EB PVD Coatings in Gas Turbine Market Size Expansion Driven by Advanced Thermal Barrier Technologies and Aerospace Demand

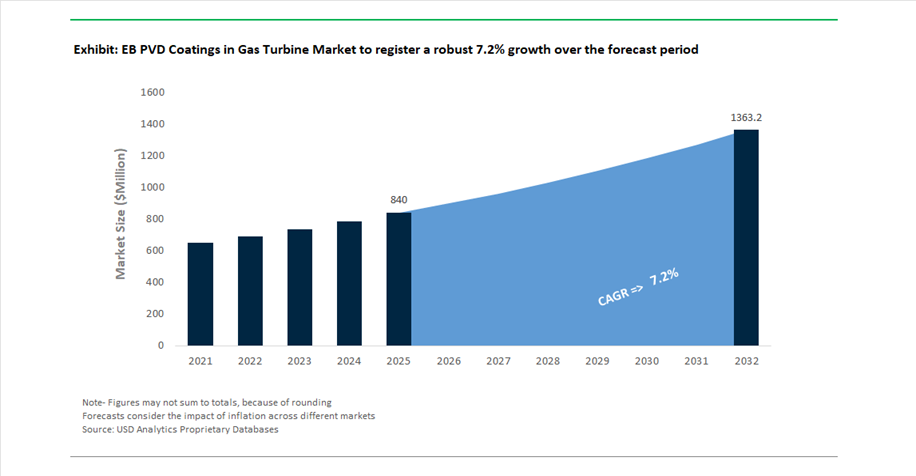

The EB PVD Coatings in Gas Turbine Market reached a valuation of USD 840 million in 2025 and is projected to grow at a CAGR of 7.2% through 2032, reaching USD 1,366.6 million by 2032. This robust growth trajectory is underpinned by the increasing adoption of electron beam physical vapor deposition (EB-PVD) coatings in high-temperature gas turbine environments, particularly within aerospace propulsion systems and industrial gas turbines (IGTs). EB-PVD coatings are critical for enabling thermal barrier coatings (TBCs) that enhance turbine efficiency, extend component lifespan, and support higher operating temperatures essential for next-generation engines.

The market is being structurally reshaped by the rapid evolution of ceramic matrix composites (CMCs), advanced superalloys, and high-efficiency turbine architectures. EB-PVD technology is uniquely suited to deposit columnar microstructures that provide superior strain tolerance and thermal cycling resistance compared to alternative coating techniques. This makes it indispensable in high-pressure turbine blades, vanes, and combustor components, particularly in engines operating under extreme thermal gradients exceeding 1,300°C.

A key macro driver is the resurgence of commercial aerospace and power generation investments, alongside the transition toward low-carbon fuels such as hydrogen and ammonia. These fuels introduce new chemical and thermal stresses inside turbine systems, increasing the demand for chemically resistant and high-performance EB-PVD coatings. Additionally, OEMs are increasingly prioritizing vertical integration of coating capabilities, ensuring tighter control over quality, cost, and supply chain resilience.

AI-Enabled EB-PVD Systems, Aerospace Qualification Breakthroughs, and Strategic Capacity Expansion Reshape Market Dynamics

The EB PVD coatings market is experiencing accelerated innovation and consolidation, driven by next-generation coating systems, aerospace qualification milestones, and strategic capacity investments. In February 2026, ALD Vacuum Technologies launched the SinCoat NG, a next-generation EB-PVD system equipped with a dual 80 kW electron beam configuration and in-situ laser triangulation for real-time thickness monitoring. Designed for industrial gas turbines, the system has already secured orders from major European OEMs, highlighting rising demand for precision-controlled coating systems capable of handling large turbine blades up to 850 mm.

A major technological milestone was achieved in January 2026, when GE Aerospace qualified a double-ceramic-layer EB-PVD TBC system for its GE9X engine platform. By integrating gadolinium zirconate with yttria-stabilized zirconia (YSZ), the coating demonstrated a 30% improvement in spallation life, directly enhancing turbine durability and reliability for long-haul aircraft applications such as the 777X program. Complementing this, Applied Materials introduced the Centura EB-PVD Pro platform in October 2025, leveraging AI-driven beam modulation to achieve coating uniformity within ±2%, addressing one of the key technical challenges in coating complex airfoil geometries.

Strategic consolidation is also reshaping the competitive landscape. In December 2025, Howmet Aerospace announced the $1.8 billion acquisition of Consolidated Aerospace Manufacturing (CAM) to strengthen its position in turbine components and coating integration. Meanwhile, Safran Aircraft Engines commissioned a dedicated EB-PVD production line in July 2025 with an annual capacity exceeding 200,000 blade coatings, signaling a clear shift toward vertical integration and reduced dependency on third-party coating service providers.

Material innovation remains central to long-term market evolution. In February 2025, Rolls-Royce validated ytterbium silicate EB-PVD environmental barrier coatings (EBCs) for silicon carbide CMC components, paving the way for next-generation turbine architectures expected post-2029. Additionally, Jiangshan Scotech Electrical Co. received AVIC certification in April 2025 for EB-PVD systems used in the COMAC C919 program, marking a significant advancement in China’s domestic aerospace coating capabilities.

Emerging fuel technologies are also influencing coating requirements. In March 2026, IHI Corporation and GE Vernova successfully demonstrated 100% ammonia combustion in gas turbines, introducing new corrosion environments that necessitate advanced EB-PVD coating chemistries. Additionally, Oerlikon Balzers launched BALORA TECH PRO in July 2024, targeting high-temperature wear applications and offering a cost-performance alternative bridging conventional PVD and EB-PVD solutions.

US DOE Hydrogen-Ready Turbine Targets Driving 1650°C Thermal Barrier Coating Innovation

The advancement of hydrogen-ready gas turbine technologies under the U.S. Department of Energy National Energy Technology Laboratory programs is setting a new performance frontier for EB-PVD coatings, particularly in high-temperature thermal barrier coating applications. By 2026, the DOE’s focus on achieving turbine inlet temperatures exceeding 1650°C is pushing coating systems beyond conventional yttria-stabilized zirconia limits, requiring significant improvements in phase stability, thermal insulation, and durability. EB-PVD remains the preferred deposition technology due to its ability to produce strain-tolerant columnar microstructures capable of withstanding extreme thermal gradients in next-generation turbine environments. Achieving these elevated temperature thresholds is directly linked to combined-cycle power plant efficiency improvements beyond 65%, making advanced EB-PVD coatings a critical enabler of energy efficiency and decarbonization strategies. Ongoing research efforts are targeting a 30% reduction in thermal conductivity compared to standard 7–8 weight percent YSZ through cluster doping and lattice defect engineering, enhancing insulation performance without compromising structural integrity. Durability benchmarks have also intensified, with coatings required to exceed 24,000 hours of base-load operation under hydrogen-rich combustion conditions, where elevated water vapor accelerates degradation mechanisms. Additionally, improved coating performance enables a 10% to 15% reduction in turbine cooling air requirements, directly increasing net power output and lowering fuel consumption across advanced turbine systems.

Rare Earth Oxide Supply Chain Volatility Reshaping EB-PVD Feedstock Strategy and Material Innovation

Geopolitical constraints on rare earth element supply chains are emerging as a critical factor influencing EB-PVD coating production economics and material innovation pathways. China’s export control measures introduced during 2025–2026 have significantly impacted the availability and pricing of key rare earth oxides such as yttrium, gadolinium, and dysprosium, which are essential for high-performance thermal barrier coatings. The cost of high-purity gadolinium oxide experienced a sharp increase of approximately 40% in early 2026, creating substantial pricing pressure across advanced coating systems, particularly pyrochlore-based materials. In response, the European Union’s Critical Raw Materials Act, fully operational in 2026, has designated rare earth oxides used in EB-PVD processes as strategic materials, requiring manufacturers to source at least 10% of these inputs from recycled feedstock by 2030. This regulatory push is accelerating investment in recycling technologies and circular material flows within the coatings supply chain. At the manufacturing level, coating facilities are optimizing EB-PVD equipment design to improve material utilization efficiency, increasing usage rates from legacy levels of approximately 15% to over 25%, significantly reducing raw material waste. Concurrently, research into rare-earth-lean alternatives such as alumina-based and silicate-based environmental barrier coatings is gaining traction, particularly for lower-temperature turbine sections. These developments are driving a strategic shift toward supply chain resilience, cost optimization, and material substitution across the EB-PVD coatings industry.

Controlled Porosity Columnar EB-PVD Coatings Enhancing Strain Tolerance and Thermal Efficiency

Advancements in EB-PVD coating microstructure engineering are creating new opportunities for high-performance thermal barrier systems through the optimization of columnar architectures and controlled porosity. By precisely tuning inter-columnar spacing and feather-like growth structures, manufacturers are achieving coatings that combine enhanced strain tolerance with improved thermal insulation properties. These next-generation coatings are capable of withstanding more than 2,000 thermal shock cycles between 1300°C and ambient conditions without delamination, addressing one of the key failure mechanisms in turbine applications. The ability to engineer controlled porosity also enables thinner coating layers while maintaining equivalent thermal protection, contributing to weight reductions of up to 5 kilograms in mid-sized aero-engine rotating components. Surface finish advantages further differentiate EB-PVD from alternative deposition methods such as air plasma spray, with coatings achieving surface roughness values below 1.0 micrometer, which reduces aerodynamic drag and preserves the functionality of film-cooling holes in turbine blades. Additionally, doping with pentavalent oxides such as tantalum oxide and niobium oxide is improving resistance to sintering at temperatures exceeding 1400°C, ensuring long-term compliance and structural flexibility throughout extended service cycles. These microstructural innovations are positioning EB-PVD as a critical technology for next-generation aerospace and power generation systems requiring high reliability under extreme thermal conditions.

Multilayer EB-PVD Thermal Barrier Coatings for Hydrogen Combustion Turbine Applications

The transition toward hydrogen-based power generation is unlocking significant opportunities for multilayer EB-PVD coating architectures designed to withstand the unique challenges of high-moisture, high-temperature combustion environments. In 2026, advanced thermal barrier coating systems are adopting a dual-layer configuration, combining a yttria-stabilized zirconia base layer for mechanical toughness and adhesion with a rare-earth zirconate top layer, such as gadolinium zirconate, for superior thermal insulation and resistance to CMAS attack. This layered approach provides a robust defense mechanism against molten calcium-magnesium-alumina-silicate deposits, which can infiltrate and degrade conventional coatings at temperatures above 1250°C. The rare-earth top layer reacts with these contaminants to form a stable apatite phase, effectively sealing coating porosity and preventing structural stiffening. Hydrogen combustion environments also introduce significantly higher water vapor concentrations, approximately 2.5 times those of natural gas systems, accelerating thermally grown oxide formation at the bond coat interface. Multilayer EB-PVD systems are demonstrating a 50% reduction in TGO growth rates under these conditions, extending coating lifespan and improving operational reliability. These advanced coatings are increasingly specified for retrofit applications in H-class turbines, where they contribute to net heat rate improvements of approximately 2%, enhancing overall plant efficiency and supporting the transition to low-carbon energy systems.

HPT Blade Coatings Dominate EB-PVD Gas Turbine Market with 52% Share Driven by Extreme Thermal Protection Needs

Component Analysis: High-Pressure Turbine Blades Lead with Advanced Thermal Barrier Coating (TBC) Systems

High-Pressure Turbine (HPT) blades account for a dominant 52.0% share of the EB-PVD coatings market in gas turbines in 2025, driven by their exposure to the most thermomechanically extreme conditions within turbine engines. Operating at temperatures exceeding 1,600°C, these components rely on Electron Beam Physical Vapor Deposition (EB-PVD) Yttria-Stabilized Zirconia (YSZ) thermal barrier coatings (TBCs) to reduce substrate temperatures by 100–200°C, preventing creep, oxidation, and catastrophic failure. The unique columnar microstructure of EB-PVD coatings enables exceptional strain tolerance during thermal cycling, ensuring long-term durability compared to conventional coatings. These coatings function as part of a multi-layer system, including bond coats (MCrAlY or platinum-aluminide) and advanced internal cooling mechanisms, critical for maintaining turbine efficiency and lifespan. This makes HPT blades the largest and most technically demanding segment in the global EB-PVD coatings market for gas turbines.

MRO Segment Leads EB-PVD Market with 56% Share Driven by Recoating Cycles and Cost-Efficiency in Turbine Maintenance

Service Type Analysis: Maintenance, Repair, and Overhaul (MRO) Drives Recurring Demand for Coating Services

The Maintenance, Repair, and Overhaul (MRO) segment dominates with a 56.0% share of the EB-PVD coatings market in 2025, fueled by the large global installed base of aero and industrial gas turbine engines. High-value turbine components such as HPT blades undergo multiple recoating cycles (2–3 times) over their operational lifespan, as coatings degrade under extreme thermal and mechanical stress. Recoating services provide a highly cost-effective alternative to replacement, with individual blades costing $10,000–$30,000+, making repair and reuse economically critical for operators. Advanced repair-grade EB-PVD coating technologies have been developed to address the metallurgical changes in service-run components, ensuring reliable performance after refurbishment. This recurring demand, combined with the economic advantages of repair over replacement, positions the MRO segment as the primary growth driver in the EB-PVD coatings market for gas turbines.

EB-PVD Coatings in Gas Turbine Market Competitive Landscape Driven by Thermal Barrier Coatings, Superalloy Integration, and MRO Demand

The EB-PVD coatings market in gas turbines is highly specialized, driven by demand for thermal barrier coatings (TBCs), high-efficiency turbines, and MRO services. Competition centers on advanced ceramic coatings, columnar microstructures, and integration with superalloy blade manufacturing for aerospace and industrial gas turbines.

Howmet Aerospace Leads EB-PVD Integration with Single-Crystal Blade Manufacturing and Digital Process Control

Howmet Aerospace Inc. dominates the EB-PVD coatings market through unmatched vertical integration, combining single-crystal superalloy blade casting with in-house EB-PVD thermal barrier coating capabilities. The company reported $8.3 billion in 2025 revenue, with its Gas Turbines segment growing 25% due to demand from AI-driven data center infrastructure. Its acquisition of CAM strengthens integration across turbine components and fastening systems. Howmet’s Digital Plume Control innovation enhances yttria distribution in EB-PVD coatings, reducing material waste by 12% and improving coating uniformity. The company is scaling production to meet a projected 32% growth in turbine demand. Its leadership in integrated turbine manufacturing and coating technologies positions it at the forefront of the EB-PVD market.

Oerlikon Advances Hybrid EB-PVD and APS Coatings with High-Entropy Oxide Innovation

Oerlikon, through its Balzers and Metco divisions, is advancing EB-PVD coatings with hybrid architectures that combine APS and EB-PVD processes for enhanced thermal performance. Its BALORA™ TECH PRO environmental barrier coatings target high-efficiency turbine hot-gas path components. The company is pioneering high-entropy oxide coatings, offering improved thermal stability compared to traditional 8YSZ systems. Oerlikon’s Smart Integrated Surface Solutions model supports OEMs with end-to-end coating services. Its expansion in India strengthens its presence in high-growth turbine markets. The company’s focus on advanced materials and hybrid coating technologies enhances its competitive position in EB-PVD coatings.

Praxair Surface Technologies Strengthens High-Strain EB-PVD Coatings with Triple-Layer Systems

Praxair Surface Technologies, a Linde company, leads in EB-PVD coatings with high strain tolerance and low thermal conductivity, delivering superior thermal protection for advanced gas turbines. Its columnar coatings achieve thermal conductivity as low as 1.7–1.8 W/m K, significantly improving insulation performance. The company expanded its U.S. facilities to support MRO demand for advanced engine programs such as LEAP and GE9X. Its triple-layer TBC system addresses CMAS infiltration, enhancing durability in harsh desert environments. PST’s R&D efforts focus on reducing heat transfer by 20% for next-generation turbines operating at 1,600°C. Its expertise in advanced ceramic coatings strengthens its leadership in EB-PVD technologies.

Chromalloy Expands EB-PVD Coating Services with LifeX Asset Extension Solutions

Chromalloy is strengthening its position in EB-PVD coatings through its Belac Coatings Center of Excellence, which supports advanced TBC applications for high-pressure turbine components. Its LifeX solutions extend the lifespan of aging turbine assets, addressing demand from operators prioritizing refurbishment over replacement. Chromalloy’s integrated capabilities in casting, coating, and machining reduce supply chain lead times by up to 20%. The company is leveraging its FAA-approved PMA parts expertise to offer performance-as-a-service models. Its focus on lifecycle extension and MRO services aligns with global turbine maintenance trends. Chromalloy’s integrated service model enhances its competitiveness in EB-PVD coatings.

ALD Vacuum Technologies Leads EB-PVD Equipment Market with SmartCoater™ Precision Systems

ALD Vacuum Technologies, part of AMG Advanced Metallurgical Group, holds 17% of the global EB-PVD equipment market. Its SmartCoater™ systems feature in-situ laser monitoring, ensuring coating thickness precision within ±2 microns for turbine components. The company reported 40% growth in coating system orders in 2025, driven by demand for high-capacity multi-source chambers. ALD is enabling Industry 4.0 integration through modular vacuum logistics, allowing seamless incorporation of EB-PVD systems into automated production lines. Its focus on precision engineering and scalability supports OEM requirements. ALD’s equipment leadership underpins the global EB-PVD coatings ecosystem.

Sulzer Expands EB-PVD Coating Services for Hydrogen Turbines and MRO Applications

Sulzer is strengthening its EB-PVD coatings presence by focusing on the MRO segment, which accounts for 45% of coating demand in industrial gas turbines. The company is deploying robotic stripping and re-coating technologies to restore turbine blade performance to OEM standards. Sulzer is also developing coatings for hydrogen-powered turbines, addressing challenges such as hydrogen embrittlement and steam corrosion. Its service segment reported a 12% margin improvement in 2025, supported by digitalized supply chain operations. The company is capitalizing on steady EB-PVD market growth driven by energy transition trends. Sulzer’s focus on advanced coatings and maintenance services enhances its market position.

United States EB-PVD Coatings Market (Gas Turbines): Advanced Ceramics and Defense Programs Driving Global Leadership

The United States leads the Electron Beam Physical Vapor Deposition (EB-PVD) coatings market for gas turbines, driven by defense programs and next-generation energy systems. Major investments under the Next Generation Air Dominance (NGAD) program are advancing EB-PVD coatings for single-crystal turbine blades, enabling higher efficiency engines.

R&D is heavily focused on durability under extreme conditions. DOE-funded programs (2025–2026) are developing gadolinium zirconate (Gd₂Zr₂O₇) coatings to resist CMAS degradation in high-temperature turbine sections. Industry leaders like GE Aerospace and Pratt & Whitney are expanding coating centers with robotic deposition systems achieving ±2% thickness uniformity. Additionally, hybrid coating architectures combining EB-PVD and magnetron sputtering are improving adhesion and lifespan, while high-rate deposition technologies (up to 10 μm/min) are reducing MRO turnaround times. Environmental regulations are also accelerating the shift toward vacuum-based EB-PVD processes over plasma spray methods.

Germany EB-PVD Coatings Market: Hydrogen Transition and Microstructural Innovation Driving Efficiency

Germany is a global leader in high-efficiency turbine coatings, particularly for stationary gas turbines used in combined heat and power (CHP) systems. Under the Energiewende initiative, EB-PVD coatings are enabling turbines to operate at temperatures ~150°C above alloy melting points, significantly improving efficiency.

Innovation is centered on material science. Research institutions are developing rare-earth-doped zirconia coatings that reduce thermal conductivity by ~30%, enhancing insulation performance. The integration of digital twin monitoring systems in coating chambers allows real-time optimization of deposition processes. Additionally, government support for hydrogen-ready turbines is driving demand for coatings that can withstand higher moisture and heat flux. Strict EU regulations are also accelerating the transition toward lead-free and chrome-free EB-PVD processes, reinforcing Germany’s sustainability leadership.

China EB-PVD Coatings Market: Aero-Engine Self-Reliance and Supply Chain Control Driving Expansion

China is rapidly scaling its EB-PVD capabilities to achieve aero-engine independence, particularly for programs like COMAC C919 and C929. The government has commissioned 15+ new EB-PVD machines (2024–2025) to support turbine blade coatings for the CJ-1000A engine.

A key advantage is supply chain dominance. China controls over 80% of the global rare-earth supply, ensuring cost-efficient production of yttria-stabilized zirconia (8YSZ) coatings. Investments such as the $1.8 billion Greater Bay Area Aero-Engine Park are expanding research and manufacturing capacity. Additionally, military upgrades and power generation projects are increasing demand for thermal barrier coatings (TBCs) capable of operating at higher turbine entry temperatures. Rapid growth in patent filings also highlights China’s rising innovation in EB-PVD technologies.

United Kingdom EB-PVD Coatings Market: Aerospace Innovation and Green MRO Driving Specialized Growth

The UK is a critical hub for aerospace EB-PVD coatings, driven by Rolls-Royce and strong R&D ecosystems. The development of the UltraFan engine has introduced double-layer thermal barrier coatings, combining dense top layers with strain-tolerant bases for improved durability.

Sustainability is a key focus. The Midlands aerospace cluster is transitioning toward “Green MRO” practices, favoring EB-PVD for its lower environmental impact. Government-backed initiatives through the Aerospace Technology Institute (ATI) are funding advanced coating technologies, including high-rate deposition of environmental barrier coatings (EBCs). Innovations such as laser-assisted EB-PVD are improving coating density and performance, while marine turbine applications are expanding demand for corrosion-resistant coatings.

Japan EB-PVD Coatings Market: Precision Manufacturing and Thermal Management Driving High-End Innovation

Japan’s EB-PVD market is defined by precision engineering and material purity, critical for advanced turbine systems. Companies like Mitsubishi Heavy Industries (MHI) are expanding facilities to support high-efficiency gas turbines, including new coating lines at Takasago Works.

Technological innovation is focused on thermal performance. The development of zig-zag columnar microstructures within EB-PVD coatings improves thermal insulation by disrupting heat transfer. Japan also leads in ultra-high-purity zirconia feedstock production, ensuring consistent coating quality. Advanced automation using AI-driven robotic arms enables uniform coating of complex turbine geometries, eliminating shadowing effects. These capabilities position Japan as a leader in high-precision EB-PVD coating technologies.

France EB-PVD Coatings Market: Defense Programs and Clean Energy Driving Dual-Sector Growth

France plays a major role in both defense and energy applications of EB-PVD coatings. Upgrades to the Rafale fighter’s M88 engine are utilizing advanced coatings to extend service intervals by ~25%, improving operational efficiency.

The commercial aviation sector is also expanding. Safran is scaling EB-PVD capacity to support the LEAP engine program, addressing strong global demand. Additionally, France’s low-carbon strategy is promoting EB-PVD coatings for high-efficiency gas turbines in industrial applications. Emerging research into Small Modular Reactors (SMRs) is further expanding use cases, while new service centers in Toulouse are strengthening maintenance capabilities.

India EB-PVD Coatings Market: Localization and Energy Transition Driving Emerging Growth

India is transitioning into a self-reliant EB-PVD coatings hub, supported by government initiatives under Atmanirbhar Bharat. The Ministry of Defence is incentivizing local development of EB-PVD systems for indigenous engine programs such as Kaveri and HAL engines.

Energy transition is a key driver. As India increases non-fossil energy capacity, gas turbines are being used for peak-load balancing, requiring coatings that can withstand frequent thermal cycling. Companies like BHEL are investing in vacuum coating technologies to upgrade aging turbine infrastructure. Additionally, foreign investment is strengthening capabilities, with new coating technical centers (e.g., Bengaluru, 2026) providing localized services. Strategic stockpiling of zirconia and yttria is also ensuring supply chain resilience, positioning India as an emerging player in advanced turbine coatings.

EB PVD Coatings in Gas Turbine Market Report Scope

EB PVD Coatings in Gas Turbine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$840 Million

|

|

Market Size (2032)

|

$1366.6 Million

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Coating Function (Thermal Barrier Coatings, Environmental Barrier Coatings, Oxidation and Corrosion Resistant Coatings, Abradable), By Material Composition (Ceramic Top Coats, Metallic Bond Coats, Advanced Multi-layered), By Turbine Component (High-Pressure Turbine, Combustion Section, Other Hot Section Components), By End-Use Industry (Aerospace, Industrial Gas Turbines, Marine Gas Turbines), By Service Type (OEM, MRO), By Substrate Material (Nickel-based Superalloys, Cobalt-based Superalloys, Ceramic Matrix Composites)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oerlikon Group, Howmet Aerospace Inc., Praxair Surface Technologies, Chromalloy Gas Turbine LLC, GE Aerospace, Pratt & Whitney, Rolls-Royce plc, MTU Aero Engines AG, Safran S.A., IHI Corporation, Liburdi Turbine Services, ALD Vacuum Technologies GmbH, Siemens Energy AG, Mitsubishi Heavy Industries, Ltd., Aalberts Surface Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

EB PVD Coatings in Gas Turbine Market Segmentation

By Coating Function

- Thermal Barrier Coatings

- Environmental Barrier Coatings

- Oxidation and Corrosion Resistant Coatings

- Abradable

By Material Composition

- Ceramic Top Coats

- Yttria-Stabilized Zirconia

- Rare-Earth Zirconates

- Alumina and Mullite-based

- Metallic Bond Coats

- Advanced Multi-layered

By Turbine Component

- High-Pressure Turbine

- Combustion Section

- Other Hot Section Components

By End-Use Industry

- Aerospace

- Industrial Gas Turbines

- Marine Gas Turbines

By Service Type

By Substrate Material

- Nickel-based Superalloys

- Cobalt-based Superalloys

- Ceramic Matrix Composites

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in EB PVD Coatings in Gas Turbine Market

- Oerlikon Group

- Howmet Aerospace Inc.

- Praxair Surface Technologies

- Chromalloy Gas Turbine LLC

- GE Aerospace

- Pratt & Whitney

- Rolls-Royce plc

- MTU Aero Engines AG

- Safran S.A.

- IHI Corporation

- Liburdi Turbine Services

- ALD Vacuum Technologies GmbH

- Siemens Energy AG

- Mitsubishi Heavy Industries, Ltd.

- Aalberts Surface Technologies

- You stopped this response

*- List not Exhaustive