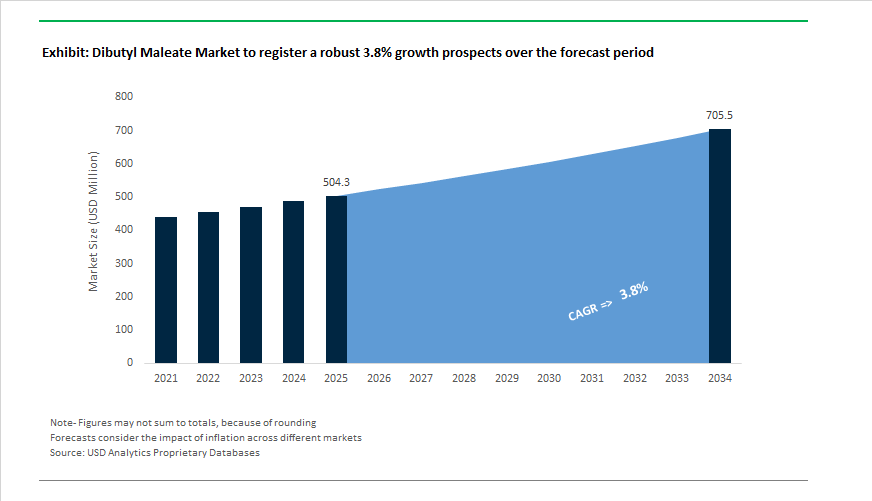

Dibutyl Maleate Market to Reach $705.4 Million by 2034 at 3.8% CAGR Driven by High-Purity Ester Demand and Automotive Plasticizer Innovation

The Dibutyl Maleate (DBM) Market is projected to expand from $504.3 Million in 2025 to $705.4 Million by 2034, registering a CAGR of 3.8%. Dibutyl maleate remains a critical unsaturated diester used as a comonomer in acrylic and vinyl emulsion polymerization, a reactive plasticizer in flexible PVC formulations, and an intermediate in specialty resins, adhesives, and coatings. Market growth is supported by infrastructure development in emerging economies, rising electric vehicle production, and the global transition toward phthalate-alternative plasticizers. Simultaneously, regulatory tightening on organotin compounds and occupational exposure standards is accelerating the shift toward high-purity DBM grades and tin-free catalyst systems across coatings and polymer manufacturing value chains.

Industrial restructuring in the plasticizer and resin ecosystem gained momentum in August 2024, when UPC Technology Corporation signed a Memorandum of Understanding with BASF SE to reinforce the maleate and adipate supply chain across Asia-Pacific. The collaboration strengthens feedstock security for DBM in electronics, cable insulation, and flexible polymer applications. In October 2024, Celanese Corporation expanded bulk logistics capacity for maleic acid dibutyl ester to support high-volume industrial consumers in North America and Europe. Around the same period, Weifang Tuoshi Chemical launched a first-grade DBM variant with enhanced purity, optimized for export-driven copolymer emulsion synthesis. TekniPlex Healthcare introduced bio-based PVC compounds in late 2024, signaling increased adoption of specialty maleate esters such as DBM in medical-grade plastics as safer alternatives to legacy phthalates. The regulatory landscape tightened further in January 2026, when the transition period for dibutyl tin maleate and related substances concluded under EU and UK frameworks, accelerating the move toward tin-free catalyst systems in industrial coatings and adhesive production.

Application-driven demand intensified through 2025. In February 2025, a leading global chemical intermediary partnered with a major automotive coatings manufacturer to co-develop high-flexibility DBM-based plasticizers for vehicle interiors. The collaboration targets enhanced durability, improved tactile quality, and reduced VOC emissions in synthetic leather and dashboard components. In May 2025, following the International Energy Agency’s Global EV Outlook publication highlighting record electric vehicle sales, manufacturers increased integration of DBM into flexible wire harnessing, UV-stable interior polymers, and low-migration cable insulation systems. India’s National Infrastructure Pipeline deployment in 2025 further elevated DBM consumption as paint producers expanded production of high-adhesion resins for smart buildings and large-scale urban infrastructure. Concurrently, Solvay’s Reactsurf 2490 adoption between 2024 and 2025 reshaped emulsion polymerization dynamics, with DBM increasingly used alongside polymerizable surfactants to improve film formation and water resistance in architectural coatings and pressure-sensitive adhesives. By January 2026, major suppliers including Nayakem and Polynt reported a pronounced shift toward >98% ester content DBM grades, now preferred for pharmaceutical intermediates and high-clarity optical adhesives. Updated health advisories in early 2026 addressing dermatitis risks in plasticizer handling have also prompted the deployment of automated closed-loop dosing systems across polymer plants, reinforcing the market transition toward higher-purity materials and safer manufacturing protocols.

Trends and Opportunities in the Global Dibutyl Maleate (DBM) Market

Internal Plasticization for Phthalate-Free and BPA-Free Polymer Compliance

- Regulatory action against migrating plasticizers is structurally accelerating the adoption of DBM as a reactive plasticizer that becomes an integral part of polymer backbones. Following the January 20, 2025 implementation of the European Union ban on BPA in food-contact materials, DBM has gained traction as a compliant alternative to external phthalates such as DOP and DINP. Unlike traditional plasticizers that can leach into fatty or acidic food matrices, DBM is co-polymerized into vinyl acetate and PVC lattices, effectively eliminating migration risk.

- Comparative formulation studies published in early 2025 demonstrated that maleate-plasticized PVC systems can reduce glass transition temperature more efficiently than DEHP while maintaining near-zero migration levels under standard food simulant testing. This performance advantage is particularly relevant for flexible food packaging films and pressure-sensitive adhesives. Parallel regulatory alignment is visible in Asia. China’s GB 4806.15-2024 standard, effective February 8, 2025, mandates stricter safety validation for food-contact adhesives, driving DBM adoption in aqueous dispersions where internal plasticization prevents film embrittlement without relying on restricted low-molecular-weight additives.

Adhesion Promotion in High-Performance Acrylics and Sealants

- DBM is increasingly specified as a functional co-monomer in acrylic and vinyl emulsions to improve adhesion, flexibility, and durability in low-VOC formulations. Industry technical updates in November 2025 highlighted the role of DBM in emulsion polymerization for commercial sealants, where it enhances peel strength and long-term elasticity on difficult substrates such as glass, aluminum, and composite panels. This capability is directly supporting growth in architectural coatings and construction sealants linked to the global acrylic polymers sector.

- Material suppliers have also emphasized DBM’s contribution to environmental resistance. Technical product disclosures from Celanese in June 2025 highlighted DBM’s role in improving water resistance and UV durability in specialty coatings. This trend is particularly pronounced in the Asia-Pacific region, where high humidity and intense solar exposure place sustained stress on residential and infrastructure coatings. DBM-enabled formulations allow manufacturers to maintain clarity, flexibility, and film integrity over extended service lifetimes, reinforcing its value in green building and urban infrastructure applications.

UV-Delayed Curing and Additive Manufacturing via Michael Addition Chemistry

- The reactive maleate double bond in DBM is unlocking new opportunities in advanced adhesives and additive manufacturing. Research presented at the American Chemical Society Fall 2025 meeting showcased anionic UV-delayed curing systems based on maleate esters. These adhesives leverage Michael addition reactions to bond light-impermeable substrates such as copper, achieving lap shear strengths of approximately 6.1 MPa while maintaining pot life exceeding 14 days at 40 degrees Celsius.

- In parallel, DBM is gaining relevance in shape-memory polymers and advanced 3D printing. A 2025 study on hybrid polymer networks demonstrated that combining aza-Michael addition with radical polymerization using maleate-type monomers produces highly homogeneous cross-linked structures. These materials enable reversible and reprogrammable 3D-printed components, with tunable cross-link density improving recovery ratios in shape-memory systems used for medical devices, soft robotics, and aerospace sensor housings.

High-Purity DBM as a Platform Intermediate for Green Surfactants and Lubricant Additives

- DBM’s role as a foundational intermediate is expanding rapidly in surfactants and lubricant additives aligned with biodegradability and performance requirements. It is the primary precursor for sulfosuccinate surfactants such as dioctyl sodium sulfosuccinate, which are widely used as high-efficiency wetting agents. In 2025, manufacturers increased investment in advanced purification processes to produce specialty-grade DBM with tightly controlled impurity profiles. These grades are essential for personal care and cosmetic applications, particularly in SPF enhancers and emollient systems where low irritation and skin compatibility are critical.

- Beyond surfactants, DBM is increasingly used in the synthesis of succinimide-type dispersants for high-performance engine oils. Product dossiers released in June 2025 indicate that DBM-derived dispersants offer superior branching and thermal stability, improving sludge control in high-temperature internal combustion engines. As automotive lubricant formulations evolve to support higher efficiency and longer drain intervals, DBM-based intermediates are emerging as enablers of durability and cleanliness in next-generation lubricant systems.

Dibutyl Maleate Market Share and Segmentation Insights

Market Share by Product Grade : Technical Grade Dominates Industrial Consumption

Technical grade dibutyl maleate accounts for 68% of market volume in 2025, reflecting its role as the standard specification for coatings, adhesives, polymer modification, and plasticizer applications where cost-performance optimization is paramount. This grade supports large-scale manufacturing of acrylic and vinyl copolymers, PVC compounds, and flexible resin systems without the need for ultra-high purity. High-purity grade serves specialty polymers, electronic materials, and advanced coatings, where tighter impurity control directly impacts product stability, adhesion, and long-term performance. Pharmaceutical grade represents the smallest yet highest-value segment, supplying drug delivery systems, regulated intermediates, and medical device components that require biocompatibility and compliance with stringent pharmacopeial standards. Together, these grades illustrate a bifurcated market structure, with volume driven by industrial applications and margins supported by high-specification specialty and pharmaceutical uses.

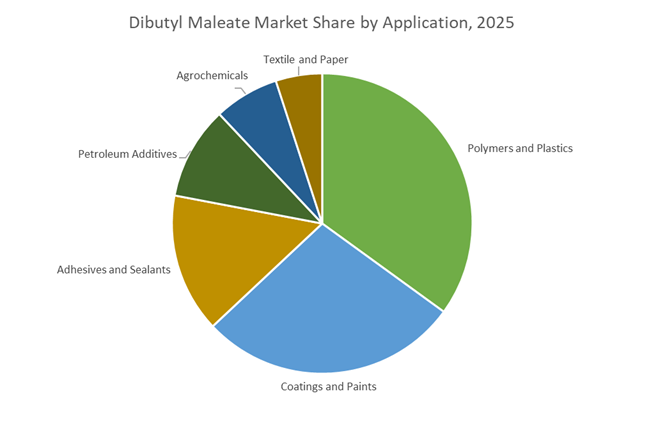

Market Share by Application : Polymers Lead as Adhesives and Coatings Expand

Polymers and plastics capture 35% of dibutyl maleate demand, driven by its use as a comonomer in acrylic and vinyl copolymers and as a PVC plasticizer that enhances flexibility, adhesion, and impact resistance. Coatings and paints represent a major secondary segment, integrating dibutyl maleate into resin systems to improve film elasticity, substrate bonding, and weather durability in industrial, automotive, and architectural coatings. Adhesives and sealants are a fast-growing application, leveraging dibutyl maleate to boost tack, peel strength, and low-temperature flexibility in pressure-sensitive adhesives and construction sealants. Petroleum additives utilize its ester functionality for lubricity enhancement, viscosity modification, and deposit control. Agrochemicals consume dibutyl maleate as a synthesis intermediate and adjuvant component, while textile and paper applications apply it as a softening and finishing auxiliary to improve surface feel and coating performance.

Competitive Landscape of the Dibutyl Maleate Market

The Dibutyl Maleate (DBM) market is shaped by vertically integrated acetyl-chain producers, specialty resin formulators, and high-purity reagent suppliers, with demand driven by non-phthalate plasticizers, water-resistant coatings, specialty adhesives, and polymerization intermediates across construction, automotive, electronics, and pharmaceuticals.

Celanese drives monomer-grade DBM supply through acetyl-chain integration

Celanese Corporation anchors the global DBM supply chain through deep acetyl-chain integration, utilizing its own maleic anhydride feedstocks to deliver cost-competitive, high-purity monomer-grade dibutyl maleate for specialty resins, films, and organic synthesis. In late 2025, Celanese updated its global DBM sales specifications to comply with tightening VOC limits across the Americas, EMEA, and Asia, reinforcing its leadership in regulatory-ready materials. Positioned within its broader emulsion and polymerization portfolio, DBM supports coatings, adhesives, and additive systems. Under its “Sustainability Through Chemistry” strategy, Celanese continues to prioritize low-emissions manufacturing and eco-friendly additive development, strengthening its footprint in performance coatings and specialty materials.

Polynt scales industrial DBM via downstream polyester resin integration

Polynt has established itself as a major European DBM supplier by embedding dibutyl maleate directly into its proprietary unsaturated polyester resin (UPR) lines for construction, automotive, and marine applications. The company commands a significant share of the European industrial-grade DBM market, supplying high-performance adhesives and sealants that demand enhanced UV and moisture resistance. With manufacturing assets spanning four continents, Polynt enables localized global supply, reducing logistics costs while improving responsiveness. Its strategic emphasis on performance chemicals positions DBM as a co-monomer for durable composites and coatings, reinforcing Polynt’s role as both an intermediate producer and downstream resin innovator in the global dibutyl maleate market.

Eastman advances non-phthalate DBM solutions for smart coatings

Eastman Chemical Company is accelerating DBM adoption as a safer alternative to traditional phthalate plasticizers, particularly for vinyl acetate dispersions and water-resistant coatings. In early 2026, Eastman increased production focus on non-phthalate systems, targeting consumer-sensitive applications and the fast-growing smart building sector. Leveraging its Advanced Materials and Naia™ R&D hubs, Eastman is developing DBM-based emulsifiers that enhance adhesive flow, tack, and weather durability. Its deep formulation expertise also extends to customized DBM derivatives for pharmaceutical and agrochemical synthesis, positioning Eastman as a technology leader in high-value, performance-driven dibutyl maleate applications.

Nayakem expands DBM exports through customized plasticization

India-based Nayakem has emerged as a fast-growing exporter of dibutyl maleate and specialty esters, supplying its NK Series maleates and benzoates as sustainable plasticizer alternatives. In late 2025, the company introduced a DBM-based film former for textiles, improving elasticity and hand-feel in synthetic leather applications. More than 40% of Nayakem’s DBM output is now exported to the Middle East and Southeast Asia, capitalizing on regional construction and textile expansion. Focused on customized plasticization, Nayakem supports small-to-mid-scale batch requirements for paints and adhesives, strengthening its position in emerging DBM markets.

Weifang Tuoshi powers China’s high-volume DBM production

Operating in Shandong’s chemical hub, Weifang Tuoshi Chemical serves China’s massive polymerization sector with first-grade dibutyl maleate packaged primarily in 200-liter drums. With China accounting for nearly 40% of global DBM demand, Tuoshi’s strategic access to low-cost raw materials and regional logistics provides a strong competitive edge. In 2025, the company upgraded distillation towers to achieve 99%+ purity, meeting rising requirements from electronics and medical plastics manufacturers. Its 2026 pivot toward e-commerce chemical platforms further expands international reach, enabling rapid bulk sales to buyers in Japan and South Korea.

Sigma-Aldrich sets the benchmark for analytical-grade DBM

Sigma-Aldrich, under Merck KGaA, remains the global reference supplier for analytical and reagent-grade dibutyl maleate used in laboratory research and pilot plants. Offering purities exceeding 99% across packaging sizes from milligrams to bulk, the company supports advanced organic synthesis, including moisture-sensitive Diels–Alder reactions with its newly launched reagent-grade DBM in 2026. Sigma-Aldrich is also a key source for cosmetics and personal care formulators, where DBM derivatives function as texture enhancers and SPF boosters. Through digital science integration and AI-enabled inventory systems, it ensures near-real-time delivery to research institutions worldwide.

China: Import Substitution Through Process Intensification and Environmental Alignment

China’s dibutyl maleate industry is undergoing a structurally important transition from import reliance to domestic self-sufficiency, driven by state-backed petrochemical policy and downstream performance requirements. Under the 2025 Seven Ministries Work Plan for Petrochemical Growth, maleic acid derivatives have been elevated as strategic intermediates, with dibutyl maleate positioned as a critical input for high-performance Vinyl Acetate Ethylene copolymer adhesives. This policy focus reflects China’s intent to secure domestic supply chains for construction, packaging, and electronics adhesives where formulation stability and plasticization efficiency are decisive.

At the production level, chemical clusters in Shandong and Zhejiang implemented AI-driven esterification controls in late 2025, targeting ≥99.5% purity thresholds required by electronics-grade coatings and specialty films. This shift toward high-purity output marks a departure from volume-centric ester manufacturing toward specification-driven supply. Environmental enforcement has further accelerated adoption. Following updates to GB 30981.1 VOC emission standards, dibutyl maleate has gained preference as an internal plasticizer in water-borne emulsions, displacing higher-volatility phthalates. Capacity expansions by Shandong Yuanli Chemical and Hangzhou Qianyang Technology in Q3 2025 have reinforced domestic availability, particularly for desensitizer applications in explosives and petroleum operations. Collectively, these developments signal China’s move toward controlled, compliance-aligned, and application-specific dibutyl maleate production.

India: Regulatory Flexibility Unlocking Adhesives, Paints, and Cosmetics

India’s dibutyl maleate market has been reshaped by a notable easing of upstream regulatory constraints combined with strong pull from infrastructure and consumer-facing industries. The Ministry of Chemicals and Fertilizers’ decision on October 24, 2025 to rescind the Quality Control Order for maleic anhydride has reduced compliance friction and stabilized raw material access for ester producers. This regulatory reset has improved cost predictability for domestic dibutyl maleate manufacturers, particularly those supplying adhesive and coatings value chains.

Downstream, the extension of BIS enforcement timelines for Ethylene Vinyl Acetate copolymers to October 2026 has given adhesive formulators additional runway to standardize high-bonding systems that rely on dibutyl maleate for flexibility and wet adhesion in textile and paper applications. Infrastructure-led demand is also material. Under the PM Gatishakti master plan, the rise of moisture-resistant wall coatings has increased the use of dibutyl maleate-based sulfosuccinate surfactants in premium paint lines, with major formulators such as Asian Paints integrating these chemistries into 2026 launches. Parallel investment in Gujarat’s PCPIR has positioned dibutyl maleate as a specialty intermediate for SPF-containing cosmetic coatings, reinforcing India’s role as a diversified demand center rather than a purely cost-driven producer.

United States: Low-Volatility Compliance and Circular Ester Strategies

In the United States, dibutyl maleate demand is increasingly shaped by VOC compliance and sustainability-linked portfolio restructuring. EPA-aligned regulatory roadmaps for 2025–2026 continue to favor low-volatility plasticizers in architectural coatings, leading to a measurable increase in the adoption of dibutyl maleate-modified acrylic emulsions in residential low-odor paint systems. This regulatory preference has translated into tangible formulation shifts rather than incremental substitutions, particularly in premium interior coatings.

Strategically, North American producers are repositioning dibutyl maleate within broader circular specialty ester frameworks. In mid-2025, Eastman Chemical Company announced a sharper focus on circular ester platforms, piloting bio-based butanol as a feedstock for dibutyl maleate to align with ESG mandates from automotive OEMs. Beyond coatings, the 2026 HFC phase-down under the AIM Act has indirectly supported dibutyl maleate demand as an intermediate in non-HFC cooling lubricants and specialty plasticizers used in energy-efficient HVAC gaskets. The U.S. market trajectory emphasizes regulatory durability, feedstock innovation, and cross-sectoral integration rather than volume expansion.

European Union (Germany and Netherlands): Compliance-Driven Consolidation and Traceability

The European dibutyl maleate landscape is being reshaped by compliance cost escalation and transparency mandates rather than demand contraction. The European Commission’s 19.5% increase in REACH registration fees, effective November 5, 2025, has disproportionately impacted smaller ester suppliers. This has triggered consolidation, with capacity and registrations increasingly concentrated among larger entities such as Polynt, which can amortize administrative and data-management costs across broader portfolios.

At the innovation front, Germany and the Netherlands are emerging as hubs for bio-based dibutyl maleate derivatives. In 2025, Clariant and Evonik showcased DBM-derived sulfosuccinates engineered for biodegradable detergents and agrochemical dispersants at the European Coatings Show, underscoring Europe’s application-led differentiation. Germany’s leadership in piloting the EU Digital Product Passport adds another layer of complexity and value. From late 2026, dibutyl maleate used in industrial adhesives will require a digital twin capturing carbon footprint and safety data, favoring suppliers with robust data infrastructure and traceability capabilities.

Comparative Overview: Dibutyl Maleate Industry by Region

Dibutyl Maleate Market Country Level Snapshot

|

Region

|

Primary Strategic Driver

|

Dominant Applications

|

Structural Outcome

|

|

China

|

Import substitution and VOC compliance

|

VAE adhesives, water-borne coatings, desensitizers

|

High-purity domestic supply with scale

|

|

India

|

Regulatory easing and infrastructure demand

|

Adhesives, damp-proof paints, cosmetic coatings

|

Cost stabilization and diversified demand

|

|

United States

|

Low-VOC regulations and circular feedstocks

|

Architectural paints, HVAC components

|

Compliance-led growth with ESG alignment

|

|

European Union

|

REACH costs and digital traceability

|

Green detergents, industrial adhesives

|

Supplier consolidation and data-driven differentiation

|

Dibutyl Maleate (DBM) Market Report Scope

Dibutyl Maleate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$504.3 Million

|

|

Market Size (2034)

|

$705.4 Million

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Product Grade (Technical Grade, High-Purity Grade, Pharmaceutical Grade), By Function (Internal Plasticizer, Chemical Intermediate, Comonomer, Surfactant Feedstock), By Application (Coatings and Paints, Adhesives and Sealants, Polymers and Plastics, Petroleum Additives, Agrochemicals, Textile and Paper), By Technology (Conventional Esterification, Catalytic Hydrogenation, Continuous Production)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Polynt S.p.A., Celanese Corporation, Eastman Chemical Company, Daihachi Chemical Industry Co., Ltd., Merck KGaA, Shandong Yuanli Chemical Co., Ltd., Hangzhou Qianyang Technology Co., Ltd., Nayakem, Yingkou Xinghuo Chemical Co., Ltd., Baoji Jinbaoyu Technology Co., Ltd., Loba Chemie Pvt. Ltd., Tokyo Chemical Industry Co., Ltd., Avantor, Inc., Nacalai Tesque, Inc., HBC Chem

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dibutyl Maleate Market Segmentation

By Product Grade

- Technical Grade

- High-Purity Grade

- Pharmaceutical Grade

By Function

- Internal Plasticizer

- Chemical Intermediate

- Comonomer

- Surfactant Feedstock

By Application

- Coatings and Paints

- Adhesives and Sealants

- Polymers and Plastics

- Petroleum Additives

- Agrochemicals

- Textile and Paper

By Technology

- Conventional Esterification

- Catalytic Hydrogenation

- Continuous Production

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dibutyl Maleate Industry

- Polynt S.p.A.

- Celanese Corporation

- Eastman Chemical Company

- Daihachi Chemical Industry Co., Ltd.

- Merck KGaA

- Shandong Yuanli Chemical Co., Ltd.

- Hangzhou Qianyang Technology Co., Ltd.

- Nayakem

- Yingkou Xinghuo Chemical Co., Ltd.

- Baoji Jinbaoyu Technology Co., Ltd.

- Loba Chemie Pvt. Ltd.

- Tokyo Chemical Industry Co., Ltd.

- Avantor, Inc.

- Nacalai Tesque, Inc.

- HBC Chem

*- List not Exhaustive