Market Overview: Thermal Runaway Mitigation, Conductive Carbon Innovation, and Solid-State Transition Accelerate Battery Additives Market

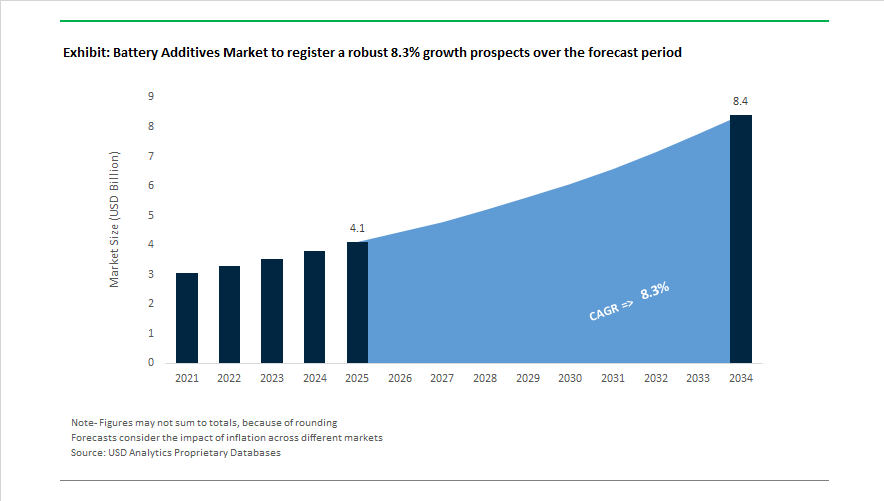

The Battery Additives Market is valued at $4.1 billion in 2025 and is projected to reach $8.4 billion by 2034, expanding at a CAGR of 8.3%. Growth is supported by rapid scale-up of lithium-ion battery additives, conductive carbon additives, electrolyte stabilizers, thermal runaway suppressants, cathode active material enhancers, graphene dispersions, and safety-focused electrolyte formulations used in EV batteries, grid energy storage systems, and advanced consumer electronics. Safety innovation intensified in October 2024 when LG Chem unveiled its temperature-responsive Safety Reinforced Layer, an additive material engineered to increase resistance during overheating events and interrupt short-circuit propagation. The same year, Ascend Performance Materials secured regulatory approval in April 2024 for Trinohex Ultra, an electrolyte stabilizing additive that neutralizes degradation byproducts in high-voltage cells. Also in November 2024, Graphene Manufacturing Group launched SUPER G slurry, a graphene-based conductive additive targeting lower charge-transfer resistance and improved cycle life for next-generation electronics batteries.

Industrial partnerships and manufacturing innovations shaped 2025 developments. March 2025 marked LG Chem’s start of mass production of precursor-free cathodes using additive-enabled synthesis routes that reduce emissions and lower cathode production costs. In June 2025, Envalior introduced Stanyl SN-PURE succinonitrile electrolyte additive to enhance cathode surface protection and thermal stability in nickel-rich EV batteries. Collaboration expanded in July 2025 when BASF and CATL signed a framework agreement for advanced cathode materials and recycling technologies. Conductive additive performance advanced in October 2025 as Cabot Corporation launched LITX 95F carbon for grid-scale storage reliability, followed by November 2025 commercialization of PRINTEX kappa 100 acetylene black from Orion. Electrolyte breakthroughs continued when Asahi Kasei licensed its acetonitrile-based electrolyte technology in November 2025, reducing internal resistance by 60% in high-power LFP cells. Structural materials integration also rose after Evonik doubled long-chain polyamide capacity in China in November 2025, strengthening battery housing and thermal management supply chains.

The shift toward next-generation chemistries and solid-state architectures became evident during late-stage 2025. In August 2025, BASF delivered its first customized cathode materials and additive packages for semi-solid-state batteries to WELION New Energy, signaling commercial readiness for hybrid electrolyte systems. Regional supply realignment dates back to 2024, when Reliance New Energy completed acquisition of Lithium Werks assets, including proprietary additive formulations for cobalt-free LFP technology. By the end of 2025, additive science increasingly addressed multi-functional performance, including thermal management, conductivity optimization, electrolyte stabilization, and cost-efficient cathode synthesis, positioning advanced battery additives as a central lever for improving EV range, battery safety, and large-scale energy storage reliability.

Trends and Opportunities Reshaping the Battery Additives Market

Market Trend: Shift Toward High-Voltage Electrolyte Additives Optimized for NMC811 and LNMO Platforms

The next phase of EV competitiveness depends on increasing driving range without adding battery mass or cost. Nickel-rich cathodes such as NMC811 and high-voltage LNMO are being engineered to operate above 4.5V, which creates accelerated oxidative breakdown at the cathode–electrolyte interface. This is directly elevating the need for electrolyte additives that can stabilize high-energy systems.

As of December 2025, additive packages using (3-aminopropyl)triethoxysilane (APTS) and Lithium Bis(fluorosulfonyl)imide (LiFSI) have benchmarked retention of 92% capacity after 350 cycles for LNMO spinel systems. For comparison, additive-free formulations typically fall below usable thresholds before 100 cycles. On the cathode side, manufacturers are pairing chemical stabilizers with physical coatings such as ALD-deposited LiF. These hybrid systems are now used in 18650 cell formats reporting energy densities above 320 Wh/kg while suppressing gas evolution during long-term storage at elevated temperatures.

From an OEM perspective, these capabilities are not optional. Automakers are tying procurement decisions to additive performance metrics because high-voltage compatibility directly influences cycle life warranties, thermal safety, and total pack architecture.

Market Trend: Silicon Anode Stabilizers Move Beyond FEC Toward Elastic and Polymer-Functional Additives

While silicon is viewed as the fastest pathway to increase battery energy density, its 300% volumetric expansion during cycling remains a central failure mode. Fluoroethylene Carbonate (FEC) continues to dominate electrolyte additive demand, yet its consumption rate during cycling adds long-term impedance and increases cost of ownership.

Intellectual property filings from LG Energy Solution and CATL in Q3 2025 demonstrate a strategic pivot toward concave silicon-carbon composite architectures, supported by polymeric binders and borate-salt additives that create elastic, mechanically self-adjusting SEI layers. These designs are now supporting more than 1,500 stable cycles at greater than 10% silicon loadings—an inflection point that makes commercial silicon adoption economically viable.

Emerging research is qualifying “polymer brush” surface-grafting additives, which permanently anchor stabilizing molecules to the silicon surface. This eliminates the need for constant replenishment during cycling and sharply reduces impedance rise, a critical parameter for premium EV battery platforms where fast charging is a core consumer feature.

Market Opportunity: Interface-Stabilizing Additives for Lithium-Metal Solid-State Batteries

Solid-state batteries (SSBs) represent the highest-value growth frontier in the Battery Additives Market, but dendritic lithium growth is a commercial roadblock without interfacial chemical solutions. Additives engineered to form stable interphases between lithium metal and solid electrolytes are now positioned as the enabling layer for SSB commercialization.

In August 2025, published research introduced a “methylurea-assisted” electrolyte system capable of reaching 99.93% Coulombic efficiency over 4,500 cycles while forming a uniform 20 nm amorphous interphase. These results signal that additive innovation may be the deciding breakthrough that determines which OEM reaches market scale first.

Demand timing is accelerating. Nissan and multiple Japanese automakers are targeting solid-state powered vehicles by 2028, and pilot-scale trials show anode-free lithium-metal cells can already reach 320 Wh/kg with chemical prelithiation support. This is creating a clear commercial runway for companies able to supply lithium metal stabilizers at automotive scale and price points.

Market Opportunity: Aqueous Binder and Dispersion Chemistry for Low-Cost, Sustainable Electrode Manufacturing

Manufacturers are aggressively adopting water-based processing to eliminate N-Methyl-2-pyrrolidone (NMP), reduce energy use, and de-risk regulatory exposure. This shift is creating entirely new revenue pools for additives that improve slurry rheology and protect aluminum collectors from corrosion during water-based cathode processing.

As of 2025, 41% of the anode binder market has already moved to water-based systems such as CMC and SBR. Technical announcements suggest cathode migration will follow, as “water-proofed” high-nickel resin systems enter commercial availability. If adopted at scale, water-based processing can reduce electrode production costs by up to 15 percent, improving battery pack economics for both EVs and stationary energy storage.

The increasing use of high-surface-area conductive additives—such as Carbon Nanotubes (CNTs)—requires sophisticated dispersants to avoid particle agglomeration in aqueous slurries. AI-driven formulation platforms are now being used to design multi-functional additives that simultaneously enhance electrical conductivity, slurry stability, and coating uniformity, making dispersant chemistry a major new differentiator for gigafactory-scale production.

Battery Additives Market Share and Segmentation Insights

Market Share by Type: Conductive and Electrolyte Additives Anchor Performance-Critical Demand

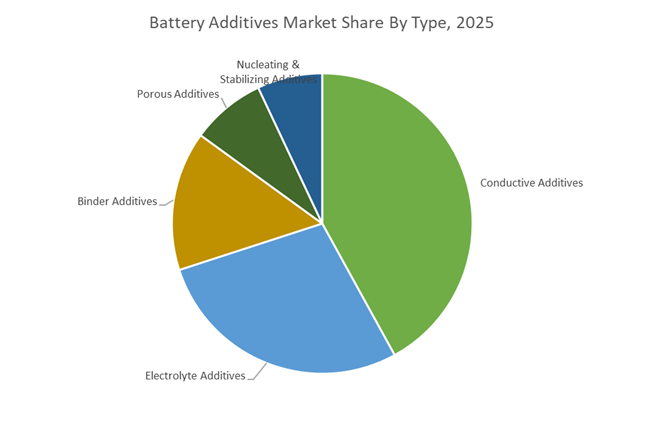

Conductive additives command the largest share of the Battery Additives Market, accounting for 42% in 2025, reflecting their indispensable role in enhancing electron transport efficiency across lithium-ion battery electrodes, particularly in electric vehicle battery packs. Carbon nanotubes and carbon black remain the dominant materials, supporting higher power density and faster charge acceptance. Electrolyte additives hold the second-largest position, driven by growing requirements for battery safety, extended cycle life, and stable performance under extreme temperatures. Binder additives, led by PVDF (polyvinylidene fluoride), are essential for electrode cohesion and mechanical integrity, although alternative binders are gaining traction amid supply chain volatility. Porous additives are emerging rapidly in solid-state batteries and high-energy-density cells to optimize ion mobility, while nucleating and stabilizing additives represent a niche but expanding segment, especially for silicon-based anodes and advanced lithium battery architectures.

Market Share by End Use Sector: Automotive Electrification Drives Volume-Led Additive Consumption

The automotive sector dominates battery additives consumption with a 52% market share in 2025, powered by accelerating global EV adoption and aggressive investments in high-performance lithium-ion battery manufacturing. Additives in this segment prioritize fast charging capability, higher energy density, and thermal management to meet electric mobility requirements. Consumer electronics remains a stable demand center, supported by continuous innovation in smartphones, laptops, and wearables that require thinner, lighter, and longer-lasting batteries. Energy Storage Systems, spanning grid-scale and residential deployments, are expanding rapidly as renewable energy integration intensifies, with additives optimized for safety and long cycle life. Industrial and robotics applications represent a smaller but rising segment, fueled by growth in automated guided vehicles, material handling equipment, and power tools, where high-power battery performance and durability are increasingly critical.

Competitive Landscape Analysis of the Battery Additives Market

The battery additives market is characterized by intense innovation across conductive carbons, binders, dispersing agents, electrolyte additives, and safety-enhancing performance materials. Leading suppliers are competing on slurry rheology optimization, high-voltage stability, fast-charging capability, thermal runaway prevention, and sustainability compliance aligned with EV battery regulations. Strategic partnerships with gigafactories, investments in AI-driven material modeling, and expansion into energy storage systems are reshaping supplier positioning. Market leaders are also differentiating through circular integration, low-carbon formulations, and system-level solutions that improve electrode integrity, manufacturing efficiency, and long-term battery performance across electric vehicles and stationary storage applications.

BASF advances battery performance through intelligent dispersions and PCF transparency

BASF has positioned itself as the chemical architect of the battery additives ecosystem, leveraging expertise in dispersions and stabilizers to enhance electrode processing and energy density. In early 2026, the company introduced next-generation dispersing agents at Plastindia that reduce cathode slurry viscosity, enabling higher solid loading and thicker electrodes. Its Lupamin and Sokalan portfolios now emphasize wetting agents that minimize coating defects in high-speed gigafactory lines. BASF’s Global Digital Hub in Hyderabad applies AI-driven molecular modeling to simulate additive behavior in ultra-high nickel NMC chemistries. A core strategic pillar is product carbon footprint transparency, supporting automakers in meeting EU Battery Passport sustainability requirements.

Cabot Corporation dominates conductive carbon additives for fast-charging batteries

Cabot Corporation leads the global market for conductive carbon additives, supplying the critical electron transport network inside lithium-ion electrodes. In January 2026, Cabot secured a multi-year agreement with PowerCo SE to deliver advanced conductive carbons for European EV battery production. Its LITX conductive carbon blacks and ATHLOS carbon nanostructures enable fast charging and high power density in performance batteries. A key differentiator is dispersion engineering, with pre-dispersed formulations that simplify slurry mixing while ensuring uniform electrode conductivity. Beyond automotive, Cabot is expanding into long-duration energy storage, where its additives significantly improve cycle life in large-scale stationary grid batteries.

Arkema strengthens PVDF binder leadership for high-voltage lithium-ion cells

Arkema remains a specialty materials leader in PVDF binders and functional additives essential for electrode cohesion under extreme electrochemical stress. In February 2026, Arkema signed an MoU with Senior to co-develop next-generation coatings for semi-solid and high-voltage batteries. Its Kynar PVDF and Incellion acrylic additives now support low-temperature cell assembly processes that reduce manufacturing energy consumption. Recent controlled deposition coatings enhance microscopic adhesion, preventing active material peeling in silicon-rich anodes. Arkema’s core strength lies in high-voltage stability, with 2026 formulations engineered to perform reliably above 4.5V, supporting next-generation long-range electric vehicle platforms.

Evonik Industries delivers safety-focused performance additives and separator solutions

Evonik Industries specializes in performance additives that improve battery safety, thermal stability, and mechanical resilience. In February 2026, the company accelerated global HTPB production with a new German facility to meet rising demand for advanced battery adhesives and sealants. Its AEROSIL fumed silica and AEROXIDE fumed alumina function as separator coatings and internal stabilizers that mitigate thermal runaway and short circuits. Evonik also expanded POLYVEST ST-E 60 production in Shanghai, supplying high-purity polybutadiene for vibration-resistant battery packs in heavy-duty electric trucks. Strategically, Evonik is evolving into a system solution provider, combining additives with integrated separator coating technologies.

Solvay optimizes electrolyte chemistry and fluorinated binder systems

Solvay is a major force in fluorinated additives and high-purity electrolyte components, focusing on preserving chemical integrity inside lithium-ion cells. As part of its 2025 to 2026 restructuring, Solvay invested €25 million to convert its Bad Wimpfen site into a global hub for battery chemicals. Its Solef PVDF binders and electrolyte additives such as F1EC help form stable SEI layers that prevent electrolyte degradation. Uniquely, Solvay produces both PVDF binders and LiTFSI salts, enabling internal chemical synergy that can extend battery life by up to 15%. In early 2026, the company exited legacy organics to prioritize EV-focused materials.

Umicore integrates circular additives with advanced cathode technologies

Umicore combines cathode active materials leadership with specialized battery additives, bridging material science and recycling. Its defining advantage is circular integration, offering Europe’s first closed-loop model that manufactures battery materials and recovers them through advanced recycling. Umicore supplies IntraCu additives, originally developed for semiconductor packaging, now adapted for smart current collectors in 2026 EV batteries. In late 2025, it introduced high-performance copper(II) oxide solutions that improve conductivity while reducing collector weight. The company’s Clean Mobility strategy embeds safety-by-design additives directly into cathode structures, enhancing thermal stability and lowering fire risks in dense urban electric mobility environments.

India Battery Additives Market: Fiscal Acceleration, Mineral Security, and Grid-Scale Pull-Through

India’s battery additives industry is entering a decisive scale-up phase, anchored by fiscal stimulus, mineral cost relief, and accelerating grid storage deployments. In February 2025, the Government of India announced a ten-fold increase in allocations for the Production-Linked Incentive Scheme for Advanced Chemistry Cell Battery Storage, lifting support from ₹15.42 crore to ₹155.76 crore. This sharp fiscal acceleration is improving project bankability for domestic manufacturers of electrolyte stabilizers, conductive additives, and anti-corrosive formulations used across lithium-ion and hybrid chemistries. Complementing incentives, the National Manufacturing Mission launched in late 2025 established a governance framework to support MSMEs producing battery motors, controllers, and specialty additives, with the explicit objective of raising domestic value addition and shortening qualification cycles for locally sourced formulations.

Input cost competitiveness has improved materially. Effective April 2025, India fully exempted Basic Customs Duty on 25 critical minerals including cobalt powder and lithium-ion scrap, directly lowering feedstock costs for high-performance additive synthesis and recycling-derived precursors. Demand-side pull-through is strengthening via grid storage. JSW Energy and Tata Power received letters of award in late 2025 for 1,500 MWh of standalone Battery Energy Storage Systems, catalyzing immediate demand for electrolyte stabilizers and corrosion inhibitors. Technology integration is also deepening. Vikram Solar announced backward integration into battery cell manufacturing with a 7.5 GWh facility that embeds proprietary conductive additives to meet FY29 targets. Finally, recycling-linked demand is expanding alongside manufacturing. The Ministry of New and Renewable Energy reported 100 GW of solar manufacturing capacity by August 2025, necessitating parallel scale-up of additives engineered for long-life lead-acid and lithium-ion hybrid systems used in storage and balancing applications.

China Battery Additives Market: Feedstock Assurance, Polymer Science Scale, and Integrated Verbund Advantage

China’s battery additives industry is reinforcing global leadership through feedstock assurance policies and polymer science scale. Effective January 1, 2026, China implemented provisional import tariff reductions on 935 products, explicitly targeting recycled black powder for lithium-ion batteries. Announced by the Customs Tariff Commission of the State Council, these cuts stabilize input costs for downstream additive synthesis and strengthen China’s role as the primary processing hub for secondary battery materials supporting EV and stationary storage supply chains.

Capacity additions are synchronized with advanced chemistry. BASF confirmed operational commissioning of its expanded advanced additives plant in Nanjing in late 2025, featuring a state-of-the-art line for controlled free radical polymerization dispersants used in binders and conductive networks. This expansion is complemented by BASF’s €10 billion Zhanjiang Verbund, which entered the core startup phase in early 2026 and provides integrated supply for high-performance polymer dispersions used in battery binders and protective coatings. Together, tariff relief and Verbund integration underpin cost stability, quality consistency, and rapid scale for China’s additive ecosystem.

South Korea Battery Additives Market: Mission-Led Materials Roadmap and Transparency Mandates

South Korea is aligning policy, transparency, and OEM collaboration to advance next-generation battery additives. In 2025, the Ministry of Science and ICT designated secondary battery materials as a top-level technology priority, explicitly targeting PFAS-free binder systems and next-generation cathode stabilizers. This mission-led roadmap is accelerating qualification of safer, higher-performance additives across domestic cell platforms.

Regulatory transparency is becoming a market differentiator. Following a December 2025 legislative push, South Korea is implementing a digital Battery Passport via QR codes that requires additive suppliers to disclose carbon footprint and recycled content data. This elevates lifecycle performance and favors suppliers with low-impact chemistries and traceable inputs. Government-led R&D support is deepening collaboration. The Special Act on the Science and Technology Strategy enacted in late 2025 provides package support for securing global minerals and fostering open innovation between additive suppliers and automotive OEMs such as Hyundai Motor Company and Kia, compressing development timelines for binder and stabilizer systems.

United States Battery Additives Market: Domestic Incentives, Silicon Anodes, and Solid-State Readiness

The United States battery additives industry is advancing through domestic production incentives and chemistry tailored for fast charging and safety. In late 2025, NEO Battery Materials commenced production at its 250 MWh Battery Foundry, commercializing silicon-enhanced additives that enable ultra-fast charging for drones and robotics. This signals early adoption of silicon-anode enabling chemistries within specialized applications.

Policy support is reinforcing localization. Under Inflation Reduction Act guidelines updated for 2026, U.S.-based additive firms are receiving enhanced tax credits for PFAS-free electrolyte additives that support Made in America compliance across EV and storage supply chains. Innovation is extending to solid-state readiness. Major U.S. chemical producers reported 2025 launches of viscosity modifiers engineered for solid-electrolyte interfaces, targeting a 30% reduction in thermal runaway risk. These developments position U.S. suppliers at the intersection of safety regulation and next-generation cell architectures.

France and Germany Battery Additives Market: Solvent-Free Processing and PFAS-Free Inflection

France and Germany are shaping Europe’s transition to cleaner electrode manufacturing and PFAS-free additives. In September 2025, Arkema inaugurated a battery dry coating laboratory in France focused on Kynar® PVDF and Incellion® acrylic polymers. The facility advances solvent-free electrode coating, eliminating evaporation steps and materially reducing energy consumption during manufacturing.

Market momentum is shifting decisively away from PFAS. In early 2026, European industry bodies and IDTechEx forecast that non-PFAS battery additives will reach a critical inflection point, driven by adoption of polyacrylic acid and polyethylene oxide systems. This transition is aligning regulatory expectations with scalable chemistries for binders and electrolyte modifiers across European gigafactory pipelines.

Country-Level Strategic Snapshot: Battery Additives Industry

Battery Additives Market County Level Snapshot

|

Country / Region

|

Strategic Emphasis

|

Key Developments

|

|

India

|

Fiscal incentives and mineral cost relief

|

PLI scale-up, duty exemptions, BESS awards, proprietary conductive additives, recycling-linked demand

|

|

China

|

Feedstock assurance and polymer scale

|

Tariff cuts on black powder, Nanjing CFRP dispersants, Zhanjiang Verbund integration

|

|

South Korea

|

Mission-led R&D and transparency

|

PFAS-free binders, Battery Passport, OEM co-innovation

|

|

United States

|

Domestic incentives and safety chemistry

|

Silicon-anode additives, IRA tax credits, solid-state SEI modifiers

|

|

France / Germany

|

Solvent-free processing and PFAS exit

|

Dry coating labs, PVDF and acrylic polymers, PAA and PEO adoption

|

Battery Additives Market Report Scope

Battery Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$8.4 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Type (Conductive Additives, Electrolyte Additives, Binder Additives, Porous Additives, Nucleating and Stabilizing Additives), By Functionality (Capacity Retention and Cycle Life Improvement, Thermal Stability and Flame Retardancy, Electrical Conductivity Enhancement, Corrosion Resistance and Overcharge Protection), By Battery Chemistry (Lithium Ion, Lead Acid, Next Generation Batteries), By End Use Sector (Automotive, Consumer Electronics, Energy Storage Systems, Industrial and Robotics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Arkema, Evonik Industries, Mitsubishi Chemical Group, Cabot Corporation, Sumitomo Chemical, LG Chem, Solvay, Umicore, Chemours, Wacker Chemie, NEO Battery Materials, Imerys, Asahi Kasei, Clariant

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Battery Additives Market Segmentation

By Type

- Conductive Additives

- Electrolyte Additives

- Binder Additives

- Porous Additives

- Nucleating and Stabilizing Additives

By Functionality

- Capacity Retention and Cycle Life Improvement

- Thermal Stability and Flame Retardancy

- Electrical Conductivity Enhancement

- Corrosion Resistance and Overcharge Protection

By Battery Chemistry

- Lithium Ion

- Lead Acid

- Next Generation Batteries

By End Use Sector

- Automotive

- Consumer Electronics

- Energy Storage Systems

- Industrial and Robotics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Battery Additives Industry

- BASF

- Arkema

- Evonik Industries

- Mitsubishi Chemical Group

- Cabot Corporation

- Sumitomo Chemical

- LG Chem

- Solvay

- Umicore

- Chemours

- Wacker Chemie

- NEO Battery Materials

- Imerys

- Asahi Kasei

- Clariant

*- List not Exhaustive