Environment Health and Safety Market to Reach $16.4 Billion by 2034 at 7.7% CAGR Amid Climate-Driven Compliance and AI-Led Risk Management

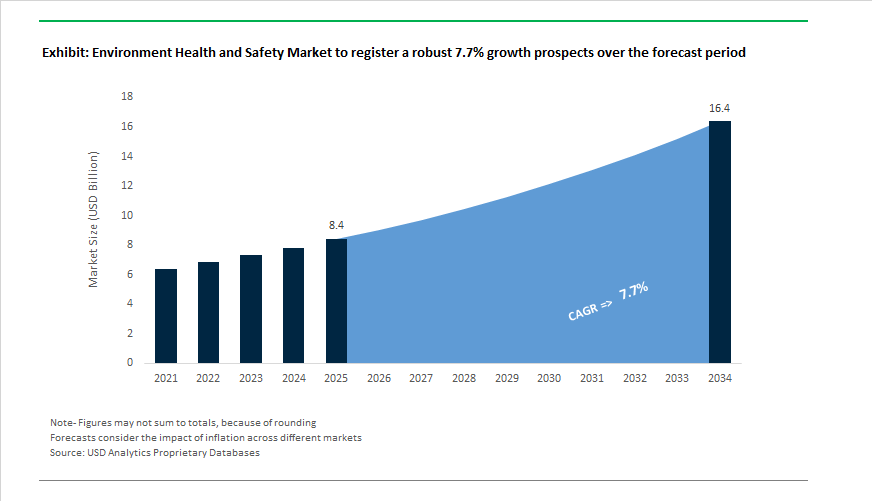

The Environment Health and Safety (EHS) Market is projected to grow from $8.4 billion in 2025 to $16.4 billion by 2034, registering a CAGR of 7.7%. Market expansion is being driven by climate-linked regulatory tightening, digital transformation of compliance systems, and enterprise demand for predictive risk analytics. In January 2026, the International Organization for Standardization released ISO/PAS 45007:2026, introducing formal guidance for integrating climate-driven hazards such as extreme heat, wildfire smoke, and flooding into ISO 45001 occupational health systems. This development has elevated EHS platforms from compliance repositories to dynamic risk-mitigation infrastructures. Concurrently, enforcement momentum intensified in 2025 when Occupational Safety and Health Administration advanced its Heat Illness Prevention Rule under the National Emphasis Program, accelerating demand for wearable heat sensors, AI-enabled worker monitoring, and automated alert systems capable of real-time physiological tracking.

Digital platform consolidation and software differentiation are reshaping competitive positioning. In January 2025, Wolters Kluwer’s Wolters Kluwer Enablon platform was ranked market leader in the Verdantix Green Quadrant, receiving top scores for configurability, master data governance, and incident lifecycle management—attributes critical for multinational enterprises operating across complex regulatory jurisdictions. In March 2025, Intelex Technologies launched Intelex Essentials to target small and mid-sized enterprises with modular incident tracking and document control systems, lowering adoption barriers in the mid-market segment. Earlier, in February 2024, VelocityEHS strengthened its contractor compliance capabilities through acquisition, enabling centralized oversight of third-party vendor safety data within its Accelerate® platform. This integration trend is mirrored in services consolidation, where Paradigm HSE acquired Paragon Safety Group in June 2025, expanding on-site staffing and industrial safety training capabilities across North America.

Large-scale environmental remediation and ESG-linked regulatory mandates are expanding the services dimension of the EHS market. In May 2025, AECOM secured an $80 million remediation contract at Vandenberg Space Force Base, highlighting the increasing federal expenditure on contaminated site management and regulatory adherence. Corporate digital transformation initiatives are reinforcing predictive analytics as a strategic differentiator; in October 2025, BASF launched its Safety Foresight initiative, embedding agentic AI across environmental sensors and HR data streams to shift from reactive incident reporting to forward-looking hazard prediction. Policy tightening in Asia is further amplifying demand. In January 2026, India strengthened its Carbon Credit Trading Scheme benchmarks, compelling heavy industries to adopt real-time emissions tracking and ESG reporting tools to mitigate financial exposure. Simultaneously, Hindustan Unilever Limited expanded its solar-powered Suvidha Centres in August 2025, demonstrating corporate integration of environmental health, sanitation infrastructure, and measurable sustainability governance. Collectively, regulatory harmonization, AI-driven safety analytics, contractor compliance digitization, and carbon accountability frameworks are redefining the global EHS technology and services landscape.

Trends and Opportunities in the Environment, Health and Safety (EHS) Market

Deep Integration of EHS Data with ESG Reporting and Financial Risk Systems

- The shift from voluntary sustainability disclosures to legally enforceable, audit-ready filings is fundamentally redefining EHS data governance. Regulatory frameworks such as the EU Corporate Sustainability Reporting Directive (CSRD) and U.S. SEC Climate Disclosure Rules are forcing EHS metrics to meet the same rigor as financial statements.

- From January 2025 onward, large accelerated filers in the United States have been preparing for first-cycle reporting under the SEC’s Final Climate Rule, which requires Scope 1 and Scope 2 emissions disclosure within Form 10-K filings. This requirement places EHS data under Internal Control over Financial Reporting (ICFR) standards, significantly raising expectations around data accuracy, traceability, and internal validation. As a result, EHS platforms are increasingly being integrated with ERP, finance, and audit systems to ensure emissions, safety incidents, and environmental liabilities can withstand regulatory and investor scrutiny.

- In Europe, the November 2025 refinement of CSRD and Corporate Sustainability Due Diligence Directive (CSDDD) thresholds expanded mandatory reporting to companies exceeding 1,750 employees and €450 million in turnover. This expansion compels thousands of organizations to operationalize double materiality assessments, quantifying both environmental impact and climate-driven financial risk. To meet phased assurance requirements moving toward reasonable assurance by 2028, enterprises are upgrading EHS platforms with immutable audit trails, sensor-linked data capture, and centralized single source of truth architectures. These upgrades are increasingly viewed as risk mitigation investments against greenwashing penalties, litigation exposure, and capital market exclusion.

AI-Driven Predictive Analytics Transforming EHS from Reactive to Preventive

- EHS management is rapidly shifting from post-incident reporting toward predictive risk prevention through artificial intelligence, machine learning, and natural language processing. Leading organizations are deploying Industrial AI to analyze unstructured data streams including maintenance logs, worker observations, video feeds, and sensor telemetry.

- In May 2025, Siemens expanded its Industrial Copilot ecosystem to include AI agents that proactively execute safety workflows. These systems interpret machine data and frontline worker inputs to predict hazardous conditions before incidents occur, with internal benchmarks indicating productivity improvements of up to 50% alongside measurable reductions in safety-related downtime.

- Operational proof points are reinforcing adoption. A June 2025 predictive maintenance pilot at the Sachsenmilch dairy processing facility identified an early-stage pump failure, preventing an unplanned shutdown and avoiding potential chemical exposure risks. The intervention delivered low six-figure cost savings while reducing emergency repair hazards. At a global policy level, International Labour Organization highlighted in its 2025 report Revolutionizing Health and Safety that AI-enabled monitoring is accelerating progress toward zero-accident workplaces. Countries across Southeast Asia are now embedding AI-based ergonomic and environmental risk detection into national occupational safety programs, signaling long-term structural demand for predictive EHS platforms.

Digital Management of Complex Chemical Regulations and Supply Chain Due Diligence

- The enforcement of the CSDDD and parallel global due diligence regulations is creating a major growth opportunity for EHS software providers specializing in chemical compliance and supply chain transparency. Under the revised April 2025 CSDDD, large EU and non-EU corporations with over 5,000 employees and €1.5 billion in turnover must conduct comprehensive environmental and human rights due diligence across multi-tier supply chains.

- This requirement is driving demand for EHS platforms capable of Tier-N supplier mapping, automated risk scoring, and real-time Safety Data Sheet management across thousands of suppliers. At the same time, regulatory fragmentation across EU REACH, UK REACH, U.S. TSCA, and state-level mandates such as California Proposition 65 is overwhelming manual compliance processes. As a result, Regulatory Change Tracking as a Service has emerged as a core purchasing criterion, with enterprises prioritizing platforms that continuously monitor and translate regulatory updates into actionable compliance workflows.

- Industry analysis from November 2025 indicates that audit readiness is now the primary driver of EHS software investment. Organizations adopting integrated EHS compliance platforms report reductions of over 40% in manual reporting effort, while improving inspection outcomes and reducing enforcement risk. This positions digital chemical compliance as one of the fastest-growing subsegments within the broader EHS market.

EHS as a Core Enabler of Clean Energy and Infrastructure Project Execution

- The acceleration of clean energy, battery manufacturing, and large-scale infrastructure projects is creating sustained demand for project-centric EHS solutions. Incentive frameworks such as the U.S. Inflation Reduction Act and the EU Green Deal have triggered unprecedented capital deployment into gigafactories, renewable energy plants, and water infrastructure.

- By Q1 2025, cumulative U.S. clean manufacturing investments exceeded $115 billion across more than 380 announced facilities. These projects introduce complex EHS risk profiles, including lithium-ion battery thermal hazards, hazardous chemical handling, and high-density construction environments. New 2025 battery safety regulations require advanced thermal management, fire suppression, and rapid isolation protocols, making EHS professionals integral to facility design rather than post-construction compliance.

- In emerging markets, projects such as Reliance Industries’ 5,000-acre giga complex in India highlight the scale at which EHS governance must operate. Parallel public infrastructure funding, including the Clean Water State Revolving Fund, is further expanding opportunities for EHS consultants and software providers to deliver integrated solutions covering permitting, contractor safety, environmental impact assessments, and community engagement. Collectively, these dynamics position EHS platforms as strategic enablers of capital-intensive growth rather than cost-center compliance tools.

Environment, Health, and Safety (EHS) Market Share and Segmentation Insights

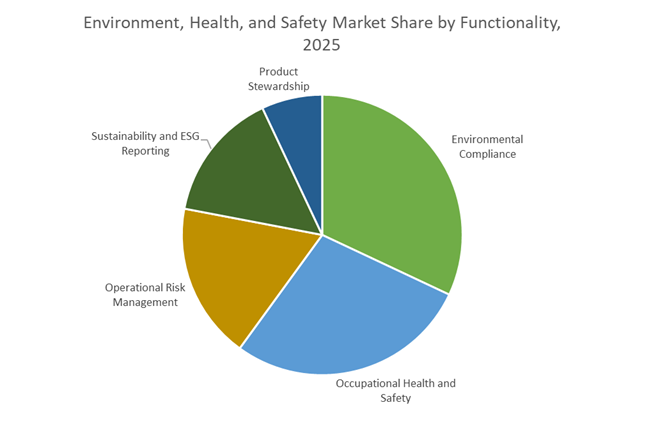

Environmental Compliance Software Captures the Largest Functional Share Amid Regulatory Pressure

Environmental compliance represents 32% of total EHS market share in 2025, reflecting escalating global regulations governing emissions, waste handling, water discharge, and chemical reporting. Organizations increasingly deploy digital EHS platforms to automate permit management, audit readiness, and regulatory submissions, minimizing operational risk and penalties. Occupational health and safety follows as a major functionality segment, supported by OSHA and ISO 45001 mandates that drive adoption of incident management, safety training, and exposure monitoring systems. Operational risk management maintains strong traction in energy, chemicals, and heavy industries, integrating process safety and asset integrity into enterprise risk frameworks. Sustainability and ESG reporting is the fastest-growing segment, propelled by investor scrutiny and climate disclosure requirements, with platforms tracking carbon footprints and ESG KPIs. Product stewardship remains niche but essential for managing REACH, TSCA, and lifecycle chemical compliance.

Energy and Utilities Sector Leads Enterprise-Wide EHS Platform Deployment

Energy and utilities account for 22% of global EHS adoption in 2025, making them the largest end-user segment due to high operational risk profiles and stringent regulatory oversight. Oil and gas operators, power generators, and renewable energy companies rely on EHS systems for process safety, environmental monitoring, and workforce protection. Chemicals and petrochemicals follow closely, using EHS platforms to manage hazardous materials, exposure risks, and complex compliance obligations. Manufacturing industries integrate EHS into lean operations to enhance worker safety and environmental performance. Construction and engineering emphasize mobile EHS tools for field inspections and incident reporting, while healthcare and pharmaceuticals deploy EHS for hazardous drug handling and accreditation compliance. Government, defense, and food and beverage represent smaller but growing segments, increasingly prioritizing sustainability reporting, supply chain transparency, and workforce safety management.

Competitive Landscape of the Environment Health and Safety (EHS) Market

The Environment Health and Safety market in 2026 is defined by rapid AI adoption, ESG-driven compliance, and the convergence of EHS, risk management, and sustainability platforms, with vendors competing on investor-grade data, connected worker technology, Scope 3 emissions management, and real-time operational risk intelligence.

Enablon leads investor-grade EHS and ESG integration through AI-powered compliance platforms

Enablon (Wolters Kluwer) remains the global benchmark for enterprise EHS and ESG software, serving large multinationals with the Enablon Vision Platform for air compliance, GHG emissions management, and risk governance. In early 2026, Wolters Kluwer strengthened its Corporate Performance & ESG unit by acquiring StandardFusion for $37.4 million and appointing new executive leadership to accelerate its AI roadmap. Enablon also launched AI-enhanced regulatory technology on Microsoft Azure and MongoDB to automate ESG data validation. Its core strength lies in investor-grade, audit-ready reporting, making Enablon the preferred platform for publicly listed enterprises prioritizing regulatory resilience, ESG transparency, and operational excellence.

VelocityEHS pioneers human-centered AI for predictive safety and ergonomics

VelocityEHS differentiates itself through human-centered AI, concentrating on workplace health, safety analytics, and chemical management. In January 2026, the company secured a US patent for its 3D human pose estimation system, using standard video to identify ergonomic risks and reportedly cutting recordable injuries by up to 97%. Its Accelerate® Platform embeds Vēlo, an AI assistant delivering real-time guidance to frontline workers. Backed by PhD AI scientists and board-certified ergonomists, VelocityEHS focuses on practical applications such as AI PSIF insights and automated hazard analysis, positioning itself as a high-impact EHS provider for manufacturers seeking measurable reductions in incidents and compliance exposure.

Cority expands converged EHS+ with embedded AI and government-grade deployments

Cority operates at the forefront of the converged EHS+ market, blending occupational health, safety, and sustainability into CorityOne. Powered by Cortex AI agents built on Google Gemini models, the platform automates tasks like medical scribing and permit analysis. In early 2026, Cority expanded into Saudi Arabia in alignment with Vision 2030 and partnered with Carahsoft to deliver its FedRAMP-authorized solution to US agencies. The launch of SIF Essentials and Audit Essentials enables rapid digital deployment for mid-market firms, reinforcing Cority’s strategy of embedding intelligence directly into factory and clinical workflows.

Intelex drives connected worker EHSQ convergence with AI-enabled field reporting

Intelex Technologies, part of Fortive, leads in EHSQ integration and connected worker solutions. Its 2026 Voice of EHS report revealed that 34% of EHS leaders now actively use AI, with mental health emerging as a core safety priority. Q1 2026 launches of Input AI: Lens and Auto-Populate enable speech-to-text and image-based hazard reporting, reducing form completion time by 70%. Intelex also enhanced its ACTS compliance system with mobile-first design and deeper industrial IoT integration, making it one of the few platforms unifying environmental data, safety performance, and ISO-aligned quality management.

Sphera dominates environmental accounting with unmatched LCA and Scope 3 intelligence

Owned by Blackstone, Sphera is the global authority in environmental accounting and product stewardship. In 2026, Sphera repositioned AI at the core of its Supplier 360 Intelligence tool to detect ESG risks and supply chain disruptions in real time. Its proprietary database includes over 500,000 emissions factors and 20,000 verified datasets, making it the market leader in Life Cycle Assessment software. A landmark Scope 3 report released in January 2026 targets the 89% of enterprises expanding indirect emissions tracking, while its LCA automation tools deliver audit-ready product carbon footprints in minutes.

United States: Compliance Intensification Driving Cloud-Based EHS Adoption

The United States Environment Health and Safety market is entering a decisive regulatory phase as federal agencies move from guidance to enforceable standards. Following the conclusion of public hearings in July 2025, Occupational Safety and Health Administration is preparing to finalize a nationwide Heat Injury and Illness Prevention Standard in 2026. This regulation mandates formal heat safety programs, real-time temperature monitoring, and documented response protocols across construction, logistics, and manufacturing environments. As a result, employers are accelerating investments in sensor-integrated EHS platforms capable of linking environmental data with workforce exposure records in real time.

Chemical risk management is tightening in parallel. Effective January 2026, Environmental Protection Agency classified PFOA and PFOS as hazardous substances under CERCLA, triggering mandatory federal cleanup and long-term liability tracking. EHS teams are responding by deploying advanced chemical inventory modules and emissions tracking tools that align with the expanded Toxic Release Inventory reporting. The addition of 16 new PFAS substances to the TRI list for the 2026 cycle has further increased demand for automated compliance dashboards, especially as penalties for willful violations reached $161,323 per incident in late 2024.

Digital compliance is also reshaping occupational health reporting. Since February 15, 2025, OSHA Voluntary Protection Program sites must submit injury and illness metrics through a centralized electronic portal. This requirement has accelerated migration toward enterprise-grade EHS software platforms such as Enablon and Cority, which integrate incident reporting, audit management, and regulatory submissions. Beyond physical safety, the U.S. Department of Labor’s expanded funding for the Total Worker Health initiative in 2025 has introduced psychosocial risk indicators into inspections, formalizing burnout and stress as measurable workplace hazards within EHS management systems.

India: Labor Code Consolidation Catalyzing Digital EHS Infrastructure

India’s EHS market is undergoing structural transformation following the formal implementation of the four consolidated Labour Codes on November 21, 2025. This regulatory overhaul unifies fragmented compliance requirements into a single framework, mandating that manufacturing, construction, and process industries register on centralized digital platforms for safety and environmental oversight. As a result, Indian enterprises are shifting rapidly from manual documentation toward cloud-enabled EHS systems that provide audit-ready records and standardized compliance reporting across states.

The Ministry of Labour and Employment’s 2025 industrial safety modernization initiative is reinforcing this transition. Factory inspections are being digitized, with regulators increasingly linking training effectiveness, certification status, and incident outcomes through connected EHS workflows. Under the Occupational Safety, Health and Working Conditions Code, high-risk sectors such as chemicals, mining, and infrastructure are now subject to mandatory safety audits supported by verifiable digital evidence. This has driven strong uptake of mobile-first hazard reporting tools and real-time incident logging applications, particularly among mid-sized manufacturers seeking to reduce inspection friction and enforcement risk.

European Union: ESG Convergence and Machine-Readable EHS Reporting

Across the European Union, with Germany and France at the center, the EHS market is being reshaped by sustainability-led governance and data standardization. From January 1, 2026, the Corporate Sustainability Reporting Directive expands to cover companies with more than 250 employees or €50 million in turnover. This requires EHS metrics to be disclosed in the European Single Electronic Format using XHTML and XBRL tagging, effectively transforming health, safety, and environmental data into machine-readable compliance assets.

The regulatory net is tightening further through the European Commission’s Omnibus Proposal and the introduction of Voluntary Reporting Standards for SMEs in early 2025. While optional for smaller firms, large enterprises are already cascading these requirements across their 2026 supply chains to ensure double materiality alignment. In parallel, the 2026 REACH Recast introduces stricter controls on microplastics and solvent-intensive formulations. German chemical majors are responding by deploying AI-driven product stewardship platforms capable of automating the reclassification and relabeling of thousands of chemical intermediates, significantly elevating the strategic importance of digital EHS solutions.

China: Real-Time Environmental Surveillance as Policy Enforcement

China’s Environment Health and Safety framework is moving decisively toward continuous monitoring and centralized enforcement. The Ecological Environment Monitoring Regulation, promulgated by the State Council in October 2025 and effective January 1, 2026, mandates that major pollution sources install video surveillance and automated monitoring equipment directly networked with environmental authorities. This requirement is accelerating adoption of integrated EHS and environmental monitoring systems capable of transmitting verified data streams to regulators without manual intervention.

Enforcement intensity is rising alongside technological oversight. In May 2025, China launched the fourth phase of its third round of central environmental inspections, covering key provinces and state-owned power enterprises. This phase marked the first use of satellite-based remote sensing to validate compliance in sensitive regions such as the Yellow River Basin. Further pressure is expected following the December 2025 Carbon Neutrality White Paper, which outlines a 2026 roadmap for expanding industrial VOC taxation. EHS managers are therefore prioritizing real-time VOC measurement and early-warning systems to mitigate both financial exposure and reputational risk.

Australia: Criminal Liability Elevating Board-Level EHS Governance

Australia’s EHS market is being fundamentally reshaped by the criminalization of severe safety breaches. As of July 1, 2024, South Australia and New South Wales joined other states in enforcing industrial manslaughter laws, exposing corporations to fines of up to $20.4 million and individuals to prison terms of up to 20 years for gross negligence. This legal shift has elevated EHS oversight to the board and executive level, driving demand for defensible audit trails and continuous compliance monitoring.

Financial exposure continues to rise with the indexation of penalties under the Model Work Health and Safety Act. From July 1, 2025, maximum fines for reckless conduct are adjusted annually in line with CPI, increasing the long-term cost of non-compliance. As a result, Australian enterprises are investing in enterprise-wide EHS platforms that integrate incident reporting, contractor safety, and regulatory alerts, positioning digital EHS governance as a core risk management function rather than an operational afterthought.

Environment Health and Safety Market: Country-Level Strategic Summary

Environment Health and Safety (EHS) Market County Level Snapshot

|

Region

|

Primary Regulatory Driver

|

Key Market Impact

|

Structural Shift

|

|

United States

|

Heat standards, PFAS enforcement

|

Surge in cloud and sensor-enabled EHS platforms

|

Proactive, data-driven compliance

|

|

India

|

Unified Labour Codes

|

Rapid digitization of inspections and audits

|

Centralized EHS governance

|

|

European Union

|

CSRD and REACH Recast

|

Machine-readable EHS and ESG integration

|

Compliance-led digital transformation

|

|

China

|

Networked environmental monitoring

|

Real-time surveillance and enforcement

|

Continuous compliance model

|

|

Australia

|

Industrial manslaughter laws

|

Board-level accountability for EHS

|

Risk-centric EHS investment

|

Environment Health and Safety (EHS) Market Report Scope

Environment Health and Safety Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.4 Billion

|

|

Market Size (2034)

|

$16.4 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Component (Software, Services), By Deployment (Cloud-Based, On-Premise, Hybrid), By Functionality (Environmental Compliance, Occupational Health and Safety, Sustainability and ESG Reporting, Operational Risk Management, Product Stewardship), By End-Use Industry (Energy and Utilities, Chemicals and Petrochemicals, Construction and Engineering, Manufacturing, Healthcare and Pharmaceuticals, Food and Beverage, Government and Defense)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Enablon, Sphera, Cority, VelocityEHS, Benchmark Gensuite, Quentic, EcoOnline, Diligent Corporation, Intelex Technologies, Alcumus, Health and Safety Institute, Donesafe, Evotix, ProcessMAP, UL Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Environment Health and Safety Market Segmentation

By Component

By Deployment

- Cloud-Based

- On-Premise

- Hybrid

By Functionality

- Environmental Compliance

- Occupational Health and Safety

- Sustainability and ESG Reporting

- Operational Risk Management

- Product Stewardship

By End-Use Industry

- Energy and Utilities

- Chemicals and Petrochemicals

- Construction and Engineering

- Manufacturing

- Healthcare and Pharmaceuticals

- Food and Beverage

- Government and Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Environment Health and Safety Industry

- Enablon

- Sphera

- Cority

- VelocityEHS

- Benchmark Gensuite

- Quentic

- EcoOnline

- Diligent Corporation

- Intelex Technologies

- Alcumus

- Health and Safety Institute

- Donesafe

- Evotix

- ProcessMAP

- UL Solutions

*- List not Exhaustive