Digital Textile Printing Inks Market Size, On-Demand Textile Production, and Sustainable Ink Innovation

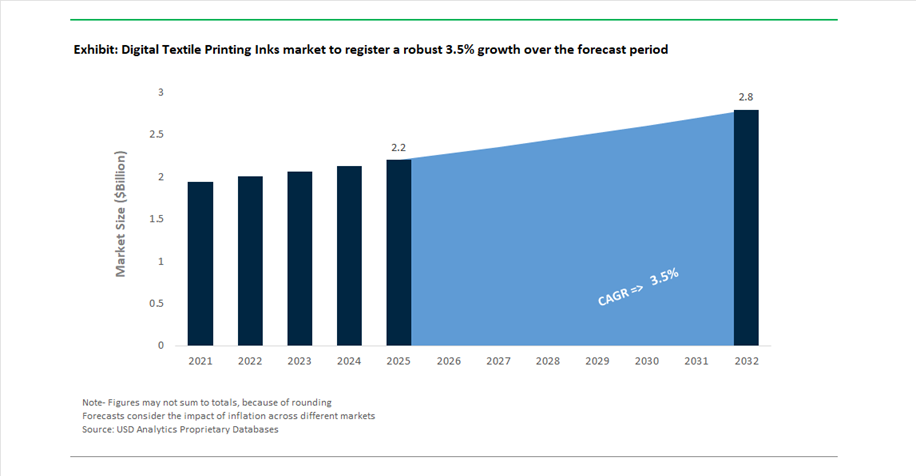

The global digital textile printing inks market was valued at $2.2 billion in 2025 and is projected to grow at a CAGR of 3.5% between 2025 and 2032, reaching $2.8 billion by 2032. This growth is supported by the increasing adoption of digital printing technologies across fashion, home textiles, sportswear, soft signage, and industrial fabrics, where inks play a critical role in delivering color vibrancy, durability, and print precision.

A key structural driver is the shift toward on-demand and short-run textile production, which reduces inventory waste and enables rapid design customization. Digital textile printing inks, including reactive, pigment, sublimation, acid, and disperse inks, are gaining traction due to their ability to support high-resolution printing, reduced water consumption, and lower chemical usage compared to conventional analog printing methods.

Sustainability is a major factor influencing market dynamics. Textile manufacturers are increasingly adopting water-based, eco-friendly inks with low-VOC emissions, aligning with global environmental regulations and brand-driven sustainability commitments. Innovations in pigment-based inks are particularly notable, as they eliminate the need for extensive pre- and post-treatment processes, reducing both water and energy consumption in textile production.

Technological advancements are also reshaping the market through the integration of high-speed inkjet printing systems, AI-driven color management, and advanced dispersion chemistry, enabling improved ink stability, faster drying times, and enhanced compatibility with a wide range of fabrics. Asia-Pacific remains the dominant production hub, driven by strong textile manufacturing ecosystems in China, India, and Southeast Asia, while Europe leads in sustainable textile innovation and regulatory compliance.

Cross-Industry Consolidation, Raw Material Pricing Pressures, and Regional Capacity Expansion Influencing Ink Supply Chains

While the digital textile printing inks market is niche, it is increasingly influenced by broader coatings and chemical industry dynamics, particularly in areas such as raw material pricing, consolidation, and regional manufacturing expansion. In February 2026, Sherwin-Williams’ integration of the Suvinil brand strengthened its global coatings footprint, particularly in Latin America. Although primarily architectural, such expansions indirectly impact the resin, pigment, and additive supply chains used in ink formulations.

Raw material volatility remains a key challenge. In March 2026, Asian Paints implemented a calibrated price increase due to fluctuations in crude oil derivatives, which are also critical inputs for solvents, binders, and dispersants used in textile inks. This reflects broader pricing pressures across the chemical value chain, influencing production costs for ink manufacturers.

Innovation trends from adjacent coatings markets are also shaping ink development. PPG’s “Refresh & Sustain” initiative (January 2026) emphasizes sustainably advantaged formulations, while AkzoNobel’s “Rhythm of Blues” color trends (September 2025) highlight evolving preferences for vibrant, expressive hues, which are increasingly mirrored in textile design and digital printing applications.

Regional capacity expansion strategies are reinforcing supply chain resilience. Nippon Paint India’s Sriperumbudur expansion (January 2026), targeting a 10–15% capacity increase, reflects broader industrial growth in South Asia, supporting the availability of coating intermediates and specialty chemicals used in ink production. Additionally, Kansai Nerolac’s amalgamation with Nerofix (February 2026) enhances operational efficiency and strengthens its position in the Indian chemical and coatings ecosystem.

Strategic acquisitions are further influencing integrated material solutions. RPM International’s acquisition of Kalzip (April 2026), while focused on building envelopes, demonstrates a broader trend toward portfolio diversification and vertical integration across coatings and materials industries, which indirectly benefits adjacent segments such as digital inks through improved technology transfer and material innovation.

Sublimation Inks Dominate Digital Textile Printing Market with 48% Share Driven by Polyester Apparel and High-Speed Printing

Ink Type Analysis: Dye-Sublimation Technology Leads with Vibrant Prints and Scalable Production Efficiency

Sublimation inks hold a dominant 48.0% share of the digital textile printing inks market in 2025, driven by their superior performance in polyester-based textile printing, sportswear manufacturing, and soft signage applications. This technology uses heat-activated disperse dyes (200–220°C) that sublimate into gas and permanently bond with polyester fibers, delivering wash-fast, breathable, and high-resolution prints without affecting fabric texture. A major growth driver is the “print-first, transfer-later” workflow, enabling centralized printing on transfer paper and global distribution to garment factories, significantly improving inventory efficiency and production flexibility. High-speed roll-to-roll printers exceeding 1,000 square meters per hour further enhance scalability for fast fashion and mass customization. With over 70% of usage concentrated in apparel applications, sublimation inks remain the cornerstone of the digital textile printing inks market, particularly in sportswear, promotional clothing, and polyester-based fabrics.

Clothing & Apparel Segment Leads with 54% Share Driven by Digital Printing Adoption and Sustainable Manufacturing

Application Analysis: On-Demand Apparel Production and Waterless Printing Technologies Fuel Market Growth

The clothing and apparel segment accounts for a leading 54.0% share of the digital textile printing inks market in 2025, driven by the rapid shift from traditional screen printing to digital textile printing technologies. Digital printing enables short production runs (1–500 units), unlimited color complexity, and faster turnaround times, aligning with the demands of fast fashion, customization, and “see-now, buy-now” retail models. A critical growth factor is sustainability, as digital printing processes—particularly pigment and sublimation inks—reduce water consumption by 90–95% compared to conventional dyeing methods, addressing environmental concerns and regulatory pressures. Additionally, the integration of hybrid analog-digital production systems in major textile hubs such as China, India, and Bangladesh is accelerating adoption. These advancements position apparel as the primary growth engine in the global digital textile printing inks market, supported by evolving consumer trends and eco-friendly manufacturing practices.

Digital Textile Printing Inks Market Competitive Landscape Driven by Water-Based Pigment Inks, Inkjet Technology, and Sustainable Textile Production

The digital textile printing inks market is highly competitive, driven by rapid adoption of inkjet printing, water-based pigment inks, and sustainable textile manufacturing. Key players compete on color performance, printhead compatibility, water reduction technologies, and scalable solutions for fashion, home textiles, and industrial applications.

Epson Leads Inkjet Textile Printing with Heat-Free Technology and Water-Saving Pigment Inks

Seiko Epson Corporation is strengthening its dominance in digital textile printing inks through its Heat-Free technology, significantly reducing energy consumption and machine wear in high-volume textile production. The Monna Lisa ML-13000 printer utilizes advanced water-based pigment inks, reducing water usage by up to 97% compared to traditional rotary printing. Its UltraChrome® ink series delivers expanded color gamut and superior durability, targeting premium fashion and home décor markets. Epson’s vertical integration of PrecisionCore® printheads and ink chemistries ensures consistent, high-quality output with minimal defects. The company is also advancing Dry Fiber Technology to enable circular textile production from waste materials. Its focus on sustainability and innovation positions Epson as a leader in next-generation textile ink solutions.

Kornit Digital Disrupts Textile Printing with On-Demand Production and Multi-Fabric Ink Systems

Kornit Digital Ltd. is transforming the textile printing inks market with its Atlas MATRIX system, offering a unified ink platform for cotton, polyester, and blended fabrics. Its Karbon Shield™ technology prevents dye migration, enhancing print quality on complex substrates such as deep-dyed polyester. Kornit’s fulfillment-as-a-service model supports on-demand apparel production, enabling zero-inventory manufacturing for global e-commerce brands. The company introduced Neon Ink configurations to address high-growth sportswear and athleisure segments, now accounting for a significant share of production volume. Operating in over 100 countries, Kornit is capitalizing on reshoring trends and localized manufacturing hubs. Its integrated hardware, software, and ink solutions redefine digital textile printing scalability.

Fujifilm Expands Digital Textile Ink Solutions with AI-Driven Color Management and Specialty Inks

FUJIFILM Holdings Corporation is positioning itself as a digital transformation partner in textile printing by integrating AI technologies into its ink and printing ecosystems. Its Revoria Press™ and Apeos platforms offer CMYK plus specialty colors such as gold, silver, and white, enabling high-value textile and signage applications. Fujifilm’s advanced RIP solutions ensure precise color consistency across multi-location production environments. The company is expanding in APAC markets, particularly India and Southeast Asia, supporting the transition from analog to digital textile printing. Its Sustainable Value Plan 2030 targets a 50% reduction in CO2 emissions through energy-efficient systems and bio-based inks. Fujifilm’s combination of digital integration and specialty inks strengthens its competitive position.

Dover (JK Group & MS Printing) Drives High-Speed Dye-Sublimation Ink Adoption for Industrial Textile Printing

Dover Corporation, through JK Group and MS Printing Solutions, remains a leader in dye-sublimation inks for digital textile printing. Its Digistar ink portfolio supports high-speed roll-to-roll production for soft signage and home textile applications. The integration of LaRio single-pass technology enables digital printing speeds comparable to traditional screen printing while maintaining flexibility. Dover focuses on industrial-scale digitalization, offering inks designed for rapid drying and reduced post-processing requirements. Its solutions align with the growing demand for high-efficiency textile production systems. The company’s expertise in sublimation and high-speed printing technologies strengthens its leadership in industrial textile inks.

DuPont Accelerates Growth in Pigment Textile Inks with Advanced Polymer Chemistry

DuPont, through its Artistri® portfolio, is capitalizing on the rapid growth of pigment-based textile inks driven by their one-step fixation process. The Artistri® P1600 ink set enhances wash fastness and elasticity, making it ideal for direct-to-garment and direct-to-film applications on stretch fabrics. DuPont’s expertise in polymer chemistry enables the development of binders that deliver a soft hand feel comparable to traditional dye-based systems. The company is collaborating with printer OEMs to optimize ink formulations for improved printhead longevity and reduced maintenance. Its focus on pigment inks aligns with sustainability trends and waterless processing requirements. DuPont’s innovation supports high-performance textile printing applications.

Huntsman Expands Digital Ink Portfolio with Focus on Technical Textiles and Sustainable Processing

Huntsman Corporation’s Textile Effects division maintains strong leadership in reactive and acid inks for luxury textiles such as silk and nylon. The company is expanding into digital pigment inks to address demand for waterless textile processing and sustainable manufacturing. Huntsman is investing in technical textile applications, including automotive and medical sectors, where inks require UV resistance and antimicrobial properties. Its supply chain realignment in Southeast Asia supports the shift of textile manufacturing away from China. The company’s expertise in specialty dyes and chemicals enhances its competitive position in high-end textile markets. Huntsman’s focus on sustainability and diversification strengthens its role in the evolving digital textile inks industry.

India Digital Textile Printing Inks Market: PM MITRA Push and Pigment Transition Driving Rapid Growth

India is emerging as the fastest-growing hub for digital textile printing inks, driven by sustainability goals and large-scale textile modernization. The rollout of PM MITRA mega textile parks has created plug-and-play infrastructure for high-capacity digital printing, accelerating adoption across major clusters.

A major structural shift is underway from reactive dyes to pigment inks, with mills reporting a 28% YoY increase in pigment ink adoption due to reduced water usage and elimination of post-processing steps like steaming and washing. Government support through the PLI scheme for MMF fabrics ($1.2 billion investment) is further boosting digital-ready production capacity. Innovation is also strong, with Indian companies developing low-viscosity eco-pigment inks compatible with advanced industrial printheads, achieving up to 95% color consistency. Additionally, sustainability initiatives—such as solar-powered curing systems adopted by 40+ units—are reducing carbon emissions by ~35%, reinforcing India’s leadership in eco-friendly textile printing.

Italy Digital Textile Printing Inks Market: Luxury Digitalization and Sustainable Chemistry Driving Premium Leadership

Italy remains the global benchmark for high-end textile printing inks, particularly in luxury and sustainable fashion. Investments such as Miroglio Textile’s Digital Eco-Factory (2025) are enabling the use of water-based inks that reduce chemical waste by up to 70%, especially in silk production.

Regulatory compliance is a key driver, with Italian manufacturers achieving a 95% phase-out of restricted chemicals (e.g., APEOs) under REACH 2.0. Technological innovation is also advancing, with nano-pigment inks offering “zero-feel” finishes on premium fabrics. The rise of on-demand printing (+42% adoption) is reducing inventory waste, while AI-driven color management systems are cutting ink consumption by ~18%. Additionally, strong growth in direct-to-fabric (DTF) printing and export of high-speed printers reinforces Italy’s leadership in premium digital textile inks.

China Digital Textile Printing Inks Market: VOC Regulation and Industrial Scaling Driving Global Dominance

China is re-engineering its digital textile printing inks market toward high-volume, low-emission production, supported by strict environmental regulations. The implementation of GB 30981.1-2025 (2026) is effectively banning many solvent-based inks, forcing a transition to low-VOC and water-based formulations.

Scale and innovation are key strengths. Investments of $2.5 billion in Zhejiang clusters are converting traditional printing to digital single-pass systems, while Ink-on-Demand (IoD) technology is reducing ink waste by ~22%. China also dominates exports, accounting for ~60% of global sublimation ink supply, supported by expanded NMP production (+35%). Emerging innovations such as graphene-enhanced conductive inks for smart textiles are further expanding application scope, reinforcing China’s global leadership.

Japan Digital Textile Printing Inks Market: Precision Engineering and Waterless Printing Driving Innovation

Japan’s market is defined by high precision and multi-substrate compatibility, particularly for premium apparel and sportswear. Major investments by companies like Mimaki and Epson ($500 million combined R&D) are advancing universal pigment inks compatible with cotton, polyester, and nylon.

Sustainability is a major focus. Japan is transitioning toward waterless digital printing, with ~65% adoption of pigment and sublimation processes to meet zero-discharge goals. The country also leads in high-resolution printing (1200 dpi), enabling premium-quality output for luxury and performance textiles. Additionally, the rapid adoption of Direct-to-Film (DTF) systems (+55% growth) is supporting small-scale designers, while mandates at events like Tokyo Fashion Week are driving demand for low-impact inks.

Turkey Digital Textile Printing Inks Market: Nearshoring and Reactive Ink Demand Driving Fast Fashion Growth

Turkey is positioning itself as a key nearshoring hub for Europe, specializing in high-speed reactive ink printing for fast fashion. Investments such as the $400 million Bursa modernization program are upgrading facilities to meet 48-hour delivery timelines for EU brands.

Demand is driven by customization trends, with personalized apparel orders rising 38%, primarily using reactive inks on locally sourced cotton. Trade agreements with the EU now require OEKO-TEX certified inks, accelerating sustainability adoption. Growth in tourism is also boosting demand for UV-curable and sublimation inks in signage and décor, while domestic production of dye precursors is improving supply chain resilience.

Brazil Digital Textile Printing Inks Market: DTG Growth and Bio-Based Innovation Driving Regional Leadership

Brazil is the leading market for digital textile printing inks in Latin America, driven by e-commerce and sustainable innovation. The Direct-to-Garment (DTG) segment is expanding rapidly, with a 14% increase in printer installations (2025) fueled by print-on-demand business models.

Sustainability is a key differentiator. Brazilian researchers have commercialized soy-based binders for pigment inks, offering renewable alternatives to conventional materials. Import substitution policies are also strengthening local production, with new ink-blending facilities established by global players. Additionally, demand for digitally printed home textiles (+20%) and growth in recycled polyester usage (+18%) are driving adoption of specialized sublimation inks, positioning Brazil as a regional innovation leader.

Digital Textile Printing Inks Market Report Scope

Digital Textile Printing Inks market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2032)

|

$2.8 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Ink Type (Sublimation Inks, Reactive Inks, Pigment Inks, Acid Inks, Disperse Inks, Others), By Substrate (Polyester and High-Polymer Derivatives, Cotton, Silk, Nylon, Wool, Blended Fabrics, Others), By Printing Technology (Direct-to-Fabric, Direct-to-Garment, Transfer Printing, Direct-to-Film), By Machine Operation Mode (Multi-Pass Printing, Single-Pass Printing), By Application (Clothing and Apparel, Home Textiles, Soft Signage and Advertising, Technical and Industrial Textiles), By Formulation Base (Water-based Inks, Solvent-based Inks, UV-curable Inks)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Huntsman Corporation, Sun Chemical, BASF SE, Sensient Technologies Corporation, JK Group, The DyStar Group, Seiko Epson Corporation, Kornit Digital Ltd., SPGPrints B.V., Marabu GmbH & Co. KG, Inx International Ink Co., Fujifilm Holdings Corporation, Zhengzhou Hongsam Digital Science & Technology Co., Ltd., Jay Chemical Industries Private Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Digital Textile Printing Inks Market Segmentation

By Ink Type

- Sublimation Inks

- Reactive Inks

- Pigment Inks

- Acid Inks

- Disperse Inks

- Others

By Substrate

- Polyester and High-Polymer Derivatives

- Cotton

- Silk

- Nylon

- Wool

- Blended Fabrics

- Others

By Printing Technology

- Direct-to-Fabric

- Direct-to-Garment

- Transfer Printing

- Direct-to-Film

By Machine Operation Mode

- Multi-Pass Printing

- Single-Pass Printing

By Application

- Clothing and Apparel

- Fashion and Haute Couture

- Sportswear and Athleisure

- Casual Wear

- Home Textiles

- Bedding and Linens

- Curtains and Upholstery

- Carpets and Rugs

- Soft Signage and Advertising

- Banners and Flags

- Backlit Displays

- Trade Show Graphics

- Technical and Industrial Textiles

- Automotive Interiors

- Medical Textiles

- Protective Clothing

By Formulation Base

- Water-based Inks

- Solvent-based Inks

- UV-curable Inks

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Digital Textile Printing Inks Market

- DuPont de Nemours, Inc.

- Huntsman Corporation

- Sun Chemical

- BASF SE

- Sensient Technologies Corporation

- JK Group

- The DyStar Group

- Seiko Epson Corporation

- Kornit Digital Ltd.

- SPGPrints B.V.

- Marabu GmbH & Co. KG

- Inx International Ink Co.

- Fujifilm Holdings Corporation

- Zhengzhou Hongsam Digital Science & Technology Co., Ltd.

- Jay Chemical Industries Private Limited

*- List not Exhaustive