Market Overview: Rapid Urbanization, Stricter Regulations, and Modular Innovation Driving Double-Digit Growth

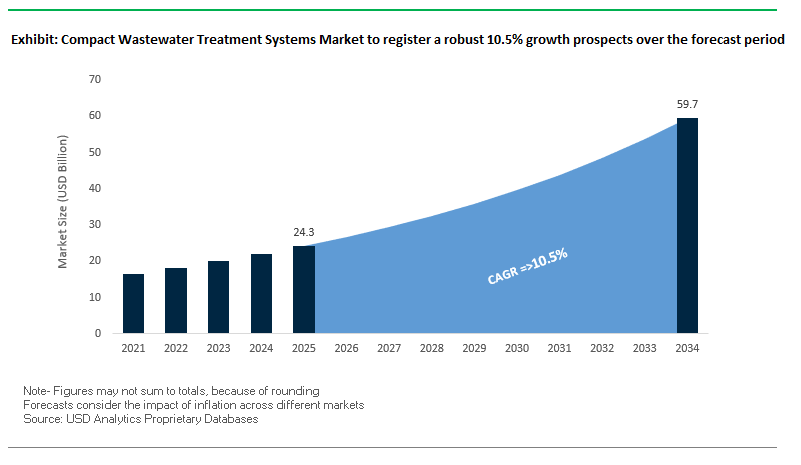

The global compact wastewater treatment systems market is projected to reach USD 24.3 billion in 2025 and expand to USD 59.7 billion by 2034, registering a CAGR of 10.5%. The growth is being propelled by rapid urban expansion in emerging economies, increasingly stringent wastewater discharge regulations in developed markets, and the accelerating adoption of modular and containerized treatment technologies.

Decentralized treatment solutions are becoming indispensable for cities struggling to keep pace with population growth. In India, the Ahmedabad Municipal Corporation’s capacity expansion exemplifies how municipal agencies are opting for modular, scalable systems that can be deployed in peri-urban zones without relying solely on centralized plants.

Regulatory tightening in Europe and North America mandates for micropollutant and nutrient removal are catalyzing the integration of membrane bioreactors (MBR) and tertiary filtration into compact systems. The shift toward containerized plug-and-play plants is also reshaping project economics, allowing developers to deploy fully functional facilities within weeks instead of months.

Water reuse has emerged as both an environmental and economic imperative. For example, a new reclamation station in Brazil will recycle municipal wastewater for industrial operations, freeing potable water for nearly 200,000 residents.

Strategic imperatives for stakeholders:

- Prioritize investment in MBR, RO, and advanced oxidation technologies to meet evolving effluent standards.

- Expand into decentralized and modular plant solutions for rapid market penetration in developing economies.

- Build strategic alliances with municipal and industrial clients to accelerate water reuse adoption.

- Leverage containerized manufacturing models to reduce project lead times and capital costs.

Market Analysis – Consolidation, Technology Integration, and Emerging Deployment Models

The competitive dynamics of 2025 are being reshaped by strategic acquisitions, high-profile municipal contracts, and the scaling of advanced compact technologies across global markets.

In July 2025, H2O America acquired Texas-based utility Quadvest for USD 540 million, committing over USD 500 million in infrastructure modernization. The signals an industry-wide shift toward vertically integrated operations capable of deploying compact systems across expanding service territories.

Veolia strengthened its position in August 2025 by partnering with Brazilian authorities to build the nation’s most advanced wastewater reuse facility for industrial use in Vitória. Featuring memDENSE™ MBR and PROflex™ RO technologies, the plant will recycle 85% of local municipal wastewater, underlining the growing role of high-recovery reuse systems in water-scarce economies.

Fluence Corporation, in March 2025, secured multiple North American contracts for its containerized Aspiral™ Flex plants, each incorporating Membrane Aerated Biofilm Reactor (MABR) technology. These decentralized units target residential developments and remote communities, reflecting market demand for energy-efficient, small-footprint plants.

Meanwhile, SUEZ’s October 2024 contract in Denmark focuses on removing pharmaceutical residues using a hybrid treatment train of ozonation and granular activated carbon (GAC) to meet stringent European discharge standards.

Historical developments also continue to influence the competitive landscape. In April 2024, SUEZ partnered with Maynilad in the Philippines to implement Cyclor Turbo technology in Manila’s Central Sewerage System, addressing land scarcity and energy efficiency concerns. Pentair’s October 2024 acquisition of Porous Media expanded its capabilities in industrial filtration as key to enhancing modular wastewater systems. Similarly, Xylem’s August 2024 launch of the Rivo™ I monitoring and control platform brought precision chemical dosing and real-time analytics into compact plant operations.

Trends and Opportunities in Compact Wastewater Treatment Systems Market

Trend 1: Prefabricated Modular Treatment Units for Rapid Urban Expansion

Rapid urbanization, especially in developing economies, is placing immense pressure on existing municipal wastewater infrastructure. Prefabricated modular wastewater treatment systems are emerging as a high-demand solution due to their scalability, space efficiency, and rapid deployment. These ""plug-and-play"" units can be installed and operational far faster than traditional stick-built facilities, reducing capital costs and accelerating the timeline for operational readiness. Modular systems also provide the flexibility to scale treatment capacity as urban populations grow, making them ideal for fast-developing cities and temporary infrastructure expansions. In India, initiatives like the Atal Mission for Rejuvenation and Urban Transformation (AMRUT) highlight the need for compact modular systems in smaller urban centers. Life cycle assessments reveal that modular MBR systems outperform conventional activated sludge (CAS) plants environmentally, with a lower global warming potential, reinforcing their appeal for sustainable urban water management.

Trend 2: Membrane Bioreactor (MBR) Dominance in Compact Municipal Systems

Stricter environmental regulations and the increasing demand for high-quality effluent are accelerating the adoption of Membrane Bioreactor (MBR) systems in compact municipal wastewater treatment. MBR technology, combining biological treatment with membrane filtration, produces effluent virtually free of pathogens and suspended solids, making it suitable for applications like landscape irrigation, industrial reuse, and toilet flushing. The integrated design significantly reduces the physical footprint up to 50% less than conventional CAS systems to address space constraints in urban areas. Additionally, MBRs deliver enhanced nutrient removal, particularly nitrogen and phosphorus, and demonstrate robust performance under fluctuating organic and hydraulic loads. Hybrid pre-treatment configurations further boost efficiency, ensuring consistent, high-quality treatment even in variable inflow conditions.

Opportunity 1: Containerized Wastewater Treatment Systems for Military & Temporary Deployments

Containerized, self-contained wastewater treatment systems present a significant opportunity in military, disaster relief, and remote worksite applications. Units like the U.S. Army's Deployable Aerobic Aqueous Bioreactor (DAAB) can treat municipal wastewater to EPA standards within 48 hours and operate semi-autonomously, requiring minimal operator training and low maintenance. Equipped with on-board or external power options, these systems are ideal for off-grid deployments. Modular and scalable, a single DAAB unit can serve up to 500 people, and multiple units can be combined for larger camps. Military-grade treatment technologies, focused on speed, reliability, and minimal oversight, can also be adapted for civilian emergency response, providing rapid, durable solutions in disaster-affected areas.

Opportunity 2: Greywater Recycling in Commercial Buildings Using Compact Systems

With growing global water scarcity, commercial buildings are increasingly adopting compact on-site systems for greywater recycling. These systems treat wastewater from showers, sinks, and laundry for non-potable reuse, including toilet flushing and irrigation, significantly reducing potable water consumption. Studies show potential reductions of up to 45% in household potable water use. Beyond water savings, greywater recycling reduces the volume of wastewater discharged to municipal systems, lowering treatment fees and easing infrastructure burdens. For businesses, these systems offer long-term cost savings, a sustainable approach to water management, and a tangible contribution to ESG goals, enhancing corporate reputation and attracting environmentally conscious tenants and customers.

Compact Wastewater Treatment Systems Market Share Insights

Biological Treatment Systems Lead with 55% Market Share as Core Technology

Biological treatment systems dominate the compact wastewater treatment systems market with approximately 55% share in 2025, owing to their cost-effectiveness and efficiency in removing organic pollutants. Technologies such as Membrane Bioreactors (MBR) and Moving Bed Biofilm Reactors (MBBR) have become industry benchmarks, offering superior performance in minimal footprint designs is critical for urban and industrial sites where space is at a premium. In comparison, hybrid treatment systems, with 30.4% share, deliver advanced pollutant removal capabilities, combining biological and physical-chemical steps to meet stringent water reuse standards.

Skid-Mounted Units Represent 45% as the Industrial Standard

Skid-mounted systems hold nearly 45% market share, making them the most widely adopted deployment model for compact wastewater treatment systems. Their pre-assembled, pre-piped, and pre-wired design offers unmatched ease of installation, scalability, and operational reliability, particularly suited for industrial facilities and municipal retrofits. Meanwhile, containerized ISO units, at 35%, are increasingly favored for remote sites and temporary projects, offering superior mobility, climate resilience, and equipment protection, especially in extreme environments.

.png)

Small-Scale Systems Dominate with 41% of Global Installations

Small-scale treatment plants (10–100 m³/day) account for 41.3% of the global compact wastewater treatment systems market, serving small communities, commercial establishments, and medium-scale industries. Their balance of capacity, compactness, and affordability makes them the sweet spot for adoption across both developed and emerging economies. Medium-scale units are growing rapidly, especially for industrial clusters, subdivisions, and small municipalities, where decentralized wastewater treatment can deliver high-value efficiency gains while avoiding costly sewer expansions.

IoT-Enabled Monitoring Secures 33.6% as the Smart Feature Baseline

IoT-enabled monitoring commands about 33.6% of the smart feature segment, underlining its role as the foundational technology for real-time system optimization. Equipped with sensors tracking flow, dissolved oxygen, turbidity, and pressure, these systems enable operators to remotely monitor performance, ensuring compliance and early fault detection. Remote process control, with 25.2% share, is the next layer of adoption, enabling operators to adjust blower speeds, dosing rates, and pumps without site visits, reducing OPEX and enhancing multi-site wastewater management.

Industrial End-Users Hold 52.1% Share as Largest Demand Drivers

Industrial applications dominate the compact wastewater treatment systems market with a 52.1% share in 2025, driven by stricter discharge regulations, water reuse imperatives, and rising surcharges for wastewater discharge. From chemicals and food processing to oil & gas and manufacturing, industries are investing in on-site compact treatment systems to ensure compliance while cutting costs. Commercial and institutional facilities such as hotels, hospitals, and universities are emerging as high-growth adopters, motivated by sustainability commitments and water recycling benefits. Municipal demand remains strategic, particularly in decentralized or satellite wastewater treatment projects supporting urban expansion and emergency deployments.

Country Analysis of the Compact Wastewater Treatment Systems Market

China: Driving Rural Decentralized Wastewater Solutions

China has elevated rural sanitation as a national priority through the Rural Residential Environment Improvement Program, creating strong demand for compact and decentralized wastewater treatment systems in villages and townships. The Ministry of Ecology and Environment mandates real-time emission data disclosure, driving adoption of advanced compact units for consistent monitoring and performance. Innovative frameworks such as the “6S principle” guide rural domestic wastewater management, while significant government investments, exceeding 100 billion CNY, fund projects incorporating compact treatment solutions. Industrial applications are also emphasizing automation and compactness, exemplified by SUEZ’s membrane-based seawater desalination plant in Shandong, underscoring the growing importance of small-footprint, high-efficiency wastewater technologies.

India: Expanding Residential and Community-Level Compact Systems

India’s Jal Jeevan Mission aims to provide safe tap water to every rural household, driving a rising need for residential and community-level compact wastewater treatment systems. Stricter discharge norms from the Central Pollution Control Board (CPCB) are accelerating adoption of advanced technologies capable of meeting regulatory standards. Initiatives such as the Namami Gange Mission and Johkasou technology facilitate decentralized treatment in smaller cities and rural areas. Additional incentives, including state-level capital subsidies, promote the use of treated wastewater in agriculture and industry. Innovations in modular STPs, membrane filtration, and IoT-enabled monitoring enhance real-time tracking, aligning with the government’s Smart Cities Mission for sustainable water management.

United States: Modular and Mobile Solutions for Urban and Rural Needs

The Bipartisan Infrastructure Law, allocating over $50 billion to water and wastewater upgrades, is driving demand for mobile and compact wastewater treatment systems in the U.S. Companies like Fluence Corporation are deploying Membrane Aerated Biofilm Reactor (MABR) systems in residential communities and schools, expanding municipal coverage. There is a strong trend toward modular, scalable treatment plants for small towns, remote locations, and growing communities. Projects such as Corix DE Systems’ energy-integrated treatment in Bellingham showcase sustainable urban development, while EPA advocacy for flexible and decentralized systems further encourages the adoption of compact, energy-efficient wastewater technologies.

Japan: Innovation in Portable and Decentralized Wastewater Systems

Japan emphasizes disaster preparedness, spurring the development of portable, decentralized, and compact wastewater treatment systems. Startups like WOTA Corp. have deployed small-scale, highly efficient water recycling systems in disaster-affected areas, reclaiming over 98% of wastewater. Leading providers such as Kubota Corporation offer Johkasou technology, ideal for decentralized applications where conventional sewage infrastructure is infeasible. Advanced technologies including IoT sensors, machine learning, and real-time water quality monitoring enhance the performance of compact systems, while the regulatory framework and sustainability focus continue to drive innovation in energy-efficient decentralized wastewater treatment.

Germany: Decentralized Compact Systems for Small Communities

Germany’s adherence to the EU Urban Wastewater Treatment Directive and stricter thresholds for small agglomerations is fueling demand for compact wastewater treatment solutions. Extended Producer Responsibility (EPR) programs incentivize companies to invest in advanced micropollutant removal, promoting the integration of tertiary treatment in compact systems. Focus on energy efficiency, resource recovery, and membrane bioreactors is increasing operational effectiveness, particularly in decentralized rural areas. Germany is witnessing a notable shift toward small-footprint, intelligent wastewater treatment systems capable of sustainable performance in both urban and remote settings.

Saudi Arabia: High-Efficiency Compact Units for Remote and Industrial Applications

Saudi Arabia’s National Water Company (NWC), in collaboration with KAUST, has deployed innovative decentralized compact wastewater treatment units using aerobic granular sludge-gravity-driven membrane (AGS-GDM) technology. These systems reduce plant footprints by up to four times and cut energy consumption by 80% compared to traditional MBRs, while producing effluent suitable for multiple reuse purposes. The country’s growing industrial parks and new city developments are increasing the need for temporary and permanent compact water solutions, aligning with Vision 2030 goals for sustainable and accessible sanitation infrastructure.

Competitive Landscape – Technological Leadership and Market Expansion Strategies

The compact wastewater treatment systems market is dominated by a mix of global water infrastructure giants and specialized modular plant innovators. Market leaders are differentiating through technology integration, strategic acquisitions, and deployment speed, targeting both municipal and industrial clients.

Veolia Environnement S.A. – Leading with Integrated, High-Efficiency Modular Systems

Veolia’s ecological transformation strategy combines advanced treatment technologies such as MBR, RO, and advanced oxidation in modular, containerized systems. Its recent Brazil project illustrates its capacity to deploy large-scale reuse systems rapidly. The Hubgrade digital platform provides real-time monitoring and predictive analytics, ensuring performance optimization across its compact treatment portfolio.

SUEZ S.A. – Compact Solutions for Urban Density and Stringent Compliance

SUEZ focuses on high-performance, resilient wastewater treatment technologies tailored for land-scarce, regulation-heavy markets. Its Cyclor Turbo system and advanced membrane filtration capabilities are deployed in Manila and Denmark to address both space constraints and micropollutant removal. Its AQUADVANCED® platform enhances operational intelligence across facilities.

Xylem Inc. – Smart, Interconnected Wastewater Management Platforms

Xylem’s competitive edge lies in digital water integration. Its modular Rivo™ I platform enables real-time process control in compact plants, enhancing compliance and efficiency. The company’s extensive hardware range of pumps, mixers, aerators support flexible deployments in both small communities and industrial settings.

Fluence Corporation Ltd. – Rapid-Deployment, Decentralized Treatment Leader

Fluence specializes in containerized MABR-based systems such as Aspiral™ and NIROBOX™, emphasizing speed to market and low operational costs. With multiple 2025 contracts in North America, Fluence is expanding its Water-as-a-Service model, appealing to clients seeking operational rather than capital expenditure solutions.

B&W Water – Industrial-Grade Compact Wastewater Solutions

B&W Water focuses on automated, sustainable industrial wastewater systems using MBBR and Hydro-PAQ™ CSAS technologies. Designed for sectors like oil & gas and food processing, its solutions prioritize low energy use, compliance, and full automation, catering to clients with complex treatment needs.

Compact Wastewater Treatment Systems Market Report Scope

Compact Wastewater Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.3 Billion

|

|

Market Size (2034)

|

$59.7 Billion

|

|

Market Growth Rate

|

10.5%

|

|

Segments

|

By Technology (Biological Treatment Systems, Physical-Chemical Systems, Hybrid Treatment Systems), By Mobility & Deployment (Skid-Mounted Systems, Containerized Units (20ft/40ft ISO), Trailer-Mobile Systems, Subsurface Installations), By Treatment Capacity (Micro Systems (<10 m³/day), Small Scale (10-100 m³/day), Medium Scale (100-1,000 m³/day), Large Compact (1,000-5,000 m³/day)), By Smart Features (IoT-Enabled Monitoring, Automated Chemical Dosing, Remote Process Control, Predictive Maintenance Systems), By End-User Sector (Municipal, Industrial Applications, Commercial/Institutional)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Sustainable Biosolutions Private Limited (SUSBIO), VA Tech WABAG Ltd., Thermax Limited, Ion Exchange India Ltd., Toshiba Water Solutions, Evoqua Water Technologies (now part of Xylem), Fluence Corporation, SFC Environmental Technologies Pvt. Ltd., Aquatech International LLC, Kingspan Environmental Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Compact Wastewater Treatment Systems Market Segmentation

By Technology

- Biological Treatment Systems

- Membrane Bioreactors (MBR)

- Moving Bed Biofilm Reactors (MBBR)

- Sequencing Batch Reactors (SBR)

- Compact Activated Sludge Systems

- Physical-Chemical Systems

- Coagulation-Flocculation Units

- Dissolved Air Flotation (DAF) Compact Systems

- Advanced Oxidation Processes (AOPs)

- Hybrid Treatment Systems

- MBR-RO Combinations

- Electrocoagulation-Biological Hybrids

- Modular Wetland Systems

By Mobility & Deployment

- Skid-Mounted Systems

- Containerized Units (20ft/40ft ISO)

- Trailer-Mobile Systems

- Subsurface Installations

By Treatment Capacity

- Micro Systems (<10 m³/day)

- Small Scale (10-100 m³/day)

- Medium Scale (100-1,000 m³/day)

- Large Compact (1,000-5,000 m³/day)

By Smart Features

- IoT-Enabled Monitoring

- Automated Chemical Dosing

- Remote Process Control

- Predictive Maintenance Systems

By End-User Sector

- Municipal

- Industrial Applications

- Food processing wastewater

- Pharmaceutical effluent

- Vehicle wash water recycling

- Construction camps

- Military forward bases

- Disaster relief operations

- Others

- Commercial/Institutional

- Hotels and resorts

- Hospitals and schools

- Shopping centers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Compact Wastewater Treatment Systems Market

- Veolia

- Xylem Inc.

- Sustainable Biosolutions Private Limited (SUSBIO)

- VA Tech WABAG Ltd.

- Thermax Limited

- Ion Exchange India Ltd.

- Toshiba Water Solutions

- Evoqua Water Technologies (now part of Xylem)

- Fluence Corporation

- SFC Environmental Technologies Pvt. Ltd.

- Aquatech International LLC

- Kingspan Environmental Ltd.

* List Not Exhaustive

Research Coverage

This report investigates the Global Compact Wastewater Treatment Systems Market, delivering in-depth analysis reviews of technological innovations, regulatory frameworks, and competitive strategies driving the sector’s double-digit growth through 2034. Published by USDAnalytics, the study highlights breakthroughs such as modular membrane bioreactors, containerized plug-and-play systems, and IoT-enabled monitoring that are reshaping project economics and compliance standards across urban, industrial, and decentralized applications. The report also highlights landmark deals including Veolia’s Brazil reuse facility and Fluence’s Aspiral™ Flex deployments, reflecting how leading companies are scaling advanced compact technologies globally. By combining insights into market size, adoption trends, and country-level strategies, this report is an essential resource for utilities, EPC contractors, regulators, and industrial stakeholders navigating the transition toward sustainable, small-footprint wastewater solutions.

Scope Includes:

- Segmentation: By Technology (Biological Systems, Hybrid Systems, MBR, MBBR, MABR, Advanced Oxidation), By Plant Configuration (Skid-Mounted, Containerized ISO Units, Fixed, Mobile), By Scale (Small, Medium, Large), By Smart Features (IoT Monitoring, Remote Process Control, Automation), and By End-Use (Industrial, Commercial, Municipal, Military/Temporary).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and analysis of 15+ key players including Veolia, SUEZ, Xylem, Fluence Corporation, and Pentair.

Methodology

The research methodology applied by USDAnalytics integrates primary and secondary research approaches to deliver reliable, actionable insights. Primary inputs were obtained from interviews with plant operators, municipal agencies, technology providers, and industry consultants, validating adoption trends, deployment models, and regulatory impacts. Secondary research drew from company disclosures, project databases, government reports, and peer-reviewed publications. Market sizing employed a triangulated top-down and bottom-up approach, aligning technology adoption rates with regional infrastructure pipelines and investment flows. Forecasting incorporated scenario modeling of regulatory tightening, modular deployment adoption, and digital monitoring penetration, ensuring a robust, data-driven outlook for the global compact wastewater treatment systems market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Compact Wastewater Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Compact Wastewater Treatment Systems Market Overview & Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $24.3 Billion

2.2.2. Forecasted Market Size (2034): $59.7 Billion at 10.5% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Rapid Urban Expansion and Decentralization

2.3.2. Stricter Wastewater Discharge Regulations

2.3.3. Adoption of Modular and Containerized Technologies

3. Market Analysis: Consolidation, Technology Integration, and Deployment Models

3.1. Overview of Strategic Acquisitions and High-Profile Contracts

3.2. Strategic Developments of Key Players

3.2.1. H2O America's Acquisition of Quadvest (July 2025)

3.2.2. Veolia's Partnership for Wastewater Reuse in Brazil (August 2025)

3.2.3. Fluence Corporation's Contracts for Containerized MABR Plants (March 2025)

3.2.4. SUEZ's Hybrid Treatment in Denmark (October 2024) and other historical developments

3.3. Emergence of Integrated and Modular Supply Chains

4. Trends and Opportunities in Compact Wastewater Treatment Systems

4.1. Trend 1: Prefabricated Modular Units for Rapid Urban Expansion

4.1.1. Benefits of Scalability and Space Efficiency

4.1.2. Lower Capital Costs and Faster Deployment

4.2. Trend 2: MBR Dominance in Compact Municipal Systems

4.2.1. Meeting Stricter Environmental Regulations

4.2.2. Reduced Physical Footprint and Enhanced Nutrient Removal

4.3. Opportunity 1: Containerized Systems for Military & Temporary Deployments

4.3.1. Self-Contained and Rapidly Deployable Units

4.3.2. Adaptability for Disaster Relief and Remote Work Sites

4.4. Opportunity 2: Greywater Recycling in Commercial Buildings

4.4.1. Reducing Potable Water Consumption and Lowering Fees

4.4.2. Alignment with ESG Goals and Corporate Reputation

5. Competitive Landscape: Technological Leadership and Market Expansion Strategies

5.1. Veolia Environnement S.A.: Integrated, High-Efficiency Modular Systems

5.2. SUEZ S.A.: Solutions for Urban Density and Stringent Compliance

5.3. Xylem Inc.: Smart, Interconnected Wastewater Management Platforms

5.4. Fluence Corporation Ltd.: Rapid-Deployment, Decentralized Treatment Leader

5.5. B&W Water: Industrial-Grade Compact Wastewater Solutions

5.6. Other Key Players

6. Market Share and Segmentation Insights: Compact Wastewater Treatment Systems

6.1. By Technology

6.1.1. Biological Treatment Systems Lead with 55% Market Share

6.1.2. Hybrid Treatment Systems (30% Share)

6.2. By Mobility & Deployment

6.2.1. Skid-Mounted Units Represent 45% as the Industrial Standard

6.2.2. Containerized ISO Units and other models

6.3. By Treatment Capacity

6.3.1. Small-Scale Systems Dominate with 40% of Installations

6.3.2. Medium-Scale and Large Compact Units

6.4. By Smart Features

6.4.1. IoT-Enabled Monitoring Secures 35% as the Baseline

6.4.2. Remote Process Control and Predictive Maintenance Systems

6.5. By End-User Sector

6.5.1. Industrial End-Users Hold 50% Share as Largest Demand Drivers

6.5.2. Commercial/Institutional and Municipal Demand

7. Country Analysis and Outlook of the Compact Wastewater Treatment Systems Market

7.1. China: Driving Rural Decentralized Wastewater Solutions

7.2. India: Expanding Residential and Community-Level Compact Systems

7.3. United States: Modular and Mobile Solutions for Urban and Rural Needs

7.4. Japan: Innovation in Portable and Decentralized Systems

7.5. Germany: Decentralized Compact Systems for Small Communities

7.6. Saudi Arabia: High-Efficiency Compact Units for Remote and Industrial Applications

7.7. Other Country Analysis

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By Technology

8.1.2. By Mobility & Deployment

8.1.3. By Treatment Capacity

8.1.4. By End-User Sector

8.1.5. By Smart Features

8.2. Europe Market Size Outlook to 2034

8.2.1. By Technology

8.2.2. By Mobility & Deployment

8.2.3. By Treatment Capacity

8.2.4. By End-User Sector

8.2.5. By Smart Features

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By Technology

8.3.2. By Mobility & Deployment

8.3.3. By Treatment Capacity

8.3.4. By End-User Sector

8.3.5. By Smart Features

8.4. South America Market Size Outlook to 2034

8.4.1. By Technology

8.4.2. By Mobility & Deployment

8.4.3. By Treatment Capacity

8.4.4. By End-User Sector

8.4.5. By Smart Features

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By Technology

8.5.2. By Mobility & Deployment

8.5.3. By Treatment Capacity

8.5.4. By End-User Sector

8.5.5. By Smart Features

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations