Diamond Coatings Market Overview: High-Hardness CVD Diamond, DLC Tribology & Copper-Diamond Thermal Solutions Redefining Industrial Performance

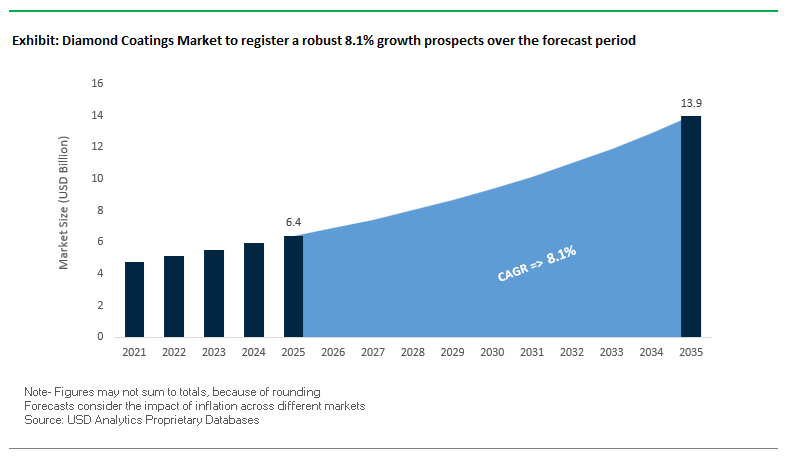

The Diamond Coatings Market, valued at USD 6.4 billion in 2025 and projected to reach USD 13.9 billion by 2035 at a strong 8.1% CAGR, is undergoing a rapid performance-driven expansion as OEMs, advanced manufacturers, and high-tech sectors prioritize extreme hardness, thermal conductivity, wear life, and material purity across mission-critical applications. CVD diamond coatings—achieving ≈80–100 GPa Vickers hardness—now underpin aerospace machining, semiconductor tooling, and composite drilling by delivering 200%+ tool-life gains and superior edge retention. At the same time, Diamond-Like Carbon (DLC) coatings continue to scale across automotive, aerospace, and medical sectors due to their ultra-low friction, chemical inertness, and proven biocompatibility, enabling precision components and long-life surgical instruments.

A new frontier is emerging in copper-diamond thermal composites, which address severe heat bottlenecks in AI accelerators, high-performance computing (HPC) systems, and GaN RF power modules by offering thermal conductivities far exceeding traditional TIMs and metal substrates. As industries transition toward higher power density, tighter dimensional tolerances, and application-specific purity levels (e.g., quantum-grade NV center control in synthetic diamond), procurement and R&D teams must increasingly evaluate suppliers based on production scalability, defect-density control, deposition uniformity, and advanced material engineering capabilities. Over the next decade, diamond coatings will shift from being niche performance enhancers to becoming foundational materials enabling next-generation electronics, quantum technologies, aerospace efficiency, and industrial reliability.

Market Analysis: product launches, capacity expansion and quantum/thermal breakthroughs

The Diamond Coatings market’s 2024–2025 activity shows coordinated product innovation, capacity investment and technology partnerships pushing diamond films from specialized tooling into thermal, environmental and quantum markets. In October 2025, Oerlikon Balzers launched Baldia Varia, a CVD diamond coating tuned for machining abrasive composites and technical ceramics - a direct commercial response to OEM needs in aerospace and e-mobility for extended tool life and repeatable surface finish. September 2025 saw a major quantum materials milestone when IonQ announced advances in synthetic diamond devices (enabled by Element Six / Lightsynq supply), accelerating diamond’s role in practical quantum networking and sensing.

Through August 2025, industrial diamond manufacturing scaled as Chinese producers optimized HPHT reactors for higher throughput and energy efficiency - easing raw material constraints for CVD feedstock and PCD tool blanks. May 2025 featured IHI Ionbond’s strategic expansion of DLC capacity near Toulouse, targeting aerospace and medical demand where ta-C coatings must meet AS9100 and ISO 13485 standards. Earlier in April 2025, Bosch and Element Six formed a joint venture to integrate synthetic diamond into quantum sensors, signaling vertical moves to commercialize diamond’s quantum and sensing potentials. January 2025 brought Element Six’s Copper-Diamond thermal composite launch for AI/HPC and GaN RF heat dissipation - a pragmatic response to skyrocketing chip power densities. Finally, the September 2024 defense research contract awarded to Element Six under the U.S. UWBGS program highlights long-term strategic investment in diamond for ultra-wide bandgap semiconductor enabling technologies.

Trends and Opportunities Accelerating Material Innovation and Application Expansion in the Diamond Coatings Market

Trend 1: Industrial Standardization of CVD Diamond Tooling as High-Volume Machining Moves Toward Ultra-Long Tool Life and Thermal Stability

A defining trend in the diamond coatings market is the broad transition toward CVD diamond-coated tools, driven by OEM qualification programs in aerospace and automotive manufacturing. As machining systems encounter increasingly abrasive materials—such as aluminum alloys, carbon fiber composites (CFRP), and hybrid lightweight structures—traditional carbide tools fail to maintain productivity, precision, and consistency.

CVD diamond tools demonstrate 50–100× longer operational life than uncoated carbide when machining CFRP, enabling production runs of 1,200 components vs. only 20 parts with conventional tooling. This dramatic gap in durability reduces machine downtime, tool change frequency, and scrap rates—critical for high-volume aerospace trim operations or EV chassis machining.

Diamond’s extremely low coefficient of friction (0.05–0.10) reduces cutting forces by 50–70%, mitigating thermal damage in composite matrices and preserving fiber integrity. This is essential for meeting aerospace standards such as sub-0.5 mm delamination and maintaining surface roughness < Ra 3.2 μm across extended machining campaigns. As OEMs increasingly mandate these parameters as baseline qualification criteria, CVD diamond coatings are becoming a requirement rather than an optional productivity enhancer.

Trend 2: Integration of Diamond Heat Spreaders Becomes Essential for GaN, SiC, and Advanced RF/Power Electronics Thermal Management

As semiconductor power densities surge in RF systems, EV inverters, and data-center processors, diamond’s exceptional thermal conductivity (up to 2000 W/(m·K)) uniquely positions it as a strategic heat-spreading material. Even leading power semiconductor materials—GaN and SiC—face thermal bottlenecks that limit areal power density, device lifetime, and efficiency unless paired with diamond.

GaN-on-diamond architectures have demonstrated 40–45% reductions in junction temperature, enabling up to 3× higher RF power density compared to GaN-on-SiC. This performance improvement directly influences radar module lifetime, base-station reliability, and satellite power efficiency.

Thermal challenges extend beyond RF. In 2024, data center CPUs reached 150 W/cm² heat flux, a 50% increase since 2020, placing unprecedented stress on traditional copper and graphite thermal solutions. Diamond’s superior heat-spreading performance is emerging as an essential enabler for next-generation server cooling and AI accelerator architectures.

In aerospace, the integration of diamond heat spreaders reduces module thermal resistance by 30% and supports a 20% reduction in cooling-system mass, directly contributing to More-Electric Aircraft objectives through weight savings and improved thermal margin.

Opportunity 1: DLC and ta-C Coatings as Critical Enablers of Ultra-Low-Friction Automotive Powertrain and EV Drivetrain Efficiency

The automotive industry’s aggressive push toward higher energy efficiency—across both internal combustion engines (ICEs) and electric drivetrains—creates a powerful adoption pathway for Diamond-Like Carbon (DLC) and tetrahedral amorphous carbon (ta-C) coatings. These coatings offer ultra-low friction, extreme hardness, and high wear resistance, making them indispensable for improving component lifespan and reducing system energy losses.

In ICEs, nearly 50% of total friction originates from the piston assembly. Hydrogen-free ta-C coatings on piston rings materially reduce these losses and translate into measurable fuel-efficiency gains, even under lubricated operating conditions.

In EV transmissions, DLC-coated gears demonstrate up to 50% reduction in frictional losses, which can increase vehicle driving range by 0.9–1.1 km per full battery cycle in urban scenarios. DLC’s ultra-low friction coefficient (0.05–0.20) parallels PTFE (Teflon) performance but with vastly superior load-bearing capability, making it ideal for high-load e-axle gears, bearings, and thrust surfaces.

As OEMs prioritize friction reduction, acoustic quietness, and long-term reliability, DLC and ta-C coatings emerge as scalable, cost-effective solutions for next-generation powertrain optimization.

Opportunity 2: Nanocrystalline Diamond Coatings Unlock New Performance Benchmarks in Biomedical Implants and Surgical Tools

Nanocrystalline Diamond (NCD) coatings represent one of the highest-value growth areas in the diamond coatings market because of their intrinsic biocompatibility, chemical inertness, ultra-high hardness, and anti-bacterial characteristics. These properties align with unmet performance needs in orthopedic implants, surgical instruments, neural electrodes, and long-term biomedical interfaces.

In orthopedic joints, NCD-coated articulating surfaces achieve the lowest recorded wear factors in pin-on-disk measurements—as low as 4.9×10⁻¹⁰ mm³/Nm—representing orders-of-magnitude improvement over conventional titanium or cobalt-chromium alloys. This reduction in wear debris dramatically extends implant lifespan and reduces osteolysis risk.

NCD also resists bacterial colonization more effectively than standard medical metals, reducing infection risks, a critical driver for hospitals seeking to avoid revision surgeries. Additionally, NCD forms an inert barrier preventing the release of metallic ions, addressing biocompatibility concerns associated with legacy metal-on-metal implants.

Diamond Coatings Market Share Analysis

Market Share by Coating Type: Diamond-Like Carbon (DLC) Leads with 55.4% Share

Diamond-Like Carbon (DLC) coatings dominate the Diamond Coatings Market with a 55.4% share in 2025, underscoring their position as the most commercially scalable and broadly adopted solution for friction reduction, wear resistance, and surface durability across industrial, automotive, and consumer applications. DLC’s leadership is driven by its low-temperature deposition compatibility, excellent adhesion to metals and alloys, and ability to deliver near-diamond performance at significantly lower cost compared to CVD diamond films. These advantages make DLC the default choice for high-volume production environments—ranging from cutting tools and engine components to medical instruments and consumer electronics—where reliability, coating uniformity, and throughput efficiency are critical. While DLC anchors market volume, the coating hierarchy reflects growing specialization: CVD diamond films remain essential for mission-critical extreme-environment applications such as semiconductor heat spreaders, aerospace components, and ultra-high-wear industrial tooling; nanodiamond coatings provide a flexible, lower-cost intermediate option for enhancing tribological performance through sprayable or electrophoretic processes. The segmentation highlights a layered market structure in which DLC drives industrial scalability, CVD diamond delivers peak performance, and nanodiamond solutions support niche engineering needs.

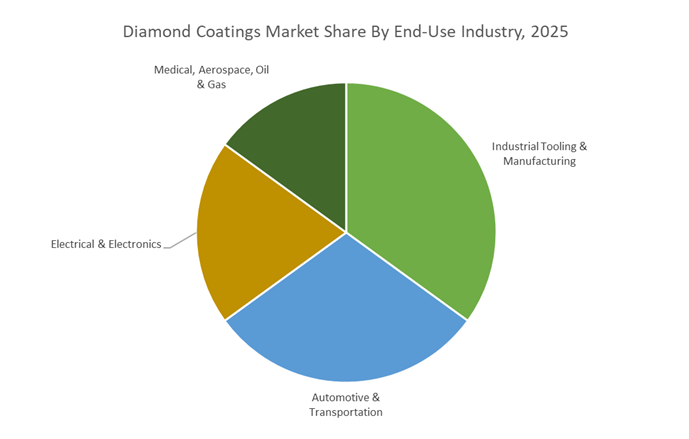

Market Share by End-Use Industry: Industrial Tooling & Manufacturing Leads with 36.9% Share

Industrial Tooling & Manufacturing represents the largest end-use segment with a 36.9% share in 2025, reflecting its foundational role in validating and scaling diamond coating technologies. This segment leads because diamond-coated tools—whether DLC, CVD diamond, or nanodiamond—offer dramatically extended tool life, reduced downtime, superior machining precision, and improved performance in abrasive or high-friction environments, directly translating into cost savings for manufacturers. Continued adoption of automated machining, high-speed cutting, micro-tooling, and precision forming processes further increases demand for durable diamond-coated surfaces across metals, composites, ceramics, and semiconductor materials. At the same time, other end-use sectors contribute to market diversification: automotive and transportation leverage high-volume DLC deposition for fuel system components, powertrain parts, and sliding interfaces; electrical and electronics increasingly adopt CVD diamond for thermal management in 5G, EV power modules, and high-performance computing; and medical, aerospace, and oil & gas rely on premium diamond coatings for biocompatibility, corrosion resistance, extreme wear protection, and mission-critical reliability.

Country Analysis: Global Diamond Coatings Market Innovation Hubs

China: Scaling Synthetic Diamond Production and Localizing High-Tech CVD Diamond Films for Electronics and Industrial Tooling

China’s diamond coatings market is expanding rapidly due to strong government support for synthetic diamonds, CVD diamond films, and superhard materials, which are officially classified under the “new materials” strategic category. This classification unlocks tax incentives, R&D grants, and industrial policy benefits, enabling China to dominate global HPHT diamond production while accelerating its ascent in high-purity CVD diamond films for semiconductor and precision applications. Regions such as Guangxi are emerging as dedicated CVD production hubs, focusing on large-area, high-purity diamond films that complement the industrial HPHT capabilities centered in Henan. This dual-track production strategy positions China to scale both bulk synthetic diamonds and high-performance CVD crystals essential for industrial and microelectronics use.

China’s rapidly expanding electronics and semiconductor industry is a major consumer of diamond-coated tools, diamond heat spreaders, and diamond wafer carriers, which improve thermal management and machining performance in chip fabrication. Government-backed industrial clusters—such as Zhecheng County, the “Diamond Capital”—offer subsidies, industrial park incentives, and talent programs that consolidate China’s superhard materials ecosystem. To improve product quality and compete globally, Chinese manufacturers are increasingly adopting Plasma-Assisted CVD (PACVD) and other advanced deposition techniques to enhance coating uniformity, adhesion strength, and wear resistance across industrial tooling, automotive components, and precision manufacturing sectors.

United States: Diamond Coatings for Semiconductor Thermal Management and High-Reliability Defense Platforms

The United States is focusing on high-performance, specialized applications for CVD diamond films and ultra-hard coatings, driven by the need to overcome thermal bottlenecks in wide-bandgap (WBG) semiconductors, aerospace components, and defense systems. A major milestone occurred in June 2025, when Diamond Technologies Inc. (DTI) acquired the full asset portfolio and Miraj Diamond® intellectual property from Akhan Semiconductor. This acquisition consolidates a critical U.S. IP base for diamond film deposition, substrate integration, and thermal carrier technologies, enabling commercial acceleration of diamond heat spreaders and wafer substrates designed for SiC and GaN power electronics.

The U.S. aerospace and defense sectors are also significant adopters of diamond coatings, integrating them into turbine blades, missile components, infrared sensors, and high-wear flight systems to reduce friction, enhance oxidation resistance, and maintain structural stability in extreme thermal environments. Meanwhile, federal R&D agencies—potentially including DARPA and DOE—continue to fund research into ultra-nanocrystalline diamond (UNCD) films for next-generation MEMS, electrochemical systems, and micro-scale actuators. This positions the United States as a global center for diamond coating innovation in thermal management, extreme-environment electronics, and strategic defense materials.

Europe (Germany/Switzerland/UK): Advancing DLC and Diamond Coatings for E-Mobility Efficiency and Medical-Grade Biocompatibility

Europe leads in applying Diamond-Like Carbon (DLC) and diamond coatings across high-value industries such as e-mobility, aerospace machining, medical implants, and renewable energy devices, supported by strict EU performance standards. A major development came in June 2025, when Oerlikon Balzers launched Baldia Varia, a next-generation CVD diamond coating engineered for high-precision machining of CFRP and composite materials. This innovation addresses Europe’s fast-growing demand for high-efficiency machining solutions in lightweight automotive and aerospace structures—sectors where surface integrity, tool life, and productivity gains are mission-critical.

European manufacturers are also advancing hybrid coating technologies that merge DLC layers with plasma electrolytic oxidation (PEO) treatments, creating coatings with superior wear resistance, lower friction, and enhanced corrosion protection—ideal for lightweight aluminum alloys used in EV powertrains. In healthcare, Europe is a global leader in supplying biocompatible diamond coatings for orthopedic implants, surgical tools, and diagnostic equipment, leveraging the material’s extreme hardness, chemical inertness, and bio-inert properties. Additionally, the EU’s Horizon Project DIAMOND (ending November 2025) has demonstrated the viability of diamond-based carbon electrodes in stabilizing perovskite solar cells, indicating significant future potential for diamond-related materials in renewable energy systems and photovoltaic durability.

Japan: Precision Diamond Tooling Leadership and Strategic Investment in Diamond Semiconductor Devices

Japan maintains a global reputation for excellence in precision machining, advanced tooling, and high-purity materials, driving strong demand for CVD diamond-coated cutting tools used in the aerospace, automotive, and electronics manufacturing sectors. Japanese toolmakers rely extensively on high-uniformity diamond coatings to ensure exceptionally long tool life, dimensional accuracy, and the ability to machine hard, abrasive materials like CFRP and high-silicon aluminum alloys. Companies such as Sumitomo Electric continue to strengthen their materials supply chain through acquisitions and strategic investments, reinforcing Japan’s leading position in superhard tool technologies.

Japan is also emerging as a strategic hub for diamond semiconductor innovation, with the government supporting next-generation high-temperature, high-radiation diamond devices for extreme environments. In 2025, the Japanese government backed Ookuma Diamond Device Co., Ltd. in constructing a dedicated facility in Fukushima to manufacture diamond semiconductor components. These devices target high-stress applications such as nuclear decommissioning, where conventional Si, SiC, and GaN devices cannot withstand radiation flux or extreme thermal loads. This positions Japan at the forefront of the emerging diamond semiconductor materials market, complementing its leadership in precision tooling and high-quality CVD materials.

Competitive Landscape: suppliers scaling CVD, DLC and engineered diamond composites for industrial and high-tech markets

The competitive field is led by vertically integrated CVD producers, coating service specialists, reactor/equipment providers and niche CVD/DLC houses. Competitive advantage derives from demonstrated coating uniformity, thickness control on complex geometries, high thermal conductivity composites, and the ability to supply quantum-grade diamond with controlled NV center densities. Below is an overview and company-level insight aligned to procurement and partner selection criteria.

Diamond coatings suppliers are evaluated on: deposition method (CVD, HFCVD, HPHT), maximum depositable thickness, thickness uniformity across large substrates, stress control, adhesion to complex tool geometries, post-processability, and ability to deliver certified medical/aerospace coatings.

Element Six - World leader in synthetic diamond materials and quantum-grade CVD innovations

Element Six is the preeminent producer of engineered CVD diamond and PCD products, supplying optical, heat-spread and quantum-grade diamonds. Its recent Copper-Diamond thermal composite (Jan 2025) directly targets AI/HPC and GaN RF thermal bottlenecks; its Diamox™ boron-doped electrodes earned a green-technology award (Sep 2025) for wastewater treatment. The Bosch joint venture (Apr 2025) and prior defense research selections (Sep 2024) underline Element Six’s strategic pivot into quantum sensing and ultra-wide bandgap semiconductor enablement. For buyers seeking quantum-grade purity and high-K thermal substrates, Element Six’s scale, IP and multi-industry integration capability are decisive advantages.

Oerlikon Balzers - Industrial coating innovator scaling BALDIA diamond solutions for aerospace and composites machining

Oerlikon Balzers extends its BALDIA portfolio with Baldia Varia (Oct 2025) - a CVD diamond coating engineered for extreme abrasion and composite stack machining. Balzers’ global service network and coating equipment expertise make it a prime partner for aerospace and automotive Tier-1 tool houses seeking reproducible gains in tool life and surface integrity. Its coatings combine ultra-high hardness with process control to reduce tool change frequency and improve first-pass yield.

IHI Ionbond - DLC and ta-C specialist expanding capacity to serve aerospace and medical device markets

IHI Ionbond’s investment in DLC capacity (May 2025) near Toulouse strengthens its ability to deliver certified ta-C coatings (Tetrabond™ Plus) for aluminum machining, implants, and aerospace components. Ionbond’s focus on quality systems (AS9100, ISO13485) and proven ta-C low-friction performance (μ < 0.1) positions it as a reliable supplier for regulated industries requiring biocompatible, wear-resistant coatings with validated lifecycle data.

CVD Diamond Corporation - Specialist supplier of PCD/CVD-coated cutting tools and precision micro-tools

CVD Diamond Corporation focuses on depositing uniform polycrystalline diamond films onto cutting inserts, micro-endmills and drills for high-efficiency machining of graphite, CFRP and non-ferrous alloys. Its tailored film geometries and industrial tooling expertise make it a strong choice for manufacturers needing high throughput and consistent micro-geometry retention when machining advanced aerospace and e-mobility components.

SP3 Diamond Technologies LLP - Hot-Filament CVD reactor & custom coating services for thick, uniform films

SP3 provides HFCVD reactor technology and contract coating services capable of depositing thick (3–50 µm), uniform diamond films on complex geometries with ±10% variation on 300 mm wafers. Its HFCVD strength lies in adaptability for large-area, high-uniformity coatings and bespoke mechanical property tuning (stress, compressive/tensile balance), which is critical for scaling diamond films into thermal spreaders, tooling, and specialty industrial components.

Diamond Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2035)

|

$13.9 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Coating Type (CVD Diamond Films, Diamond-Like Carbon Coatings, Nanodiamond Coatings), By Deposition Technology (Chemical Vapor Deposition, Physical Vapor Deposition, Plasma-Assisted CVD), By End-Use Industry (Industrial Tooling, Automotive, Electrical & Electronics, Medical & Healthcare, Aerospace & Defense, Oil & Gas), By Substrate Material (Metals, Ceramics, Composites, Polymers), By Function (Wear & Abrasion Resistance, Low Friction, Thermal Management, Corrosion Resistance, Biocompatibility, Electrical Insulation)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Element Six, Oerlikon Balzers, Sandvik AB, Kyocera Corporation, IHI Ionbond AG, CemeCon AG, Advanced Diamond Technologies Inc., II-VI Incorporated, Sumitomo Electric Industries Ltd., Diamond Coatings Inc., Techno-Coat GmbH, Diamond Technologies Inc., Zhongnan Diamond Co. Ltd., Hyperion Materials & Technologies, Mustad & Son AS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diamond Coatings Market Segmentation

By Coating Type

- CVD Diamond Films

- Diamond-Like Carbon (DLC) Coatings

- Nanodiamond Coatings

By Deposition Technology

- Chemical Vapor Deposition

- Physical Vapor Deposition

- Plasma-Assisted Chemical Vapor Deposition (PACVD)

By End-Use Industry

- Industrial Tooling

- Automotive

- Electrical & Electronics

- Medical & Healthcare

- Aerospace & Defense

- Oil & Gas

By Substrate Material

- Metals (Steel, Carbide, Titanium Alloys)

- Ceramics (Al₂O₃, Si₃N₄)

- Composites (CFRP, Glass Fiber)

- Polymers (Specialty Plastics)

By Function

- Wear & Abrasion Resistance

- Low Friction / Dry Lubrication

- Thermal Management (Heat Dissipation)

- Corrosion Resistance

- Biocompatibility

- Electrical Insulation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diamond Coatings Market

- Element Six

- Oerlikon Balzers

- Sandvik AB

- KYOCERA Corporation

- IHI Ionbond AG

- CemeCon AG

- Advanced Diamond Technologies, Inc.

- II-VI Incorporated

- Sumitomo Electric Industries, Ltd.

- DIAMOND COATINGS, Inc.

- Techno-Coat GmbH

- Diamond Technologies Inc.

- Zhongnan Diamond Co., Ltd.

- Hyperion Materials & Technologies

- Mustad & Son AS

*- List not Exhaustive