Electronic Films Market Expansion Fueled by AI Electronics, Foldable Displays, and Advanced Optical Film Innovation

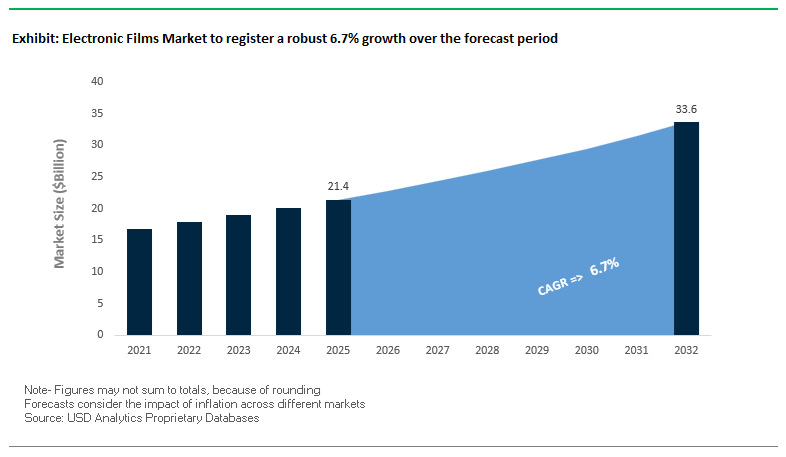

The global Electronic Films Market was valued at USD 21.4 billion in 2025 and is projected to grow at a CAGR of 6.7% between 2025 and 2032, reaching USD 33.7 billion by 2032. This growth is driven by the rapid proliferation of advanced electronics, electric vehicles (EVs), AI-driven computing infrastructure, and next-generation display technologies. Electronic films play a critical role in enabling optical clarity, electrical conductivity, thermal stability, and environmental protection across applications such as semiconductors, displays, batteries, and printed circuit boards (PCBs).

A key structural driver is the increasing demand for high-performance optical films in automotive and consumer electronics. The evolution toward large-format, curved, and interactive displays, particularly in EV dashboards and infotainment systems, is accelerating the adoption of polarizing films, anti-reflective coatings, and transparent conductive films (TCFs). Additionally, the rapid growth of foldable and rollable devices is creating demand for films that combine flexibility, scratch resistance, and long-term mechanical durability, pushing the boundaries of materials engineering.

Another major growth vector is the expansion of AI data centers and high-speed computing systems, which require advanced electronic films for signal integrity, heat management, and miniaturization. Films used in copper-clad laminates (CCLs) and semiconductor packaging are becoming increasingly sophisticated, with requirements for low dielectric loss, high thermal resistance, and contamination-free processing. Simultaneously, regulatory pressures are driving the transition toward PFAS-free and environmentally compliant materials, particularly in semiconductor manufacturing processes.

High-Temperature Films, Foldable Display Breakthroughs, and AI-Driven Thin-Film Manufacturing Reshape Market Dynamics

The electronic films market is undergoing rapid transformation driven by material innovation, display technology evolution, and strategic supply chain expansion. In January 2026, Toray Industries introduced the world’s first 160°C heat-resistant polypropylene release film, addressing a critical bottleneck in semiconductor packaging and composite processing. This innovation enables faster processing speeds and reduces contamination risks, particularly in IC substrate manufacturing and carbon fiber-reinforced materials.

Automotive electronics and display applications are emerging as major growth engines. In May 2025, Nitto Denko Corporation reported record financial performance driven by demand for large-format optical films and battery bonding tapes. The shift toward wide, curved EV dashboards is significantly increasing the need for advanced polarization and anti-reflective films. Complementing this trend, in March 2025, Toray Industries launched nano-multilayer HUD films, solving visibility issues for drivers wearing polarized sunglasses by optimizing light phase control—an important safety advancement in automotive display systems.

The transition toward next-generation consumer electronics is also accelerating innovation. In February 2026, 3M introduced advanced optical films for foldable devices, capable of withstanding over 200,000 fold cycles without delamination or crease formation. This development directly addresses durability challenges in foldable smartphones and tablets, a key barrier to mainstream adoption. At the same time, Sumitomo Chemical restructured its LCD polarizing film business in December 2024, reallocating resources toward OLED and next-generation display technologies, reflecting a broader industry shift away from traditional LCD dominance.

Advanced manufacturing technologies and supply chain integration are further shaping the market. In October 2025, Applied Materials launched the Centura EB-PVD Pro system, enabling high-precision deposition of transparent conductive films with ±2% thickness uniformity, critical for wearable and touch-sensitive devices. Meanwhile, in February 2026, Formosa Plastics Group (via Nanya Technology) expanded into specialty electronic film chemicals for AI-driven PCBs, targeting high-speed data transmission in next-generation data centers.

Sustainability and regulatory compliance are increasingly central to product development. In May 2024, Toray Industries commercialized a PFAS-free mold release film, enabling semiconductor manufacturers to meet environmental standards without compromising yield. Additionally, Covestro strengthened its supply chain for aliphatic isocyanates in January 2026, ensuring stable raw material availability for high-performance polyurethane protective films used in autonomous vehicle sensors.

EU RoHS and Ecodesign Regulations Driving Halogen-Free Electronic Films and Flame Retardant Innovation

The regulatory landscape in Europe is reshaping the material composition of electronic films, with the combined influence of RoHS directives and the Ecodesign for Sustainable Products Regulation targeting the elimination of halogenated flame retardants in polymer-based substrates. By 2026, compliance with halogen-free standards defined under IEC 61249-2-21 has become a baseline requirement for leading OEMs, limiting chlorine and bromine content to 900 ppm each and total halogen concentration to 1,500 ppm. This shift is primarily driven by end-of-life recyclability considerations, as halogenated compounds complicate material recovery and increase environmental toxicity during disposal. Concurrent regulatory refinements under Directive (EU) 2024/232 are also forcing manufacturers to reassess recycled PVC streams, particularly for legacy lead and cadmium stabilizers that could compromise compliance. The tightening of toxicity thresholds extends to electronic glass and ceramic films, where a mandated 30% reduction in lead-based thick-film paste usage compared to 2020 levels is influencing formulation strategies in high-precision electronic components. As a result, phosphorus-based non-halogenated flame retardants are gaining traction, provided they meet stringent UL 94 V-0 fire resistance standards while maintaining low dielectric constants below 3.5 for high-frequency electronics. These regulatory pressures are accelerating innovation in sustainable, high-performance electronic film materials while redefining supplier qualification criteria across European electronics value chains.

China GB/T 41646 Standard Establishing Aerospace-Grade Outgassing Benchmarks for Electronic Films

China’s GB/T 41646 standard, supported by critical updates implemented in 2024, is establishing a rigorous performance framework for electronic films used in aerospace and satellite applications. The standard focuses on minimizing outgassing in vacuum environments, a critical requirement for preventing molecular contamination of sensitive optical and electronic components in low-earth orbit. By 2026, electronic films must meet strict Total Mass Loss thresholds of 1.0% or lower and Collected Volatile Condensable Material limits of 0.10% or less under high-temperature vacuum testing conditions. The inclusion of Water Vapor Recovery metrics ensures that films return to near-original mass levels following testing, reducing the risk of moisture-induced structural failures such as delamination in orbital environments. The technical alignment of GB/T 41646 with ASTM E595 has enhanced global interoperability, enabling Chinese manufacturers to supply materials for international satellite programs with standardized outgassing certification data. Manufacturing processes are also evolving to meet these stringent requirements, with advanced cleanroom coating facilities achieving ISO Class 5 standards to ensure contamination-free film surfaces for high-resolution imaging systems. These developments are elevating the performance expectations for aerospace-grade electronic films and strengthening China’s position in the global space materials supply chain.

Ultra-Thin Polyimide Films Enabling Foldable OLED Display Innovation

The rapid commercialization of foldable OLED devices is creating a high-growth opportunity for ultra-thin polyimide films engineered for extreme flexibility, optical clarity, and thermal stability. These films serve as critical structural and protective layers in next-generation displays, particularly in the form of colorless polyimide cover plates that replace traditional glass substrates. By 2026, ultra-thin polyimide films with thicknesses of 25 micrometers or less are achieving dynamic bending radii below 1.0 millimeter, with the ability to withstand more than 200,000 folding cycles without visible deformation or electrical performance degradation. To balance flexibility with durability, manufacturers are applying ultra-thin high-hardness coatings of approximately 5 micrometers, achieving scratch resistance levels equivalent to 3H to 5H pencil hardness while retaining polymer toughness. Thermal performance is another critical parameter, with these films engineered to exhibit glass transition temperatures exceeding 450 degrees Celsius, enabling compatibility with low-temperature polysilicon processing used in high-refresh-rate OLED panels. Additionally, precise control of the coefficient of thermal expansion to values below 10 ppm per degree Celsius ensures dimensional stability and prevents delamination within multi-layer display architectures. These advancements are positioning ultra-thin polyimide films as a foundational material in the evolution of flexible and foldable consumer electronics.

High-Conductivity Graphite Films Advancing Thermal Management in 5G Electronic Devices

The proliferation of 5G-enabled devices is driving a surge in demand for advanced thermal management materials, with synthetic graphite films emerging as a critical solution for dissipating high power densities in compact electronic systems. These films are produced through the graphitization of high-purity polyimide precursors, resulting in materials with exceptional in-plane thermal conductivity ranging from 1,300 to 1,800 watts per meter-kelvin, significantly outperforming conventional metals such as copper while maintaining lower weight and thickness. The anisotropic nature of graphite films enables efficient lateral heat spreading across device surfaces, preventing localized hotspots that can degrade performance and reliability. Recent advancements have also improved through-plane thermal conductivity to levels exceeding 10 watts per meter-kelvin, facilitating faster heat transfer from critical components such as processors to external heat dissipation layers. The market opportunity is particularly strong for ultra-thin graphite films in the 12 to 25 micrometer range, which are optimized for integration into space-constrained smartphone architectures. Enhanced graphitization techniques are achieving anisotropy ratios greater than 100:1, ensuring directional heat flow control and protecting temperature-sensitive components such as batteries and camera modules. These performance characteristics are making graphite films indispensable in the design of next-generation 5G electronics, where thermal management is a key determinant of device performance and longevity.

Optical Films Dominate Electronic Films Market with 41% Share Driven by Display Technology Demand

Function Analysis: Optical Enhancement Films Lead with LCD, OLED, and Mini-LED Integration

Optical films account for a leading 41.0% share of the electronic films market in 2025, driven by their critical role in flat panel display performance across TVs, smartphones, laptops, and automotive displays. These films—including brightness enhancement films (BEF), diffuser films, reflective polarizers, micro-lens array (MLA) films, and anti-reflective (AR) coatings—are essential components in display backlight units, optimizing light transmission, brightness uniformity, viewing angles, and energy efficiency. A key growth driver is the transition to Mini-LED and advanced display technologies, which require high-precision optical films to manage thousands of micro light sources and eliminate hot spots. Additionally, the rise of automotive displays—featuring curved, high-resolution screens—demands optical films with superior thermal stability (-40°C to +95°C), UV resistance, and glare reduction, creating a premium segment within the market. These factors firmly establish optical films as the backbone of the global electronic films market.

Consumer Electronics Segment Leads Electronic Films Market with 52% Share Driven by High Device Volumes and Innovation in Display Technologies

End-Use Sector Analysis: Smartphones, TVs, and Foldable Devices Drive Market Expansion

The consumer electronics segment dominates the electronic films market with a 52.0% share in 2025, fueled by the massive global production of smartphones, tablets, televisions, and laptops. Each device integrates multiple functional films, including optical films, touch sensor films, protective layers, and thermal management films, making electronic films indispensable to modern electronics manufacturing. With approximately 1.2 billion smartphones shipped annually, volume demand remains exceptionally high. A major innovation driver is the emergence of foldable and rollable displays, which require specialized films such as ultra-thin glass (UTG) laminated with flexible polymer layers and ultra-durable optical films capable of withstanding repeated bending cycles. These advanced materials command 5x–10x price premiums, significantly boosting market value. Additionally, ongoing advancements in smart devices and display technologies continue to drive demand, positioning consumer electronics as the primary growth engine in the global electronic films market.

Electronic Films Market Competitive Landscape Driven by OLED Materials, Optical Films, and High-Performance Polymer Substrates

The electronic films market is highly competitive, driven by demand for OLED materials, optical films, EMI shielding, and thermal management solutions across consumer electronics, EVs, and data centers. Key players compete through advanced polymer films, vertical integration, and innovation in flexible, high-performance substrates.

Toray Strengthens Electronic Films Leadership with OLED Materials and MLCC Demand Surge

Toray Industries, Inc. is reinforcing its leadership in electronic films through strong performance in MLCC release films and advanced OLED materials targeting foldable devices. Its Darwin Project has improved profitability, contributing ¥3 billion in incremental gains in FY2025/26. The company is expanding in data center and consumer electronics applications despite temporary softness in battery separator films. Toray’s expertise in PET and polyimide films ensures high thermal resistance and durability for next-generation electronics. Strategic pricing initiatives are expected to deliver ¥10 billion in annual profit impact by 2026. Its focus on high-growth segments like flexible displays strengthens its competitive positioning.

3M Drives Electronic Film Innovation with AI Simulation and Advanced Display Materials

3M Company is redefining electronic film innovation through AI-powered simulation tools launched at CES 2026, enabling faster product development cycles. The company dominates display materials with films that enhance brightness, contrast, and energy efficiency in large and foldable screens. It is transitioning to a co-innovation model, particularly in automotive electronics and smart cockpit displays. 3M’s portfolio includes EMI shielding and thermal management films essential for 5G infrastructure and AI data centers. Its solutions support high-speed electronics reliability and miniaturization. The company’s integration of digital tools and advanced materials reinforces its leadership in electronic films.

DuPont Advances High-Durability Electronic Films with Renewable Manufacturing and Tedlar® Innovation

DuPont de Nemours, Inc. is strengthening its electronic films portfolio through sustainability and advanced material innovation. Its Tedlar® film production is now powered by 100% renewable electricity, aligning with net-zero goals. The company’s FilmTec™ Fortilife™ and Tedlar® films are widely used in extreme environments, offering unmatched durability. DuPont’s innovation was recognized with multiple Edison Awards in 2026. The divestiture of its Aramids business allows a sharper focus on high-margin electronic materials. Its expansion into applications like COASTALUME™ roofing highlights cross-industry adoption of advanced film technologies.

Nitto Denko Leads Optical Film Market with Thin-Film Polarizers and EV Adhesive Solutions

Nitto Denko Corporation maintains a dominant position in optical films, particularly polarizers used in high-end displays. Its patented thin-film polarizer technology enables ultra-slim devices such as tablets and laptops. The company is benefiting from recovery in smartphone production and increased demand for automotive sensor films. Nitto is investing in bio-based polyimide materials for flexible printed circuits, supporting sustainability in electronics. Its adhesive-functional films combine bonding and insulation for EV battery modules. The company’s Global Niche Top strategy ensures leadership in specialized electronic film applications.

Sumitomo Chemical Expands OLED and Photoresist Film Portfolio with Strong ICT Growth

Sumitomo Chemical Co., Ltd. is experiencing strong growth in its ICT and Mobility Solutions segment, with core operating income rising significantly in FY2025/26. The company is capitalizing on the shift toward OLED displays in tablets and notebooks. Its restructuring program is improving profitability across petrochemical-linked film assets. Sumitomo’s vertical integration provides cost advantages in producing polarizing films and touchscreen substrates. The company is also expanding its high-value photoresist materials for semiconductor and display applications. Its focus on advanced electronic materials strengthens its global competitiveness.

Toyobo Targets Circular Electronics with Biopolymer Films and Advanced Display Solutions

Toyobo Co., Ltd. is positioning itself in the electronic films market through advanced functional materials and sustainable innovation. Its COSMOSHINE SRF™ film is critical for high-end LCDs, eliminating rainbow effects in automotive and outdoor displays. The company is prioritizing biopolymer-based films to support circular electronics and reduce environmental impact. Toyobo is expanding into life sciences, leveraging film-based separation technologies such as exosome recovery systems. Its upcoming 2030 roadmap emphasizes high-value functional materials over commodity fibers. The company’s focus on biodegradable substrates aligns with emerging sustainability trends in electronics.

India Electronic Films Market: Component Ecosystem Expansion Driving Localization

India is rapidly emerging as a key hub for electronic films, supported by strong government incentives and supply chain localization. The expansion of the Electronics Components Manufacturing Scheme (ECMS) to ₹40,000 crore (~$4.8 billion) is accelerating domestic production of display films, dielectric layers, and PCB materials.

Strategic initiatives are reshaping the market. Under India Semiconductor Mission (ISM) 2.0, the focus has shifted toward materials and chemicals, driving local production of high-purity photoresist and dielectric films. The surge in smartphone exports ($12 billion in H1 FY2025–26) is boosting demand for EMI shielding films and protective layers, while new industrial clusters (₹41,863 crore investment across 22 projects) are strengthening manufacturing infrastructure. Additionally, R&D into flexible electronics and NFC-enabled films is expanding applications in smart packaging and logistics, positioning India as a fast-growing electronics materials hub.

South Korea Electronic Films Market: Foldable Displays and Optical Innovation Driving Leadership

South Korea remains the global leader in advanced display films, particularly for foldable and high-brightness applications. Companies like Samsung and LG are scaling production of polyimide (PI) and colorless polyimide (CPI) films with enhanced thermal stability for next-generation OLED devices.

Innovation is focused on optics and performance. Developments include high-refractive-index (HRI) films for AR/VR devices and advanced optical layers for large-format LED displays. The government’s K-Belt Semiconductor Strategy is supporting domestic production of EUV pellicle films, while investments in PPS films for EV motor insulation are expanding applications into electric mobility. These advancements reinforce South Korea’s leadership in high-performance electronic films.

United States Electronic Films Market: Defense-Grade Materials and Energy Transition Driving High-Value Growth

The United States market is focused on high-reliability and advanced functional films, particularly for defense, semiconductors, and EVs. Under CHIPS Act Phase 2, funding is prioritizing advanced packaging materials, driving demand for ABF-equivalent films and redistribution layer (RDL) materials.

Innovation is also expanding into energy and healthcare. The launch of traction-grade polypropylene film capacitors (up to 3,800VDC) is supporting EV power systems, while radiative cooling films (TARC) are being deployed in 5G infrastructure for passive thermal management. Defense programs are funding nanocomposite dielectric films for high-energy systems, and the rise of wearable health devices is increasing demand for biocompatible sensor films. Additionally, nearshoring efforts are expanding domestic cleanroom film production capacity.

China Electronic Films Market: Rare-Earth Dominance and Battery Innovation Driving Scale

China dominates the global electronic films market through control of raw materials and large-scale production. The country leads in graphene-enhanced conductive films and ceramic-coated battery separator films, critical for EV and electronics applications.

Policy mandates are accelerating growth. The government requires low-loss LCP films for 5G infrastructure, while China produces over 85% of global photovoltaic backsheet films, increasingly shifting toward recyclable variants. Innovations such as graphene-silver nanowire hybrid films are replacing traditional ITO coatings, reducing costs. Additionally, regulatory pressure is phasing out solvent-based coating lines in favor of UV/EB-curable systems, reinforcing China’s leadership in both scale and sustainability.

Japan Electronic Films Market: Ultra-Precision Materials and Semiconductor Integration Driving Excellence

Japan is a global leader in high-purity electronic films and precision materials, particularly for semiconductors and advanced electronics. The development of sub-500 nm release films is enabling high-capacitance MLCC production for AI servers and 5G devices.

Innovation is focused on advanced applications. Japan is leading in flexible semiconductor films (FlexIC) for RFID and smart packaging, as well as electrochromic smart window films that reduce cooling loads by ~20%. The country also dominates supply of ultra-high-purity zirconia feedstocks, critical for advanced deposition processes. Additionally, the shift toward bio-based PEN films is supporting sustainability goals, reinforcing Japan’s leadership in precision and eco-friendly materials.

Germany Electronic Films Market: Hydrogen Economy and Smart Infrastructure Driving Innovation

Germany is focusing on high-performance electronic films for energy and industrial applications, particularly under its energy transition initiatives. The development of proton exchange membrane (PEM) films is critical for hydrogen fuel cell systems, especially in heavy-duty transport.

Regulatory frameworks are shaping innovation. The EU Data Act (2026) is driving adoption of RFID-enabled films for lifecycle tracking, while new circular economy mandates require 30% recycled content in non-functional films. Applications are expanding into smart building facades, where transparent conductive films support integrated photovoltaics and thermal management. Additionally, demand for anti-reflective and anti-fingerprint films in automotive displays and high-temperature BOPP films for wind energy converters highlights Germany’s role in advanced industrial applications.

Electronic Films Market Report Scope

Electronic Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.4 Billion

|

|

Market Size (2032)

|

$33.7 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Type (Conductive Films, Transparent Conductive Films, Opaque Conductive Films, Non-Conductive, Semiconductive Films), By Thickness (Ultra-thin Films, Thin Films, Thick Films), By Function (Optical Films, Protective Films, Heat Management, Sensing and Touch Panel Films, Decorative and Aesthetic Films), By Application (Electronic Displays, Printed Circuit Boards, Semiconductors, Energy Storage and Generation, Automotive Electronics, Wires and Cables), By End-Use Sector (Consumer Electronics, Automotive, Healthcare, Industrial and Smart Buildings, Aerospace and Defense)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, DuPont de Nemours, Inc., Toray Industries, Inc., Nitto Denko Corporation, LG Chem Ltd., Samsung SDI Co., Ltd., Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, Fujifilm Holdings Corporation, Merck KGaA, Eastman Chemical Company, Saint-Gobain, Gunze Ltd., Toyobo Co., Ltd., SKC Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electronic Films Market Segmentation

By Type

- Conductive Films

- Transparent Conductive Films

- Opaque Conductive Films

- Non-Conductive

- Semiconductive Films

By Thickness

- Ultra-thin Films

- Thin Films

- Thick Films

By Function

- Optical Films

- Protective Films

- Heat Management

- Sensing and Touch Panel Films

- Decorative and Aesthetic Films

By Application

- Electronic Displays

- Printed Circuit Boards

- Semiconductors

- Energy Storage and Generation

- Automotive Electronics

- Wires and Cables

By End-Use Sector

- Consumer Electronics

- Automotive

- Healthcare

- Industrial and Smart Buildings

- Aerospace and Defense

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Electronic Films Market

- 3M Company

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Nitto Denko Corporation

- LG Chem Ltd.

- Samsung SDI Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Fujifilm Holdings Corporation

- Merck KGaA

- Eastman Chemical Company

- Saint-Gobain

- Gunze Ltd.

- Toyobo Co., Ltd.

- SKC Co., Ltd.

*- List not Exhaustive