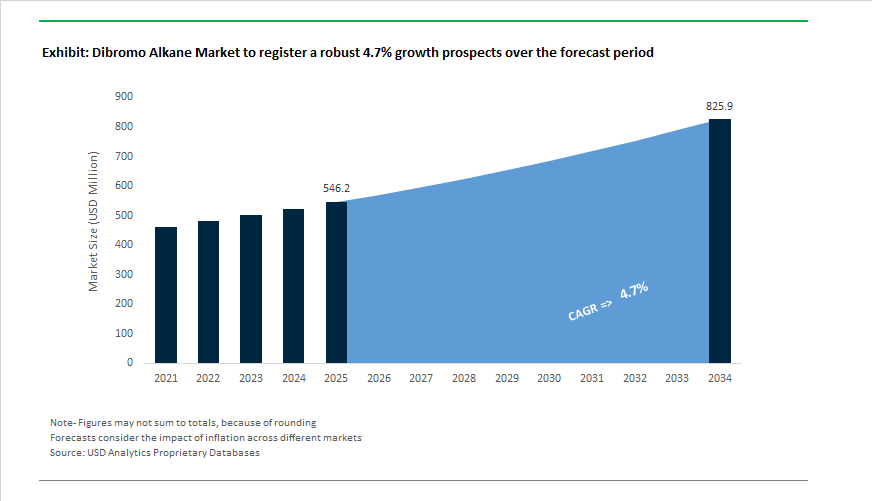

Dibromo Alkane Market to Reach $825.8 Million by 2034 at 4.7% CAGR Amid Bromine Supply Realignments and High-Purity Pharma Demand

The Dibromo Alkane Market is projected to grow from $546.2 Million in 2025 to $825.8 Million by 2034, registering a CAGR of 4.7%. Dibromo alkanes remain essential intermediates in brominated flame retardants, pharmaceutical synthesis, agrochemicals, drilling fluids, and specialty solvents. Market dynamics are closely tied to upstream bromine supply stability, regulatory shifts in legacy flame retardants, and rising demand for high-purity brominated intermediates in advanced API production. The sector is increasingly characterized by portfolio restructuring among global bromine majors, regional capacity expansion in India and China, and a gradual pivot toward higher-margin specialty derivatives aligned with electronics and energy storage applications.

Supply-side volatility intensified in January 2026, when Albemarle Corporation reported a major flooding event at the Jordan Bromine Company joint venture. Although operations returned to full rates shortly afterward, the disruption is expected to temporarily impact 2026 bromine and derivative volumes, including dibromo alkanes. Concurrently, Albemarle advanced its portfolio simplification strategy between January and March 2026, divesting its 50% stake in Eurecat for $123 million and progressing toward the sale of a controlling stake in Ketjen. This restructuring underscores a sharper focus on specialty bromine and energy storage materials. In November 2025, ICL Group announced a specialties-driven strategy aimed at maximizing value in its bromine and industrial products segment, reporting improved profitability despite lower elemental bromine volumes. Financial resilience was reinforced in December 2025, when ICL declared a $62 million dividend, signaling balance sheet strength to support R&D in bromine-based energy storage technologies such as zinc-bromine flow batteries. Market stabilization in China also emerged in December 2025, when Gulf Resources regained Nasdaq compliance following a reverse stock split, a development critical to maintaining export confidence in organobromine supply chains.

Strategic alliances and regional industrial policy are reshaping the competitive landscape. In February 2026, Chemtura signed a Letter of Intent with India-based Archean Group to establish a strategic alliance leveraging Archean’s marine chemical infrastructure in Gujarat for long-term bromine sourcing. That same month, the Government of India unveiled its Chemical Parks scheme under the 2026 budget, proposing three cluster-based facilities to reduce import dependency and enhance domestic production of high-value intermediates, including brominated alkanes for pharmaceuticals. Silox India secured ₹300–360 crore in February 2026 for expansion within the Dahej PCPIR, targeting specialty brominated intermediates and high-purity derivatives. Downstream innovation continues to influence demand patterns. Between 2024 and 2025, Lanxess and other producers scaled up Emerald Innovation series flame retardants that rely on advanced dibromo alkane precursors as replacements for restricted substances such as HBCD. In early 2025, pharmaceutical manufacturers increasingly shifted toward high-purity dibromo alkane grades to minimize side reactions and accelerate API synthesis timelines. BASF India’s February 2026 expansion of dispersions capacity in Mangalore further strengthens regional specialty chemical infrastructure, indirectly supporting brominated intermediate applications in coatings, electronics, and industrial systems.

Trends and Opportunities in the Global Dibromo Alkane Market

Migration to Captive and Closed-Loop Intermediate Synthesis

- Heightened regulatory oversight of brominated substances is accelerating the migration of dibromo alkane usage into tightly controlled, on-site synthesis pathways. In June 2025, the Australian Department of Climate Change, Energy, the Environment and Water placed several brominated chemicals under stricter scheduling within the IChEMS Register. This action reinforced that high-risk bromine precursors are restricted to essential uses only, signaling a broader global trajectory toward containment rather than open-market handling.

- Within Europe, the European Chemicals Agency continues to estimate 1,2-dibromoethane volumes in the 1,000 to 10,000 tonne per annum range, but usage is increasingly limited to reagent and entrainment roles inside automated synthesis units. These systems are designed to minimize worker exposure while supporting high-value pharmaceutical intermediates. Company safety disclosures from Sigma-Aldrich and Lanxess in late 2025 highlight the continued importance of 1,2-dibromoethane as an in situ activator for magnesium in Grignard reactions. In this role, it converts passive magnesium into reactive species while producing ethylene gas and magnesium bromide as low-risk byproducts. This chemistry underpins the synthesis of complex active pharmaceutical ingredients, positioning dibromo alkanes as non-substitutable process enablers rather than merchant solvents.

Rising Demand for Specialty Alpha,Omega Dibromoalkanes in Electronics

- As the hazard profile of short-chain dibromo alkanes becomes increasingly restrictive, research and industrial demand is pivoting toward longer-chain specialty dibromo alkanes with lower volatility and improved handling characteristics. Compounds such as 1,3-dibromopropane and 1,6-dibromohexane are gaining traction in electronics and optoelectronic materials, where purity and structural symmetry are critical.

- In December 2025, industry assessments of next-generation photovoltaics indicated that the perovskite solar cell sector is scaling rapidly toward a projected valuation of 2.7 billion dollars by 2028. Ultra-high-purity dibromo alkanes are being used as organic cation precursors that enhance film stability and power conversion efficiency, addressing long-standing challenges related to moisture and thermal degradation. Parallel to this, industrial synthesis updates during 2024 and 2025 show increased substitution of 1,3-dibromopropane for 1,2-dibromoethane in laboratory and pilot-scale organic chemistry. Its lower vapor pressure and improved safety profile make it the preferred bromo-alkylating agent for constructing spirocyclic drug motifs, which now represent roughly half of new drug approvals in the modern pharmaceutical era.

Bridging Units for OLED and Liquid Crystal Display Materials

- One of the most attractive growth opportunities for dibromo alkanes lies in advanced display technologies. Organic light-emitting diode and liquid crystal display materials rely on rigid, rod-like molecular architectures where dibromo alkanes function as precisely defined spacers that control electronic coupling and thermal behavior. Research published during 2024 and 2025 in Materials Chemistry Frontiers demonstrated that 1,4-dibromobutane plays a critical role in fourth-generation OLED emitters based on symmetric diarylcarbazole structures. These dibromo-derived bridges significantly enhance thermal and morphological stability, contributing to a reported doubling of device lifetime compared with earlier emitter generations.

- Liquid crystal innovation further underscores this role. In October 2025, synthesis studies on asymmetrical liquid crystals for sensing and display applications used 1,2-dibromoethane to fine-tune spacer length and molecular alignment. By adjusting the alkane bridge, researchers achieved controlled nematic and smectic phase transitions within a temperature window of approximately 110 to 129 degrees Celsius. This level of precision highlights how dibromo alkane chemistry directly determines performance envelopes in LCD host materials and high-temperature sensor platforms.

Cross-Linking Agents for Fuel Cell and Energy Storage Membranes

- The global acceleration of hydrogen and energy storage technologies is opening a structurally new demand channel for dibromo alkanes as polymer cross-linkers. Their bifunctional nature enables controlled network formation in ion-conductive membranes, delivering mechanical robustness and chemical stability under extreme operating conditions. In August 2025, a study published in the International Journal of Hydrogen Energy showed that cross-linking polybenzimidazole with alpha,alpha prime dibromo-p-xylene achieved proton conductivities of up to 0.151 siemens per centimeter at 180 degrees Celsius. This performance exceeds that of several commercial membranes and supports the development of high-temperature proton exchange membrane fuel cells that operate without external humidification.

- At an industrial scale, the push toward net-zero energy systems is reinforcing this opportunity. With global clean energy investment projected to approach two trillion dollars annually by 2030, dibromo alkanes are increasingly used in bromo-alkylation steps for quaternized anion exchange membranes. Cross-linkers such as 1,6-dibromohexane provide the mechanical strength and alkaline stability required for next-generation water electrolyzers, enabling zero-liquid discharge operation and higher hydrogen purity for fuel cell vehicle supply chains. As a result, dibromo alkanes are evolving from tightly regulated intermediates into critical building blocks for advanced energy infrastructure.

Dibromo Alkane Market Share and Segmentation Insights

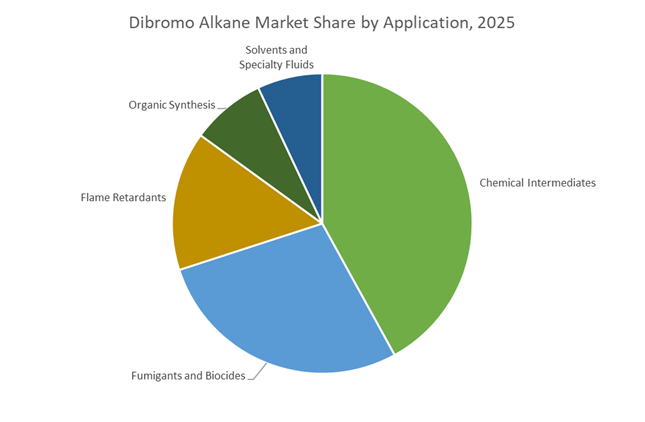

Market Share by Application : Chemical Intermediates Anchor Demand Amid Regulatory Shifts

Chemical intermediates account for 42% of global dibromo alkane consumption in 2025, positioning these compounds as critical brominated building blocks for pharmaceuticals, agrochemicals, and specialty chemicals where selective bromination enables targeted reactivity and bioactivity. Fumigants and biocides remain a sizable segment, particularly in soil treatment and quarantine applications for exported commodities, although tightening environmental and occupational safety regulations are accelerating phase-downs in developed markets. Flame retardants represent another important outlet, supplying brominated additives for plastics, electronics, and technical textiles, even as OEMs increasingly evaluate non-halogenated alternatives. Organic synthesis applications leverage dibromo alkanes as alkylating agents in fine chemical manufacturing and custom pharmaceutical development. Solvents and specialty fluids form a smaller, high-value niche, using dibromo alkanes for mineral separation, gauge fluids, and precision industrial processes where high density and unique solvency characteristics provide functional advantages.

Market Share by End-Use Industry : Agrochemicals Lead While Energy Storage Emerges

Agrochemicals dominate end-use with 38% share, driven by dibromo alkane utilization in pesticide intermediates and legacy soil fumigation chemistries, despite ongoing regulatory pressure pushing innovation toward safer substitutes. Pharmaceuticals and healthcare represent a strategic growth segment, consuming dibromo alkanes in API synthesis for sedatives, antispasmodics, and other therapeutics requiring brominated intermediates under strict quality control. Plastics and polymers rely on dibromo alkane derivatives in brominated flame retardant production for electronic housings, wire insulation, and automotive components meeting fire safety standards. Oil and gas applications include completion fluids and specialty well-control systems where high-density, non-flammable liquids are essential. Electrical and electronics continue steady consumption through flame-retardant materials, while energy storage remains an emerging niche, with dibromo alkanes under evaluation for flow batteries and electrolyte formulations, signaling early-stage diversification beyond traditional markets.

Competitive Landscape of the Dibromo Alkane Market

The Dibromo Alkane market is moderately consolidated, shaped by bromine resource control, electronics-grade purity requirements, and rising demand from flame retardants, pharmaceuticals, and advanced polymers, with vertically integrated producers dominating global supply while specialty reagent players serve high-margin R&D niches.

ICL Group leverages Dead Sea bromine to lead specialty dibromo alkane production

ICL Group anchors the global dibromo alkane value chain through unrivaled access to low-cost Dead Sea bromine, giving it a structural feedstock advantage. For 2026, the company guided consolidated EBITDA between $1.4 billion and $1.6 billion, with its Industrial Products segment contributing a significant share. In late 2025, ICL secured a long-term agreement with a major electronics OEM to supply high-purity brominated intermediates for next-generation circuit boards. Under its 2026 “Portfolio Realignment,” ICL is prioritizing specialty growth engines while pruning non-core assets. This deep vertical integration supports consistent quality for dibromo alkane derivatives used in electronics, polymers, and specialty intermediates.

Albemarle balances bromine specialties with disciplined capital allocation

Albemarle remains a premier supplier of 1,2-dibromoethane and specialty dibromo alkane chain extenders, serving high-performance polymers and flame-retardant systems. Despite flooding at its Jordan Bromine Company joint venture in January 2026, Albemarle restored full operating rates within weeks, stabilizing global supply. The company announced a 65% reduction in 2026 CAPEX to approximately $550–$600 million, emphasizing asset discipline and margin protection. Strategically, Albemarle is targeting data centers and renewable energy infrastructure, where dibromo alkane-derived flame retardants are critical for fire safety in dense server environments. This operational resilience and sector focus reinforce Albemarle’s role in high-value bromine specialties.

LANXESS accelerates dibromo alkane innovation through AI-driven R&D

LANXESS has strengthened its bromine intermediates portfolio following the Chemtura acquisition, becoming a top-tier supplier of dibromo alkane derivatives for pharmaceuticals and agrochemicals. In 2026, the company began integrating artificial intelligence into R&D workflows to shorten development cycles for new actives. Its FORWARD! action plan targets aggressive cost reductions at German sites to offset regional energy pressures. LANXESS is also expanding its Scopeblue labeling for circular and low-carbon raw material products as part of its Climate Neutrality 2040 roadmap. A major supplier of alkylating agents for quaternary ammonium synthesis, LANXESS combines regulatory-grade chemistry with sustainability-led differentiation.

Gulf Resources dominates China’s regional dibromo alkane supply through resource control

Gulf Resources is a critical regional producer, holding an estimated 25.6% share of China’s dibromo alkane segment in early 2026. Operating near the Weifang chemical hub, the company benefits from logistical efficiency and proximity to China’s massive agrochemical manufacturing base. In late 2025, Gulf transitioned to continuous reactors to improve isomer consistency and reduce waste in 1,3-dibromopropane production. Its control over bromine brine extraction creates a strong resource moat against volatile domestic pricing. This vertically aligned model positions Gulf Resources as a reliable high-volume supplier to China’s coatings, agrochemical, and specialty intermediate markets.

TCI Chemicals supplies ultra-pure dibromo alkanes for pharmaceutical R&D pipelines

TCI Chemicals serves the high-purity end of the dibromo alkane market, supporting pharmaceutical discovery and pilot-scale synthesis. Its catalog exceeds 30,000 reagents, including α,ω-dibromoalkanes from C1 to C12 with purities above 98% GC. In 2026, TCI expanded its Hyderabad warehouse to enable same-day dispatch for India’s fast-growing API sector. The company also introduced stabilized dibromomethane with BHT to improve shelf life and safety during sea freight. Known for custom synthesis, TCI provides tailored dibromo isomers for complex API routes, making it a preferred partner for specialty pharma and advanced organic chemistry programs.

United States: Domestic Bromine Security and High-Purity Specialization

The United States dibromo alkane market is being reshaped by upstream bromine security and downstream specialization. In August 2025, TETRA Technologies completed a definitive feasibility study for its Arkansas bromine project, a strategically significant move aimed at reinforcing domestic bromine availability. With a planned Phase I capacity of 75 million pounds per year, the project is positioned to support both traditional clear brine fluids and emerging dibromoalkane-based applications in advanced energy storage. This upstream investment reflects growing concern among U.S. policymakers and industrial buyers about supply concentration risks in global bromine markets, especially as demand diversifies beyond oilfield services into grid-scale technologies.

On the specialty chemicals side, Albemarle Corporation has emerged as a bellwether for value migration within the dibromo alkane chain. In its Q3 2025 disclosures, the company reported strong performance in its Specialties segment, supported by resilient demand for brominated flame retardants in electrical and electronics applications. Importantly, Albemarle exceeded its 2025 productivity targets, unlocking $450 million in cost savings that are now being reinvested into high-precision distillation infrastructure. This capital reallocation is directly strengthening U.S. capacity for pharmaceutical-grade dibromoalkanes such as 1,3-dibromopropane. At the same time, EPA-driven low-GWP transitions under the AIM Act are repositioning dibromoalkanes as reactive intermediates in non-HFC cooling systems and foam stabilizers. Combined with rising Department of Energy-backed investments in zinc-bromine flow batteries, the U.S. market is clearly pivoting from volume-driven bromine supply toward purity, reliability, and application-specific performance.

China: Process Optimization and Export-Oriented Substitution

China’s dibromo alkane industry is advancing under a coordinated industrial policy framework that emphasizes efficiency, substitution, and export resilience. The 2025–2026 petrochemical stabilization plan issued by the Ministry of Industry and Information Technology targets steady chemical value growth while explicitly prioritizing high-end electronic chemicals. Dibromoalkanes occupy a critical position in this strategy as precursors for electronic-grade intermediates, specialty polymers, and advanced flame retardant systems. As a result, domestic producers are being encouraged to upgrade process control and product purity rather than expand undifferentiated capacity.

A defining feature of this transition is the adoption of AI-driven bromination control in Shandong’s bromine clusters. By late 2025, manufacturers had begun deploying data-driven optimization platforms to reduce hazardous byproduct formation by an estimated 10%. Trade friction has further accelerated substitution trends. Following U.S. duties on Chinese phosphorus-based solutions, exporters increasingly pivoted toward bromine-based alternatives, including dibromoalkane-derived flame retardants, to maintain competitiveness in global markets. At the same time, China continues to play a dominant role in agrochemical supply chains. As of early 2026, the country remains a major production hub for 1,2-dibromoethane used as a fumigant and pesticide intermediate for Southeast Asian and African markets. China’s dibromo alkane profile is therefore evolving into a dual-track model, combining process-intensified domestic production with export-oriented specialty positioning.

Israel: Profitability-Focused Bromine Strategy

Israel’s dibromo alkane market is closely tied to strategic shifts within its bromine sector. In November 2025, ICL Group unveiled new strategic principles that sharpened its focus on industrial bromine products. While elemental bromine volumes moderated, the company reported improved profitability driven by higher pricing and stronger demand for specialty bromine derivatives, including dibromoalkanes used in high-value industrial formulations. This emphasis on margin over volume reflects a broader recalibration toward specialty-led growth rather than capacity expansion.

Portfolio discipline is reinforcing this direction. With $1.5 billion in available liquidity reported in late 2025, ICL signaled that future investments would prioritize core bromine extraction and derivative upgrading while exiting non-core downstream battery ventures outside Israel. Crucially, regulatory clarity provided by the Israeli government in 2025 regarding the Dead Sea concession has underpinned long-term planning certainty. This clarity secures bromine extraction rights well beyond 2030, allowing Israeli producers to pursue incremental efficiency improvements and specialty upgrades without regulatory overhang. For global dibromo alkane buyers, Israel is consolidating its role as a stable, profitability-driven supplier of high-quality bromine derivatives.

India: Pharmaceutical Pull and Localization Momentum

India’s dibromo alkane market is being pulled forward by pharmaceutical demand and policy-backed industrial localization. In late 2025, fine chemical manufacturers in Gujarat and Maharashtra reported higher output of high-purity 1,3-dibromopropane, primarily for use in antihistamine synthesis such as Olopatadine Hydrochloride. This shift underscores India’s growing role as a supplier of pharma-grade dibromoalkanes, where purity, traceability, and consistency outweigh sheer volume considerations.

Policy support has been instrumental in accelerating this transition. Under the NITI Aayog chemical hub strategy launched in July 2025, infrastructure subsidies for hazardous halogen handling have reduced entry barriers for domestic dibromoalkane producers. These measures align with the broader Make in India push, under which domestic production of linear dibromoalkanes has expanded to reduce import dependence for polymer and textile intermediates. India’s trajectory suggests a gradual climb up the value curve, from basic halogenated intermediates toward regulated, high-purity specialty supply for pharmaceuticals and performance materials.

Comparative Snapshot: Dibromo Alkane Industry by Country

Dibromo Alkane Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Industry Direction

|

Structural Impact

|

|

United States

|

Bromine security and pharma-grade purity

|

Domestic projects and specialty distillation

|

Supply resilience with value upgrading

|

|

China

|

Process efficiency and export substitution

|

AI-optimized bromination and flame retardants

|

Cost control with specialty positioning

|

|

Israel

|

Margin-led bromine specialization

|

Focus on industrial bromine derivatives

|

Stable, profitability-driven supply

|

|

India

|

Pharmaceutical intermediates and localization

|

High-purity production with policy support

|

Import substitution and value addition

|

Dibromo Alkane Market Report Scope

Dibromo Alkane Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$546.2 Million

|

|

Market Size (2034)

|

$825.8 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Product Type (1,2-Dibromoethane, 1,3-Dibromopropane, Dibromomethane, 1,4-Dibromobutane, 1,5-Dibromopentane, Other Dibromoalkanes), By Purity Grade (Technical Grade, Pharmaceutical Grade, Electronic Grade), By Application (Chemical Intermediates, Flame Retardants, Fumigants and Biocides, Organic Synthesis, Solvents and Specialty Fluids), By End-Use Industry (Pharmaceuticals and Healthcare, Agrochemicals, Plastics and Polymers, Electrical and Electronics, Oil and Gas, Energy Storage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albemarle Corporation, ICL Group Ltd., LANXESS AG, Tosoh Corporation, TETRA Technologies, Inc., Gulf Resources, Inc., Shandong Haiwang Chemical Co., Ltd., Jordan Bromine Company, Tata Chemicals Limited, Agrocel Industries Pvt. Ltd., Chemcon Speciality Chemicals Ltd., Shandong Yuyuan Group Co., Ltd., Prominex, Morre-Tec Industries Inc., Satyesh Brinechem Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dibromo Alkane Market Segmentation

By Product Type

- 1,2-Dibromoethane

- 1,3-Dibromopropane

- Dibromomethane

- 1,4-Dibromobutane

- 1,5-Dibromopentane

- Other Dibromoalkanes

By Purity Grade

- Technical Grade

- Pharmaceutical Grade

- Electronic Grade

By Application

- Chemical Intermediates

- Flame Retardants

- Fumigants and Biocides

- Organic Synthesis

- Solvents and Specialty Fluids

By End-Use Industry

- Pharmaceuticals and Healthcare

- Agrochemicals

- Plastics and Polymers

- Electrical and Electronics

- Oil and Gas

- Energy Storage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dibromo Alkane Industry

- Albemarle Corporation

- ICL Group Ltd.

- LANXESS AG

- Tosoh Corporation

- TETRA Technologies, Inc.

- Gulf Resources, Inc.

- Shandong Haiwang Chemical Co., Ltd.

- Jordan Bromine Company

- Tata Chemicals Limited

- Agrocel Industries Pvt. Ltd.

- Chemcon Speciality Chemicals Ltd.

- Shandong Yuyuan Group Co., Ltd.

- Prominex

- Morre-Tec Industries Inc.

- Satyesh Brinechem Pvt. Ltd.

*- List not Exhaustive