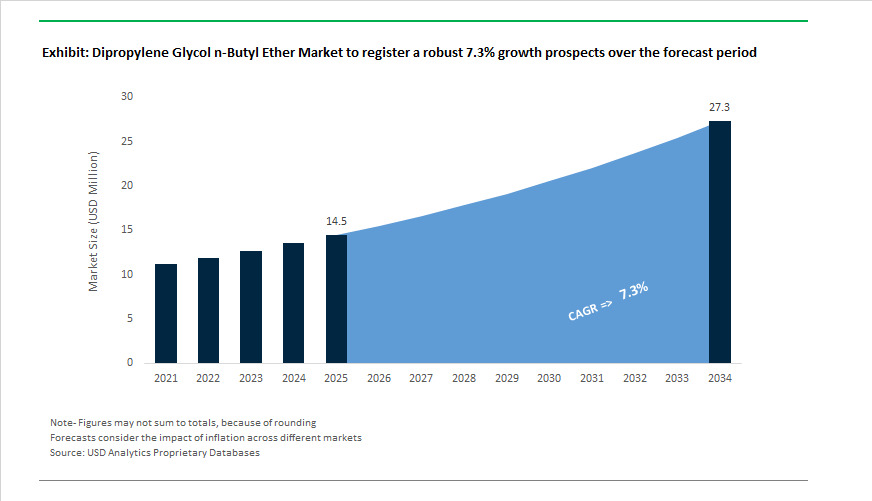

Dipropylene Glycol n-Butyl Ether Market to Reach $27.3 Million by 2034 at 7.3% CAGR Driven by Low-VOC Coatings and Circular Feedstocks

The Dipropylene Glycol n-Butyl Ether (DPnB) Market is projected to expand from $14.5 Million in 2025 to $27.3 Million by 2034, registering a CAGR of 7.3%. Growth momentum is anchored in rising demand for low-VOC solvents in architectural coatings, automotive refinishes, and industrial cleaning formulations. In May 2024, Dow completed a capacity expansion at its propylene glycol facility in Thailand, reinforcing Asia-Pacific supply for high-performance façade coatings and waterborne systems that utilize DPnB as a coupling agent and coalescent. Earlier in 2024, Dow introduced sustainable Propylene Glycol REN and CIR grades, derived from bio-circular and recycled feedstocks, providing downstream manufacturers with the necessary building blocks to produce circular DPnB formulations aligned with global carbon reduction mandates. In November 2024, Dow partnered with the Delian Group to advance automotive circularity initiatives, targeting DPnB-based coatings and cleaning agents used in vehicle production and maintenance cycles.

Structural supply adjustments and upstream volatility are reshaping the cost framework entering 2026. In September 2024, BASF unveiled its 2025–2028 corporate strategy, classifying Chemicals and Industrial Solutions as core segments while prioritizing the startup of the Zhanjiang Verbund site in China as a central production hub for glycols and performance solvents. Through 2025, LyondellBasell advanced construction at its Channelview, Texas complex to convert ethylene into 882 million pounds per year of propylene, strengthening internal propylene oxide availability for dipropylene glycol ether derivatives. Despite reporting a $738 million net loss in January 2026 due to compressed industry margins, LyondellBasell indicated recovery prospects tied to glycol demand in de-icing and industrial cleaner markets. In parallel, BASF announced price increases for Oxo-C4 alcohols in January 2026, directly impacting n-butanol costs and cascading into higher DPnB pricing structures. Eastman followed with a global glycol ether price hike effective February 12, 2026, reflecting escalating feedstock and operational expenses across North and Latin America. Dow also confirmed it will begin shutting down three upstream European assets starting mid-2026, aiming for a $200 million EBITDA uplift through footprint rationalization by late 2027.

Market demand is increasingly shaped by regulatory pressure and environmental performance benchmarks. Throughout 2025 and into 2026, formulators shifted from traditional PnB to DPnB due to its lower VOC profile, improved biodegradability, and compatibility with modern waterborne coating technologies. Adoption is accelerating in North America and China under tightened emissions rules and Ministry of Ecology and Environment standards. The migration toward low-VOC aesthetic coatings in automotive OEM and architectural segments has elevated DPnB’s role as a preferred solvent for maintaining film integrity and gloss retention without exceeding environmental thresholds. Supporting long-term competitiveness, BASF confirmed the launch of its global Digital Hub in Hyderabad in Q1 2026, leveraging AI-driven supply chain optimization to enhance cost control and service delivery in specialty solvents. This combination of sustainable feedstock innovation, regional capacity expansion, and regulatory-driven substitution continues to redefine the competitive landscape of the Dipropylene Glycol n-Butyl Ether market.

Trends and Opportunities Defining the Dipropylene Glycol n-Butyl Ether (DPhB) Market

Regulatory Consolidation Toward High-Performance Industrial Coatings

- Regulatory tightening in North America is accelerating the consolidation of Dipropylene Glycol n-Butyl Ether into professional and industrial coatings where reactivity-based VOC standards are now decisive. The U.S. EPA’s January 2025 Final Rule on National VOC Emission Standards for Aerosol Coatings prioritizes solvent reactivity and long-term emission behavior over simple mass-based VOC metrics. This framework strongly favors slow-evaporating P-series glycol ethers such as DPhB over more volatile Hazardous Air Pollutants.

- As a result, DPhB is increasingly specified in automobile refinish, coil coatings, and heavy-duty maintenance coatings where leveling, flow, and defect control are mission-critical. With a relative evaporation rate below 0.01 and a boiling point near 220°C, DPhB enables controlled solvent release during curing, preventing surface defects such as popping and orange peel in high-solids systems. In February 2025, Dow’s price increase for DOWANOL™ DPnB reflected tightening supply as industrial customers shift away from regulated solvents, particularly in a global industrial maintenance coatings segment projected to reach USD 4.99 billion in 2025. This trend reinforces DPhB’s role as a specification-driven solvent rather than a discretionary additive.

DPhB as a Coalescing Stabilizer in Advanced Waterborne Formulations

- As waterborne coatings evolve toward higher solids, multi-additive architectures, and low-SVOC compliance, Dipropylene Glycol n-Butyl Ether is emerging as a critical hydrophobic coalescing stabilizer. Modern latex systems increasingly incorporate wax dispersions, hydrophobic biocides, and specialty fillers that are prone to phase separation under humidity or low-temperature application conditions. DPhB’s balanced polarity allows it to plasticize hard resin domains while maintaining compatibility within aqueous matrices.

- Innovation trends in 2025 underscore this positioning. Dow’s Dalpad™ A Plus technology, recognized in January 2025 for reducing semi-volatile organic compound emissions by over 60 %, is frequently paired with DPhB in commercial formulations to stabilize complex resin packages. According to late 2024 data from the American Coatings Association, hydrophobic coalescing agents represented the fastest-growing segment in the coatings additives space, expanding at 5.6% annually. DPhB benefits directly from this momentum due to its low odor profile and ability to deliver consistent film formation in interior architectural paints and low-odor industrial latex coatings without compromising regulatory compliance.

Process Solvent for High-Temperature Polymers in Electronics and EV Applications

- The global effort to replace N-Methyl-2-pyrrolidone is opening a meaningful opportunity for Dipropylene Glycol n-Butyl Ether in high-performance polymer processing. In early 2025, peer-reviewed research highlighted the use of benign, high-boiling solvents in the synthesis of photosensitive polyimides and related electronic materials. DPhB’s strong solvency for polyphenylene sulfide precursors, combined with its recoverability at elevated temperatures around 220°C, makes it a viable process solvent for polymer purification and film casting.

- This opportunity is reinforced by growth in electronics encapsulation and electric vehicle battery insulation, segments within an industrial coatings market valued at approximately USD 222 billion in 2025. In these applications, residual solvent toxicity and odor are increasingly scrutinized due to consumer safety and indoor air quality requirements. DPhB’s favorable toxicological profile and low volatility position it as a practical alternative where solvent recovery and regulatory acceptance are critical to scale-up.

Carrier Solvent for Low-Volatility Agrochemical and Nutrient Formulations

- Agricultural formulations represent a structurally attractive opportunity for Dipropylene Glycol n-Butyl Ether, particularly as regulators target volatilization drift from herbicides. In September 2025, Health Canada’s Pest Management Regulatory Agency proposed restrictions on certain dicamba applications due to off-target movement. This regulatory pressure is accelerating interest in low-vapor-pressure carrier solvents that anchor active ingredients to plant surfaces.

- DPhB’s low volatility and coupling efficiency make it well-suited for use in low-volatility ester formulations of dicamba and 2,4-D, reducing drift risk without compromising efficacy. Additionally, agrochemical majors such as Bayer and Corteva are increasingly using glycol ethers as coupling agents to integrate hydrophobic micronutrients into water-based spray systems. DPhB improves rainfastness and formulation stability, aligning with global Farm to Fork objectives to reduce overall pesticide application rates while maintaining crop protection performance.

Dipropylene Glycol n-Butyl Ether (DPnB) Market Share and Segmentation Insights

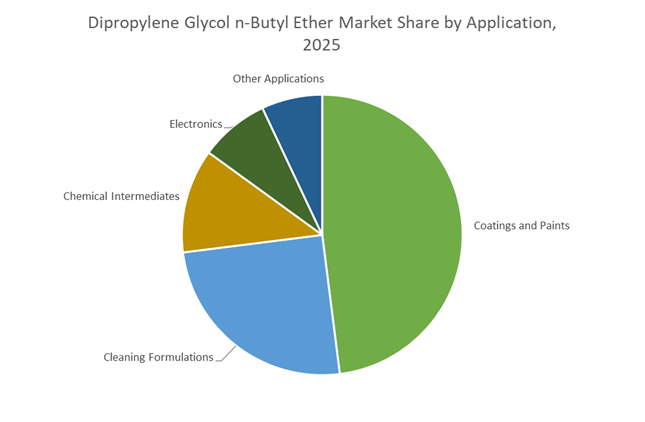

Coatings and Paints Dominate as Low-VOC Construction Fuels Growth

Coatings and paints command 48% of DPnB demand in 2025, positioning Dipropylene Glycol n-Butyl Ether as a core coalescing agent and solvent in waterborne architectural and industrial coatings. Its slow evaporation rate, strong solvency, and ability to reduce minimum film formation temperature make DPnB essential for high-quality, durable finishes in low-VOC formulations. Cleaning formulations represent a significant secondary segment, utilizing DPnB in industrial degreasers, hard surface cleaners, and graffiti removers where deep penetration and grease removal are required. Chemical intermediates consume DPnB as a building block for specialty esters and plasticizers in pharmaceutical and agrochemical synthesis. Electronics is a rapidly growing application, driven by use in photoresists, edge bead removers, and precision PCB cleaning requiring ultra-low residue. Other niche uses include printing inks, textile auxiliaries, and agricultural formulations that benefit from DPnB’s controlled evaporation profile.

Building and Construction Leads End Use as Electronics Accelerates

Building and construction account for 38% of DPnB consumption, driven by architectural paints, protective coatings, and construction sealants aligned with global adoption of environmentally compliant, low-VOC materials. Industrial manufacturing and maintenance form a major segment, using DPnB in equipment cleaning, industrial coatings, and facility upkeep where solvency and controlled drying improve operational efficiency. Automotive and transportation contribute significant volume through refinish coatings, component cleaning, and assembly aids. Consumer goods and household care rely on DPnB in DIY paints and household cleaners that demand performance with safety. Electrical and electronics represent the fastest-growing end-use, with high-purity DPnB increasingly specified for semiconductor processing, display manufacturing, and electronic materials cleaning, reinforcing its strategic role in advanced manufacturing value chains.

Competitive Landscape of the Dipropylene Glycol n-Butyl Ether (DPnB) Market

The Dipropylene Glycol n-Butyl Ether (DPnB) market in 2026 is defined by propylene oxide backward integration, low-odor solvent innovation, and accelerating demand from architectural coatings, I&I cleaners, automotive refinish, and electronics manufacturing. Competition centers on coalescent efficiency, REACH-compliant purity, bio-attributed grades, and APAC capacity expansion, with leading producers leveraging feedstock control and formulation expertise to defend margins.

Dow Inc. leads DPnB innovation with DOWANOL™ and low-odor solvent platforms

Dow Inc. anchors the global DPnB landscape through its flagship DOWANOL™ DPnB, one of the industry’s most effective slow-evaporating coalescents for water-borne latex coatings. In late 2025, Dow optimized its P-series glycol ether capacity on the U.S. Gulf Coast, directly addressing surging demand for high-solids architectural paints. Technically, Dow’s DPnB delivers exceptional surface tension reduction, making it a preferred solvent for industrial & institutional (I&I) cleaners targeting greasy soil removal. In early 2026, Dow introduced low-odor DPnB grades for indoor consumer paint systems, reinforcing its leadership in performance-driven, LVP-VOC-compliant solvent solutions.

LyondellBasell Industries scales DPnB through propylene oxide integration and China expansion

LyondellBasell Industries N.V. leverages world-class propylene oxide (PO) technology to secure a low-cost, integrated supply of DPnB for automotive and infrastructure markets. Its expanded Sinopec joint venture in China (early 2026) significantly increased regional PO output, strengthening DPnB availability across Asia. The company dominates the automotive refinish segment, where DPnB ensures film uniformity and high-gloss topcoats. In 2025, LyondellBasell achieved ISCC PLUS certification across multiple glycol ether sites, enabling bio-attributed DPnB for European customers. Feedstock integration remains its core strength, allowing consistent quality and pricing resilience in volatile solvent markets.

BASF SE drives electronics-grade DPnB via Zhanjiang Verbund and PCF transparency

BASF SE applies its Verbund manufacturing strategy to deliver high-purity DPnB for electronics, industrial coatings, and specialty cleaning. During 2025–2026, BASF positioned its Zhanjiang Verbund site in China as a central APAC hub for downstream glycol ethers, bypassing logistics bottlenecks while improving regional service levels. Marketed within the Solvenon™ range, BASF’s DPnB meets strict EU REACH standards and is increasingly supplied in electronics-grade purity for semiconductor photoresists and PCB cleaning. Strategically, BASF is piloting Product Carbon Footprint (PCF) tracking, allowing customers to quantify CO2 impact per kilogram of solvent, reinforcing its decarbonization roadmap.

Eastman Chemical Company targets agrochemical formulations with high-value specialty glycol ethers

Eastman Chemical Company competes in the premium DPnB segment, emphasizing specialty glycol ethers with optimized hydrophilic-hydrophobic balance for complex formulations. The company is a major supplier to agrochemical in-can systems, where DPnB functions as both penetrant and stabilizer for active ingredients. In early 2026, Eastman implemented price adjustments across North America to reflect rising precursor costs, while doubling down on formulation consultation services for coatings manufacturers. Its co-solvent expertise enables customers to fine-tune DPnB ratios for precise drying times and film formation, positioning Eastman as a performance partner rather than a commodity solvent supplier.

Jiangsu Yida Chemical Co., Ltd. emerges as a high-volume APAC challenger with 12% global DPnB output

Jiangsu Yida Chemical Co., Ltd. has rapidly become one of the world’s largest DPnB producers, accounting for nearly 12% of global volume in 2026 following a major 2024–2025 debottlenecking program. The company is aggressively expanding exports into the Middle East and Africa, positioning itself as a cost-competitive alternative to Western majors. Strategically, Yida is investing in ultra-pure DPnB grades to penetrate display and semiconductor cleaning applications under its “High-End Substitution” initiative. Deep vertical integration within China’s petrochemical ecosystem provides a decisive cost advantage, accelerating its rise in the global merchant DPnB market.

United States: TSCA Endorsement and Price-Led Margin Reset

The U.S. dipropylene glycol n-butyl ether market is being shaped by regulatory certainty and disciplined pricing strategies. Effective February 1, 2025, Dow implemented a $0.10 per pound price increase for DOWANOL DPnB across North America, reflecting a strategic recalibration to absorb sustained feedstock volatility and higher operating costs across the Gulf Coast petrochemical network. This pricing action signaled confidence in downstream demand resilience, particularly from coatings and industrial cleaning segments that value DPnB’s balance of solvency and low toxicity.

From a regulatory standpoint, the EPA’s TSCA risk evaluations finalized in late 2024 reaffirmed DPnB’s status as a preferred low-toxicity solvent relative to ethylene-series glycol ethers. This endorsement has driven a measurable procurement shift, with U.S. industrial cleaning formulators reporting a 12% reallocation toward DPnB to qualify for Safer Choice aligned product portfolios. Demand momentum is further reinforced by the secondary automotive refurbishing market. Rising vehicle repair and repainting activity through Q3 2025 has increased consumption of DPnB-based waterborne coatings that deliver superior coalescence, block resistance, and film uniformity. On the supply side, Monument Chemical expanded domestic high-purity solvent capacity through the optimization of its Bayport, Texas facility, strengthening U.S. supply security for electronics and specialty intermediate customers.

China: Policy-Driven Upgrading and EV Coatings Pull

China’s DPnB market trajectory is tightly aligned with industrial upgrading policies rather than short-term price cycles. Under the Ministry of Industry and Information Technology’s 2025 Petrochemical Industry Growth Stabilization Plan, incentives have been directed toward P-series glycol ethers to accelerate the transition from bulk chemicals to high-purity, application-specific solvents. This policy shift is reshaping domestic investment priorities, particularly within electronic-grade and advanced coatings solvent lines.

Demand-side growth is anchored in electric vehicle manufacturing and environmental compliance. With China targeting a 20% EV penetration rate by 2026, coating formulators have introduced DPnB-blended waterborne primers that enable thinner, lighter coatings while maintaining adhesion and corrosion resistance. These formulations contribute to incremental vehicle weight reduction, supporting battery efficiency targets. Simultaneously, updated 2025 VOC and biodegradability standards from the Ministry of Ecology and Environment require architectural coating plants, especially in the Pearl River Delta, to adopt solvents exceeding 90% biodegradability. This regulatory filter structurally favors DPnB over mineral spirits. Export logistics have also matured. AI-enabled supply chain coordination introduced in 2025 across major glycol ether hubs has cut port-to-customer lead times by approximately 15%, supporting annual exports exceeding 45,000 metric tons of P-series ethers.

Germany: Non-VOC Classification and Energy-Efficient Integration

Germany represents a regulation-buffered but cost-sensitive DPnB market within the European Union. As of January 2026, DPnB continues to be classified as a non-VOC substance under Directive 2004/42/EC for specific architectural coatings, insulating it from the aggressive solvent phase-outs affecting aromatic hydrocarbons. This classification has preserved DPnB’s role in waterborne coatings and industrial maintenance applications even as broader solvent restrictions tighten.

At the same time, heightened scrutiny of chemical imports under Regulation 2025/1151 has encouraged domestic producers to double down on integrated manufacturing models. BASF and other German producers are leveraging Verbund integration to offset high regional energy costs through superior feedstock and heat recovery efficiency. Beyond coatings, German chemical parks have expanded the use of DPnB-modified cleaning solvents in precision heat exchanger maintenance. Field data from 2025 indicates improved removal of carbonized residues, translating into higher thermal efficiency and reduced downtime for energy-intensive industrial operations.

India: Localization Push and Infrastructure-Driven Consumption

India’s DPnB market is transitioning from import reliance to localized production, supported by policy-driven capital formation. The Production Linked Incentive framework for specialty chemicals has catalyzed approximately ₹1.5 lakh crore in investments through 2025, enabling domestic producers to scale P-series glycol ether capacity for pharmaceutical, paint, and infrastructure applications. This localization effort is strategically important as downstream users seek consistent supply and pricing stability.

Pharmaceutical demand has emerged as a notable growth vector. In 2025, major API manufacturing hubs in Hyderabad reported a 9% increase in DPnB usage for selected crystallization and formulation processes, reflecting its favorable solvency profile and regulatory acceptance. Infrastructure spending under the Smart Cities Mission has further expanded consumption. DPnB is increasingly specified as a primary coalescent in weather-resistant, water-based wood and metal coatings used across public buildings and urban assets, aligning durability requirements with evolving environmental norms.

South Korea: Electronic-Grade Differentiation and Export Stability

South Korea’s DPnB market is distinguished by its emphasis on ultra-high purity and export orientation. In Q4 2025, domestic manufacturers achieved a 99.9% purity benchmark for DPnB tailored to next-generation OLED panel cleaning. This milestone positions South Korea as a preferred supplier for electronics-grade solvents where trace impurities directly impact yield and device performance.

Despite global petrochemical pricing pressure, South Korean exports of specialty ethers remained resilient throughout 2025. Preferential access under the Korea-ASEAN Free Trade Agreement has preserved tariff advantages in Southeast Asian markets, allowing Korean producers to sustain volumes even as North American competitors face higher landed costs. This combination of purity leadership and trade alignment continues to underpin South Korea’s role in the regional DPnB supply chain.

Dipropylene Glycol n-Butyl Ether Market: Country-Level Strategic Snapshot

Dipropylene Glycol n-Butyl Ether Market County Level Snapshot

|

Country

|

Primary Market Driver

|

Key Demand Anchors

|

Strategic Positioning

|

|

United States

|

TSCA preference, pricing discipline

|

Industrial cleaning, automotive refurbishing

|

Regulation-backed substitution

|

|

China

|

Policy-led upgrading

|

EV coatings, architectural coatings

|

High-purity domestic scaling

|

|

Germany

|

Non-VOC protection, integration

|

Waterborne coatings, industrial maintenance

|

Energy-efficient compliance

|

|

India

|

Localization incentives

|

Pharma solvents, urban infrastructure

|

Import replacement growth

|

|

South Korea

|

Ultra-high purity focus

|

OLED cleaning, ASEAN exports

|

Electronics-grade leadership

|

Dipropylene Glycol n-Butyl Ether Market Report Scope

Dipropylene Glycol n-Butyl Ether Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.5 Million

|

|

Market Size (2034)

|

$27.3 Million

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Grade (Standard Grade, High Purity Grade, Electronic Grade), By Application (Coatings and Paints, Cleaning Formulations, Chemical Intermediates, Electronics, Other Applications), By End-User Industry (Building and Construction, Automotive and Transportation, Electrical and Electronics, Industrial Manufacturing and Maintenance, Consumer Goods and Household Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., LyondellBasell Industries Holdings B.V., BASF SE, Eastman Chemical Company, Indovinya, Manali Petrochemicals Limited, SABIC, INEOS Oxide, Monument Chemical, Jiangsu Ruijia Chemistry Co., Ltd., Yida Chemical, Shell Chemicals, Huntsman Corporation, KH Neochem Co., Ltd., Shiny Chemical Industrial Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dipropylene Glycol n-Butyl Ether Market Segmentation

By Grade

- Standard Grade

- High Purity Grade

- Electronic Grade

By Application

- Coatings and Paints

- Cleaning Formulations

- Chemical Intermediates

- Electronics

- Other Applications

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Electrical and Electronics

- Industrial Manufacturing and Maintenance

- Consumer Goods and Household Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dipropylene Glycol n-Butyl Ether Industry

- Dow Inc.

- LyondellBasell Industries Holdings B.V.

- BASF SE

- Eastman Chemical Company

- Indovinya

- Manali Petrochemicals Limited

- SABIC

- INEOS Oxide

- Monument Chemical

- Jiangsu Ruijia Chemistry Co., Ltd.

- Yida Chemical

- Shell Chemicals

- Huntsman Corporation

- KH Neochem Co., Ltd.

- Shiny Chemical Industrial Co., Ltd.

*- List not Exhaustive