Market Overview: Rising Demand for Advanced ESD-Safe Materials in Electronics and Automotive

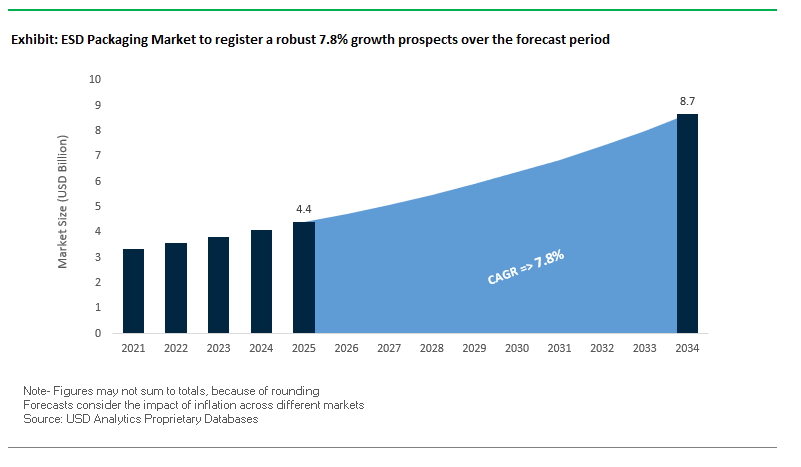

The Global Electrostatic Discharge Packaging Market is projected to grow from USD 4.4 billion in 2025 to USD 8.7 billion by 2034, expanding at a CAGR of 7.8%. This industry plays a crucial role in safeguarding sensitive electronics, semiconductors, and automotive components from electrostatic discharge, which can cause costly product failures. The sector is defined by continuous innovation in conductive polymers, advanced coatings, and recyclable materials, as well as increasing integration of sustainability and reusability into packaging design.

A key growth driver is the miniaturization of electronics. As microchips, PCBs, and sensors become more complex and fragile, demand for high-performance Electrostatic Discharge packaging continues to rise. Similarly, the automotive industry’s transition to EVs and ADAS systems has amplified the need for reliable ESD protection during production, shipping, and storage.

Sustainability is emerging as a critical focus. Electronics manufacturers are increasingly adopting reusable static-safe trays and PCR-based materials, aiming to reduce waste and comply with circular economy goals. Additionally, smart ESD packaging integrating RFID, NFC, and real-time monitoring sensors is gaining traction, enabling enhanced traceability and improved product security.

Key Insights for Industry Stakeholders:

- Market Value: USD 4.4B (2025) → USD 8.7B (2034), CAGR 7.8%.

- Miniaturization and semiconductor complexity driving advanced ESD needs.

- EVs and ADAS systems are major demand boosters in automotive applications.

- Growing adoption of recyclable, reusable, and PCR-based ESD packaging.

- Integration of smart sensors and conductive polymers shaping next-gen solutions.

Market Analysis: Recent Developments Driving the ESD Packaging Sector

The Global Electrostatic Discharge(ESD) Packaging Industry is rapidly evolving, with innovation in materials, sustainability, and partnerships driving strategic momentum.

In August 2025, a report noted increasing adoption of static dissipative packaging, preferred for sensitive electronic components due to its controlled charge dissipation. Another study in the same month highlighted that conductive plastics reached a 40% share in some market segments, underscoring the growing reliance on engineered polymers.

In July 2025, the automotive industry’s adoption of ESD solutions for EV components was highlighted, with rising demand linked to the integration of sensors and electronic control units. In May 2025, a leading distributor launched a new line of eco-friendly, recyclable Electrostatic Discharge boxes tailored for e-commerce electronics shipments, aligning with sustainability regulations.

The aerospace and defense sector is also driving innovation. A report from April 2025 revealed increased use of reusable ESD containers for high-value avionics, helping companies cut waste while improving efficiency. Similarly, in March 2025, a manufacturer of conductive polymers partnered with a global electronics firm to develop next-generation antistatic trays, showing the importance of collaborative R&D.

Material science continues to evolve. In February 2025, a chemical giant launched antistatic hot melt adhesives with low-temperature application, reducing energy use. The same month, the semiconductor industry reported a trend toward smart Electrostatic Discharge packaging with integrated sensors, enabling real-time monitoring of static levels for traceability.

Breakthrough Trends and Emerging Opportunities Reshaping the Global ESD Packaging Market

Strategic Shift Towards Sustainable and Recyclable Polymer Structures

The Electrostatic Discharge (ESD) packaging market is undergoing a structural transformation as manufacturers move away from non-recyclable multi-layer laminates toward mono-material, recyclable polymer structures. This trend is directly tied to the circular economy agenda, as traditional multi-layer packaging—often a mix of plastics, metals, and paper—is notoriously difficult and expensive to recycle. With major electronics OEMs enforcing stringent sustainability mandates, suppliers are now offering 100% polyethylene and polypropylene ESD films that deliver static protection while being easily recyclable. R&D efforts are heavily focused on creating mono-materials that match the moisture, oxygen, and contaminant barrier performance of conventional laminates while maintaining recyclability. Industry players that successfully commercialize these solutions are gaining a competitive edge by helping brands reduce environmental impact without compromising component safety. As sustainability becomes a procurement priority for semiconductor and electronics giants, this shift presents a major growth avenue in sustainable ESD packaging.

Integration of Smart and Connected Features for Real-Time Asset Tracking

A defining trend in the electrostatic discharge packaging market is the evolution of packaging from a passive protector to an active supply chain intelligence tool. With the integration of RFID tags, NFC chips, and serialized QR codes, Electrostatic Discharge (ESD) packaging is now enabling real-time visibility of high-value semiconductor components from fabrication plants to assembly lines. This is particularly critical in the semiconductor industry, where even a minor misplacement or error can result in substantial financial losses. By embedding tracking technology into ESD shielding bags, trays, and containers, companies are not only preventing counterfeiting but also automating inventory management and reducing manual handling errors. This convergence of physical protection and digital traceability creates a high-value niche in the ESD packaging industry, offering manufacturers the ability to sell packaging as both a protective medium and a data-driven service. Over time, this is reshaping the value chain into a more interconnected, analytics-driven ecosystem that enhances security, reduces costs, and builds resilience against counterfeit risks.

Development of High-Performance, Compostable Static-Dissipative Materials

One of the most compelling opportunities in the Electrostatic Discharge packaging market is the development of compostable and biodegradable materials that meet strict surface resistivity and charge decay standards. Current compostable options like PLA (Polylactic Acid) lack the heat resistance and structural strength needed for sensitive electronic transport, creating a technology gap in the market. Research is advancing toward plant-based, biodegradable anti-static films designed to naturally break down in composting environments while offering certified ESD protection. This innovation has the potential to drastically reduce landfill waste and microplastic pollution generated by single-use ESD packaging for lower-value electronic components. Manufacturers capable of commercializing high-performance compostable static-dissipative films stand to benefit from strong demand among eco-conscious OEMs and regulatory pressures pushing toward greener supply chains. Moreover, this opportunity is catalyzing collaborations between chemical innovators, material scientists, and packaging producers, fostering a more circular and sustainable value chain.

Expansion of Reusable and Reconditioned ESD Container Pooling Services

The ESD packaging sector is also seeing strong potential in the expansion of reusable container pooling services, a model particularly relevant for semiconductor and electronics manufacturing plants. Traditional single-use ESD packaging used for in-factory transport is both costly and environmentally unsustainable, whereas reusable conductive totes and static-dissipative containers provide a long-term cost advantage through durability and stackability. Third-party providers are now offering subscription-based container pooling services that include cleaning, reconditioning, tracking, and certified compliance, ensuring that packaging is reused efficiently without compromising ESD safety standards. This model lowers operational costs, reduces packaging waste, and aligns with the circular economy goals of large electronics producers. As global manufacturers shift toward just-in-time and closed-loop logistics models, reusable ESD container pooling services represent a high-value growth segment. The approach is fostering deeper collaboration between packaging manufacturers, logistics partners, and semiconductor companies, creating a data-driven ecosystem that enhances efficiency and sustainability in electronics supply chains.

Competitive Landscape: Leading Companies Shaping the ESD Packaging Market

The Global ESD Packaging Industry is highly competitive, with established leaders and specialized innovators focusing on sustainability, advanced materials, and tailored solutions.

Desco Industries focuses on complete ESD control solutions

Desco Industries is a leading provider of ESD control products, offering shielding bags, conductive foams, trays, and corrugated boxes. Its strength lies in a comprehensive portfolio designed for full Electrostatic Protected Areas (EPA). The company continues to invest in standards-compliant innovations, ensuring its solutions meet evolving electronics industry demands.

Smurfit Kappa develops anti-static corrugated packaging after WestRock merger

Smurfit Kappa, now part of Smurfit WestRock, leverages its paper-based expertise to produce anti-static corrugated boxes and inserts. Following its merger, the company benefits from an extended global manufacturing network and innovation capacity. Its focus is on sustainable corrugated packaging that ensures protection and premium unboxing for electronics and industrial goods.

Sealed Air integrates recycled content into protective ESD solutions

Sealed Air Corporation, best known for BUBBLE WRAP®, is a leader in protective packaging. In February 2025, it partnered with Best Buy to deploy recycled-content solutions, including high-recycled cushioning materials for electronics. Its strategy emphasizes automation, cost efficiency, and circular economy goals, catering to both consumer electronics and industrial electronics shipments.

Conductive Containers expands portfolio with Crestline Plastics acquisition

Conductive Containers, Inc. specializes in conductive and static dissipative packaging, including bins, totes, and corrugated products. In late 2024, it acquired Crestline Plastics, boosting production capacity in the U.S. Southwest. The company’s focus is on reusable Electrostatic Discharge packaging systems, helping manufacturers cut waste while improving efficiency in electronics and aerospace supply chains.

Pregis innovates with antistatic inflatable systems for electronics

Pregis offers protective solutions across foams, films, and bubble systems, with a strong focus on sustainability and efficiency. Its AirSpeed® inflatable packaging systems with antistatic films provide lightweight yet protective cushioning for electronics. The company emphasizes eco-friendly materials and automation, making it a preferred choice for electronics e-commerce and logistics providers.

ESD Packaging Market Share Insights

Bags Lead Market Share by Product Type in ESD Packaging

In the Electrostatic Discharge packaging market, bags hold the largest share at 35%, reflecting their versatility, scalability, and cost-effectiveness. Anti-static and shielding bags are ubiquitous across global supply chains, protecting billions of small components—such as semiconductors, resistors, and printed circuit boards—against static discharge, dust, and moisture. Their lightweight nature and adaptability make them ideal for bulk packaging while maintaining compliance with IEC and ANSI/ESD standards. Growth is reinforced by their compatibility with automated packaging lines and labeling systems, ensuring traceability in high-volume electronics manufacturing. While trays and foams offer specialized internal protection, bags remain the frontline solution, bridging performance reliability with affordability, thereby cementing their leading role across both consumer and industrial electronics sectors.

Electronics Sector Maintains Largest Market Share by End-Use in ESD Packaging

The consumer and industrial electronics sectors combined account for over 50% of the Electrostatic Discharge (ESD) packaging industry, reflecting their scale and critical reliance on static protection. Consumer electronics drives demand through mass volumes of devices requiring low-cost, disposable packaging, while industrial electronics emphasizes durable, reusable formats to support automated assembly and global distribution. This dual demand dynamic illustrates why electronics remains the dominant end-use category, as packaging failure in this sector can lead to catastrophic financial losses and product recalls. The rise of advanced semiconductors, 5G devices, and IoT components further amplifies the need for stringent protection, ensuring that electronics will continue to anchor ESD packaging market share well into the next decade.

United States ESD Packaging Market Gaining Momentum Through Regulatory Compliance and Smart Packaging Innovations

The United States Electrostatic Discharge (ESD) packaging market is strongly influenced by federal and state-level regulations, particularly Extended Producer Responsibility (EPR) laws that shift the burden of recycling and waste management from taxpayers to manufacturers. This regulatory environment is incentivizing companies to design ESD packaging that is recyclable, material-efficient, and free from problematic components. Technological innovations are a key growth driver, with smart packaging integrating QR codes and NFC chips enabled by digital printing, offering enhanced supply chain traceability and consumer engagement through digital product passports.

Corporate investments further accelerate market growth. For instance, EcoCortec launched EcoSonic VpCI-125 PCR HP Films and Bags in November 2024, utilizing 30% post-consumer recycled material to meet sustainability targets. Demand is particularly strong in consumer electronics and semiconductor sectors, propelled by the U.S. CHIPS and Science Act, which is boosting semiconductor fabrication and increasing the requirement for protective ESD packaging. Sustainability remains a key business priority, with biodegradable films and recyclable paperboard gaining traction to reduce environmental impact without compromising ESD performance.

Germany ESD Packaging Market Leading Through Circular Economy and High-Performance Innovations

Germany’s ESD packaging market is guided by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates fully recyclable or reusable packaging by 2030 and phasing out chemicals like PFAS. The country’s advanced Extended Producer Responsibility (EPR) system fosters innovation in recyclable and reusable ESD packaging, including containers and trays designed for sensitive electronic components. Companies are developing nanotube-based ESD materials, providing superior static protection while avoiding particle contamination from carbon black.

Key applications include the automotive, electronics, and industrial sectors, with electric vehicles (EVs) and advanced manufacturing driving demand for ESD packaging that protects sensors, battery management systems, and other sensitive electronics. Strategic partnerships between film producers and brand owners support customized high-performance flexible packaging solutions. The EU’s mandatory reuse rates are pushing the market towards durable, reusable ESD containers, reflecting Germany’s leadership in sustainable and technologically advanced packaging solutions.

China ESD Packaging Market Expanding on Green Initiatives and Smart Manufacturing

China’s ESD packaging industry is influenced by the government’s “dual carbon” goals and the March 2024 Action Plan for promoting equipment upgrades and sustainable materials. Regulatory reforms, including limits on packaging layers and void ratios effective September 2023, are shaping packaging design for electronic products sold through e-commerce, driving demand for optimized ESD packaging.

Technological advancements, including automation, AI, and integration of “5G plus industrial internet,” are enhancing production efficiency and flexible manufacturing. Companies such as Sanwei are innovating in static-dissipative circulation boxes that meet international standards. A push for domestic manufacturing is reducing reliance on imported technology, while rapid growth in consumer electronics, semiconductors, and e-commerce is creating high demand for durable, circular, and digitally printed packaging solutions across China.

Japan ESD Packaging Market Focusing on Bio-Based Materials and High-Performance Films

Japan’s ESD packaging sector is a core component of its precision manufacturing ecosystem, with companies turning to bio-polypropylene (bio-PP) and other bio-based materials to align with sustainability objectives. The Plastic Resource Circulation Act, effective April 2022, is promoting environmentally responsible packaging and reducing single-use plastics, targeting 2 million tonnes per year of bio-PP production by 2030.

Innovation is concentrated on high-performance films with superior barrier properties and real-time tracking using IoT sensors, enabled by digital printing. Functional enhancements, such as high dimensional stability and deformation resistance, are becoming critical for protecting sensitive electronics. Corporate collaborations, such as LyondellBasell’s partial incorporation of bio-based PP into Shiseido’s packaging, highlight cross-industry innovation and the adoption of sustainable, high-tech ESD solutions in Japan.

Brazil ESD Packaging Market Accelerating Through Regulatory Support and Sustainable Manufacturing

Brazil’s ESD packaging market is driven by the National Solid Waste Policy and new legislation banning single-use disposable items, mandating that all packaging be returnable, recyclable, or compostable by 2030. Compliance with these regulations is shaping market trends toward sustainable materials and packaging solutions.

Technological advancements, including robotics and AI, are enhancing manufacturing efficiency and quality control. The development of biodegradable films using carboxymethyl cellulose (CMC) derived from sugarcane bagasse is a notable innovation. Corporate investments, such as Wheaton’s interactive design facility in São Paulo, are boosting the production of sustainable ESD packaging. Key applications include electronics, food and beverage, and cosmetics sectors, where eco-friendly, high-performance packaging solutions are increasingly in demand. The Brazilian market is witnessing strong growth driven by green manufacturing initiatives, sustainable material adoption, and increasing awareness of environmental responsibility.

ESD Packaging Market Report Scope

ESD Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.4 Billion

|

|

Market Size (2034)

|

$8.7 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Product Type (Boxes, Trays, Bags, Foams, Other Packaging Types), By Material Type (Plastic, Paper & Paperboard, Fabric), By End-Use Industry (Consumer Electronics, Industrial Electronics, Aerospace & Defense, Automotive, Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Amcor plc, Desco Industries Inc., Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, Pregis LLC, Sealed Air Corporation, Rengo Co., Ltd., WestRock Company, DS Smith plc, Sonoco Products Company, Nefab AB, Teknis Limited, V.P. Enterprises

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electrostatic Discharge (ESD) Packaging Market Segmentation

By Product Type

- Boxes

- Trays

- Bags

- Foams

- Other Packaging Types

By Material Type

- Plastic

- Paper & Paperboard

- Fabric

By End-Use Industry

- Consumer Electronics

- Industrial Electronics

- Aerospace & Defense

- Automotive

- Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Electrostatic Discharge (ESD) Packaging Market

- 3M Company

- Amcor plc

- Desco Industries Inc.

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- Pregis LLC

- Sealed Air Corporation

- Rengo Co., Ltd.

- WestRock Company

- DS Smith plc

- Sonoco Products Company

- Nefab AB

- Teknis Limited

- V.P. Enterprises

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive, multi-faceted research methodology to deliver an in-depth analysis of the Global ESD Packaging Market, combining primary and secondary research techniques for maximum accuracy. Primary research included detailed interviews with packaging manufacturers, electronics OEMs, automotive suppliers, logistics providers, and sustainability experts to capture insights on demand drivers, regulatory compliance, technological adoption, and innovation trends. Secondary research involved reviewing company filings, press releases, trade journals, patent databases, government regulations, and sustainability reports to validate market sizing, competitive landscape, and emerging technologies. Quantitative forecasting assessed market value growth, CAGR, and segmentation by product type, material, and end-use industry, while qualitative analysis highlighted trends such as the shift to recyclable mono-material polymers, smart and connected ESD packaging, high-performance compostable films, and reusable container pooling services. USDAnalytics also evaluated regional dynamics across the U.S., Germany, China, Japan, and Brazil, focusing on regulatory frameworks, green initiatives, e-commerce penetration, and automation adoption. This methodology ensures a precise, data-driven outlook, enabling stakeholders to make strategic, operational, and investment decisions in the evolving Electrostatic Discharge packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.