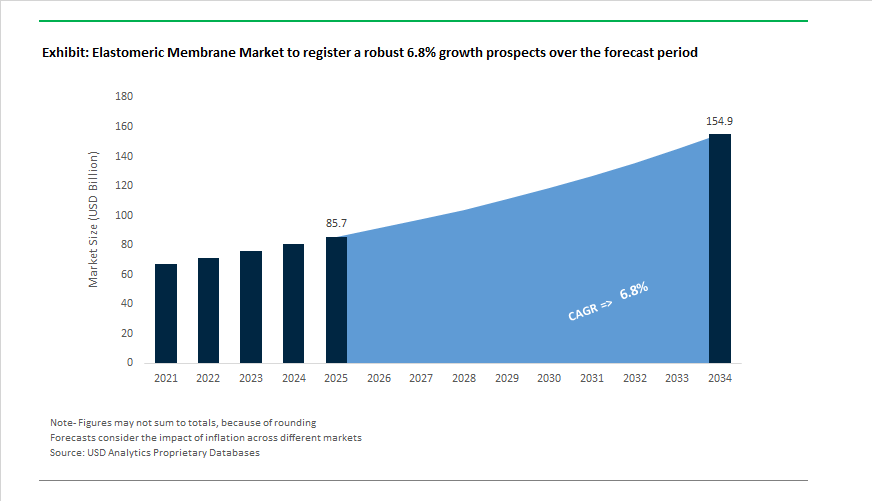

Elastomeric Membrane Market to Reach $154.9 Billion by 2034 at 6.8% CAGR as Cool Roofs, Bio-Based EPDM, and Integrated Building Envelopes Accelerate

The Elastomeric Membrane Market is projected to grow from $85.7 billion in 2025 to $154.9 billion by 2034, expanding at a CAGR of 6.8%. Market expansion is being shaped by regulatory-driven energy efficiency standards, rising reroofing demand, and the integration of low-carbon materials into commercial and residential building envelopes. In January 2026, Sika introduced Sikalastic®-701, a next-generation polyurethane liquid-applied membrane engineered for high UV resistance and solar reflectivity. Field-tested in Spain, Dubai, and Malaysia, the product aligns with the global cool roof movement aimed at reducing urban heat island intensity and lowering HVAC loads in high-density cities.

Sustainability innovation is increasingly embedded in elastomer chemistry. In 2025, Dow launched NORDEL™ REN EPDM, a bio-based ethylene propylene diene monomer feedstock that enables manufacturers to lower the embodied carbon of roofing and façade membranes. This shift supports LEED-certified construction and ESG-driven procurement mandates. Complementing this trend, Sika launched the SikaMembran®-820 Allround system in August 2025, a hybrid EPDM façade membrane that delivers four times the tensile strength of traditional alternatives despite being half the thickness. The product also claims a 50% lower carbon footprint and pairs with solvent-free Sikaflex®-525 adhesive systems, reinforcing the transition toward low-emission construction materials.

Strategic acquisitions are redefining competitive positioning within the elastomeric waterproofing landscape. In October 2025, Holcim signed a binding agreement to acquire Xella for approximately €1 billion, expanding its Building Solutions portfolio. The deal, expected to close in H2 2026, creates cross-selling opportunities between high-value elastomeric membranes and sustainable walling systems. Carlisle Companies reinforced its Carlisle Construction Materials (CCM) platform during 2025 with $110 million in acquisitions targeting labor-efficient and environmentally responsible envelope systems. By February 2026, Carlisle reported $1.1 billion in operating cash flow for 2025, underlining the resilience of reroofing and retrofit demand in North America.

Regional production investments continue to strengthen supply capacity. In March 2024, Mapei inaugurated a $13.9 million facility in Portugal to expand elastomeric waterproofing output while integrating installer training via the Mapei Academy. Saint-Gobain, through CertainTeed and GCP, introduced an integrated six-sided waterproofing system in 2024, combining elastomeric membranes with structural moisture barriers for complex commercial geometries. Meanwhile, SOPREMA secured a major Indian infrastructure project in 2024 using its Colphene BSW SBS elastomeric bitumen membrane, reflecting strong growth in South Asian urban waterproofing demand.

Sustainability recognition and material innovation continue to influence procurement. Sika received a Silver EcoVadis rating in August 2025, acknowledging advances in bio-based amine hardeners and low-emission adhesives. At the May 2025 Venice Biennale, Holcim showcased biochar-embedded construction materials, a technology being adapted to elastomeric membranes to create carbon-sequestering roofing solutions. These developments indicate that elastomeric membranes are evolving beyond waterproofing into multifunctional building envelope systems that combine durability, thermal performance, structural integration, and carbon reduction across global construction markets.

Trends and Opportunities in the Elastomeric Membrane Market

Stringent Building Energy Code Revisions Driving Air and Vapor Barrier Adoption

- Building energy codes are increasingly mandating continuous air and vapor barriers to reduce uncontrolled air leakage, making fluid-applied elastomeric membranes a preferred solution over mechanically fastened sheet systems. The 2024 International Energy Conservation Code now requires continuous air barriers across most climate zones, favoring liquid-applied membranes that can seal complex penetrations, transitions, and irregular substrates with fewer failure points.

- Technical analysis by the U.S. Department of Energy linked to ASHRAE 90.1-2022 indicates that buildings designed to meet these updated envelope requirements can achieve average site energy savings of 9.8 %, with whole-building air leakage testing becoming mandatory for many commercial structures under 25,000 square feet. This regulatory shift is materially increasing membrane specification rates in new construction and major retrofits.

- Manufacturers are aligning product portfolios accordingly. In June 2025, Polyglass U.S.A. highlighted its compliance with the FORTIFIED Roof program and the International Building Code, emphasizing self-adhered and fluid-applied membranes capable of withstanding temperatures up to 250°F and maintaining UV resistance for up to 60 days during construction sequencing. These performance benchmarks are now baseline expectations rather than premium features in high-performance envelopes.

Material Innovation for Class 4 Hail and Extreme Weather Resilience

- The sharp increase in hailstorms, heat waves, and freeze-thaw cycles is driving a material science pivot toward impact-resistant and elastomerically resilient membranes. Roofing and enclosure systems are increasingly specified to meet Class 4 impact resistance under UL 2218 and FM standards, as insurers seek to reduce catastrophic loss exposure.

- In July 2025, updated guidance from the International Institute of Building Enclosure reinforced stricter pass-fail criteria under FM protocols, requiring membranes to exhibit no cracking or splitting after high-energy impact testing. This has accelerated the adoption of thicker membranes, reinforced scrims, and advanced polymer blends that maintain elasticity under extreme thermal cycling.

- Insurers are reinforcing this trend through financial incentives. Buildings utilizing membranes compliant with ASTM D6083 or high-thickness TPO and EPDM systems are increasingly eligible for premium credits. Products such as EverGuard Extreme TPO from GAF are now tested for extended heat aging to preserve flexibility in high-solar-load environments. At the chemistry level, advanced 100% acrylic emulsions, including RHOPLEX EC-2020 from Dow, are enabling coatings that meet multiple ASTM performance classes while resisting dirt pick-up and brittle fracture during rapid temperature shifts.

Integration with Building-Integrated Photovoltaics and Green Roof Systems

- Urban decarbonization strategies are accelerating the adoption of building-integrated photovoltaics and vegetative roofing systems, creating demand for elastomeric membranes that function as both waterproofing and structural substrates. These applications require membranes capable of withstanding localized heat loads, constant moisture exposure, and biological activity over multi-decade service lives.

- In July 2025, Mitrex completed the SunRise Residential project in Canada, featuring a 30,000-square-foot solar mural integrated directly into the building envelope. Projects of this scale rely on elastomeric membranes beneath BIPV systems that can tolerate elevated surface temperatures without loss of adhesion or waterproofing integrity.

- Peer-reviewed research published in December 2025 demonstrated that combining green roofs with photovoltaic systems can improve solar efficiency by approximately 5% through evaporative cooling. This synergy depends on root-resistant elastomeric membranes such as TPO and PVC KEE that can maintain watertight performance for more than 25 years under continuous moisture and root pressure. Municipal cool-roof mandates in major U.S. cities are further accelerating demand for high-Solar Reflectivity Index elastomeric coatings, which can lower roof surface temperatures by up to 38°C and materially reduce cooling loads in solar-equipped buildings.

Rehabilitation of Water Infrastructure with Spray-Applied Polyurea Liners

- Aging municipal water and wastewater infrastructure represents one of the largest growth avenues for elastomeric membranes, particularly fast-curing spray-applied polyurea and polyurethane systems. Public funding under the American Relief Act and the EPA Clean Water State Revolving Fund is unlocking billions of dollars for rehabilitation projects, with federal estimates indicating over USD 630 billion in required investment over the next two decades.

- Spray-applied elastomeric liners are gaining preference due to their ability to restore concrete tanks, pipelines, and containment structures to service within hours rather than days. These systems form seamless, monolithic barriers that resist hydrogen sulfide gas, chemical abrasion, and microbial corrosion. Providers such as ArmorThane have expanded wastewater-specific product lines to address aggressive operating environments in sewer and treatment facilities.

- Regulatory momentum is also supporting potable water applications. The 2025 Drinking Water Infrastructure Needs Survey identified a growing requirement for NSF and ANSI 61 certified elastomeric linings, accelerating development of membranes that prevent leaching while delivering projected service lives of up to 50 years. This positions elastomeric membranes not only as construction materials, but as long-term asset protection solutions critical to public health and infrastructure resilience.

Elastomeric Membrane Market Share and Segmentation Insights

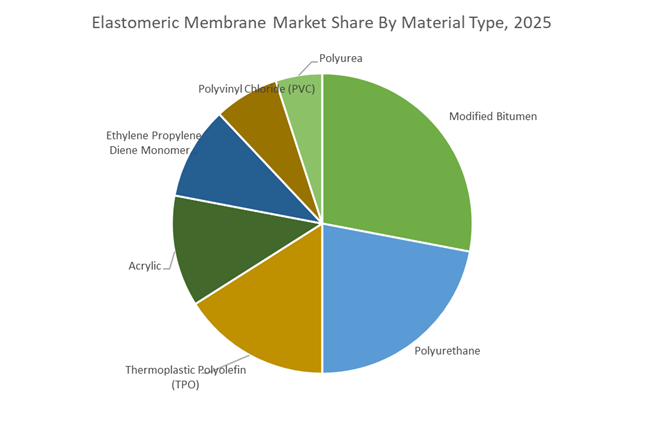

Modified Bitumen Leads Material Adoption as TPO and Polyurethane Accelerate in High-Performance Roofing

Modified bitumen accounts for 28% of elastomeric membrane market share in 2025, supported by its long-standing use in low-slope commercial roofing, proven durability, and cost efficiency across torch-down and cold-applied systems. Polyurethane dominates the liquid-applied membrane category, valued for seamless installation, high flexibility, and chemical resistance in terraces, balconies, and podium decks. Thermoplastic polyolefin (TPO) is the fastest-growing single-ply roofing material, driven by heat-weldable seams, reflective energy-saving surfaces, and recyclability in new commercial construction. Acrylic membranes maintain strong uptake in refurbishment and maintenance projects due to water-based formulations, UV stability, and ease of roller or brush application. EPDM remains a reliable synthetic rubber option with excellent weathering and low-temperature flexibility, while PVC gains traction in green roofs and industrial facilities for chemical and fire resistance. Polyurea occupies a premium niche for ultra-fast curing and extreme durability in infrastructure and containment applications.

Non-Residential Buildings Anchor Demand as Infrastructure Projects Drive High-Growth Installations

Non-residential construction represents 45% of global elastomeric membrane consumption in 2025, encompassing commercial offices, retail centers, warehouses, factories, and institutional buildings. These large, low-slope roof structures predominantly specify TPO, PVC, and modified bitumen membranes, with demand reinforced by energy-efficient roofing mandates and ongoing commercial development. Residential applications form a substantial secondary segment, covering roof underlayments, flashing, and waterproofing for balconies, terraces, and basements across single-family and multi-family housing. Renovation activity in aging housing stock continues to support acrylic coatings and liquid-applied polyurethane systems. Infrastructure and public works is the fastest-growing end-user category, spanning bridges, tunnels, dams, water treatment plants, and transport hubs. These projects increasingly deploy high-durability polyurethane and spray-applied polyurea membranes to withstand hydrostatic pressure, chemical exposure, and mechanical stress, ensuring long-term protection of critical public assets and accelerating market expansion.

Competitive Landscape of the Elastomeric Membrane Market

The Elastomeric Membrane Market in 2026 is shaped by aggressive consolidation, ESG-driven product innovation, and rising demand for TPO roofing membranes, liquid-applied waterproofing systems, and high-elasticity construction chemicals, with global leaders competing on PCF transparency, installation efficiency, and building-envelope integration.

ESG-driven roofing membranes and bio-based innovation leadership by Sika AG

Sika continues to define the high-performance elastomeric membrane landscape through deep R&D and unmatched global integration. In February 2026, Sika advanced its “Fast Forward” efficiency program to optimize manufacturing and accelerate digital transformation. The company generated CHF 11.2 billion in 2025 sales and expects to outperform the market by 3% to 6% in 2026, targeting 19.5% to 20.0% EBITDA margins. Its Sarnafil® and Sikaplan® systems now feature full Product Carbon Footprint (PCF) and LCA transparency for EU ESG compliance. Sika also launched bio-based liquid-applied membranes that retain elasticity down to −5°C, reinforcing leadership in MEA and emerging markets where localized production drives double-digit growth.

Commercial re-roofing dominance and installer-efficiency strategy at Carlisle Companies Inc.

Through Carlisle Construction Materials, Carlisle anchors North America’s elastomeric roofing market, especially in single-ply commercial re-roofing, a segment less volatile than new construction. For Q4 2025, CCM delivered approximately $827 million in revenue with a strong 26.8% adjusted EBITDA margin, while 2026 guidance targets margin expansion of 50 bps. Carlisle also launched a $1 billion share repurchase program in 2026, reflecting robust cash flow. Its “Carlisle Experience” emphasizes labor-reducing accessories and pre-fabricated exact-fit membranes, addressing skilled labor shortages. This installer-centric approach strengthens Carlisle’s position in TPO and EPDM roofing membranes across institutional and retail construction projects.

Integrated waterproofing platforms powered by acquisitions at Saint-Gobain

Saint-Gobain has transformed into a global leader in light and sustainable construction following its acquisition of Fosroc International, dramatically expanding elastomeric waterproofing capabilities across 70 countries. The group now delivers “all-six-sides” building protection by integrating GCP Applied Technologies and Chryso into unified envelope systems. Its Zero Damp Advance membranes offer warranties up to 12 years with enhanced seepage resistance. Under the Lead & Grow 2026–2030 plan, Saint-Gobain targets €12 billion in growth capex and M&A, aiming for construction chemicals sales above €9 billion by 2030. Emerging markets and North America now contribute 68% of operating income, underscoring its global membrane market momentum.

TPO roofing scale and cool-roof technology leadership from GAF Materials Corporation

GAF remains the benchmark supplier in TPO elastomeric membranes, driven by its EverGuard® portfolio and comprehensive “Total Roof” systems. In early 2026, GAF controlled an estimated 29.8% share of the global TPO roofing segment, significantly ahead of competitors. Its strategy centers on cool roofing membranes with ultra-high Solar Reflective Index (SRI) values to mitigate urban heat islands and reduce building cooling loads. GAF’s extensive Master Select contractor network ensures consistent installation quality, lowering warranty exposure while accelerating adoption in commercial and industrial projects. Scale, distribution reach, and reflective membrane innovation keep GAF at the forefront of energy-efficient roofing systems.

Self-healing bitumen membranes and circular construction by SOPREMA Group

SOPREMA combines elastomeric bitumen expertise with advanced liquid systems, generating over €4.84 billion in global turnover with operations in 90+ countries and 128 factories. Its ALSAN and DUOFLEX ranges stand out in 2026, with DUOFLEX delivering self-healing, monolithic waterproofing across a building’s lifespan. SOPREMA also expanded its SOPREMAPOOL reinforced membrane line for luxury pools and water containment. Unlike peers exiting bitumen, SOPREMA innovated with SBS-modified compounds that remain flexible at −30°C. A growing closed-loop recycling model now converts old membranes into raw material, strengthening SOPREMA’s position in circular construction and high-performance waterproofing.

United States: Code-Driven Envelope Upgrades and Low-VOC Reformulation

The United States elastomeric membrane market is being reshaped by building envelope modernization and regulatory tightening around chemical inputs. At the 2025 International Builders’ Show, Magnera Corporation under its TYPAR brand introduced Liquid Flashing, a gun-grade elastomeric membrane engineered for window openings and joint detailing. The product eliminates the need for primers while delivering high UV resistance and waterproofing performance, directly aligning with emerging U.S. building code requirements that emphasize continuous air and water barriers. This reflects a broader shift toward liquid-applied elastomeric membranes that simplify installation while improving long-term envelope integrity.

From a supply and compliance perspective, midstream volatility in the U.S. Gulf Coast prompted tiered price adjustments in Q2 2025, with Dow recalibrating polyolefin and acrylic feedstock pricing to reflect a 7.3% increase in logistics and raw material overheads. At the same time, the U.S. EPA’s 2026 TSCA roadmap is accelerating a structural transition away from solvent-heavy polyurethane systems toward low-VOC, aqueous-based elastomeric membranes, particularly in commercial reroofing. Sustainability is also moving from concept to execution. In April 2025, Dow and Saint-Gobain formalized a partnership to integrate REVOLOOP post-consumer recycled resins into building materials, cutting lifecycle emissions by an estimated 2.8 tons of CO2e per major product line. These dynamics, combined with Inflation Reduction Act incentives, drove record cool roof retrofit activity across high-heat urban zones in 2025.

India: Infrastructure-Led Scaling and Localization of Waterproofing Systems

India’s elastomeric membrane market is expanding rapidly on the back of infrastructure investment and localization policies. In April 2025, RENOLIT commenced construction of a new manufacturing facility in Pune, scheduled to be operational by April 2026. With a planned capacity of 6,000 tons annually, the plant is focused on high-performance geomembranes for civil engineering, landfill lining, and renewable energy storage applications. This investment underscores India’s emergence as a regional production hub rather than a purely import-dependent market.

Demand is being structurally reinforced by renewable energy integration and urban housing mandates. Government-backed Integrated Renewable Energy Storage Projects have created sustained demand for elastomeric geomembranes used in pumped hydro and solar storage installations, particularly across Gujarat and Andhra Pradesh. Under the Production Linked Incentive scheme for specialty chemicals, domestic players such as Pidilite Industries have scaled liquid-applied elastomeric membrane production, achieving an estimated 15.3% domestic supply share in the waterproofing segment by late 2025. Concurrently, programs like PMAY-Urban and the Smart Cities Mission have institutionalized the use of high-durability elastomeric coatings in wet-area waterproofing, accelerating adoption of TPO and EPDM sheet membranes in high-rise residential construction.

Saudi Arabia: Giga-Project Localization and Polymer Supply Security

Saudi Arabia’s elastomeric membrane market is tightly linked to Vision 2030 giga-project execution and supply chain localization. In 2025, Sika acquired Awazil Al Khaleej Industrial Co., also known as Gulf Seal, in Riyadh. This acquisition secures localized production of bituminous and elastomeric waterproofing membranes for mega-developments such as NEOM and the Red Sea Project, where performance guarantees, climate resilience, and supply reliability are critical procurement criteria.

On the upstream side, SABIC’s Nusaned initiative is catalyzing domestic production of high-molecular-weight polymers used in elastomeric membranes. This effort is projected to reduce reliance on imported European intermediates by roughly 12% for the 2026 cycle. The combined effect of localized manufacturing and polymer self-sufficiency is positioning Saudi Arabia as a strategically insulated market, capable of executing large-scale construction programs without exposure to global supply shocks.

China: Production Rationalization and Infrastructure Export Orientation

China’s elastomeric membrane market is undergoing strategic recalibration as the domestic real estate cycle cools and public infrastructure takes priority. In 2025, Sika announced structural adjustments in its China operations under its Fast Forward program, committing CHF 120–150 million toward digital acceleration and high-efficiency production of TPO membranes. The objective is to align capacity with infrastructure and public works demand while maintaining cost competitiveness amid softer residential construction activity.

Export momentum is increasingly important. Government data from Q3 2025 shows that Belt and Road Initiative projects across Southeast Asia and Africa have become the largest external destinations for Chinese-manufactured liquid-applied polyurea and thermoplastic membranes. These exports are supported by China’s scale manufacturing advantage and its ability to deliver specification-compliant membranes for transportation, water infrastructure, and energy projects under tight timelines.

Germany (European Union): Compliance-First Innovation and Energy Transition Integration

Germany’s elastomeric membrane market is defined by regulatory leadership and energy transition alignment. In preparation for the 2026 REACH recast, German manufacturers have redirected R&D toward solvent-free, moisture-curing elastomeric systems that comply with the EU’s Safe and Sustainable by Design framework. This shift is reshaping formulation chemistry across roofing, waterproofing, and façade membranes, with compliance increasingly treated as a baseline requirement rather than a differentiator.

Energy transition policies are also influencing product design. In 2025, Paul Bauder expanded its Green Roof membrane portfolio by integrating photovoltaic mounting systems directly into EPDM elastomeric sheets. This innovation enables commercial and industrial buildings to meet Germany’s 2026 Solar Mandate while maintaining long-term waterproofing integrity, positioning elastomeric membranes as multifunctional components within the built environment.

Elastomeric Membrane Market: Country-Level Strategic Summary

Elastomeric Membrane Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Key Material Focus

|

Strategic Market Direction

|

|

United States

|

Energy-efficient retrofits and TSCA compliance

|

Liquid-applied, low-VOC membranes

|

Envelope performance and recycled content

|

|

India

|

Infrastructure and renewable storage

|

Geomembranes, liquid-applied systems

|

Localization and capacity scaling

|

|

Saudi Arabia

|

Vision 2030 giga-projects

|

Bituminous and elastomeric sheets

|

Supply chain localization

|

|

China

|

Public infrastructure and BRI exports

|

TPO, polyurea membranes

|

Production efficiency and export orientation

|

|

Germany

|

REACH recast and solar mandates

|

Solvent-free EPDM systems

|

Compliance-led multifunctional design

|

Elastomeric Membrane Market Report Scope

Elastomeric Membrane Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$85.7 Billion

|

|

Market Size (2034)

|

$154.9 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Material Type (Thermoplastic Polyolefin, Ethylene Propylene Diene Monomer, Polyvinyl Chloride, Polyurethane, Acrylic, Modified Bitumen, Polyurea), By Type (Sheet-Based Membranes, Liquid-Applied Membranes), By Application (Roofing, Walls and Facades, Underground Construction, Wet Areas, Civil Engineering), By End-User Industry (Non-Residential, Residential, Infrastructure and Public Works)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Saint-Gobain S.A., Dow Inc., BASF SE, Carlisle Companies Incorporated, Soprema Group, Standard Industries Inc., Pidilite Industries Limited, Paul Bauder GmbH & Co. KG, Oriental Yuhong, Keshun Waterproof Technology Co., Ltd., Mapei S.p.A., Fosroc International Limited, Firestone Building Products, Johns Manville

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Elastomeric Membrane Market Segmentation

By Material Type

- Thermoplastic Polyolefin

- Ethylene Propylene Diene Monomer

- Polyvinyl Chloride

- Polyurethane

- Acrylic

- Modified Bitumen

- Polyurea

By Type

- Sheet-Based Membranes

- Liquid-Applied Membranes

By Application

- Roofing

- Walls and Facades

- Underground Construction

- Wet Areas

- Civil Engineering

By End-User Industry

- Non-Residential

- Residential

- Infrastructure and Public Works

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Elastomeric Membrane Industry

- Sika AG

- Saint-Gobain S.A.

- Dow Inc.

- BASF SE

- Carlisle Companies Incorporated

- Soprema Group

- Standard Industries Inc.

- Pidilite Industries Limited

- Paul Bauder GmbH & Co. KG

- Oriental Yuhong

- Keshun Waterproof Technology Co., Ltd.

- Mapei S.p.A.

- Fosroc International Limited

- Firestone Building Products

- Johns Manville

*- List not Exhaustive