Digital Inks Market to Reach $25.6 Billion by 2034 at 9.4% CAGR Fueled by UV, Textile and Sustainable Inkjet Innovation

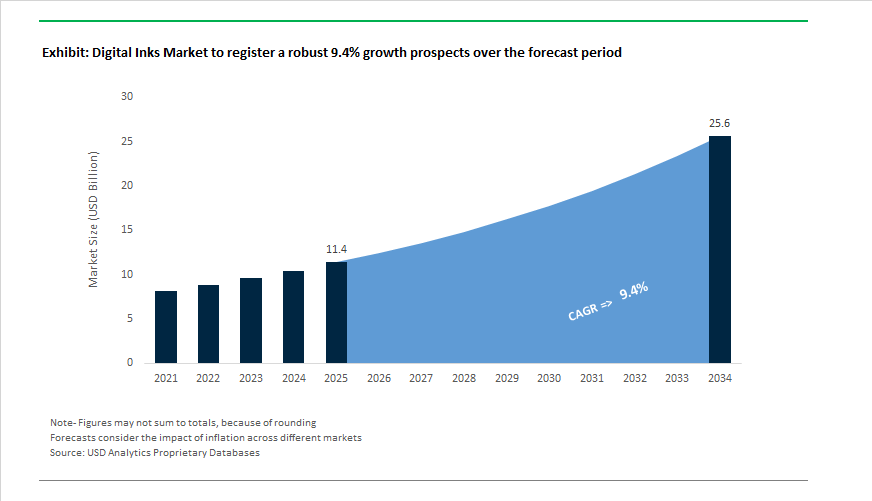

The Digital Inks Market is projected to expand from $11.4 billion in 2025 to $25.6 billion by 2034, registering a robust CAGR of 9.4%. Growth is being driven by rapid adoption of UV-curable inks, water-based pigment inks, sublimation inks, and direct-to-film formulations across packaging, textile, commercial print, and industrial signage applications. The market landscape through 2024–2026 reflects structural consolidation among printer OEMs, aggressive expansion of Asian ink manufacturing capacity, and integration of AI-driven workflow optimization into digital press ecosystems.

In 2024, the Agfa-Gevaert Group strengthened its packaging portfolio by integrating Inca Digital Printers, enabling the rollout of single-pass corrugated packaging systems powered by proprietary water-based and UV-curable ink technologies. This strategic pivot intensified competition with analog flexographic printing by offering higher customization and reduced setup time. During May 2025, Epson launched new PrecisionCore printheads engineered for high-viscosity UV digital inks, incorporating recirculation mechanisms to prevent pigment sedimentation in label and industrial printing. In the same month, DuPont Artistri unveiled the Artistri DTF-120 film and expanded its pigment ink gamut with Orange and Green channels at FESPA 2025, enabling textile printers to achieve broader color reproduction on synthetic and blended fabrics.

Sustainability and manufacturing localization defined mid-2025 developments. In July 2025, Sun Chemical introduced the Xennia Sapphire pigment inks at FuturePrint Brazil, eliminating steaming and washing stages through dry-heat fixation technology, addressing water-scarcity concerns in textile hubs. By October 2025, Sun Chemical expanded reactive ink production in Shanghai to serve India, Bangladesh, and Vietnam textile clusters, shortening lead times for Xennia Amethyst Evo and ElvaJet sublimation series. India simultaneously emerged as a global hub for water-based ink intermediates in 2025, with domestic chemical producers commissioning high-purity dispersion units under the National Infrastructure Pipeline, aligning export-grade formulations with European sustainability benchmarks.

Technological consolidation accelerated in October 2025 when Brother Industries announced its intention to acquire Mutoh Holdings, combining Brother’s inkjet engineering with Mutoh’s wide-format signage capabilities to create integrated ink-and-hardware ecosystems. That same month, HP Inc. integrated CMYK+ high-solid inks and Regenerated Imaging Oil systems into its Indigo line, reducing carbon emissions by up to 16% while improving press uptime. Mutoh America introduced the HydrAton 1642 utilizing Fujifilm AQUAFUZE hybrid ink chemistry, merging water-based and UV-LED advantages for flexible substrate adhesion without primers. Market data released in Q3 2025 confirmed Epson captured a 34.1% global inkjet printer market share, supported by EcoTank adoption and Heat-Free technology that lowers energy consumption.

By January 2026, Fujifilm India launched the Revoria Press EC2100S and SC285S featuring five-color toner engines, enabling specialty metallic and white ink effects for luxury packaging. The combination of UV-compatible printheads, AI-enabled consumable management, expanded Asian reactive ink capacity, and sustainable dry-fixation pigment systems underscores the structural shift toward high-margin digital textile inks, industrial inkjet formulations, and environmentally compliant packaging inks across global markets.

Trends and Opportunities Shaping the Digital Inks Market

Functional Inks Emerge as Core Materials for Printed Electronics

- Digital inks have transitioned into high-value electronic materials that enable additive manufacturing of circuits, sensors, and antennas directly onto flexible and rigid substrates. This trend is being driven by demand for lightweight, compact, and low-waste electronics across wearables, medical devices, and IoT infrastructure. In January 2025, Celanese Micromax expanded its portfolio with nine new conductive ink grades engineered for printed circuits in wearable devices. These silver-based inks deliver conductivity levels approaching 80% of bulk metallic silver, meeting the electrical performance thresholds required for 5G millimeter-wave antennas and advanced RFID applications.

- Healthcare and medical connectivity are reinforcing this trajectory. In February 2025, Henkel introduced functional ink platforms for smart surfaces and connected medical devices. These formulations allow biosensors and conductive pathways to be printed directly onto medical-grade plastics, reducing process scrap and material waste by up to 40% compared with conventional subtractive etching. As additive manufacturing gains regulatory acceptance in medical electronics, functional digital inks are becoming a critical enabler of cost-efficient, miniaturized device architectures.

Shift Toward UV-LED and Water-Based Inks Driven by VOC and Energy Regulations

- Sustainability has moved from a brand preference to a legal and economic necessity in the digital inks market. By late 2025, traditional solvent-based inks containing 300 to 500 grams per liter of VOCs were increasingly replaced by UV-LED and water-based systems emitting less than 10 grams per liter. This transition is being accelerated by escalating compliance costs, as the installation of thermal oxidizers for solvent ink lines now exceeds USD 280,000 per production line, eroding operating margins.

- Energy efficiency is equally influential. In September 2025, Siegwerk showcased its SICURA Nutriflex LEDTec series, designed to comply with the German Ink Ordinance while enabling dual curing under UV-LED systems. These inks deliver up to 50% energy savings compared with mercury-arc lamp curing, offering printers a hedge against volatile electricity prices across Europe. As brand owners demand low-migration, food-safe, and energy-efficient printing solutions, UV-LED compatible digital inks are becoming the default standard rather than a premium option.

Digital Textile Printing Accelerates On-Demand and Eco-Denim Production Models

- Digital textile printing has crossed the threshold from sampling and prototyping into industrial-scale production, fundamentally altering apparel manufacturing economics. In December 2025, EFI Reggiani launched the Titan platform, capable of printing at speeds of 600 meters per hour using EcoTerra pigment inks. These inks eliminate the need for pre- and post-treatment steps, significantly reducing water, chemical, and energy consumption while enabling rapid design changes and localized production.

- A particularly strong opportunity lies in denim manufacturing. Digital inkjet processes can replicate distressed and faded effects without stone washing or enzymatic treatments. Pilot implementations of EFI’s eco-denim concept in late 2024 demonstrated the potential to eliminate traditional washing stages, which historically consume vast volumes of water. At scale, this transition could save billions of liters of water annually, aligning textile producers with tightening environmental regulations and sustainability commitments from global fashion brands.

Ceramic and Glass Inks Enable Functional Architectural and Automotive Surfaces

- The jetting of inorganic pigments and conductive materials onto glass is opening new frontiers for digital inks in construction and mobility. In 2025, Durst Group and Fenzi Group introduced advanced ceramic ink systems capable of achieving optical densities above 3.0 using ultra-thin layers. These inks are widely adopted for architectural glass fritting, where controlled opacity and solar management contribute directly to LEED and other green building certifications.

- Automotive glass represents a parallel growth avenue. New conductive silver ink formulations released in mid-2025 enable the direct printing of defrosting elements, antennas, and embedded sensors onto laminated glass. These inks are engineered to survive high-temperature firing processes while maintaining low resistivity, a requirement for integration with high-voltage EV battery management and advanced driver-assistance systems. As vehicles evolve into connected, sensor-rich platforms, digital glass inks are becoming integral to automotive design rather than a niche embellishment.

Digital Inks Market Share and Segmentation Insights

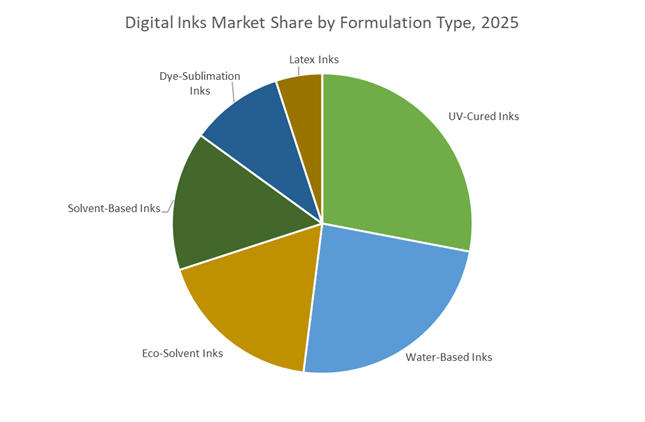

Digital Inks Market Share by Formulation Type : UV-Cured Inks Lead as Water-Based Systems Accelerate Sustainability Shift

UV-cured inks command the largest share at 28% in 2025, driven by instant curing, zero VOC emissions, and excellent adhesion on non-porous substrates such as plastics, glass, and metals. Their durability and outdoor resistance make them the preferred choice for industrial digital printing, signage, and packaging graphics. Water-based digital inks represent the second-largest and fastest-growing segment, fueled by tightening environmental regulations and rising demand for eco-friendly printing in textiles, fine art, and food packaging. Eco-solvent inks maintain strong adoption in sign and graphics applications, balancing durability with reduced odor for vehicle wraps and indoor displays. Traditional solvent-based inks continue to serve harsh outdoor environments but are gradually losing share to UV and eco-solvent alternatives. Dye-sublimation inks support rapid growth in digital textile printing for sportswear and soft signage, while latex inks remain a niche option for premium signage and wallpaper, limited by higher equipment costs.

Digital Inks Market Share by End-User Industry : Advertising Dominates While Fashion and Packaging Gain Momentum

Advertising and media account for 35% of global digital inks demand, supported by strong uptake in billboards, banners, vehicle wraps, point-of-purchase displays, and event graphics. The shift toward short-run, customized, and fast-turnaround campaigns continues to accelerate digital inkjet adoption. Fashion and home decor form the fastest-growing end-use segment, driven by digital textile printing for customized apparel, soft signage, and interior furnishings that benefit from vibrant colors and zero minimum order quantities. Food and beverage packaging represents a significant share as brands increasingly deploy digitally printed labels and limited-edition packaging, favoring UV-cured and water-based inks compliant with food-contact requirements. Consumer electronics maintain steady demand for UV inks used on device housings and functional components. Pharmaceuticals and healthcare remain a smaller but strategic niche, leveraging digital inks for serialized labels, medical device markings, and compliant pharmaceutical packaging requiring high durability and traceability.

Competitive Landscape of the Digital Inks Market

The Digital Inks Market in 2026 is defined by rapid innovation in inkjet printing technologies, water-based digital inks, AI-enabled color management, and industrial-scale adoption across packaging, textiles, electronics, and additive manufacturing. Market leaders are competing on closed-loop ecosystems, pigment dispersion science, energy-efficient printing, and sustainable ink formulations to capture high-growth commercial and industrial segments.

HP Inc. drives high-volume digital printing through AI-powered ink ecosystems

HP Inc. continues to dominate the global digital inks market by leveraging its vast install base of Indigo and PageWide presses across commercial and packaging applications. Its proprietary HP Indigo ElectroInk and HP Latex Inks anchor the market for water-based digital inks that deliver solvent-like durability with aqueous sustainability. In late 2025, HP introduced AI-powered ink management, using real-time sensors to optimize drop placement and reduce ink consumption by up to 15% without sacrificing color density. Strategically, HP expanded into additive manufacturing with the Industrial Filament 3D Printer 600HT in early 2026. Its core competitive advantage remains deep vertical integration between printheads and consumables, creating a high-barrier closed-loop digital printing ecosystem.

Seiko Epson accelerates heat-free inkjet adoption with PrecisionCore technology

Seiko Epson Corporation is leading the shift toward heat-free inkjet printing, emphasizing energy efficiency and precision micro-piezo control for both office and industrial environments. In early 2026, Epson’s regional operations reported aggressive replacement of laser printers with inkjet, highlighting up to 85% lower energy consumption and reduced maintenance cycles. Epson has also expanded its Printhead Sales Business, supplying PrecisionCore technology to third-party OEMs and accelerating digital ink adoption in textiles and labels. The company dominates dye-sublimation printing through UltraChrome® DS inks, known for superior color gamut and wash fastness. Sustainability remains central, with Epson advancing its PaperLab circular recycling systems to close the loop between printing and paper reuse.

DIC Corporation and Sun Chemical anchor global pigment supply for digital inks

DIC Corporation, through its subsidiary Sun Chemical, operates as the world’s largest producer of printing inks and pigments, supplying critical colorants across the digital ink value chain. In early 2026, the group invested $10 million to expand quinacridone pigment capacity in Delaware, securing high-performance red and violet pigments for inkjet applications. Its SunJet portfolio addresses ceramics, conductive electronics inks, and food-safe packaging. Complementing inks, Sun Chemical launched a solvent-free ultra-low monomer adhesive in 2026, enabling fully green flexible packaging systems. The company’s unmatched expertise in pigment dispersion science positions it as the foundational supplier behind many premium digital ink formulations globally.

Fujifilm transforms industrial inkjet with AI-driven workflow and specialty colors

Fujifilm Holdings Corporation has reinvented itself as a major force in industrial digital printing, combining advanced inkjet fluids with intelligent production systems. Its Revoria Press™ and Apeos platforms utilize Super EA-Eco Toner and high-speed inkjet technologies for textured and heavy substrates. At PAMEX 2026, Fujifilm showcased a one-pass five-color engine, enabling metallic toners like gold and silver in a single digital run. From 2024 to 2026, the company committed over ¥170 billion to electronic materials and high-spec inks, building long-term competitive moats. Its AI-enabled Smart Monitoring Gates now correct color variation in real time, reinforcing Fujifilm’s leadership in workflow automation and production consistency.

DuPont advances water-based pigment inks for textiles and food-safe packaging

DuPont sets the benchmark for water-based digital pigment inks, particularly in textiles and flexible packaging where safety and soft-touch performance are essential. Its DuPont™ Artistri® platform celebrated 35 years in 2025 to 2026, with growing focus on Direct-to-Garment (DTG) and Direct-to-Film (DTF) applications. The newly launched Artistri® P1600 ink set delivers higher color vibrancy with reduced ink volumes, supporting high-productivity textile mills. DuPont also leads in food-compliant digital inks, meeting strict global migration standards. Backed by decades of polymer science, DuPont engineers binders that adhere to non-porous plastics and foils without toxic primers, strengthening its position in sustainable packaging inks.

Japan: Printhead Scale-Up and Smart Curing as Competitive Moats

Japan’s digital inks market in 2025–2026 is being shaped by upstream hardware dominance and downstream sustainability mandates. In October 2025, Seiko Epson Corporation completed a 5.1 billion yen factory expansion at Tohoku Epson, quadrupling capacity for PrecisionCore MicroTFP printheads. This move is strategically significant because printhead availability directly constrains digital ink adoption in textile, décor, and industrial printing. By expanding domestic printhead output, Japanese suppliers are reinforcing their control over ink-printhead co-optimization, enabling higher jetting reliability, pigment loadings, and viscosity control for next-generation digital inks.

Technology differentiation has accelerated in parallel. In early 2025, HP Inc., leveraging Japanese manufacturing partnerships, unveiled its next-generation PageWide Thermal Inkjet platform featuring a CMYK+ ink package with 16% higher solid concentration. This development directly reduces carrier oil and water usage per printed square meter, lowering waste handling costs for converters. On the regulatory front, the Ministry of Economy, Trade and Industry tightened its Green Printing certification guidelines for 2026, pushing ink makers such as Toyo Ink toward fully water-based flexo-inkjet hybrid systems. Complementing this, Panasonic and Kyocera launched a joint R&D program in late 2025 to integrate AI-enabled UV-LED curing sensors into industrial presses, optimizing ink pinning and cure depth for pharmaceutical packaging lines.

United States: AI-Driven Efficiency and Regulatory-Led Ink Reformulation

The United States digital inks market is increasingly defined by efficiency gains and regulatory compliance rather than pure volume growth. In October 2025, HP Inc. introduced AI-integrated ink management tools for its industrial presses. The Perfectly Formatted Prints feature automatically optimizes layouts to minimize ink laydown, with internal estimates pointing to up to 10% reduction in specialty ink consumption for small and medium workflows. This reflects a broader shift toward software-led value creation in digital inks.

Sustainability has become a measurable differentiator. HP Indigo launched a supply package in 2025 incorporating Regenerated Imaging Oil, enabling in-press recycling of ink carrier fluids and cutting carbon emissions from consumables by up to 16% per job. Regulatory pressure is reinforcing this direction. The U.S. EPA finalized 2026 Clean Air Act amendments for the printing sector, effectively mandating low-VOC and HAP-free digital inks for wide-format signage and point-of-purchase displays. At the same time, textile on-demand reshoring has gained momentum. Driven by broader industrial policy logic under the CHIPS and Science Act, textile hubs in North Carolina invested over $200 million in 2025 in fully digital micro-factories that rely on pigment-based digital inks to eliminate water-intensive dyeing. This is structurally expanding demand for high-fastness, low-water digital textile inks.

India: Manufacturing Localization and Digitization-Led Demand Expansion

India’s digital inks market is transitioning from import dependence to in-country manufacturing and application-led growth. In July 2025, Epson established its first high-capacity ink tank printer manufacturing facility in Chennai in partnership with RIKUN Manufacturing. Mass production beginning in October 2025 is designed to serve a domestic installed base exceeding 8 million users, anchoring long-term consumption of OEM-qualified digital inks.

Macro digitization trends are amplifying this base. India’s IT spending is projected to reach $176.3 billion in 2026, with packaging and labeling among the fastest digitizing segments. The expanded Digital India roadmap now includes Smart Packaging mandates, encouraging variable data printing and the use of conductive digital inks for pharmaceutical traceability. In parallel, the 2026 Union Budget allocated funding for Global Media Hubs, supporting a forecasted 20% increase in large-format outdoor advertising. This is directly translating into higher demand for eco-solvent and UV-cured digital inks that can withstand Indian climatic conditions while meeting emerging environmental norms.

China: Policy-Backed Digitalization and Functional Ink Innovation

China’s digital inks market is entering a policy-accelerated growth phase aligned with national digitalization goals. The National Data Administration confirmed in December 2025 that the 15th Five-Year Plan will prioritize the intelligent transformation of traditional printing into high-precision digital production. This policy signal is driving investments across packaging, décor, and functional printing segments. Consumer-side incentives are reinforcing this trend. The Ministry of Commerce’s 2026 smart product subsidy scheme encourages the purchase of high-efficiency digital printers, indirectly boosting demand for high-yield ink consumables.

Beyond graphics, China is investing heavily in functional digital inks. In 2025, semiconductor majors collaborated with domestic formulators to commercialize nano-silver conductive inks for flexible circuit boards, targeting lower-carbon electronics manufacturing. Upstream chemical support has also strengthened. The Nanjing Verbund site reached full operational optimization in 2025 for dispersant production, supplying critical raw materials for pigment stabilization and jetting performance. These developments position China not only as a volume market but as an innovation hub for electronic and functional digital inks.

Germany: Circular Ink Systems and Industrial Traceability Demand

Germany’s digital inks market is being shaped by industrial policy and circular economy objectives. Under the Made for Germany initiative launched in July 2025, 61 companies committed €631 billion in investments through 2028, with digitalization of Mittelstand SMEs as a core pillar. Short-run packaging and customization are key beneficiaries, driving adoption of digital inks that enable rapid changeovers and low waste.

Sustainability innovation is equally central. BASF and Siegwerk initiated a 2025 pilot for de-inkable digital inks, designed to simplify recycling of plastic films and paper substrates in line with EU Circular Economy Action Plan targets for 2026. Regulatory spillovers from automotive policy are also visible. The implementation of Euro 7 emission norms in 2026 has increased the use of digital inkjet marking for real-time parts traceability, lifting demand for heat-resistant, high-durability industrial digital inks across German automotive supply chains.

Comparative Snapshot: Digital Inks Market by Country

Digital Inks Market County Level Snapshot

|

Country

|

Primary Growth Lever

|

Strategic Catalyst

|

Market Implication

|

|

Japan

|

Printhead and curing innovation

|

Green Printing certification

|

High-precision, low-waste ink systems

|

|

United States

|

AI efficiency and VOC regulation

|

Clean Air Act amendments

|

Software-led ink optimization

|

|

India

|

Localization and digitization

|

Digital India and media hubs

|

Rapid expansion of eco-solvent and UV inks

|

|

China

|

National digital policy

|

15th Five-Year Plan

|

Scale-up of functional and electronic inks

|

|

Germany

|

Circular economy and traceability

|

EU Circular Economy, Euro 7

|

Premium industrial and recyclable ink demand

|

Digital Inks Market Report Scope

Digital Inks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.4 Billion

|

|

Market Size (2034)

|

$25.6 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Formulation Type (Water-Based Inks, Solvent-Based Inks, UV-Cured Inks, Eco-Solvent Inks, Latex Inks, Dye-Sublimation Inks), By Substrate (Paper and Cardboard, Plastics and Polymers, Textiles, Ceramics and Glass, Metals and Conductive Surfaces), By Printing Technology (Drop-on-Demand Inkjet, Continuous Inkjet, Electrophotography), By Application (Packaging and Labeling, Commercial Printing, Industrial Printing, Publication Printing), By End-User Industry (Food and Beverage, Pharmaceuticals and Healthcare, Consumer Electronics, Fashion and Home Decor, Advertising and Media)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

HP Inc., Seiko Epson Corporation, Canon Inc., Roland DG Corporation, Ricoh Company, Ltd., Fujifilm Holdings Corporation, Brother Industries, Ltd., Dover Corporation, Danaher Corporation, Mimaki Engineering Co., Ltd., Flint Group, Sun Chemical Corporation, Durst Group AG, Electronics For Imaging, Inc., Nazdar Ink Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Digital Inks Market Segmentation

By Formulation Type

- Water-Based Inks

- Solvent-Based Inks

- UV-Cured Inks

- Eco-Solvent Inks

- Latex Inks

- Dye-Sublimation Inks

By Substrate

- Paper and Cardboard

- Plastics and Polymers

- Textiles

- Ceramics and Glass

- Metals and Conductive Surfaces

By Printing Technology

- Drop-on-Demand Inkjet

- Continuous Inkjet

- Electrophotography

By Application

- Packaging and Labeling

- Commercial Printing

- Industrial Printing

- Publication Printing

By End-User Industry

- Food and Beverage

- Pharmaceuticals and Healthcare

- Consumer Electronics

- Fashion and Home Decor

- Advertising and Media

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Digital Inks Industry

- HP Inc.

- Seiko Epson Corporation

- Canon Inc.

- Roland DG Corporation

- Ricoh Company, Ltd.

- Fujifilm Holdings Corporation

- Brother Industries, Ltd.

- Dover Corporation

- Danaher Corporation

- Mimaki Engineering Co., Ltd.

- Flint Group

- Sun Chemical Corporation

- Durst Group AG

- Electronics For Imaging, Inc.

- Nazdar Ink Technologies

*- List not Exhaustive