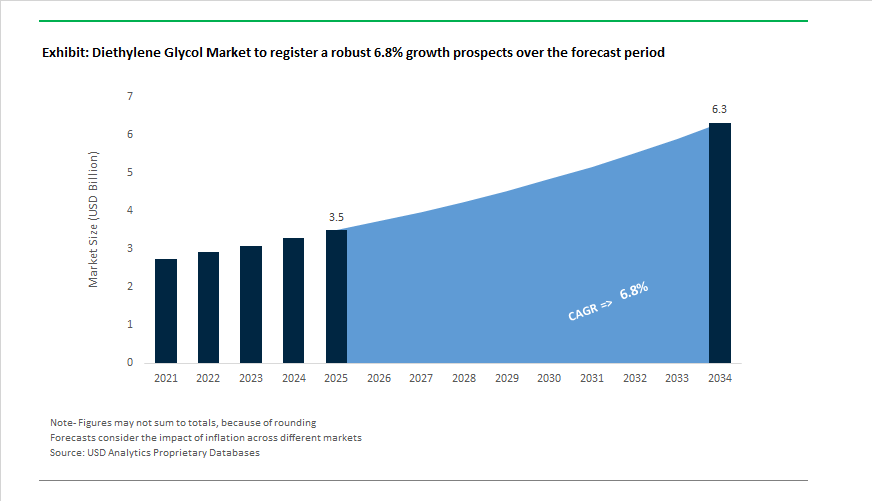

Diethylene Glycol Market to Reach $6.3 Billion by 2034 at 6.8% CAGR as Capacity Additions and Regional Volatility Redefine Supply Dynamics

The Diethylene Glycol (DEG) Market is projected to grow from $3.5 billion in 2025 to $6.3 billion by 2034, expanding at a CAGR of 6.8%. Diethylene glycol remains a critical intermediate in polyester resins, antifreeze formulations, plasticizers, solvents, and specialty chemical synthesis. Market performance through 2024–2026 reflects a structural shift in global glycol supply chains, influenced by new mega-capacity additions, regulatory reform in Europe, and regional demand acceleration in India and China. Oversupply conditions in commodity grades coexist with tightening dynamics in high-purity and specialty glycols, creating segmentation across the value chain.

In early 2026, BASF is scheduled to commission a major 800,000-ton ethylene glycol facility, a development expected to significantly increase global glycol availability and intensify inventory accumulation in East China and export markets. The co-product nature of DEG within the ethylene oxide chain suggests sustained supply pressure into 2026. In contrast, Dow exited the merchant Monopropylene Glycol business at its Freeport site in December 2025, creating a divergence within glycols: DEG faces structural oversupply, while MPG and DPG are entering 2026 with relatively tighter balances. The Chinese glycol market in 2025 followed a strong-to-weak trajectory. Prices remained volatile in early 2025 but entered a sustained decline from late August 2025 amid oversupply, before modestly rebounding in December 2025 due to maintenance shutdowns and seasonal restocking. Benchmark indicators further confirmed this softness, as MEGlobal and EQUATE set the February 2026 Asian Contract Price at $590/MT CFR in January 2026, signaling a flat-to-soft market tone across integrated ethylene oxide and glycol chains.

Regional policy, price management, and asset optimization strategies are reshaping competitiveness. Reliance Industries implemented multiple domestic DEG price revisions between October 2025 and January 2026, reflecting feedstock volatility and India’s expanding downstream demand in resins and antifreeze segments. India’s Dahej PCPIR secured nearly ₹360 crore in February 2026 to expand specialty glycols and intermediates, reinforcing the country’s ambition to become a chemical export hub. Indorama Ventures is executing its IVL 2.0 strategy through 2025–2026, targeting over $200 million in asset monetization from Rotterdam, Canada, and Australia while reallocating capital toward high-growth organic projects. Regulatory developments also influence product positioning. EU chemical frameworks implemented in 2024 drove a 12% increase in eco-friendly glycol adoption, accelerating low-toxicity antifreeze and solvent innovations. Pharmaceutical-grade DEG consumption grew 9.5% in 2024, driven by stricter purity standards in drug formulation to prevent contamination incidents historically associated with industrial grades. Meanwhile, manufacturers reported a 7% operational efficiency improvement during 2024–2025 through Industry 4.0 deployment, including digital twin modeling and real-time yield optimization in glycol distillation. SABIC’s specialty PPE oligomer expansion announced in December 2025, targeting completion in late 2026, further highlights the shift toward higher-value, technology-driven applications linked to advanced glycol chemistry.

Trends and Opportunities Transforming the Global Diethylene Glycol (DEG) Market

Energy Sector Stability Anchored by DEG-to-TEG Conversion

- The expansion of global LNG export infrastructure and shale gas extraction is reinforcing DEG’s critical role as the primary feedstock for triethylene glycol production. TEG remains indispensable for natural gas dehydration, where moisture removal is essential to prevent hydrate formation, corrosion, and flow assurance failures in high-pressure pipelines. According to the International Energy Agency gas outlook for 2025, global natural gas consumption increased by 2.8% in 2024, directly translating into higher glycol dehydration throughput across upstream and midstream assets.

- Operational efficiency is becoming a decisive factor. Updates to the U.S. EPA Natural Gas STAR program in March 2025 emphasized optimized TEG circulation and regeneration as a key methane reduction lever. This focus on lean glycol systems with purity levels exceeding 99% is pushing gas processors to secure higher-grade DEG feedstocks capable of producing low-foaming, thermally stable TEG. As cryogenic LNG facilities tighten dew-point specifications, DEG suppliers that can consistently deliver impurity-controlled material are gaining preferred supplier status.

Regulatory Substitution and Structural Exit from High-End Resin Applications

- In contrast to energy-linked stability, DEG demand is contracting in several polymer and resin segments due to regulatory pressure and material performance limitations. A December 2025 assessment of the unsaturated polyester resin sector showed North American volumes declining roughly 10% versus 2024 levels. DEG-based UPR systems are increasingly displaced by propylene glycol and neopentyl glycol alternatives, which offer superior hydrolytic resistance and higher glass transition temperatures required in structural composites and premium coatings.

- Regulatory momentum is accelerating this shift. Heightened scrutiny of migratory substances in food-contact materials under U.S. and Asian safety frameworks in 2025 has further restricted DEG use in plasticizers and flexible packaging. Compliance with updated GB 4806.15-2024 and revised REACH provisions is prompting a managed withdrawal of DEG from sensitive consumer-facing applications. As a result, DEG demand is consolidating into industrial and infrastructure uses where exposure risks are controlled and performance economics remain favorable.

Upstream Building Block for Morpholine and Power-Sector Corrosion Inhibitors

- One of the most durable growth avenues for DEG lies in its role as a precursor for morpholine, a chemical experiencing renewed demand from power generation, water treatment, and industrial boiler systems. Industrial synthesis data from 2024 and 2025 confirm that advanced catalytic routes using DEG and ammonia can achieve morpholine yields approaching 77 %, improving feedstock economics and reducing waste generation.

- This opportunity aligns closely with power sector investment cycles. With the global corrosion inhibitors market exceeding USD 9.5 billion in 2025 and power generation accounting for more than 31% of demand, morpholine-based inhibitors are increasingly specified for high-pressure boiler systems. Their compatibility with water-based chemistries and low environmental persistence supports zero-liquid-discharge objectives in modern power plants, positioning DEG as a strategically important upstream molecule rather than a declining glycol.

Industrial Processing Aid Demand in Construction and Aviation

- DEG continues to play a vital role as a cost-efficient humectant and processing aid in energy-intensive industries. In cement manufacturing, glycol-based grinding aids are now integral to efficiency optimization. By reducing clinker agglomeration, DEG can lower milling energy consumption by up to 25 kilowatt-hours per ton, a material advantage in markets such as India and Indonesia where infrastructure expansion remains cement-intensive. With regional cement consumption exceeding 680 million metric tons in the past year, DEG-linked grinding aids are becoming a structural component of cost and emissions management strategies.

- Seasonal but high-volume demand also persists in aviation de-icing applications. The shift toward Type II and Type IV de-icing fluids is favoring glycol-based blends that provide longer holdover times under severe winter conditions. The deployment of high-capacity spray systems at major airports in 2025 is increasing per-event fluid consumption while prioritizing formulations that balance efficiency, aircraft safety, and operational throughput. This reinforces DEG’s relevance in specialized industrial fluids even as consumer-facing applications contract.

Diethylene Glycol (DEG) Market Share and Segmentation Insights

Diethylene Glycol Market Share by Grade : Industrial Grade Dominates While Bio-Based DEG Gains Momentum

Industrial grade diethylene glycol commands 68% of global DEG market share in 2025, driven by its broad adoption across polyester resin manufacturing, natural gas dehydration, and plasticizer production where standard 99%+ purity meets performance requirements. This grade underpins large-volume applications such as unsaturated polyester resins, PET processing aids, and antifreeze intermediates, making it the backbone of the global diethylene glycol supply chain. High purity DEG serves specialty segments including pharmaceuticals, cosmetics, and regulated chemical intermediates, where tighter impurity control is essential for product stability and compliance. Meanwhile, bio-based diethylene glycol is emerging as a high-growth niche, produced from renewable bio-ethylene to deliver identical functional performance with a reduced carbon footprint. Sustainability mandates, ESG targets, and brand-led decarbonization strategies are accelerating interest in bio-based DEG, positioning it as a strategic growth lever within the broader glycol chemicals market.

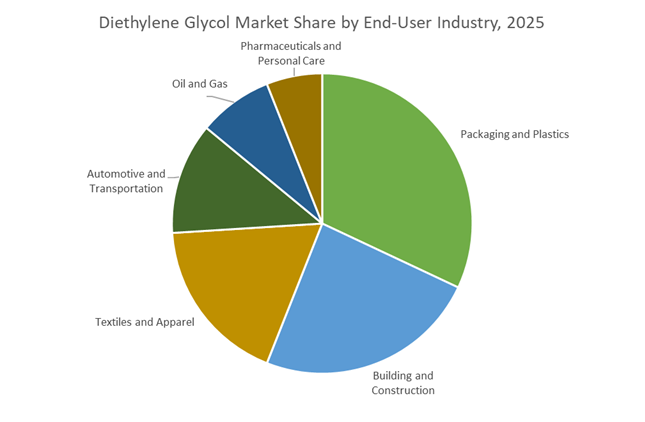

Diethylene Glycol Market Share by End-User Industry : Packaging and Plastics Lead as Oil and Gas Sustains Structural Demand

The packaging and plastics sector accounts for 32% of DEG consumption, making it the largest end-user industry in 2025. Diethylene glycol is widely used in unsaturated polyester resins for packaging components, flexible films, and containers, while also serving as a plasticizer and PET processing aid. Building and construction follows closely, leveraging DEG-based resins in fiberglass panels, bathroom fixtures, grouts, and sealants for improved flexibility and workability. Textiles and apparel utilize DEG in polyester fiber production, dyeing solvents, and fabric softening to enhance dye uptake and hand feel. Automotive and transportation applications span antifreeze, brake fluids, and composite body panels. The oil and gas industry remains a critical demand pillar, using DEG for natural gas dehydration to prevent hydrate formation and pipeline corrosion. Pharmaceuticals and personal care represent a smaller but high-value segment, relying on high-purity DEG for safe, consistent formulations.

Competitive Landscape of the Diethylene Glycol (DEG) Market

The Diethylene Glycol market is led by vertically integrated petrochemical majors with strong ethylene oxide back-integration, global logistics reach, and growing adoption across polyester resins, antifreeze formulations, cement grinding aids, gas dehydration, and specialty solvents, with 2026 competitiveness shaped by feedstock security, AI-enabled manufacturing, and export-driven growth.

SABIC drives global DEG supply through feedstock integration and AI-enabled manufacturing

SABIC holds a dominant position in the global diethylene glycol market, supported by deep integration from ethane and naphtha to finished glycols. The company supplies high-purity industrial-grade DEG for polyester resins, antifreeze, and coolant formulations, backed by a powerful logistics network serving Europe and North America. During 2025–2026, SABIC strengthened its China collaboration with Sinopec, optimizing joint-venture crackers to meet rising Asian plastics and construction demand. Its 2026 “Digital Manufacturing” rollout applies AI-driven process control to ethylene oxide hydrolysis, improving DEG yield consistency. This vertical integration enables SABIC to maintain competitive pricing despite raw material volatility.

Reliance Industries scales DEG exports while anchoring India’s cement and polyester demand

Reliance Industries Limited dominates India’s DEG landscape, operating approximately 1.7 MMTPA MEG/DEG capacity across five western Indian sites, including Jamnagar. In February 2026, Reliance implemented a domestic DEG price hike amid tight supply and strong demand from polyester and cement sectors. It is a key merchant supplier of DEG as a cement grinding aid, improving fineness while lowering energy consumption in large infrastructure projects. Reliance also integrated DEG coolants into EV thermal systems in 2025, delivering reported 18% efficiency gains. Early 2026 saw accelerated exports of fiber intermediates into MEA and Europe, reinforcing its global footprint.

MEGlobal strengthens the global glycol supply chain through strategic ethylene sourcing

MEGlobal is a dedicated ethylene glycols specialist producing over 1.34 million metric tons annually and marketing more than 3.5 million MTA worldwide. In October 2025, MEGlobal expanded its ethylene agreement with Dow, adding 100 KTA from the US Gulf Coast to support Oyster Creek output in 2026. Known for high-performance DEG with strong hygroscopicity and low volatility, the company leverages the Asian Contract Price mechanism to provide pricing stability across APAC. Its “Reliability of Supply” strategy integrates Kuwaiti and US assets into a seamless global network for multinational buyers of DEG-based industrial formulations.

Shell advances high-purity DEG for gas dehydration and specialty chemical applications

Shell plc remains a tier-1 technology leader in glycols, supplying DEG for natural gas dehydration, where it prevents hydrate formation and pipeline corrosion. In early 2026, Shell streamlined its Chemicals and Products organization to accelerate customer-facing innovation. The company is converting its Wesseling refinery into a chemicals-focused hub post-2026 and continues licensing its proprietary OMEGA technology, which optimizes ethylene oxide conversion and influences global DEG coproduct availability. Shell is also investing in bio-based DEG pathways and carbon-capture-integrated manufacturing, aligning its glycol portfolio with its 2050 net-zero ambition.

LyondellBasell targets high-margin DEG for pharma, PVC, and advanced coatings

LyondellBasell Industries supplies high-grade DEG primarily for flexible PVC, paints, coatings, and specialty solvents across North America and Europe. In 2026, the company adopted a value-driven operating model in Europe, prioritizing pharmaceutical and personal care DEG grades to offset elevated energy costs. Leveraging its integrated C2-streams and leadership in polypropylene and oxyfuels, LyondellBasell channels coproducts into premium glycol applications. A notable 2025 innovation includes low-toxicity DEG-derived plasticizers for medical and children’s products, supporting tightening regulatory standards while reinforcing its position in high-specification downstream markets.

China: Self-Sufficiency Mandate and AI-Led Efficiency Gains

China’s diethylene glycol market is being reshaped by an explicit national mandate to raise domestic self-reliance in specialty glycols while tightening the environmental footprint of bulk chemical production. In late 2025, the Ministry of Industry and Information Technology, alongside six other central departments, issued the Work Plan for Stabilizing Growth, which targets a 5% annual increase in chemical added value through 2026. Within this framework, DEG is prioritized as a strategic intermediate supporting downstream polyester resins, plasticizers, and functional fluids, with the policy objective of lifting specialty chemical self-sufficiency toward 90%. This policy emphasis has accelerated investment into integrated ethylene oxide to glycol value chains rather than stand-alone commodity capacity.

Operational execution is being enabled by rapid digitalization. Under the AI + Petrochemicals initiative, major production clusters in Jiangsu and Zhejiang have embedded digital twin platforms into DEG synthesis units. These systems are reported to improve ethylene oxide conversion selectivity while lowering energy intensity by around 12% during 2025, materially improving unit economics and consistency. At the same time, China’s National Development and Reform Commission revised its 2025–2026 roadmap to restrict new coal-to-methanol projects, signaling a shift away from carbon-intensive routes. Preference is now given to integrated glycol complexes that deploy carbon capture, utilization, and storage technologies, repositioning DEG as a more acceptable bulk chemical within China’s evolving decarbonization framework.

India: Safety Enforcement and Specialty Chemical Localization

India’s diethylene glycol market in 2025–2026 is defined by a dual narrative of accelerated localization and stringent toxicology oversight. On the industrial front, the Production Linked Incentive scheme for pharmaceuticals and bulk drugs has played a catalytic role. By December 2025, the Ministry of Chemicals and Fertilizers confirmed that the scheme had avoided imports worth ₹1,807 crore, largely by enabling domestic production of high-purity solvents and excipients where DEG derivatives play a supporting role. This has strengthened India’s position in pharmaceutical formulations, coatings, and resin systems that require controlled-specification glycols.

Conversely, safety governance has tightened dramatically following global alerts. After the World Health Organization’s Medical Product Alert N°5/2025, India’s Central Drugs Standard Control Organization imposed immediate production halts at several facilities in Gujarat and Madhya Pradesh linked to DEG contamination incidents. The regulatory response mandated batch-level gas chromatography testing across the industry, fundamentally changing compliance economics for DEG handling and downstream use. Parallel infrastructure planning supports long-term growth. A 2025 NITI Aayog report on global value chains emphasized shifting domestic petrochemicals toward complex derivatives rather than bulk polymers. Within this strategy, DEG is positioned as a critical intermediate for India’s emerging polyurethane and unsaturated polyester resin sectors, aligning safety reforms with higher-value industrial demand.

United States: Low-Carbon Pilots and Feedstock Security

In the United States, the diethylene glycol market is evolving around decarbonization pilots, feedstock resilience, and enhanced pharmaceutical testing standards. In November 2025, Dow announced the startup of a low-carbon ethylene glycol pilot facility in Texas. This site integrates carbon capture technology and produces DEG as a high-value co-product, reflecting a broader shift toward lowering the carbon intensity of foundational chemical intermediates. Such pilots are increasingly relevant as U.S. buyers and global brand owners tighten Scope 3 emissions requirements across supply chains.

Feedstock reliability is being addressed through strategic agreements. In October 2025, Dow and MEGlobal finalized an agreement to supply an additional 100 kilotons per annum of ethylene from Gulf Coast assets, securing the raw material base for the Oyster Creek facility and supporting DEG demand growth in antifreeze and industrial fluids for both domestic and Asian markets. Product innovation is also emerging. In September 2025, MEGlobal, part of the EQUATE Group, introduced a bio-based glycol grade offering performance parity with fossil-derived DEG, targeting fashion and consumer brands pursuing 2030 sustainability commitments. On the regulatory front, the U.S. Pharmacopeia’s February 2025 proposal to revise accelerated GC-MS test methods for ethylene glycol and DEG reinforces a safety-first environment for excipient and solvent applications.

Saudi Arabia: Functional Glycol Pivot and Export Logistics

Saudi Arabia’s diethylene glycol strategy is increasingly oriented toward downstream diversification and logistics optimization rather than volume expansion. In mid-2025, SABIC disclosed a strategic shift toward higher-value functional glycols, including DEG grades tailored for electronics and semiconductor cleaning applications. This repositioning reflects an effort to hedge against volatility in traditional polyester markets by supplying sectors that value purity, consistency, and technical performance over sheer volume.

Complementing this product strategy is logistics investment. Under the Global Supply Chain Resilience Initiative, the Port of Jeddah recorded a 15% increase in liquid chemical throughput during 2025, driven in part by DEG exports to the Asia-Pacific region. The commissioning of automated chemical storage terminals has reduced turnaround times and improved handling safety, strengthening Saudi Arabia’s role as a reliable export hub for refined glycols serving electronics, coatings, and industrial fluids markets.

Japan: High-Purity Focus and Circular Economy Pilots

Japan’s diethylene glycol market is being reshaped by a decisive move away from commodity competition toward functional specialization and circular feedstocks. In December 2025, Mitsubishi Chemical Group announced a restructuring of its glycol portfolio, concentrating resources on high-purity DEG grades for lithium-ion battery electrolytes and semiconductor processing. This strategic focus reflects both domestic demand growth in advanced electronics and pressure from lower-cost overseas suppliers in commodity glycols.

Circularity is emerging as a parallel pillar. In November 2025, Maruzen Petrochemical partnered with regional recycling firms to pilot chemical recycling routes that convert mixed plastic waste back into monomers for glycol production. While still at pilot scale, these initiatives align with Japan’s broader circular economy objectives and position DEG as a candidate molecule for recycled-content certification in high-specification industrial applications.

Comparative Snapshot: Diethylene Glycol Market Dynamics by Country

Diethylene Glycol (DEG) Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Key Industrial Response

|

Structural Implication

|

|

China

|

Self-sufficiency and energy efficiency

|

AI-enabled DEG plants, CCUS-ready integration

|

Competitive scale with lower carbon intensity

|

|

India

|

Safety enforcement and localization

|

Mandatory GC testing, PLI-backed solvent production

|

Higher compliance costs, stronger domestic value chains

|

|

United States

|

Decarbonization and feedstock security

|

Low-carbon pilots, bio-based grades

|

Premium positioning and supply resilience

|

|

Saudi Arabia

|

Downstream diversification

|

Functional glycol focus, port automation

|

Export strength in high-spec applications

|

|

Japan

|

Functional purity and circularity

|

High-purity DEG, chemical recycling pilots

|

Differentiation from commodity imports

|

Diethylene Glycol (DEG) Market Report Scope

Diethylene Glycol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$6.3 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Grade (Industrial Grade, High Purity Grade, Bio-Based Grade), By Application (Unsaturated Polyester Resins, Polyester Polyols, Antifreeze and Coolants, Chemical Intermediates, Solvents and Plasticizers, Cement Grinding Aids), By End-User Industry (Automotive and Transportation, Building and Construction, Textiles and Apparel, Packaging and Plastics, Oil and Gas, Pharmaceuticals and Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SABIC, Dow Inc., MEGlobal, China Petroleum & Chemical Corporation, Reliance Industries Limited, Indorama Ventures Public Company Limited, BASF SE, Shell Chemicals, Lotte Chemical Corporation, Mitsubishi Chemical Group Corporation, Formosa Plastics Corporation, LyondellBasell Industries N.V., Nippon Shokubai Co., Ltd., Huntsman International LLC, Indian Oil Corporation Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diethylene Glycol Market Segmentation

By Grade

- Industrial Grade

- High Purity Grade

- Bio-Based Grade

By Application

- Unsaturated Polyester Resins

- Polyester Polyols

- Antifreeze and Coolants

- Chemical Intermediates

- Solvents and Plasticizers

- Cement Grinding Aids

By End-User Industry

- Automotive and Transportation

- Building and Construction

- Textiles and Apparel

- Packaging and Plastics

- Oil and Gas

- Pharmaceuticals and Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diethylene Glycol Industry

- SABIC

- Dow Inc.

- MEGlobal

- China Petroleum & Chemical Corporation

- Reliance Industries Limited

- Indorama Ventures Public Company Limited

- BASF SE

- Shell Chemicals

- Lotte Chemical Corporation

- Mitsubishi Chemical Group Corporation

- Formosa Plastics Corporation

- LyondellBasell Industries N.V.

- Nippon Shokubai Co., Ltd.

- Huntsman International LLC

- Indian Oil Corporation Limited

*- List not Exhaustive