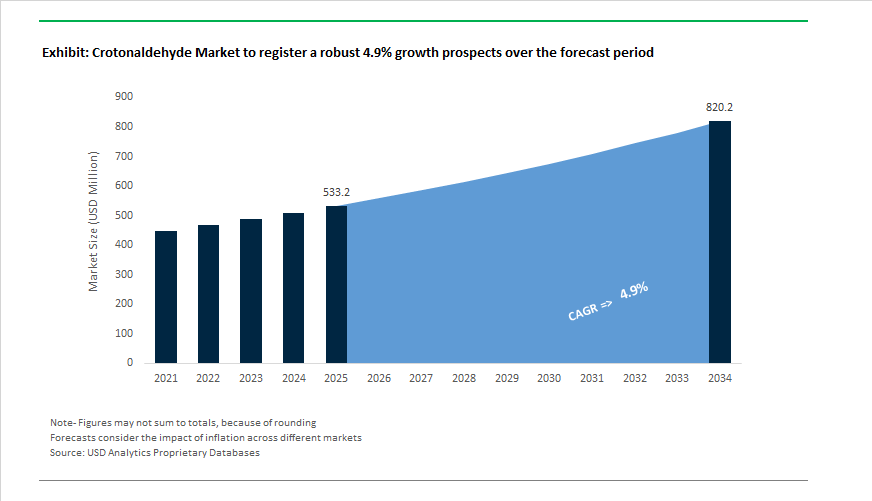

Crotonaldehyde Market to Reach $820.1 Million by 2034 at 4.9% CAGR Driven by Bio-Based Production, Sorbic Acid Demand, and Acetyl Chain Realignment

The Crotonaldehyde Market is projected to expand from $533.2 Million in 2025 to $820.1 Million by 2034, reflecting a CAGR of 4.9%. Crotonaldehyde remains a critical α,β-unsaturated aldehyde intermediate in the synthesis of sorbic acid, pyridine derivatives, pharmaceuticals, agrochemicals, plasticizers, and performance resins. Market expansion is closely linked to growth in packaged foods, specialty intermediates, and high-value pharmaceutical molecules, alongside structural realignments among acetyl chain producers. Increasing emphasis on bio-based feedstocks, localized Asia-Pacific production, and digital optimization of volatile intermediate manufacturing is reshaping supply dynamics across the global crotonaldehyde value chain.

Demand-side acceleration became evident during 2024–2025, when global sorbic acid manufacturers reported record production volumes to meet expanding packaged food consumption in Asia and Africa. As sorbic acid is synthesized directly from crotonaldehyde, the surge tightened industrial-grade supply and elevated spot pricing volatility. In April 2025, BASF entered a strategic joint venture with a Chinese chemical partner to strengthen intermediates production capacity across Asia-Pacific, enhancing regional availability for pharmaceutical and agrochemical formulations. Structural optimization intensified in 2025 as BASF implemented its FORWARD! cost-saving program at Ludwigshafen, consolidating European assets and redirecting investment toward high-margin intermediates and sustainable production technologies. Meanwhile, India’s achievement of its 20% ethanol blending target in early 2025 materially shifted feedstock economics, incentivizing the conversion of ethanol into higher-value downstream chemicals including crotonaldehyde and sorbic acid.

Bio-based production leadership advanced in May 2025, when Godavari Biorefineries commissioned its expanded specialty chemicals facility in Sakarwadi, utilizing bio-ethanol as a renewable feedstock for sustainable crotonaldehyde manufacturing. This positioning strengthens India’s role as a green intermediate hub. In July 2025, Godavari Biorefineries secured patent validation across the UK, Spain, and the EU for an anti-cancer molecule derived from its specialty intermediates, underscoring pharmaceutical-grade applications within the crotonaldehyde derivative portfolio. Capacity scaling continued in September 2025, when Jubilant Ingrevia expanded throughput at Bharuch and Gajraula to support pyridine derivatives and specialty intermediates reliant on crotonaldehyde building blocks. On the cost side, Celanese announced price increases for acetyl chain derivatives effective March 2026, citing elevated energy and feedstock costs, while completing the divestiture of its Micromax® business in February 2026 to sharpen focus on core acetyl intermediates. BASF further strengthened digital manufacturing oversight with the opening of its Global Digital Hub in Hyderabad in Q1 2026, applying AI-driven process modeling to optimize yields and safety in volatile aldehyde synthesis. Additionally, Godavari Biorefineries announced the expected commissioning of a 200 KLPD grain-based distillery by Q4 fiscal 2026, securing dual-feedstock resilience for downstream crotonaldehyde and sorbic acid production in an increasingly supply-sensitive market environment.

Trends and Opportunities in the Global Crotonaldehyde Market

Geopolitical Fragmentation Driving Regional Price Divergence

- Global trade realignment and uneven capacity utilization are creating a fragmented crotonaldehyde market in which regional fundamentals increasingly outweigh global spot pricing signals. In North America, market conditions remained relatively resilient through the third quarter of 2025 despite broader industrial cooling. U.S. industrial output expanded by only 0.1% in September, yet downstream demand for crotonaldehyde derivatives remained stable, supported by consumer-facing sectors and steady purchasing power. With unemployment holding near 4.3 %, demand for food additives, coatings intermediates, and specialty solvents continued to absorb domestic crotonaldehyde output, partially insulating producers from global ethylene-linked margin pressure.

- By contrast, Asia Pacific experienced pronounced oversupply dynamics throughout 2025. Elevated inventories in China and South Korea exerted sustained downward pressure on domestic prices as producers ramped up output to compensate for earlier global shortages. This oversupply environment has created a buyer’s market across the region, particularly in China, where industrial production expanded by approximately 6.5% year on year in late 2025. Growth was concentrated in New Energy Vehicle manufacturing and higher value chemical production, enabling downstream processors to secure crotonaldehyde feedstock at favorable terms while compressing margins for upstream suppliers without captive derivative integration.

Demand Consolidation Around Sorbic Acid and Specialty Solvent Derivatives

- Growth in the crotonaldehyde market is increasingly dictated by a narrow set of high value derivatives, most notably sorbic acid and 3 methoxybutanol. Sorbic acid, and its potassium salt form, remains a cornerstone preservative in global food systems, with demand shifting toward higher purity and pharmaceutical grade specifications. In 2025, food processing activity in China expanded by 2.2% while food service output grew by 5.3 %, reinforcing the pull for antimicrobial preservatives that meet clean label and extended shelf life requirements. This demand directly anchors crotonaldehyde consumption within the sorbic acid value chain, particularly for export oriented food and beverage manufacturers.

- In parallel, solvent demand is emerging as a structurally important driver. In India, agriculture and allied sectors recorded growth of 3.5% in the second quarter of fiscal year 2024 to 2025, increasing the use of advanced agrochemical formulations. This expansion is supporting rising demand for 3 methoxybutanol, a crotonaldehyde derived solvent valued for its stability and performance in pesticide formulations designed for tropical climates. As agrochemical producers prioritize formulation efficiency and controlled delivery, specialty solvents synthesized from crotonaldehyde are gaining preference over lower performance alternatives.

Emergence of Bio-Based and Green Crotonaldehyde Production Routes

- Sustainability mandates in Europe and North America are opening a high margin opportunity for bio based crotonaldehyde produced from renewable ethanol derived acetaldehyde. The global bio acetaldehyde market is reaching commercial maturity, enabling scalable green routes for crotonaldehyde synthesis. In India, Godavari Biorefineries is advancing ethanol based chemical pathways, while in the Nordic region Sekab is utilizing first and second generation bio ethanol for catalytic acetaldehyde production. These circular processes significantly reduce the carbon footprint of downstream sorbates used in food, fragrance, and personal care applications.

- Policy support is reinforcing this transition. In July 2025, NITI Aayog highlighted green chemistry as a central pillar of India’s ambition to build a one trillion dollar chemicals sector by 2040. The proposed Chemical Fund initiative emphasizes shared infrastructure for bio purification and conversion technologies, including pathways that convert agricultural sugar residues into 3 hydroxybutyraldehyde, a direct bio route to sustainable crotonaldehyde. These developments position green crotonaldehyde as a premium offering rather than a cost driven substitute.

Specialty Monomers and Advanced Polymer Applications

- Beyond traditional preservative and solvent uses, niche applications in advanced polymers and coatings are emerging as high growth opportunities for crotonaldehyde derivatives. In 2025, electronics and aerospace manufacturers increasingly specified vinyl crotonate as a high purity reactive diluent and crosslinker in radiation curable coatings. These materials deliver enhanced thermal resistance and structural rigidity in thin film applications, while meeting stringent impurity thresholds required under ISO and IEC laboratory and material qualification standards.

- Water treatment polymers represent another promising avenue. Research published in October 2025 in Industrial and Engineering Chemistry Research demonstrated that catalytic hydrogenation of crotonaldehyde using tin platinum intermetallic catalysts improves the selective production of crotyl alcohol. This monomer is a key building block for specialized polymers and chelating agents used in industrial desalination and wastewater recycling systems. As investment in water infrastructure and reuse accelerates globally, crotonaldehyde derived monomers are gaining relevance in high reliability treatment chemistries, extending the market beyond its traditional commodity profile.

Crotonaldehyde Market Share and Segmentation Insights

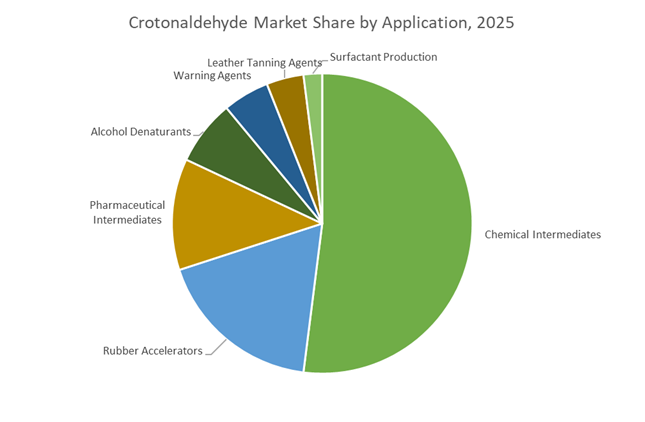

Application Segmentation: Chemical Intermediates Dominate While Rubber Accelerators Sustain Industrial Demand

Chemical intermediates account for 52% of crotonaldehyde consumption in 2025, positioning this reactive α,β-unsaturated aldehyde as a critical building block in sorbic acid, crotonic acid, and fine chemical synthesis. Its conjugated double bond and aldehyde functionality enable versatile derivatization pathways used in preservatives, copolymers, and specialty chemicals. Rubber accelerators represent the second-largest segment, where crotonaldehyde derivatives influence vulcanization kinetics and mechanical performance in tire manufacturing and industrial rubber goods. Pharmaceutical intermediates form a high-purity niche, supporting synthesis of selected sedatives and antihypertensive compounds under stringent quality control standards. Alcohol denaturants constitute a volume-driven but lower-margin application, rendering ethanol unsuitable for consumption in solvents and cosmetic bases. Warning agents leverage crotonaldehyde’s pungent odor for gas leak detection in fuel gases, while leather tanning and surfactant production represent mature or slowly declining specialty uses.

End-Use Industry Distribution: Agrochemicals Lead as Food Preservation and Polymers Expand Integration

Agrochemicals account for 28% of crotonaldehyde demand, reflecting its role in herbicide and insecticide intermediates as well as sorbic acid derivatives used in grain preservation. Rubber and polymers represent a major downstream sector through accelerator production and crotonic acid copolymers applied in adhesives, coatings, and thermoplastic modifiers, with tire manufacturing as a key driver. Food and beverage applications rely indirectly on crotonaldehyde via sorbic acid and potassium sorbate preservatives used in baked goods, cheeses, and beverages, aligning with extended shelf-life requirements. Pharmaceuticals and life sciences require secure supply chains and consistent purity for regulated synthesis processes. Oil and gas consumes smaller volumes for fuel gas odorization to meet safety regulations, while textiles and dyes utilize crotonaldehyde intermediates in specialty dye synthesis and finishing chemistries.

Competitive Landscape of the Crotonaldehyde Market

The Crotonaldehyde Market is driven by acetyl-chain integration, bio-based innovation, and rising demand from food preservatives, vitamin intermediates, rubber chemicals, and life science actives, with competition centered on feedstock security, derivative portfolios, and margin-focused specialty strategies.

Celanese leads acetyl-chain integration for high-value crotonaldehyde derivatives

Celanese Corporation holds a dominant global position through its world-scale acetyl-chain infrastructure, primarily producing high-purity technical-grade crotonaldehyde for downstream chemical synthesis. The company’s integrated acetaldehyde-to-crotonaldehyde process supports key applications such as sorbic acid (food preservation) and trimethylhydroquinone for vitamin E manufacturing. In early 2026, Celanese strategically shifted away from commodity volumes toward higher-margin specialty chemicals, prioritizing value-added derivatives to expand profitability. Its sustainability-driven acetyl chain strategy focuses on minimizing emissions from aldol condensation while maintaining cost leadership. This vertically integrated model positions Celanese as a core supplier to global food, nutrition, and industrial chemical markets.

Godavari Biorefineries accelerates bio-based crotonaldehyde for green chemistry

Godavari Biorefineries has emerged as a major renewable alternative supplier, leveraging bio-based feedstocks to produce crotonaldehyde for pharmaceutical and agrochemical applications across Asia. In Q3 FY26, the company reported a 152% jump in Profit Before Tax, with bio-based chemicals now contributing roughly 62% of its product portfolio. A January 2026 partnership with Synthomer advanced development of bio-based monomers, reinforcing Godavari’s green chemistry positioning. The company also launched a pilot DME plant in late 2025, expanding its biorefinery capabilities. Its strength lies in high-purity grades for drug formulations, aligning strongly with global sustainability and pharmaceutical sourcing trends.

BASF strengthens European supply through Verbund-driven specialty intermediates

BASF remains a cornerstone supplier in Europe, supported by its highly integrated Verbund production complex in Ludwigshafen, ensuring stable acetaldehyde feedstock and cost efficiency. Crotonaldehyde from BASF plays a critical role in rubber compounding, automotive components, specialty coatings, and adhesives, functioning as both cross-linking agent and accelerator. The company has expanded German production capacity to meet rising demand for performance materials, with approximately 32% of new European specialty formulations now incorporating BASF crotonaldehyde. Under its broader specialty chemicals strategy, BASF continues to embed crotonaldehyde into advanced industrial systems while driving operational efficiency and regional supply security.

Jubilant Ingrevia builds fine chemical pipelines around crotonaldehyde chemistry

Jubilant Ingrevia operates a deeply integrated life science platform, using crotonaldehyde as a core building block for fine chemicals, agro-innovators, and CDMO projects. Targeting an EBITDA of ₹2,000 crore by FY30, the company is prioritizing high-margin specialty manufacturing, with 18 new products under development in FY26. Construction of a multipurpose plant in Gajraula, scheduled for late 2026, will significantly expand capacity for advanced chemical synthesis. Jubilant’s global leadership in pyridine and diketene derivatives creates strong internal demand for crotonaldehyde, reinforcing vertical integration and positioning the company as a fast-growing specialty supplier.

Nantong Acetic Acid Chemical anchors China’s high-volume food-grade supply

Nantong Acetic Acid Chemical is a key pillar of the Chinese crotonaldehyde market, operating within a region that accounts for nearly 47% of global output. The company holds a strong share of food-grade crotonaldehyde, primarily supplying sorbic acid manufacturers worldwide. During 2025–2026, Nantong expanded exports to North America and Europe, responding to a roughly 15% rise in global demand for crotonaldehyde-based food preservatives. Backward integration with acetaldehyde and formaldehyde producers enables low-cost, high-volume manufacturing. Its portfolio also supports agrochemical intermediates, making Nantong a critical supplier to pesticide and food additive value chains.

India: Bio-Refinery Scale-Up and Downstream Demand Recovery

India has consolidated its position as a structurally important crotonaldehyde producer by combining scale, bio-based feedstocks, and strong downstream integration. As of 2024–2025, Godavari Biorefineries remains the country’s largest producer with 12,000 MTPA capacity, leveraging an integrated bio-refinery model to supply high-purity crotonaldehyde for chemical intermediates. This scale advantage is being reinforced through feedstock diversification. In late 2025, a ₹130 crore investment was announced for a new 200 KLPD corn and grain-based distillery at Gajraula, scheduled for commissioning by Q4 FY 2026. The project strengthens acetaldehyde availability and improves feedstock flexibility for crotonaldehyde synthesis, reducing exposure to molasses-linked volatility.

Downstream demand fundamentals have turned structurally positive. Jubilant Ingrevia reported in its Q2 FY26 results that the agrochemical sector has exited the destocking phase, driving volume recovery across pyridine and diketene portfolios that consume crotonaldehyde. Specialty chemicals capacity is also expanding, with a new plant inaugurated at Sakarwadi in late 2025 focused on high-value bio-derived molecules from the ethanol-to-crotonaldehyde chain. Policy support under the 2025 Bio-Manufacturing and Bio-Foundry initiative prioritizes 2G ethanol scale-up, stabilizing raw material supply for bio-based crotonaldehyde. Nutraceutical demand is an additional growth vector, as crotonaldehyde remains a critical intermediate in Vitamin B3 synthesis, an area where Jubilant Ingrevia maintained global leadership through 2025.

China: Capacity Discipline, Automotive Pull, and Digitalized Operations

China’s crotonaldehyde market in 2025–2026 is shaped by state-led capacity discipline and uneven demand signals. The National Development and Reform Commission and the Ministry of Industry and Information Technology released the Work Plan for Stabilising Growth in the Petrochemical and Chemical Industry, setting a 5% annual expansion target while tightening approvals for new bulk intermediate capacity. Despite this, oversupply pressures persisted in 2025. During Q3, the China Crotonaldehyde Price Index softened amid negative producer price inflation of 2.3% and elevated ethylene inventories across APAC, compressing margins for commodity-grade output.

Demand resilience is increasingly linked to mobility and manufacturing. Strong New Energy Vehicle production throughout 2025 supported consumption of crotonaldehyde derivatives used in rubber accelerators and specialty coatings. On the operations side, the AI plus Petrochemical initiative mandated for completion by end-2025 is driving VOC reduction and energy efficiency upgrades at plants handling hazardous intermediates, including crotonaldehyde. Export dynamics have become more complex. On October 9, 2025, the Ministry of Commerce of China introduced export controls on chemical processing equipment, constraining the global rollout of specialized distillation units and indirectly influencing international capacity additions.

United States: Process Efficiency and Compliance-Led Cost Pressure

The U.S. crotonaldehyde industry in 2025 emphasizes operational efficiency and supply assurance under rising compliance costs. Producers such as Celanese implemented proprietary oxo-technology upgrades that lifted yields and reduced energy intensity by approximately 12 %, partially offsetting higher operating expenses. Nevertheless, margin pressure persisted. The U.S. Producer Price Index for chemicals rose 2.6% in August 2025, reflecting higher input costs even as natural gas prices stabilized, narrowing spreads for intermediate producers.

Supply chain resilience has become a strategic priority. TRInternational expanded its U.S. stocking footprint to more than 20 locations in late 2025 to mitigate geopolitical risks and ensure reliable supply to pharmaceutical and metalworking customers. Regulatory scrutiny is also intensifying. As crotonaldehyde is a key intermediate for sorbic acid and potassium sorbate, producers are preparing for stricter 2026 audits by the U.S. Food and Drug Administration focused on impurity profiles in food-grade preservatives. This is pushing investments toward higher-purity production and tighter process control.

European Union: Compliance Pressure and Portfolio Rebalancing

In the European Union, regulatory obligations dominate crotonaldehyde market dynamics. Effective September 16, 2025, the REACH Candidate List was migrated to the ECHA CHEM database, triggering immediate compliance requirements for companies using crotonaldehyde as a Substance of Very High Concern in non-intermediate applications. This shift increases documentation and substitution pressure, particularly in downstream specialty uses. At the same time, sustainability-linked offerings are gaining relevance. In mid-2025, BASF added ISCC EU certification to its biomass-balanced portfolio, enabling the supply of certified sustainable intermediates aligned with 2026 regulatory expectations in chemicals and biofuels.

Strategic restructuring is also underway. Celanese announced plans to cease operations at its Lanaken site by 2026, citing an unfavorable investment climate and regulatory intensity. This move underscores a broader trend of rationalizing European production footprints while reallocating capital toward regions with more predictable compliance costs and growth headroom.

Comparative Summary: Country-Level Positioning in the Crotonaldehyde Industry

Crotonaldehyde Market County Level Snapshot

|

Region

|

Primary Structural Driver

|

Demand Anchor

|

Strategic Direction

|

|

India

|

Bio-refinery integration and policy incentives

|

Vitamins, agrochemicals, specialty chemicals

|

Bio-based scale-up and downstream integration

|

|

China

|

Capacity discipline and digitalization

|

NEVs, rubber, coatings

|

Oversupply management and efficiency upgrades

|

|

United States

|

Process efficiency and compliance

|

Food preservatives, pharma intermediates

|

Yield optimization and supply resilience

|

|

European Union

|

REACH and sustainability mandates

|

Certified intermediates

|

Portfolio rebalancing and footprint rationalization

|

Crotonaldehyde Market Report Scope

Crotonaldehyde Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$533.2 Million

|

|

Market Size (2034)

|

$820.1 Million

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Type (High Purity, Technical Grade), By Application (Chemical Intermediates, Pharmaceutical Intermediates, Warning Agents, Alcohol Denaturants, Rubber Accelerators, Leather Tanning Agents, Surfactant Production), By End-Use Industry (Food and Beverage, Pharmaceuticals and Life Sciences, Agrochemicals, Rubber and Polymers, Textiles and Dyes, Oil and Gas)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Celanese Corporation, Godavari Biorefineries Limited, Jubilant Ingrevia Limited, BASF SE, Wacker Chemie AG, Jinyimeng Group, Shandong Kunda Biotechnology Co., Ltd., Jilin Songtai Chemical Co., Ltd., China Overseas Pioneer Chemicals, Atul Ltd., Actylis, Kanto Chemical Co., Inc., Tokyo Chemical Industry Co., Ltd., Lonza Group AG, TRInternational, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Crotonaldehyde Market Segmentation

By Type

- High Purity

- Technical Grade

By Application

- Chemical Intermediates

- Pharmaceutical Intermediates

- Warning Agents

- Alcohol Denaturants

- Rubber Accelerators

- Leather Tanning Agents

- Surfactant Production

By End-Use Industry

- Food and Beverage

- Pharmaceuticals and Life Sciences

- Agrochemicals

- Rubber and Polymers

- Textiles and Dyes

- Oil and Gas

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Crotonaldehyde Industry

- Celanese Corporation

- Godavari Biorefineries Limited

- Jubilant Ingrevia Limited

- BASF SE

- Wacker Chemie AG

- Jinyimeng Group

- Shandong Kunda Biotechnology Co., Ltd.

- Jilin Songtai Chemical Co., Ltd.

- China Overseas Pioneer Chemicals

- Atul Ltd.

- Actylis

- Kanto Chemical Co., Inc.

- Tokyo Chemical Industry Co., Ltd.

- Lonza Group AG

- TRInternational, Inc.

*- List not Exhaustive