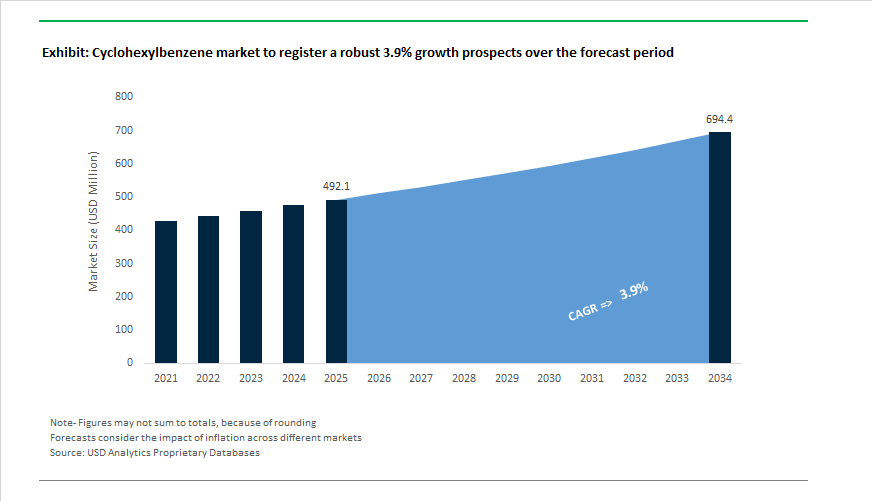

Cyclohexylbenzene Market to Reach $694.4 Million by 2034 at 3.9% CAGR Fueled by Battery Electrolytes, Electronics Demand, and Benzene Feedstock Dynamics

The Cyclohexylbenzene (CHB) Market is projected to grow from $492.1 Million in 2025 to $694.4 Million by 2034, reflecting a CAGR of 3.9%. Cyclohexylbenzene remains a critical benzene-derived intermediate used in lithium battery electrolytes, liquid crystal materials, specialty solvents, and phenolic synthesis. Market momentum is increasingly linked to electric vehicle battery safety enhancements, expansion of electronic-grade CHB capacity in Asia-Pacific, and evolving environmental compliance standards for aromatic hydrocarbons. While downstream textile and industrial solvent sectors face cyclical softness, high-purity and specialty-grade cyclohexylbenzene segments are demonstrating resilient structural demand.

Capacity rationalization and specialty-grade upgrades began accelerating in 2024, when regional producers such as Anhui Fulltime and Jintan Jinnuo Chemical completed debottlenecking projects for electronic-grade cyclohexylbenzene. These expansions specifically targeted South Korean and Chinese LCD manufacturing supply chains, where CHB serves as a precursor for 4-ethyl cyclohexyl benzoic acid used in advanced liquid crystal formulations. In parallel, Tokyo Chemical Industry (TCI Chemicals) introduced an ultra-high-purity CHB grade tailored to stringent impurity thresholds required in electronics and display technologies. Procurement digitization gained traction in September 2024, when Agilis and Evonik launched the AI-powered Alchemist commerce suite, enabling global buyers to optimize specification management and sourcing efficiency for specialty intermediates such as high-purity cyclohexylbenzene. Distribution networks expanded further in 2025, as Thermo Fisher Scientific and Merck (Sigma-Aldrich) broadened global agreements to include research-grade CHB, supporting intensified R&D activity in electrolyte additives and high-thermal-stability organic synthesis.

Demand diversification became more pronounced in May 2025, when the paints and coatings sector reported increased utilization of cyclohexylbenzene as a high-boiling solvent in UV-protective and corrosion-resistant formulations for aerospace and architectural applications. In mid-2025, several leading battery material manufacturers integrated high-purity CHB into standard Lithium Iron Phosphate (LFP) electrolyte formulations to improve thermal stability and overcharge tolerance, aligning with safety requirements for the 2026 generation of mass-market electric vehicles. Aerospace composite industrialization also reinforced the relevance of advanced aromatic intermediates in November 2025, when Syensqo and Bell Textron partnered to scale next-generation composite prepregs, reflecting broader value chain linkages involving phenolic and aromatic chemical systems.

Feedstock volatility influenced pricing dynamics entering January 2026, when cyclohexane and cyclohexylbenzene prices in China experienced a marginal increase driven by higher benzene costs and port congestion in Shanghai, despite seasonal weakness in textile and solvent demand. Sustainability and compliance pressures intensified in late 2025, as Asia-Pacific producers transitioned toward advanced catalytic hydrogenation systems and closed-loop solvent recovery to meet tightening 2026 environmental mandates from European and international regulators. Health profile updates in 2025 highlighted potential central nervous system and bone marrow risks associated with CHB exposure, prompting broader adoption of automated, closed-dosing systems across manufacturing facilities. Investment in regional specialty intermediate capacity advanced further in February 2026, when chemical leaders within India’s Dahej PCPIR secured nearly ₹360 crore for 2026 deployment projects, reinforcing domestic production of benzene-derived intermediates including cyclohexylbenzene. These developments position the market around high-purity electronics grades, battery electrolyte integration, solvent innovation in coatings, and cost-sensitive benzene feedstock economics across Asia-Pacific.

Trends and Opportunities in the Global Cyclohexylbenzene Market

Captive Integration and Process Optimization in Phenol Production Chains

- Phenol producers are increasingly redesigning their process configurations to reduce exposure to merchant market volatility and improve energy efficiency. A major strategic shift underway is the adoption of integrated benzene to cyclohexylbenzene to phenol pathways as an alternative to conventional cumene based routes. This approach allows producers to better control intermediate flows and reduce dependency on acetone co-product economics, which have shown pronounced cyclicality in recent years.

- In early 2025, leading phenol manufacturers across Asia Pacific, a region accounting for close to 48% of global phenol output, announced increased use of selective hydrogenation technologies. These processes maximize cyclohexylbenzene yield while minimizing unwanted by-products, enabling more stable phenol production even when downstream acetone demand weakens. The strategic benefit lies in smoothing operating rates and improving plant level profitability in volatile demand environments.

- A clear example of this integration-driven strategy is the upcoming phenol complex developed by Haldia Petrochemicals. The company finalized timelines for its 300,000 tons per annum phenol facility scheduled for commissioning in the first quarter of 2026. The project is designed around captive intermediates, ensuring that cyclohexylbenzene and related aromatics remain within a closed loop system. This approach directly addresses the supply disruptions experienced in European merchant markets during 2024 and reflects a broader industry pivot toward regional self sufficiency.

Rising Importance as a Battery Safety Additive in Lithium Ion Cells

- Beyond phenol, cyclohexylbenzene is gaining prominence as a critical safety additive in high energy density lithium ion batteries. As battery pack sizes exceed 100 kilowatt hours and operating voltages rise, thermal runaway mitigation has become a non negotiable design requirement. Studies published in mid 2025 demonstrated that the combined use of cyclohexylbenzene and biphenyl significantly expands the safety voltage threshold of graphite lithium cobalt oxide cells to nearly 12 volts.

- This synergistic mechanism works by forming a protective polymeric film on the cathode surface under overcharge conditions, effectively interrupting the electrochemical reaction before catastrophic failure. As a result, cyclohexylbenzene is increasingly specified as a functional safety component rather than an optional additive, particularly in long range electric vehicles and energy storage systems.

- Purity standards are tightening in parallel. Demand for 99.9% electronic grade cyclohexylbenzene is accelerating as manufacturers such as INEOS and Mitsui Chemicals refine distillation and purification processes. High purity material is essential for lithium iron phosphate and nickel cobalt manganese chemistries, where trace impurities can accelerate electrolyte degradation and undermine long term safety certifications. This trend directly supports the automotive sector’s dual objective of lowering battery cost per kilowatt hour while strengthening safety performance.

Feedstock Role in High Temperature, Low Dielectric Advanced Polymers

- Cyclohexylbenzene is emerging as a valuable precursor in the synthesis of advanced polymers such as polybenzoxazole and polybenzimidazole, which are critical for aerospace, defense, and next generation communications infrastructure. Technical evaluations released in August 2025 show that PBO films derived from cyclohexyl based monomers can achieve dielectric constants as low as 2.13. This represents an approximate 25% reduction compared with conventional polyimides, making these materials highly attractive for high speed printed circuit boards and semiconductor packaging used in 5G and emerging 6G systems.

- Another growth driver is thermal budget optimization during device fabrication. The development of photosensitive PBO precursors that cure at lower temperatures is enabling their use in temperature sensitive semiconductor components. This is particularly relevant for gallium arsenide heterojunction bipolar transistors, where excessive heat can damage device architecture. Cyclohexylbenzene based intermediates allow protective polymer layers to be applied without exceeding critical thermal limits, expanding adoption in advanced electronics manufacturing.

Scaffold for CNS Focused Pharmaceuticals and Selective Agrochemicals

- The unique dual ring structure of cyclohexylbenzene is also opening opportunities in medicinal chemistry and crop protection. In pharmaceutical research, the cyclohexyl aromatic scaffold is being leveraged to enhance lipophilicity and improve blood brain barrier penetration. Patent activity in 2024 and 2025, including filings such as US11192849B2, highlights the use of cyclohexylbenzene motifs in compounds targeting ferroptosis modulation and excitotoxicity. These mechanisms are central to emerging therapies for neurodegenerative disorders such as Alzheimer’s and Parkinson’s disease, where central nervous system access remains a key challenge.

- In agrochemicals, cyclohexylbenzene derivatives are being applied to improve formulation stability and selectivity. By fine tuning metabolic resistance through the cyclohexyl group, manufacturers are developing herbicides that achieve efficacy at lower application rates. This aligns with the European Union Farm to Fork strategy, which targets a 50% reduction in chemical pesticide use by 2030. As regulatory scrutiny intensifies, cyclohexylbenzene based chemistries offer a pathway to meet performance and sustainability objectives simultaneously.

Cyclohexylbenzene Market Share and Segmentation Insights

Application Segmentation: Battery Additives Dominate as Specialty Chemical Uses Expand

Battery additives account for 45% of cyclohexylbenzene demand in 2025, reflecting its critical role as an electrolyte additive in high-voltage lithium-ion batteries. Cyclohexylbenzene improves overcharge protection and cycle life, directly supporting electric vehicle production and stationary energy storage systems. Chemical intermediates represent the second-largest application, leveraging cyclohexylbenzene in specialty synthesis pathways for agrochemicals, pharmaceuticals, and performance materials. Solvents and penetrants form a substantial segment, utilizing its high boiling point and strong solvency in industrial cleaners, penetrant oils, and textile dye carriers where controlled evaporation is essential. Organic synthesis remains a smaller but strategically important niche, supporting academic and industrial R&D as a reaction medium and precursor for novel chemical entities.

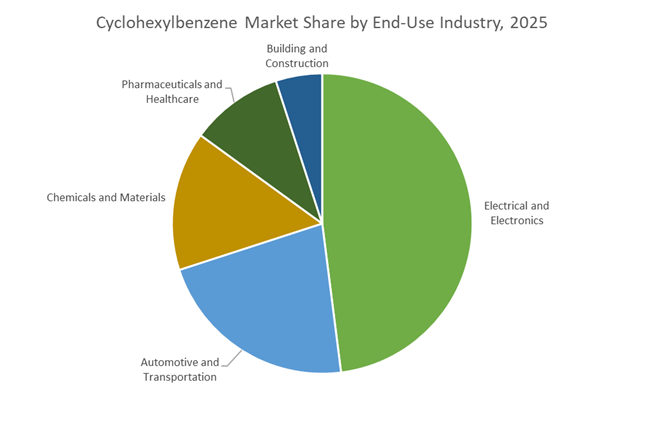

End-Use Industry Breakdown: Electronics Lead Consumption as EV Supply Chains Accelerate Growth

Electrical and electronics account for 48% of cyclohexylbenzene consumption, anchored by lithium-ion battery manufacturing and supported by additional use in capacitor impregnation and specialty electronic solvents requiring high purity and thermal stability. Automotive and transportation is a rapidly growing segment, tightly linked to electric vehicle expansion and rising demand for advanced electrolyte additives. Chemicals and materials represent a stable base market, supplying intermediates and formulated solvents for industrial applications. Pharmaceuticals and healthcare utilize cyclohexylbenzene in API synthesis and regulated processing environments where specific solvency characteristics are required. Building and construction remains a smaller segment, with niche use in specialty sealants, concrete curing compounds, and construction chemicals that benefit from cyclohexylbenzene’s penetration and slow evaporation profile.

Competitive Landscape of the Cyclohexylbenzene Market

The Cyclohexylbenzene (CHB) Market is shaped by battery-grade purity requirements, vertically integrated benzene supply chains, and accelerating demand from lithium-ion batteries, heat transfer fluids, pharmaceuticals, and electronic solvents. Leading producers are differentiating through electronic-grade CHB, ultra-low moisture control, and localized capacity expansions aligned with EV manufacturing growth.

JFE Chemical drives battery-grade cyclohexylbenzene through steel-integrated feedstocks

JFE Chemical Corporation holds a strategic leadership position by leveraging crude benzene recovered directly from coke oven gas at its own steel plants, ensuring cost-stable and secure CHB production. The company specializes in Electronic Grade cyclohexylbenzene with ultra-low moisture and acid content, tailored for advanced electrolyte formulations. JFE is a dominant supplier to the anode and electrolyte segments of the Asia-Pacific lithium-ion battery market, benefiting from proximity to regional gigafactories. Its “Mobility & Battery” strategy prioritizes materials supporting automotive carbon neutrality, positioning CHB as a critical intermediate for EV energy storage. Deep vertical integration remains JFE’s core competitive moat in high-purity battery chemicals.

Schultz Canada Chemicals advances thermal-fluid applications with CHB-based formulations

Schultz Canada Chemicals focuses on functional CHB applications, producing SCHULTZ® S760 high-temperature heat transfer fluid where cyclohexylbenzene provides exceptional boiling point stability and thermal endurance. The company operates a highly integrated refining model from oil-derived feedstocks, enabling tight quality control across production. During 2025–2026, Schultz expanded distribution across North America and Europe to capture rising demand for battery safety and thermal management chemicals. Its automated control systems enable consistent high-purity isomer production across extreme operating ranges from −4°F to 660°F. Schultz’s technical leadership positions it strongly in industrial heat transfer fluids and next-generation energy infrastructure.

Merck KGaA sets reagent-grade standards for battery and research cyclohexylbenzene

Merck KGaA anchors the premium reagent segment with Battery Grade cyclohexylbenzene launched in late 2025, offering ≥99% purity with water content below 100 ppm and acidity under 200 ppm to prevent electrolyte degradation. Through its SAFC® platform, Merck supports custom synthesis and scale-up for pharmaceutical customers using CHB as a chemical intermediate. The company also supplies isotope-labeled CHB for forensic and life science research, a niche but high-margin category. Its “Digital Science” strategy integrates AI-driven supply chain tracking to enable just-in-time delivery for battery manufacturers, reinforcing Merck’s role as the global benchmark for ultra-high-purity CHB.

Thermo Fisher scales industrial cyclohexylbenzene for pharma and recycling markets

Thermo Fisher Scientific commands a significant share of the Standard Grade cyclohexylbenzene market in 2026, supplying high-boiling-point solvent volumes to pharmaceutical and semiconductor ecosystems. The company expanded Alfa Aesar and Acros Organics portfolios to include bulk CHB totes exceeding 1,000 liters, supporting chemical recycling and API production scale-up. Thermo Fisher’s global e-commerce and logistics infrastructure enables next-day delivery to research hubs in more than 150 countries. CHB is widely deployed in API synthesis as both penetrant and intermediate, positioning Thermo Fisher as a critical volume supplier bridging laboratory development with industrial commercialization.

TCI Chemicals strengthens mid-scale CHB supply for displays and pharma synthesis

TCI Chemicals specializes in mid-scale production of cyclohexylbenzene derivatives, offering ≥98.0% phenylcyclohexane refined through advanced distillation to remove sulfur traces that degrade battery catalysts. The company emphasizes synthesis innovation, supplying functionalized CHB variants for liquid crystal display materials and specialty electronics. With an organic reagent catalog exceeding 30,000 products, TCI enables bundled sourcing of CHB alongside catalysts and co-solvents. In early 2026, TCI opened a new logistics center in India to serve rapidly expanding pharmaceutical and generic drug manufacturing, strengthening its footprint across South Asia’s high-growth specialty chemicals corridor.

Changzhou Junchi Chemical powers China’s EV-driven CHB consumption

Changzhou Junchi Chemical is a pivotal regional supplier as China accounts for nearly 47% of global cyclohexylbenzene demand. Following a 2025 capacity upgrade at its Jiangsu facility, Junchi emerged as one of the largest producers of industry-grade CHB for coatings, adhesives, and rubber applications. Over 60% of its output now feeds the domestic LFP battery supply chain, directly supporting China’s EV manufacturing surge. The company employs proprietary low-pollution catalytic pathways to minimize alkylation by-products and recently introduced CHB-based antioxidant blends that enhance durability in lightweight automotive plastics.

China: Battery Safety Regulation and AI-Enabled Process Efficiency

China’s cyclohexylbenzene industry in 2025 is being reshaped by battery safety mandates and rapid digitalization of aromatic hydrogenation processes. In late 2025, the Ministry of Industry and Information Technology issued updated safety guidelines for high-energy-density batteries used in Next-Generation Vehicles. These guidelines explicitly encourage the incorporation of overcharge protection additives such as cyclohexylbenzene to mitigate thermal runaway risks. As a result, CHB has moved from being a niche solvent to a strategically important battery electrolyte stabilizer, particularly for fast-charging and high-voltage lithium-ion systems. This policy-driven demand is strengthening long-term offtake visibility for domestic producers supplying electronic-grade material.

On the supply side, major chemical clusters in Jiangsu and Zhejiang have integrated AI-optimized catalytic hydrogenation systems throughout 2025. These systems improve the selective conversion of biphenyl into cyclohexylbenzene, lowering energy consumption by an estimated 15% while improving batch consistency. Feedstock security has also improved following SABIC’s confirmation in November 2025 that its Fujian Petrochemical Complex is scaling up high-purity aromatics output, ensuring stable benzene and cyclohexane availability for downstream CHB synthesis. Meanwhile, the Ministry of Commerce has maintained strict anti-dumping oversight on petrochemical intermediates, protecting expanding domestic producers such as Anhui Fulltime and Jintan Jinnuo as they target electronic-grade solvent markets.

United States: Environmental Risk Review and Pharmaceutical Upside

In the United States, cyclohexylbenzene demand is increasingly linked to pharmaceutical innovation and environmental compliance. During mid-2025, FDA-supported research initiatives highlighted CHB as a critical intermediate in the synthesis of novel organic molecules for oncology applications. The emphasis on high-purity derivatives for clinical trial precursors has elevated quality requirements, positioning cyclohexylbenzene as a specialty input rather than a commodity aromatic. This pharmaceutical pull is complemented by federal interest in safer chemical transformation pathways.

Regulatory pressure is shaping production practices. Under the EPA’s 2025–2026 TSCA work plan, updated risk profiles for bicyclic hydrocarbons are pushing manufacturers toward closed-loop solvent recovery and low-emission processing. In response, U.S. specialty chemical firms accelerated the deployment of nickel-on-silica catalysts in 2025 to convert carcinogenic biphenyl into higher-value cyclohexylbenzene. This approach aligns environmental remediation goals with value-added manufacturing, allowing producers to simultaneously reduce hazardous inventories and expand CHB supply for regulated applications such as pharmaceuticals and advanced coatings.

South Korea: Electronic-Grade Scaling for Batteries and Semiconductors

South Korea’s cyclohexylbenzene industry is tightly coupled with its advanced electronics and battery ecosystems. In December 2025, LG Chem and Samsung SDI announced collaborative R&D programs aimed at developing thermally stable electrolyte formulations for next-generation fast-charging batteries. These 2026-focused projects prioritize cyclohexylbenzene as a co-solvent to maintain dielectric strength and thermal stability under high current loads, reinforcing its role in premium battery chemistries.

Parallel to battery-driven demand, producers at the Ulsan National Industrial Complex expanded late-2025 output of 99.9% purity cyclohexylbenzene. This material is increasingly required by domestic LCD and semiconductor manufacturers, where solvent stability and low impurity profiles are critical for yield control. The convergence of battery and semiconductor applications positions South Korea as a high-purity consumption hub rather than a volume-driven market.

India: PLI-Led Aromatics Expansion and Infrastructure Coatings

India’s cyclohexylbenzene market is developing through policy-backed capacity expansion and infrastructure-driven consumption. Under the Production Linked Incentive scheme, domestic majors such as Reliance Industries and Atul Ltd broadened their aromatics portfolios in 2025, explicitly targeting cyclohexylbenzene for its dual use as a pharmaceutical intermediate and a high-performance penetrant. This localization strategy reduces reliance on imports while enabling downstream integration into specialty chemicals and drug intermediates.

Infrastructure standards are reinforcing demand. The 2025 update to the PM Gatishakti National Master Plan prioritized durable protective coatings for coastal and high-humidity infrastructure. High-boiling solvents such as cyclohexylbenzene are increasingly specified in corrosion-resistant paint systems due to their penetration characteristics and thermal stability. This combination of policy support and infrastructure usage is steadily anchoring industrial-grade CHB demand within India.

Germany: Compliance-Driven Sustainability and Precision Chemistry

Germany’s cyclohexylbenzene industry reflects the country’s broader emphasis on regulatory compliance and precision chemistry. In 2025, the European Chemicals Agency tightened documentation requirements for high-boiling aromatics under REACH, prompting German producers to innovate around sustainability credentials. In response, BASF introduced mass-balanced cyclohexylbenzene variants that incorporate bio-circular feedstocks, enabling customers to lower the carbon footprint of downstream synthesis without altering process performance.

At the fine chemicals end of the spectrum, Merck KGaA expanded its Darmstadt-based catalog for 2026 to include high-purity cyclohexylbenzene grades. These products are positioned as stable solvents for advanced organic synthesis, materials science, and laboratory-scale innovation. Germany’s market thus emphasizes compliant, high-value applications over bulk consumption.

Snapshot Summary: Cyclohexylbenzene Industry by Country

Cyclohexylbenzene Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Focus

|

Industry Direction

|

|

China

|

EV battery safety mandates

|

Electronic-grade CHB, AI-optimized hydrogenation

|

Policy-led scale and efficiency

|

|

United States

|

Pharma research and TSCA compliance

|

High-purity intermediates, closed-loop processing

|

Environmental remediation plus value addition

|

|

South Korea

|

Batteries and semiconductors

|

Ultra-high-purity CHB

|

Electronics-led specialization

|

|

India

|

PLI incentives and infrastructure coatings

|

Dual-use industrial and pharma grades

|

Localization and downstream integration

|

|

Germany

|

REACH compliance and fine chemicals

|

Mass-balanced and lab-grade CHB

|

Sustainability and precision chemistry

|

Cyclohexylbenzene Market Report Scope

Cyclohexylbenzene market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$492.1 Million

|

|

Market Size (2034)

|

$694.4 Million

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Purity Grade (Electronic Grade, Industrial Grade, Pharmaceutical Grade), By Application (Battery Additives, Chemical Intermediates, Solvents and Penetrants, Organic Synthesis), By Technology (Catalytic Hydrogenation, Alkylation, Dehydrogenation), By End-Use Industry (Electrical and Electronics, Automotive and Transportation, Pharmaceuticals and Healthcare, Chemicals and Materials, Building and Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Exxon Mobil Corporation, Eastman Chemical Company, Mitsubishi Chemical Group Corporation, Reliance Industries Limited, LG Chem Ltd., Anhui Fulltime Specialized Solvents Co., Ltd., Jintan Jinnuo Chemical Co., Ltd., Schultz Canada Chemicals Ltd., Merck KGaA, Tokyo Chemical Industry Co., Ltd., Jiangsu Zhongneng Chemical Technology Co., Ltd., Hefei TNJ Chemical Industry Co., Ltd., SABIC, Wanhua Chemical Group Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cyclohexylbenzene Market Segmentation

By Purity Grade

- Electronic Grade

- Industrial Grade

- Pharmaceutical Grade

By Application

- Battery Additives

- Chemical Intermediates

- Solvents and Penetrants

- Organic Synthesis

By Technology

- Catalytic Hydrogenation

- Alkylation

- Dehydrogenation

By End-Use Industry

- Electrical and Electronics

- Automotive and Transportation

- Pharmaceuticals and Healthcare

- Chemicals and Materials

- Building and Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Cyclohexylbenzene Industry

- BASF SE

- Exxon Mobil Corporation

- Eastman Chemical Company

- Mitsubishi Chemical Group Corporation

- Reliance Industries Limited

- LG Chem Ltd.

- Anhui Fulltime Specialized Solvents Co., Ltd.

- Jintan Jinnuo Chemical Co., Ltd.

- Schultz Canada Chemicals Ltd.

- Merck KGaA

- Tokyo Chemical Industry Co., Ltd.

- Jiangsu Zhongneng Chemical Technology Co., Ltd.

- Hefei TNJ Chemical Industry Co., Ltd.

- SABIC

- Wanhua Chemical Group Co., Ltd.

*- List not Exhaustive