid plastics and glass in WRB applications. In May 2025, the Ministry of Health, Labour and Welfare (MHLW) revised standards under the Food Sanitation Act, introducing stricter requirements for food-contact packaging materials, which also influence WRB material development.

The market is increasingly shifting toward bio-based alternatives. For example, LyondellBasell’s bio-based polypropylene was partially adopted by Shiseido for packaging in 2025, reflecting the trend toward sustainable material integration. Japan’s WRB sector is also focused on enhancing functionality, with innovations that deliver superior dimensional stability, resistance to deformation, and long-term performance in demanding commercial applications. By blending advanced recycling, bio-based materials, and high-tech product innovation, Japan continues to position itself as a global leader in sustainable and high-performance commercial water resistive barrier technologies.

Commercial Wall Water Resistive Barrier Market Report Scope

Commercial Wall Water Resistive Barrier Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10 Billion

|

|

Market Size (2034)

|

$21 Billion

|

|

Market Growth Rate

|

8.6%

|

|

Segments

|

By Product Type (Mechanically Attached Sheet Barriers, Self-Adhered Sheet Barriers, Fluid-Applied Barriers), By Material Type (Polyethylene, Polypropylene, Asphalt-saturated Kraft Paper, Other Materials), By Application (New Construction, Renovation & Retrofit), By End-Use (Commercial Buildings, Institutional Buildings, Industrial Facilities, Retail & Hospitality)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Henry Company, Carlisle Companies Inc., Sika AG, GAF, Georgia-Pacific Building Products, CertainTeed (Saint-Gobain), Kingspan Group, BASF SE, Johns Manville, WR Grace, Polyguard Products, Dow, GCP Applied Technologies, Tremco CPG Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Commercial Wall Water Resistive Barrier Market Segmentation

By Product Type

- Mechanically Attached Sheet Barriers

- Self-Adhered Sheet Barriers

- Fluid-Applied Barriers

By Material Type

- Polyethylene

- Polypropylene

- Asphalt-saturated Kraft Paper

- Other Materials

By Application

- New Construction

- Renovation & Retrofit

By End-Use

- Commercial Buildings

- Institutional Buildings

- Industrial Facilities

- Retail & Hospitality

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Commercial Wall Water Resistive Barrier Market

DuPont de Nemours, Inc.

- Henry Company

- Carlisle Companies Inc.

- Sika AG

- GAF

- Georgia-Pacific Building Products

- CertainTeed (Saint-Gobain)

- Kingspan Group

- BASF SE

- Johns Manville

- WR Grace

- Polyguard Products

- Dow

- GCP Applied Technologies

- Tremco CPG Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive and structured research methodology to deliver an authoritative analysis of the global Commercial Wall Water Resistive Barrier (WRB) Market. The approach integrated primary research through detailed interviews with architects, contractors, commercial developers, and WRB manufacturers, combined with secondary research from regulatory documents, building codes, sustainability mandates, and industry publications. Market sizing, trends, and forecasts were derived from historical adoption patterns, fluid-applied versus mechanically attached barrier usage, vapor-permeable system demand, and NFPA 285 compliance across key regions including the U.S., Germany, China, India, Brazil, and Japan. Segmentation analysis covered product types (mechanically attached sheet, self-adhered sheet, fluid-applied), material types (polyethylene, polypropylene, asphalt-saturated Kraft paper), applications (new construction, renovation/retrofit), and end-use industries (commercial, institutional, industrial, retail & hospitality). Competitive benchmarking of global leaders such as DuPont de Nemours, Henry Company, Carlisle Companies, Sika AG, and GAF emphasized strategies in fire compliance, integrated systems, sustainable material innovation, and distribution scale. By combining regulatory insights, technological advances, and regional market dynamics, USDAnalytics provides actionable intelligence for industry professionals seeking procurement strategies, product innovation opportunities, and market expansion guidance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.