Market Overview: Ultra-Low Temperature Engineering Driving the Global Cryogenic Valves Market Expansion

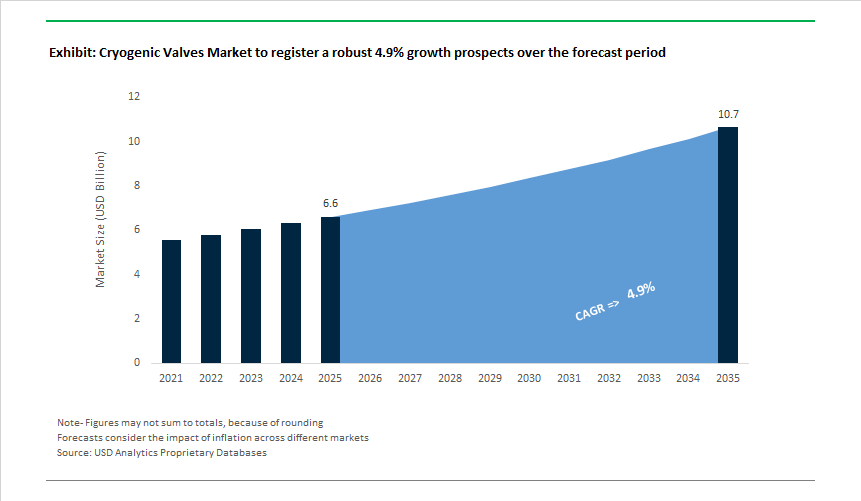

The Cryogenic Valves Market is valued at USD 6.6 billion in 2025 and is projected to reach USD 10.6 billion by 2035, growing at a 4.9% CAGR, as ultra-low-temperature fluid control becomes a non-negotiable enabler of LNG expansion, hydrogen deployment, and industrial gas reliability. This is not a discretionary capex market; cryogenic valves sit at the failure-critical interface of storage, transport, and processing systems where leakage, material embrittlement, or thermal inefficiency translate directly into safety risk, product loss, and regulatory exposure.

Market demand is structurally anchored in LNG infrastructure, which continues to absorb the largest installed base of cryogenic valves. Valves engineered for −165°C to −196°C service remain essential across liquefaction trains, storage tanks, loading arms, and regasification terminals. As LNG trade volumes rise and terminals move toward higher throughput and tighter emissions control, valve performance is being evaluated on boil-off minimization, seat integrity under thermal cycling, and long-term sealing stability. Extended bonnet designs are increasingly treated as standard architecture rather than optional upgrades, as they materially reduce heat ingress and protect packing systems from cryogenic exposure.

A second, faster-moving growth vector is the liquid hydrogen (LH₂) economy, where operating temperatures drop to −253°C and material performance margins narrow significantly. Hydrogen embrittlement, permeability, and fatigue resistance have elevated material selection to a strategic decision point. As a result, 316L stainless steels, austenitic grades, and nickel-based alloys certified for deep cryogenic service are becoming default specifications. For valve manufacturers, hydrogen readiness now directly influences eligibility for next-generation energy projects, pilot plants, and export infrastructure.

Regulatory pressure around fugitive emissions is reshaping competitive dynamics. Methane leakage thresholds are tightening globally, and cryogenic valves are under increasing scrutiny as point sources of emissions. Leading designs now achieve sub-100 ppm methane leakage under standards such as ISO 15848-1 and API 624, turning emissions performance into a commercial differentiator rather than a compliance checkbox. This shift is accelerating innovation in stem sealing systems, low-temperature packing materials, and precision machining tolerances.

At the component level, tight shutoff performance is becoming central to value capture. Cryogenic ball and globe valves increasingly integrate PTFE, PCTFE, and hybrid metal-seated sealing systems capable of maintaining Class V-VI shutoff after repeated thermal cycling and rapid cooldown events. These capabilities are critical not only for safety, but for minimizing product loss in LNG and industrial gas handling, where leakage has direct economic impact.

From a strategic standpoint, the cryogenic valves market is rewarding suppliers that move beyond mechanical reliability toward system integration and digital readiness. OEMs and operators are increasingly favoring valves compatible with smart plant architectures, digital inspection, and predictive maintenance platforms to reduce unplanned downtime in continuous-operation assets. Advanced coatings, surface treatments, and inspection traceability are also gaining weight in procurement decisions as operators extend maintenance intervals and demand higher lifecycle certainty.

Market Analysis: Strategic Developments and Technology Shifts Reshaping the Cryogenic Valves Market

The Cryogenic Valves Industry is undergoing accelerated transformation driven by mergers, digitalization, hydrogen infrastructure commitments, and large-scale LNG investments across major economies. In July 2025, Flowserve completed the integration of Velan Inc., strengthening its global footprint in high-performance cryogenic and severe-service valves. This strategic move enhanced its LNG and industrial gas portfolio, reinforcing the company’s position in a market where engineered reliability and material science expertise command premium value. Earlier, in May 2025, multiple manufacturers intensified adoption of real-time diagnostics and automated actuation, elevating cryogenic valves into core components of smart plants. These advancements are particularly relevant for LNG terminals embracing predictive maintenance, asset integrity solutions, and automated emergency shutdown mechanisms.

The hydrogen economy is a major catalyst in 2025. In March 2025, U.S. government incentives accelerated investments in LH₂-focused valve manufacturing facilities, supporting domestic energy transition policies. Similarly, Asian LNG momentum remained strong as Chinese suppliers secured significant cryogenic valve contracts for new regasification terminals in February 2025, confirming Asia Pacific as a high-volume demand center. The market has also seen significant innovation cycles beginning in 2024. Demaco Netherlands BV introduced an extended-body cryogenic valve upgrade in February 2024, reducing condensation and qualifying for FDA-regulated food-gas applications-an expansion of addressable markets for cryogenic OEMs. On the other hand, Habonim’s January 2024 advancements in floating ball valve technology resolved unidirectionality issues linked to pressure relief hole dynamics, improving flow efficiency and durability.

Industry-wide technological maturity advanced further in October 2024, where additive manufacturing became mainstream for lightweight, precision cryogenic components. Manufacturers also achieved ASME B31.12 certification in September 2024, enabling wider deployment of valves in hydrogen pipelines and reinforcing compliance-driven procurement behavior.

Cryogenic Valves Market Trends and Opportunities

Market Trend 1: Upsizing and High-Integrity Specification for Mega-Train LNG Infrastructure

Global LNG infrastructure is entering a scale-driven upgrade cycle in which cryogenic valves are no longer treated as commodity piping components but as mission-critical assets tied directly to plant uptime, safety performance, and emissions compliance. As LNG trade volumes crossed 400 million tonnes in 2024 and more than 170 million tonnes of new liquefaction capacity is scheduled to come online through 2030, project developers are standardizing around large-bore cryogenic ball and gate valves—often exceeding 36–48 inches in diameter—to manage extreme flow rates in U.S. Gulf Coast and Middle Eastern mega-train facilities. This physical upsizing is accompanied by a parallel tightening of mechanical, thermal, and leakage specifications. Valves are increasingly engineered with extended bonnets that thermally isolate packing systems from −162 °C LNG service, along with upstream pressure-relief features designed to prevent cavity overpressure during liquid-to-gas phase transitions. Operational requirements are also reshaping valve architecture. By late 2025, integrated leak detection, position feedback, and remote diagnostics had shifted from optional enhancements to baseline requirements, driven by stricter methane-emissions monitoring, ESG reporting obligations, and plant safety audits. These smart cryogenic valves enable continuous condition monitoring across liquefaction and regasification terminals, materially reducing unplanned shutdown risk while aligning operators with regulatory scrutiny on fugitive emissions and long-term asset resilience.

Market Trend 2: Qualification of Cryogenic Valves for Liquid Hydrogen Service

The acceleration of national hydrogen strategies is forcing a step-change in cryogenic valve engineering, as liquid hydrogen service introduces technical challenges well beyond conventional LNG operations. At −253 °C, LH₂ exposure significantly magnifies risks related to hydrogen embrittlement, seal permeability, and material fatigue under extreme thermal cycling. In response, valve manufacturers are requalifying advanced alloys such as Inconel 718 and duplex stainless steels that retain fracture toughness while resisting hydrogen diffusion and micro-crack propagation. Public funding is materially shaping this transition: multi-billion-dollar hydrogen hub programs in the United States and Europe are directly supporting component-level R&D, compressing the timeline from laboratory validation to field-ready hardware. Testing regimes have also become markedly more rigorous. By the end of 2025, pressure-cycle testing using actual liquid hydrogen—rather than nitrogen substitutes—had become a baseline requirement for check and isolation valves rated above 10,000 psi. At the same time, European hydrogen pipeline projects are tightening certification thresholds, pushing manufacturers to deliver zero-leakage performance under ATEX and TA-Luft compliance frameworks. Collectively, these dynamics are elevating LH₂-qualified cryogenic valves into a distinct, premium subsegment where qualification depth, metallurgical expertise, and validation infrastructure outweigh traditional price competition.

Market Opportunity 1: Advanced Sealing and Actuation for Aerospace Cryogenic Propulsion

The resurgence of space launch activity and the parallel push toward hydrogen-powered aviation are creating a high-value opportunity for lightweight, fast-response cryogenic valves tailored to aerospace propulsion systems. Modern launch vehicles and upper-stage engines demand valves capable of supporting rapid fueling, precise flow modulation, and instantaneous shutoff under extreme vibration and thermal shock. By 2025, heavy-lift programs and reusable launch platforms had shifted demand toward compact solenoid-actuated poppet and ball valve designs that eliminate bulky external actuation systems, delivering meaningful mass reduction while improving response time and reliability. This requirement extends into experimental LH₂ aviation platforms, where cryogenic valves must operate consistently across repeated thermal cycles during flight without contributing to excessive boil-off or pressure instability. Advanced sealing architectures—combining metal-to-metal primary seats with compliant secondary seals—are being adopted to maintain tight shutoff while accommodating differential thermal contraction between valve components. As aerospace propulsion programs transition from demonstration to scaled deployment, suppliers capable of certifying cryogenic valves across both spaceflight and aviation duty cycles are positioned to secure long-duration, high-margin contracts.

Market Opportunity 2: Precision Cryogenic Valves for Quantum Computing and Medical Imaging

Beyond energy and aerospace, a quieter yet highly profitable opportunity is emerging in scientific and medical cryogenics, where precision flow control directly underpins system performance and reliability. Quantum computing infrastructure—particularly dilution refrigerators operating at millikelvin temperatures—requires miniature cryogenic valves with extremely fine flow resolution and minimal thermal leakage to preserve qubit coherence and system stability. The rapid expansion of quantum hardware investment through 2025 has translated into sustained demand for ultra-clean helium-handling valves capable of continuous operation without inducing vibration or parasitic heat ingress. A similar dynamic is unfolding in medical imaging. MRI systems remain heavily dependent on liquid helium cooling, and healthcare providers are increasingly prioritizing zero-boil-off architectures to mitigate helium scarcity and cost volatility. This shift is driving demand for valves that minimize leakage, reduce flash losses during maintenance, and enable closed-loop cryogenic circulation. In both quantum and medical applications, purchasing decisions are driven less by valve size and more by precision, reliability, and lifecycle performance, creating a defensible niche for manufacturers with micro-fabrication expertise, ultra-clean production capabilities, and deep cryogenic validation know-how.

Market Share Analysis: Cryogenic Valves Market

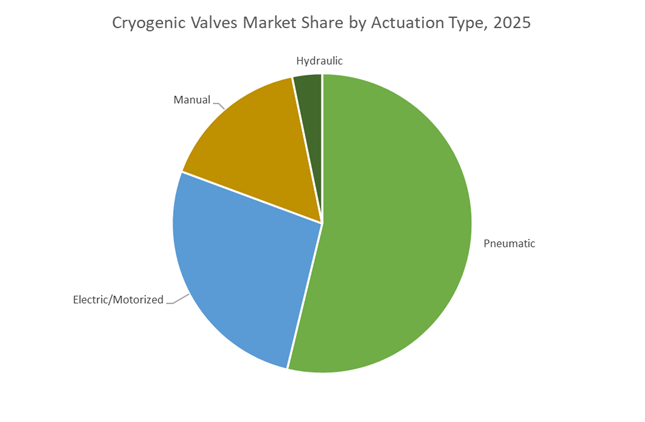

Market Share by Actuation Type: Pneumatic Actuators Dominate Safety-Critical Cryogenic Control

Pneumatic actuation commands around 50% of the global cryogenic valves market because it remains the only actuation technology that consistently meets the fail-safe, ultra-fast response, and extreme-temperature reliability demanded by LNG, liquid hydrogen, and industrial gas facilities. In 2025 procurement frameworks, safety engineering—not cost—defines buying decisions, and pneumatic systems outperform electric alternatives where loss of power must default to immediate valve closure. Leading manufacturers such as Vinco Valves and Velan now certify pneumatic cryogenic valves for 2,000 rapid open–close cycles at temperatures down to −196°C, addressing the fatigue risks associated with frequent loading and unloading operations at LNG terminals. Response speed is equally decisive: Samson and Emerson performance data show sub-10 millisecond emergency shut-off capability, a threshold critical for preventing pressure spikes during trip events in high-flow cryogenic pipelines. Structurally, the dominance of **spring-return “fail-close” architectures—accounting for roughly 85% of pneumatic orders in LNG applications—**reflects operator preference for mechanical safety over software-dependent redundancy. The segment’s leadership further extends into liquid hydrogen handling, where pneumatic designs incorporating welded stainless steel bellows maintain operational integrity down to −254°C, a regime that still disables most electric actuator lubricants. Collectively, these performance and safety advantages anchor pneumatic actuation as the default specification in cryogenic valve tenders globally.

Market Share by Application: Energy & Power Infrastructure Anchors Cryogenic Valve Demand

The Energy & Power segment accounts for approximately 35% of total cryogenic valve demand, making it the market’s primary revenue anchor as LNG, liquid hydrogen, and air separation infrastructure expands under global decarbonization mandates. Cryogenic valve selection in this segment is dictated by physics as much as policy: cooling natural gas to −162°C reduces its volume by nearly 600×, creating extreme pressure potential that requires valves certified to SIL-3 safety standards in 2025 LNG terminal designs. Demand momentum is being reinforced by a 42% surge in LNG infrastructure investment, driven by large-scale liquefaction and regasification projects across North America and the Middle East, including capacity expansions tied to export security and geopolitical energy realignment. At the component level, valve acceptance criteria have tightened sharply—manufacturers such as Flowserve and Mecco now report universal adoption of helium mass spectrometer testing, with allowable leakage thresholds approaching molecular-level zero (helium-tight) rather than traditional bubble-tight metrics. This shift is particularly critical for liquid hydrogen and high-purity gas service, where even nanoscopic leaks can compromise safety and economics. With U.S. LNG export capacity alone expanding by roughly 33% in 2025, Energy & Power applications continue to dictate volume growth, technical standards, and long-cycle replacement demand across the cryogenic valves market.

Competitive Landscape: Leading Cryogenic Valve Manufacturers and Strategic Market Positioning

The competitive landscape is defined by engineering expertise, global service networks, innovation in sealing materials, compliance with hydrogen-ready standards, and diversification across LNG and industrial gas applications. Companies are increasingly prioritizing R&D in ultra-low-temperature materials, additive manufacturing for precision components, and emission-reduction technologies to align with regulatory pressures and sustainability goals. Strategic acquisitions, such as Flowserve’s integration of Velan, and continuous product innovation across the market signify an industry driven by reliability, lifecycle performance, and application-specific customization.

Emerson Electric Co.: Automation Leadership in Cryogenic Flow Control

Emerson remains a dominant force through its Fisher portfolio, offering the easy-e™ Cryogenic Control Valve capable of throttling at temperatures down to −198°C. The company leverages its proven ENVIRO-SEAL™ packing systems to achieve industry-leading fugitive emission control, positioning Emerson as a preferred partner for LNG, chemical processing, and industrial gas applications. Its extensive catalog spans both large-format cryogenic control valves and compact solenoid valves, enabling integration into diverse instrumentation setups. With metal-to-metal seating and robust tight-shutoff capabilities, Emerson emphasizes lifecycle reliability and operational performance across ultra-low-temperature environments.

Flowserve Corporation: Expanded Portfolio Through Velan Integration

Flowserve significantly strengthened its cryogenic offerings following the July 2025 integration of Velan Inc., securing deep expertise in nuclear and LNG cryogenic valves. Its engineered products portfolio now spans ball, gate, globe, and check valves tailored for extreme temperatures and mission-critical isolation. Flowserve’s strong sustainability positioning-focused on reducing emissions and enhancing energy efficiency- aligns with the environmental goals of LNG liquefaction and regasification operators. The company’s broad installed base and engineering capabilities give it strong leverage in high-value global projects.

Parker Hannifin (Bestobell): Lightweight Precision For Industrial Gas and LNG

Parker Hannifin’s Bestobell division specializes exclusively in cryogenic valves for LNG transport, industrial gas storage, and high-purity aerospace applications. Its cryogenic ball valves are engineered to be 30% lighter than traditional full-bore designs, reducing load and supporting easier installation-an advantage widely recognized in LNG carriers and terminals. The company’s solutions maintain performance at −196°C, incorporating extended bonnet systems and PTFE/PCTFE seals to ensure leak-tight performance. Parker’s presence in LOX and LH₂ systems positions it as a critical supplier to future aerospace and hydrogen-fueling infrastructures.

Kitz Corporation: Japan’s Tier-1 Cryogenic Valve Engineering Powerhouse

KITZ delivers one of the widest product portfolios in the cryogenic space, offering stainless steel and carbon steel gate, globe, ball, and check valves optimized for LNG and ethylene plants. Its strong internal R&D programs in sealing technology and materials science support a catalog exceeding 90,000 engineered products, covering diverse global specifications. KITZ also operates cryogenic test facilities that replicate ultra-low-temperature conditions and perform low-emission methane tests aligned with API standards, enabling compliance across Europe, Asia, and the Americas. This globalized engineering approach strengthens its position as a trusted supplier for large EPC contractors.

Baker Hughes: High-Performance Cryogenic Solutions For LNG and Industrial Gas

Baker Hughes provides cryogenic valve solutions through its Masoneilan control valve line and Consolidated pressure relief valves, serving critical sectors such as ASUs, LNG facilities, and industrial gas transport. The company prioritizes lifecycle efficiency, ruggedized sealing performance, and low fugitive emissions, making its products highly suitable for large-scale energy projects. With a global network of service centers, Baker Hughes ensures maintenance continuity and operational safety. Its strong position in oil & gas naturally extends to LNG liquefaction and regasification markets, where project scale and reliability benchmarks are exceptionally high.

The United States continues to anchor global demand in the cryogenic valves market, underpinned by LNG export expansion and renewed aerospace momentum. Through late 2024 and into 2025, the U.S. Department of Energy (DOE) has overseen the progression of second-wave LNG export terminals, including Golden Pass LNG and Plaquemines LNG. These facilities are specifying high-pressure cryogenic ball and globe valves engineered for continuous service at −162 °C, with enhanced fugitive-emission performance to meet tightening EPA methane standards. The scale and redundancy requirements of U.S. LNG infrastructure are driving preference for triple-offset and metal-seated designs capable of sustaining extreme thermal cycling with near-zero leakage.

Beyond LNG, the aerospace and space exploration sector has emerged as a high-value demand node. With NASA’s Artemis missions and SpaceX Starship testing accelerating in 2025, procurement of liquid oxygen (LOX) and liquid hydrogen (LH₂) valves has surged. These applications demand micron-level tolerances to prevent contraction-induced seat failure at −253 °C. In parallel, CHIPS and Science Act–driven semiconductor reshoring has increased domestic installation of Air Separation Units (ASUs), pulling through demand for ultra-high-purity cryogenic valves used in electronics-grade nitrogen and argon production. Collectively, LNG, aerospace, and semiconductors position the U.S. as the highest-value cryogenic valve market globally.

China: “New Quality Productivity” and Industrial Gas Decarbonization

China is reshaping its cryogenic valves industry from volume manufacturing toward high-end, emissions-compliant flow control. In 2024, the country produced over 1,005 million tons of crude steel, requiring vast oxygen flows from ASUs. In response, the MIIT’s 2025 ultra-low-emission mandates are accelerating adoption of bubble-tight shutoff cryogenic valves to minimize oxygen losses and energy inefficiency in steelmaking operations. This regulatory pressure is elevating demand for precision-engineered valves rather than commoditized designs.

Energy security further reinforces growth. China’s expansion of LNG import infrastructure—illustrated by projects such as Wenzhou LNG Phase II—is driving demand for trunnion-mounted cryogenic ball valves optimized for high-cycle regasification duty. Simultaneously, the national hydrogen roadmap has triggered deployment of large-scale cryogenic hydrogen storage hubs in northern provinces. These projects require advanced valve metallurgy capable of mitigating hydrogen embrittlement, positioning cryogenic valves as a strategic enabler of China’s long-term clean energy transition.

India: National Green Hydrogen Mission and Port-Led Infrastructure

India has emerged as one of the fastest-growing cryogenic valves markets, propelled by the scale-up of the National Green Hydrogen Mission (NGHM). In October 2025, the Ministry of New and Renewable Energy (MNRE) designated Deendayal, V.O. Chidambaranar, and Paradip ports as primary green hydrogen hubs. These sites are initiating tenders for cryogenic valve manifolds and loading arms to support export-oriented liquid ammonia and hydrogen supply chains, creating immediate demand for corrosion-resistant and low-leakage valve systems.

Domestic manufacturing is also accelerating. In 2025, Indian engineering majors expanded public–private R&D programs focused on forged steel cryogenic valves for aerospace, nuclear, and chemical processing applications. This localization push is reducing dependence on imported European valves while aligning with India’s broader industrial self-reliance agenda. Additionally, the fertilizer sector’s transition toward green ammonia feedstocks—highlighted by a 2025 auction for 724,000 metric tons—is generating sustained demand for high-purity cryogenic control valves, reinforcing India’s role as a structurally expanding market.

Saudi Arabia: Localization, Gas Expansion, and Blue Ammonia Logistics

Saudi Arabia is positioning itself as a regional manufacturing hub for cryogenic valves, closely aligned with gas expansion and blue ammonia exports. In early 2025, Velan’s Saudi manufacturing facility recorded its first major order, supplying cryogenic valves for Saudi Aramco’s Jafurah gas field. This development reflects the scale of gas processing infrastructure underway, where thousands of valves are required for LNG, NGL, and hydrogen-adjacent services.

The Kingdom’s Vision 2030 strategy further amplifies demand through investments in blue ammonia production. In 2025, Aramco finalized offtake agreements with Japanese buyers, necessitating construction of cryogenic maritime loading terminals at King Abdullah Port. Importantly, the IKTVA localization mandate is incentivizing global valve OEMs to relocate casting, machining, and assembly operations to Saudi Arabia, making the country both a major demand center and an emerging supply base for cryogenic valves.

Germany: EU Hydrogen Backbone and Clean Industrial Transition

Germany stands at the center of Europe’s hydrogen infrastructure build-out, creating a high-specification market for cryogenic valves. In December 2025, the EU Innovation Fund earmarked €5.2 billion for net-zero technologies, including €1.3 billion dedicated to hydrogen auctions. German valve manufacturers reported record order intake in 2025, largely tied to hydrogen production, storage, and import terminals.

Strategic projects such as the Brunsbüttel FSRU conversion—which will handle ammonia imports and cracking into hydrogen—are driving replacement of legacy valve systems with ammonia-compatible cryogenic designs. In parallel, Germany’s proposal for over 9,100 km of hydrogen-capable pipelines, accelerated by the Net Zero Industry Act, is generating demand for bellows-sealed, zero-leakage cryogenic valves. Germany’s focus on regulatory rigor and emissions compliance makes it the technical benchmark market in Europe.

South Korea: Liquid Hydrogen Mobility and Maritime Leadership

South Korea is concentrating on liquid hydrogen mobility and shipbuilding, two segments with stringent cryogenic valve requirements. The Saemangeum Industrial Complex has become a focal point for hydrogen infrastructure, where domestic players are ramping up production of LH₂ refueling station components. These systems rely on ultra-low-temperature check valves and safety relief valves engineered for rapid cycling and absolute leak prevention.

In parallel, South Korea’s global leadership in shipbuilding is reinforcing demand. During 2024–2025, shipyards secured record orders for LNG carriers (LNGCs) and very large ammonia carriers (VLACs). These vessels specify extended-stem butterfly and globe valves to thermally isolate actuators from cryogenic fluids. The 2025 designation of cryogenic fluid handling as a national strategic technology, coupled with R&D tax credits of up to 50%, cements South Korea’s role as a high-innovation, maritime-focused cryogenic valve market.

2025 Strategic Matrix: Cryogenic Valves National Comparison

Cryogenic Valves Strategic Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Valve Type / Technology Focus

|

|

United States

|

LNG exports & aerospace

|

Second-wave LNG terminals and Artemis-scale LH₂ demand

|

High-pressure LH₂ & LOX cryogenic valves

|

|

China

|

Steel decarbonization & LNG imports

|

Ultra-low-emission ASU mandates

|

Bubble-tight shutoff cryogenic designs

|

|

India

|

National Green Hydrogen Mission

|

Three ports designated as hydrogen hubs

|

Forged steel and green ammonia cryogenic valves

|

|

Saudi Arabia

|

Localization & gas expansion

|

First major orders from Velan Saudi plant

|

IKTVA-compliant gas processing valves

|

|

Germany

|

EU hydrogen backbone

|

€5.2 bn EU clean transition funding

|

Bellows-sealed, zero-emission valves

|

|

South Korea

|

Maritime & hydrogen mobility

|

LH₂ refueling station commercialization

|

Extended-stem shipboard cryogenic valves

|

Cryogenic Valves Market Report Scope

Cryogenic Valves Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.6 Billion

|

|

Market Size (2035)

|

$10.6 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Valve Type (Ball, Butterfly, Gate, Globe, Check, Safety & Relief Valves), By Actuation Type (Manual, Pneumatic, Electric/Motorized, Hydraulic), By Material Type (Stainless Steel, Cast/Carbon Steel, Alloys, Forged Steel), By End-Use Industry (Energy & Power, Chemicals & Petrochemicals, Healthcare & Medical, Electronics & Semiconductors, Aerospace, Food & Beverage)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Emerson Electric Co., Flowserve Corporation, KITZ Corporation, Velan Inc., Baker Hughes, Samson AG, Parker Hannifin, The Weir Group PLC, Schlumberger, Neles, Crane CP&E, Bray International, IMI Critical Engineering, Powell Valves, Herose GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cryogenic Valves Market Segmentation

By Valve Type

- Ball Valves

- Butterfly Valves

- Gate Valves

- Globe Valves

- Check Valves

- Safety & Relief Valves

By Actuation Type

- Manual

- Pneumatic

- Electric/Motorized

- Hydraulic

By Material Type

- Stainless Steel

- Cast Steel / Carbon Steel

- Alloys (Monel, Inconel, Hastelloy)

- Forged Steel

By End-Use Industry

- Energy & Power

- Chemicals & Petrochemicals

- Healthcare & Medical

- Electronics & Semiconductors

- Aerospace

- Food & Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Cryogenic Valves Market

- Emerson Electric Co.

- Flowserve Corporation

- KITZ Corporation

- Velan Inc.

- Baker Hughes

- Samson AG

- Parker Hannifin

- The Weir Group PLC

- Schlumberger

- Neles

- Crane CP&E

- Bray International

- IMI Critical Engineering

- Powell Valves

- Herose GmbH

*- List not Exhaustive