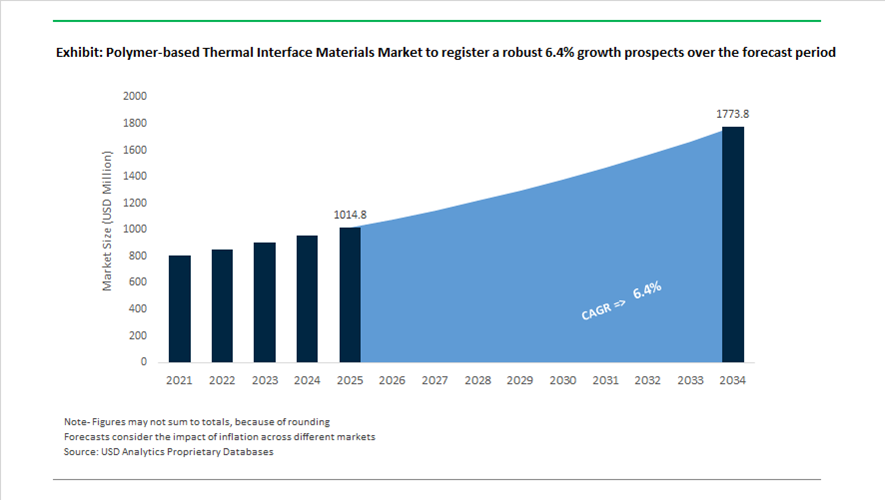

Polymer-Based Thermal Interface Materials Market Size 2025–2034: $1,014.8 Million to $1,773.6 Million at 6.4% CAGR Driven by EV Battery Cooling, AI Hardware, and High-Density Electronics

The global polymer-based thermal interface materials (TIM) market is projected to grow from $1,014.8 million in 2025 to $1,773.6 million by 2034, registering a CAGR of 6.4%. Demand is accelerating across electric vehicle (EV) battery packs, AI servers, telecom infrastructure, medical electronics, and miniaturized consumer devices. Polymer-based TIMs—including silicone gap pads, dispensable gels, thermally conductive epoxies, cure-in-place (CIP) materials, and phase change compounds—are essential for transferring heat between semiconductors and heat sinks while maintaining electrical insulation and mechanical compliance. As chip power densities increase and battery fast-charging becomes standard, advanced polymer matrices with higher thermal conductivity and lower pump-out risk are gaining adoption.

Hybrid material innovation is reshaping performance benchmarks. In October 2024, Dow partnered with Carbice to commercialize CNT-silicone thermal interfaces combining Dow’s silicone chemistry with Carbice’s aligned carbon nanotube technology. Products such as Carbice® SA-90 deliver enhanced thermal stability, reworkability, and mechanical resilience for semiconductors and EV power modules. Similarly, in December 2025, Indium Corporation highlighted its Heat-Spring® metal-polymer hybrid interfaces designed to prevent pump-out and bake-out failures in high-heat AI processing systems—an increasingly critical reliability requirement in data center hardware.

EV battery assemblies remain a core growth engine. In May 2025, Henkel expanded its CoolTherm portfolio with TC-850 adhesive, engineered to provide both structural bonding and effective thermal dissipation for fast-charging battery modules. In October 2025, Dymax introduced TPO-free adhesives and conformal coatings tailored for EV battery packs and PCB assemblies, aligning with evolving regulatory standards around photoinitiators. These developments reflect the convergence of thermal management, mechanical stability, and regulatory compliance in battery system design.

High-density electronics and automation are driving product diversification. Throughout 2025, Parker Hannifin’s Chomerics division expanded its TIM catalogue, introducing ultra-low hardness gap filler pads capable of conforming to irregular surfaces without damaging sensitive components. The company also released dispensable gels with vertical tackiness to prevent slumping in inverted assemblies, as well as two-component cure-in-place systems optimized for automated mixing and robotic dispensing. These innovations reduce assembly variability and improve throughput in telecommunications and medical device manufacturing.

Miniaturization is increasing reliance on thermally conductive epoxies and flowable materials. In January 2025, Master Bond launched EP53TC, a specialty filler-loaded epoxy designed for small potting and bonding applications where traditional pads cannot fit. Such materials are critical for compact sensor modules and wearable electronics. In November 2025, Dymax showcased its 2000-MW series light-curing adhesives for medical wearables, formulated without IBOA to ensure biocompatibility while managing localized heat dissipation.

The phase change material (PCM) segment is also evolving. In August 2025, PCMwala introduced IP05, an inorganic PCM for +5°C applications in cold-chain logistics, signaling broader movement toward thermally stable, non-paraffin formulations that compete with traditional organic PCMs.

Technology-Led Trends and High-Impact Opportunities in the Polymer-Based Thermal Interface Materials (TIMs) Market

Strategic Shift Toward High-Performance, Filler-Optimized Liquid TIMs

The polymer-based Thermal Interface Materials market is undergoing a decisive transition toward liquid-form TIMs as thermal densities in advanced electronics continue to escalate. In AI accelerators, high-performance CPUs, GPUs, and optical transceivers, localized heat flux has already crossed 100 W/cm², with near-junction hotspots in advanced packaging architectures exceeding 1 kW/cm². Under these conditions, traditional gap pads and elastomeric sheets introduce unacceptable contact resistance due to their inherent thickness and limited surface conformity.

Liquid TIMs such as thermal pastes and gels are increasingly preferred because they enable ultra-thin Bond Line Thickness while achieving exceptionally high filler loadings using boron nitride, aluminum oxide, or hybrid ceramic systems. By late 2025, leading formulations consistently exceeded 80–85% filler content by weight, allowing thermal conductivities to move well beyond the historical 6–8 W/m-K ceiling associated with legacy polymer TIMs.

A key inflection point occurred in October 2025 when Henkel commercialized Loctite TCF 14001, a silicone-based liquid TIM designed for 800G and emerging 1.6T optical transceivers used in AI data centers. With a measured thermal conductivity of 14.5 W/m-K, this product effectively doubled the performance of conventional high-end liquid TIMs, directly addressing the cooling bottlenecks in next-generation photonics and co-packaged optics. Importantly, this performance gain was achieved without sacrificing dispensability or long-term reliability.

Durability has become as critical as conductivity. Repeated thermal cycling in hyperscale servers and telecom infrastructure often causes pump-out failure, where TIM material is gradually displaced from the interface. Recent advances in polymer-filler matrix engineering have introduced thixotropic and self-healing rheological behavior, allowing liquid TIMs to retain interfacial coverage for more than 100,000 operating hours. This shift has transformed liquid TIMs from high-performance but maintenance-sensitive solutions into viable long-life materials for mission-critical electronics.

Vertical Integration and Automotive-Grade Qualification for EV Power Electronics

In parallel with data center demand, the electrification of mobility is reshaping requirements for polymer-based TIM suppliers. In electric vehicles, TIMs are no longer commodity consumables but safety-critical materials embedded within battery packs, inverters, onboard chargers, and power control units. This shift has driven the adoption of formal automotive qualification frameworks, most notably AQG 324, which is derived from the German LV 324 standard for power electronics.

AQG 324 qualification requires TIMs to demonstrate stable thermal resistance during both short-cycle and long-cycle power cycling tests, replicating the extreme mechanical and thermal fatigue experienced over a vehicle lifetime. Materials must withstand thousands of power-on and power-off events while maintaining consistent heat transfer in environments where continuous operating temperatures routinely exceed 120°C. By 2025, compliance with AQG 324 had become a prerequisite for TIM inclusion in high-volume EV programs rather than a differentiating feature.

To meet these requirements, suppliers such as DuPont and Dow are investing in vertically integrated development programs aligned with hybrid, electric, and autonomous vehicle platforms. Their focus has shifted toward low-density polymer systems that reduce overall vehicle mass while maintaining dielectric strengths above 10 kV/mm, a critical safety threshold in high-voltage battery and inverter assemblies. This combination of thermal conductivity, electrical insulation, and mechanical robustness is redefining the competitive landscape for automotive TIMs.

Phase-Change Materials for 2.5D and 3D Heterogeneous Integration

The rapid adoption of chiplet architectures, 2.5D interposers, and 3D-stacked integrated circuits has introduced complex, non-planar thermal pathways that conventional TIMs struggle to manage. This has opened a high-value opportunity for polymer-based Phase-Change Materials that remain solid at room temperature for ease of handling but transition into a low-viscosity state at operating temperatures.

In August 2025, research presented at the IMAPS conference demonstrated that PCM-graphite composite TIMs can act as transient thermal buffers in 3D ICs. By exploiting latent heat of fusion, these materials absorb short-duration power spikes and maintain near-isothermal conditions during peak workloads, significantly reducing thermal stress on sensitive junctions. This capability is particularly valuable for AI accelerators and high-bandwidth memory stacks, where burst power loads are common.

From a manufacturing perspective, reflowable polymer TIMs are gaining traction in System-on-Package designs. These materials can be pre-applied as dry films or printed layers and then activated during final assembly, reducing takt time and improving yield consistency. For high-density semiconductor packaging lines, this combination of thermal performance and process efficiency represents a compelling replacement for traditional greases.

Thermally Conductive Adhesives for Cell-to-Pack and Structural Battery Designs

One of the most structurally disruptive opportunities for polymer-based TIMs lies in their evolution into load-bearing materials within EV battery architectures. As OEMs adopt Cell-to-Pack and Cell-to-Chassis designs to eliminate intermediate module housings, thermally conductive adhesives are replacing mechanical fasteners and standalone TIM layers.

According to U.S. Department of Energy and industry assessments published through 2024–2025, structural TCAs such as BETAMATE and BETAFORCE TC systems can reduce overall battery pack weight by eliminating screws, brackets, and gaskets. At the same time, these adhesives provide uniform thermal pathways across thousands of cells, improving temperature homogeneity and extending battery life.

Safety considerations further amplify this opportunity. In late 2025, suppliers including 3M and Henkel emphasized the rapid uptake of flame-retardant thermally conductive adhesives that combine thermal conductivities in the 3–5 W/m-K range with intrinsic resistance to flame spread. These materials act as thermal barriers that slow or prevent heat propagation between failing cells, a critical factor in meeting stringent global EV safety standards and achieving top-tier crash and fire ratings.

Polymer Based Thermal Interface Materials Market Share and Segmentation Insights

Silicone-Based Thermal Interface Materials Lead Thermal Management Solutions in Electronics and Automotive Systems

Silicone-based thermal interface materials accounted for 48.60% of the Polymer Based Thermal Interface Materials Market by material type in 2025, reflecting their widespread use in electronic cooling applications. Silicone-based TIM formulations provide high thermal conductivity, mechanical compliance, and long-term reliability across wide temperature ranges, making them suitable for consumer electronics, automotive electronics, and telecommunications equipment. Their flexible structure accommodates thermal expansion mismatches between heat sources and heat sinks, ensuring stable thermal performance during device operation. In 2025, development of low-bleed silicone thermal interface materials is addressing contamination concerns in miniaturized electronics by preventing oil migration while maintaining efficient heat transfer performance in densely integrated electronic systems.

Consumer Electronics Sector Drives Thermal Interface Material Demand in Compact Device Cooling

Consumer electronics represented 42.80% of the Polymer Based Thermal Interface Materials Market by application in 2025, reflecting the high thermal management requirements of modern electronic devices. Smartphones, tablets, laptops, gaming consoles, and wearable electronics generate significant heat within compact enclosures, requiring effective heat dissipation solutions to maintain device performance and reliability. Thermal interface materials improve heat transfer between processors, power components, and heat sinks used in electronic assemblies. In 2025, increasing demand for ultra-thin thermal interface solutions for slim electronic devices is driving development of high-conductivity thermal gels, thin gap filler pads, and graphite-polymer composite materials designed to deliver efficient heat dissipation in sub-0.5 millimeter interface gaps.

Polymer-Based Thermal Interface Materials Market Competitive Landscape

The global polymer-based thermal interface materials (TIM) market is advancing toward high-conductivity (>10 W/m·K) gels, phase change materials, and automation-ready formulations. Competition is defined by AI data center cooling, EV battery thermal management, and the balance between thermal performance and manufacturability.

Henkel Leads High-Conductivity TIM Innovation for AI Infrastructure and EV Battery Systems

Henkel AG & Co. KGaA, through its Bergquist portfolio, dominates liquid gap fillers and high-performance TIM solutions. The Loctite TCF 1000 targets AI data centers and optical transceivers with optimized thermal dissipation for high-density networking hardware. Loctite TCF 14001 delivers 14.5 W/m·K conductivity, positioning it among the highest-performing silicone-based TIMs for GPUs. The Loctite TLB 9300 APSi adhesive integrates bonding and thermal management for EV battery cell-to-pack designs. Form-in-place elastomers support robotic dispensing and eliminate pump-out risks in sensitive semiconductor assemblies. Strategy focuses on high conductivity, automation compatibility, and AI-driven thermal management.

Dow Expands Silicone-Based Thermal Ecosystems with Integrated Cooling Solutions for HPC and Data Centers

Dow Inc. is strengthening its position through advanced silicone TIMs and integrated cooling platforms. The Dow Cooling Science Studio in Shanghai supports co-development of next-generation thermal gels and immersion cooling technologies. The DOWSIL™ TC Series, including TC-3080 and TC-5888, addresses high thermal design power requirements in AI servers and HPC systems. Integration with DOWSIL™ immersion cooling fluids and DOWFROST™ LC enables hybrid cooling architectures for hyperscale data centers. Participation in Data Centre World 2025 highlights its focus on direct-to-chip cooling solutions. Strategy emphasizes ecosystem integration, silicone chemistry expertise, and energy-efficient thermal management.

Parker Chomerics Delivers Multi-Functional TIMs with High Conductivity and EMI Shielding Capabilities

Parker Hannifin’s Chomerics division leads in multifunctional TIMs combining thermal management with EMI shielding. The THERM-A-GAP GEL 120 offers 12.0 W/m·K conductivity, supporting high-performance electronics manufacturing. CHO-THERM HV provides high dielectric strength for EV battery packs and energy storage systems. The CHO-AIR® AFT Chassis Seal aligns with ANSI/VITA 48.5-2026 standards for embedded computing thermal management. THERM-A-GAP PAD 80 delivers 8.3 W/m·K conductivity with low compression force for telecom and 5G applications. Strategy focuses on multifunctionality, high conductivity, and reliability in harsh environments.

Solstice Advanced Materials Strengthens PCM Leadership for Semiconductor and Data Center Applications

Solstice Advanced Materials operates as a pure-play specialty materials company following its 2025 spin-off. The company holds over 5,700 patents and focuses on phase change materials (PCMs) for semiconductor and server cooling. PCMs provide solid-state handling with liquid-phase thermal performance, enabling ultra-thin bond lines and improved heat transfer. These materials are widely used in semiconductor burn-in testing due to their thermal cycling stability. The company is developing remanufacture-friendly TIMs to support reworkability in high-value electronics. Strategy centers on PCM innovation, semiconductor reliability, and sustainable thermal solutions.

Shin-Etsu Strengthens Silicone TIM Portfolio with Vertical Integration and Automotive Electronics Focus

Shin-Etsu Chemical Co., Ltd. leverages full vertical integration in silicone chemistry to deliver high-purity thermal interface materials. The company is expanding ultra-soft thermal pads designed for complex geometries in automotive ECUs and ADAS systems. Sustainability initiatives target carbon neutrality by 2050 while improving production efficiency of TC Series materials. Oil-based thermal compounds maintain long-term oxidation stability, supporting extended lifecycle requirements in industrial and automotive applications. Integration of materials and dispensing equipment provides turnkey solutions for electronics manufacturers. Strategy focuses on reliability, vertical integration, and automotive-grade thermal management.

Laird (DuPont) Advances Anisotropic and Thin-Film TIMs for Next-Generation Electronics and Aerospace Systems

Laird Performance Materials, part of DuPont Electronics & Industrial, specializes in advanced TIM architectures for semiconductor and electronics applications. Integration with DuPont enables development of harmonized TIM1 and TIM2 systems to reduce thermal expansion mismatch. Pyrolytic graphite TIMs enable lateral heat spreading, critical for ultra-thin smartphones and foldable devices. Expansion in automotive radar systems supports ADAS and autonomous vehicle technologies with combined thermal and EMI solutions. The company is developing low-outgassing materials for space and satellite applications where conventional TIMs fail. Strategy emphasizes advanced materials engineering, anisotropic heat management, and high-reliability applications.

United States – Capacity Scale-Up Aligned with AI, Defense, and EV Electrification

The United States remains a core innovation and scale hub for polymer-based thermal interface materials, with recent developments reinforcing its leadership across electronics, AI infrastructure, aerospace, and electric mobility. In September 2025, Henkel Adhesive Technologies completed a $30 million expansion of its Brandon, South Dakota facility, doubling the site to 70,000 square feet. The site is now positioned as a North American manufacturing and application hub for LOCTITE® and BERGQUIST® thermal management materials, supporting high-volume demand from data centers, automotive electronics, and industrial power modules. The expansion integrates paperless production systems and automated temperature control, aligning manufacturing practices with the 2026 U.S. Industrial Decarbonization Roadmap and reinforcing compliance readiness for OEM supply chains.

Corporate and financial restructuring is further accelerating U.S. innovation depth. In October 2025, Honeywell completed the spin-off of its Advanced Materials business into Solstice Advanced Materials, isolating high-growth polymer and thermal technologies to fast-track aerospace- and electronics-grade R&D. Venture capital activity is also shaping next-generation TIM design, with TDK Ventures investing in NovoLINC to develop polymer TIMs optimized for AI clusters and GPU heat sinks. At the application level, Indium Corporation showcased a new liquid-metal containment architecture at IMAPS Thermal 2025, enabling reliable polymer-hybrid TIMs for defense electronics. Complementing this, Henkel’s North America Battery Application Center in Michigan, launched in late 2025, is accelerating injectable TIM validation for cell-to-pack EV battery architectures.

Germany – Automotive Power Electronics and Precision Formulation Leadership

Germany’s polymer-based TIM market is anchored in automotive electrification, power electronics reliability, and precision material engineering. In November 2025, Henkel introduced Loctite SI 5643 and SI 5637 in Düsseldorf, two-component fast-curing silicone potting compounds engineered for integrated x-in-1 EV powertrain architectures. These materials address the thermal, vibration, and dielectric requirements of on-board chargers and inverters, reinforcing Germany’s role in defining materials standards for next-generation EV platforms.

Customization speed and reliability are key competitive levers in the German ecosystem. Parker Chomerics expanded its European footprint in 2025 with a rapid sampling and prototyping facility, allowing OEMs to shorten qualification cycles for gap fillers and gels. The company’s 2025 TIM catalogue refresh, including THERM-A-GAP GEL 120, directly addresses oil-bleed challenges in vertical automotive assemblies. At Productronica 2025, German materials experts also presented mixed-alloy polymer systems designed to extend component lifetimes under extreme thermal cycling, highlighting Germany’s emphasis on long-term reliability over short-term conductivity gains.

Japan – Reliability-Driven Materials for AI Servers and High-Voltage EV Systems

Japan’s polymer-based TIM industry continues to differentiate through reliability engineering, material purity, and advanced silicone chemistry. In mid-2025, Shin-Etsu Chemical launched the CLG series of pump-out-resistant gap fillers, addressing a critical failure mode in high-power AI servers where repeated thermal expansion causes material migration. These formulations are gaining traction in hyperscale data centers where uptime and long service intervals are non-negotiable.

Hybrid material innovation is expanding application reach. Panasonic Industrial updated its graphite-polymer TIM portfolio in November 2025, targeting EV charger thermal management with compressibility exceeding 40%, a key requirement for uneven interfaces. Japanese suppliers are also proactively responding to sustainability scrutiny by phasing out microplastic-contributing silicones, as showcased at Supplier’s Day 2025. Beyond traditional TIMs, Shin-Etsu’s heat-shrinkable silicone rubber tubing for high-voltage EV busbars, industrialized for 2025–2026 vehicle models, underscores Japan’s system-level approach to thermal and electrical safety integration.

China – Data Center Cooling and Localization of Thermal Expertise

China’s polymer-based TIM market is expanding rapidly in response to surging demand from data centers, AI compute infrastructure, and domestic semiconductor manufacturing. At Data Centre World 2025, Dow highlighted its DOWSIL™ TC-5960 thermally conductive compound, engineered specifically for high-density GPU workloads and large-scale data center deployments. These solutions are optimized for automated dispensing and long-term stability, addressing China’s fast-scaling hyperscale environments.

Localization of technical support and qualification capabilities is strengthening domestic adoption. Indium Corporation’s presence at TestConX China 2025 emphasized advanced testing protocols aligned with local semiconductor packaging standards. In parallel, Laird Technologies, under DuPont ownership, opened its first Customer Solution Enablement Center in China in 2025. This facility enables real-time thermal modeling and co-development with regional OEMs, reducing dependency on overseas design cycles and accelerating time-to-market for polymer TIM solutions across Asia-Pacific electronics supply chains.

Comparative Snapshot – Polymer-Based TIM Industry by Country

Polymer-based Thermal Interface Materials Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Focus Area

|

Market Positioning

|

|

United States

|

AI computing, defense electronics, EV batteries

|

Capacity expansion and venture-backed innovation

|

Global innovation and scale leader

|

|

Germany

|

EV power electronics and automotive reliability

|

Precision formulation and rapid prototyping

|

Automotive-centric materials benchmark

|

|

Japan

|

AI servers and high-voltage EV systems

|

Reliability, pump-out resistance, hybrid materials

|

High-reliability technology leader

|

|

China

|

Data centers and domestic semiconductor growth

|

Localized R&D and application engineering

|

Fast-scaling high-volume adopter

|

Polymer-based Thermal Interface Materials Market Report Scope

Polymer-based Thermal Interface Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1014.8 Million

|

|

Market Size (2034)

|

$1773.6 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Material Type (Silicone-Based Thermal Interface Materials, Non-Silicone Polymer Thermal Interface Materials, Phase Change Materials, Thermally Conductive Adhesives, Thermal Tapes & Films), By Product Form (Thermal Gels & Greases, Thermal Gap Filler Pads, Thermal Potting Compounds & Encapsulants, Graphite-Polymer Composite Sheets), By Application (Consumer Electronics, Automotive, Telecommunications, High-Performance Computing, Medical Devices, Industrial & Power Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., Honeywell International Inc., Parker Hannifin Corporation, Shin-Etsu Chemical Co. Ltd., DuPont, Indium Corporation, 3M Company, Panasonic Holdings Corporation, Songwon Industrial Co. Ltd., Dymax Corporation, Fujipoly, Dexerials Corporation, Wacker Chemie AG, Kerafol Keramische Folien GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymer-Based Thermal Interface Materials Market Segmentation

By Material Type

- Silicone-Based Thermal Interface Materials

- Non-Silicone Polymer Thermal Interface Materials

- Phase Change Materials

- Thermally Conductive Adhesives

- Thermal Tapes & Films

By Product Form

- Thermal Gels & Greases

- Thermal Gap Filler Pads

- Thermal Potting Compounds & Encapsulants

- Graphite-Polymer Composite Sheets

By Application

- Consumer Electronics

- Automotive

- Telecommunications

- High-Performance Computing

- Medical Devices

- Industrial & Power Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymer-Based Thermal Interface Materials Industry

- Henkel AG & Co. KGaA

- Dow Inc.

- Honeywell International Inc.

- Parker Hannifin Corporation

- Shin-Etsu Chemical Co. Ltd.

- DuPont

- Indium Corporation

- 3M Company

- Panasonic Holdings Corporation

- Songwon Industrial Co. Ltd.

- Dymax Corporation

- Fujipoly

- Dexerials Corporation

- Wacker Chemie AG

- Kerafol Keramische Folien GmbH

*- List not Exhaustive