Ethanolamines Market to Reach $6.2 Billion by 2034 as Gas Treatment, Surfactants, and Sustainable Derivatives Drive Structural Demand

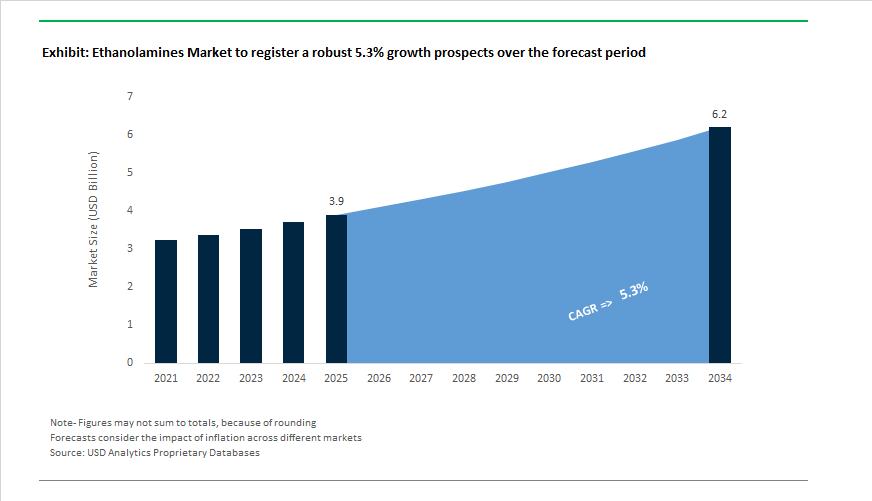

The Ethanolamines Market is projected to grow from $3.9 billion in 2025 to $6.2 billion by 2034, reflecting a CAGR of 5.3%, underpinned by resilient demand in gas sweetening, detergents, agrochemicals, and high-purity electronics applications. A defining structural development occurred in September 2024 when BASF inaugurated a world-scale alkyl ethanolamines facility at its Antwerp Verbund site. This investment expanded global production capacity for dimethyl ethanolamine (DMEOA) and methyl diethanolamine (MDEOA) by nearly 30%, lifting BASF’s annual output above 140,000 metric tons. The expansion reflects accelerating consumption in CO₂ capture, gas treatment systems, and surfactant intermediates. Concurrently, the BASF–Sinopec joint venture (BASF-YPC Co., Ltd.) completed capacity expansions in Nanjing in Q2 2024, reinforcing Asia-Pacific supply for monoethanolamine (MEA), diethanolamine (DEA), and triethanolamine (TEA). These integrated expansions signal a strategic shift toward localized, feedstock-secured production hubs aligned with regional petrochemical ecosystems.

Pricing dynamics in 2025 highlighted tightening supply fundamentals and rising operational costs. Dow implemented a $0.05 per pound increase across all ethanolamine grades in North America effective July 15, 2025, citing elevated energy inputs and sustained downstream demand from detergents and gas purification sectors. Meanwhile, refinery and ethylene upgrades in China are structurally reinforcing feedstock integration. Sinopec completed the second-phase expansion of its Zhenhai Refinery in December 2024, adding 18 production units and enhancing domestic availability of ethylene oxide precursors used in ethanolamine synthesis. Similarly, PetroChina advanced its Jilin petrochemical upgrading program through 2025, emphasizing green growth and more energy-efficient ethylene production to stabilize ethanolamine feedstock supply in North China. These developments collectively reduce reliance on imports while mitigating volatility across the amines value chain.

Sustainability and certification are reshaping competitive positioning. Nouryon secured ISCC PLUS certification in June 2024 for ethanolamines and ethylene oxide production, enabling the commercialization of biomass-balanced and circular grades for personal care and home care manufacturers. The company further strengthened its innovation footprint with the opening of a Mumbai R&D center in November 2024 to develop tailored ethanolamine formulations for India’s fast-growing agricultural and cosmetics markets. In parallel, Clariant expanded its sustainable intermediates portfolio in 2025, focusing on bio-based ethanolamine derivatives to align with tightening EU regulations targeting biodegradable surfactants and reduced solvent emissions. These initiatives reflect a broader migration from purely petrochemical amines toward traceable, lower-carbon alternatives demanded by multinational FMCG brands.

Downstream integration into electronics and high-performance chemicals is also intensifying. Dow’s updated DOWANOL™ solvent systems introduced in 2024 incorporate ethanolamine-based additives engineered for semiconductor wafer cleaning and precision pH control in advanced fabrication processes. At the same time, Huntsman Corporation reset its dividend in late 2025 to preserve financial flexibility amid cyclical margin pressure in performance products, underscoring industry-wide capital discipline during a period of feedstock volatility. BASF’s modernization of its chloroformates and acid chlorides facilities in Ludwigshafen (2024–2026) further stabilizes derivative supply chains critical to pharmaceuticals and crop protection chemicals.

Trends and Opportunities in the Ethanolamines Market

Strategic Shift Toward Derivative-Optimized Ethanolamine Production

- Global chemical producers are actively reconfiguring ethylene oxide integration strategies to prioritize ethanolamines and other specialty derivatives over traditional balanced slates. This shift reflects margin pressure in commoditized ethylene glycol markets and accelerating demand from surfactants, water treatment, and agricultural applications.

- In March 2025, Dow announced at the International Petrochemicals Conference the indefinite shutdown of its 300,000-tonne ethylene glycol unit at Seadrift, Texas. The company confirmed that purified ethylene oxide streams would be redirected toward higher-value derivatives, including monoethanolamine and triethanolamine, to support growth in performance surfactants, specialty solvents, and heat-transfer fluids. This move underscores a broader industry trend where capacity is being redeployed toward derivative chains offering pricing power and application stickiness.

- At the same time, BASF commissioned a new world-scale alkyl ethanolamines plant at its Antwerp Verbund site during late 2024 and early 2025. The facility is designed to serve specialty amine demand in gas treatment, water purification, and industrial cleaning, lifting BASF’s effective global capacity for alkyl ethanolamines by roughly 30%. The investment highlights the strategic value of integrated Verbund production in ensuring supply reliability and derivative customization.

- Regionally, Asia-Pacific continues to dominate ethanolamine consumption, accounting for approximately 44% of global demand in 2024 and 2025. This concentration is driven by China’s infrastructure build-out and India’s chemical sector expansion under the Production Linked Incentive framework, which has accelerated domestic surfactant, agrochemical, and cement additive manufacturing.

Scaling High-Purity Ethanolamines for Industrial Carbon Capture Applications

- Post-combustion carbon capture has emerged as one of the most structurally significant demand drivers for high-purity monoethanolamine. Despite advances in alternative solvents, MEA remains the benchmark absorbent due to its high reactivity with carbon dioxide, predictable kinetics, and established operating know-how.

- By December 2025, the Global Status of CCS identified 77 commercial carbon capture projects in operation and 47 additional facilities under construction. Projects such as the Northern Lights expansion and the Alberta Pulp Mill pilot launched in late 2025 are accelerating demand for audit-ready MEA with tightly controlled impurity profiles. These installations require solvent systems capable of sustaining capture efficiencies above 95% while minimizing degradation and corrosion risks.

- Technical studies conducted in 2025 revealed that at 100% capture intensity, MEA degradation rates can increase between 24% and 138% depending on flue gas composition and operating severity. This has triggered a parallel market for stabilizer packages, reclaiming systems, and advanced purification technologies that extend solvent life and reduce operating expenditure. Publicly backed investments, including Italy’s Snam allocation of approximately €0.5 billion and the Nebraska CCS project capturing 1.2 million tons of carbon dioxide annually as of January 2025, continue to prioritize amine-based systems due to their maturity and bankability.

Formulation of Low-VOC Cement Grinding Aids for Low-Carbon Construction

- The global cement industry is under intense pressure to reduce its clinker factor and associated emissions, creating a sustained opportunity for ethanolamines as performance-enhancing grinding aids. Triethanolamine and diethanolamine are increasingly specified to improve mill efficiency and early strength development in blended cement formulations.

- Between 2024 and 2025, more than 950 cement plants worldwide adopted AI-assisted dosing systems for grinding aids, enabling precise addition of ethanolamines. These systems have delivered energy savings of up to 25 kilowatt-hours per ton of cement while increasing mill throughput by an average of 12%. Grinding aids are now used in over 85% of composite cement production lines, supporting clinker reductions of up to 25% through higher fly ash and slag incorporation without compromising early strength performance.

- Regulatory momentum is reinforcing this trend. In Europe and India, blended cements now account for more than 40% of total output, supported by standards targeting a 30% reduction in cement-related carbon emissions by 2030. Within this context, ethanolamine-based grinding aids are increasingly viewed as non-negotiable tools for meeting both productivity and decarbonization objectives.

High-Value Intermediates for Glufosinate and Next-Generation Herbicides

- Agricultural chemistry is undergoing a structural shift away from glyphosate, creating strong downstream demand for ethanolamines as intermediates in alternative herbicide pathways. Monoethanolamine and alkyl ethanolamines play a central role in oxidative deamination and amination steps required for advanced non-selective herbicides.

- Major agrochemical producers, including BASF, are scaling L-glufosinate formulations that emphasize the biologically active isomer. These products require highly controlled amine donor systems to maximize L-isomer yield, significantly increasing the value contribution of high-purity ethanolamines. Formulation innovation is also accelerating, with ADAMA Ltd and peers deploying proprietary technologies to combine glufosinate with complementary actives such as S-metolachlor. These multi-mode formulations rely on ethanolamines to ensure chemical stability, rapid uptake, and improved burn-down efficacy against glyphosate-resistant weeds.

- Despite trade disruptions observed in early 2025, demand for agrochemical-grade ethanolamines has remained resilient. Industry surveys indicate that 79% of stakeholders now rank product purity of at least 99% as the most critical procurement criterion, reflecting the increasing technical and regulatory sensitivity of modern crop protection formulations.

Ethanolamines Market Share and Segmentation Insights

Monoethanolamine Leads Volume Consumption Across Gas Treatment and Chemical Intermediates

Monoethanolamine (MEA) commands 48% of total ethanolamines market share in 2025, reflecting its versatility as both a reactive intermediate and an acid-gas scavenger. MEA is the preferred amine for CO₂ and H₂S removal in natural gas processing, refineries, and ammonia plants, while also serving as a key building block for surfactants, detergents, and agrochemical intermediates. Diethanolamine maintains a substantial position in household and personal care surfactants, textile auxiliaries, and herbicide production, supported by its balanced reactivity profile. Triethanolamine plays an important multifunctional role as an emulsifier, pH adjuster, corrosion inhibitor, and cement grinding aid, enabling diverse industrial applications. Alkyl ethanolamines remain niche, serving specialized performance requirements in corrosion inhibition and gas treatment additives where modified solubility and reactivity are essential for targeted formulations.

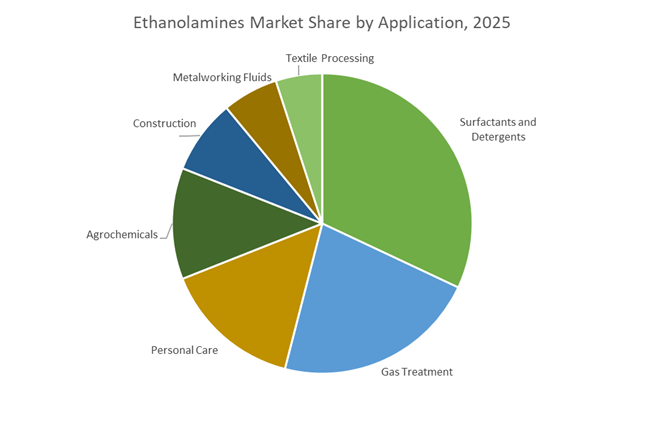

Surfactants and Detergents Anchor Demand as Energy and Agrochemical Uses Expand

Surfactants and detergents account for 32% of ethanolamines consumption in 2025, driven by sustained demand for household cleaners, industrial detergents, and personal hygiene products where ethanolamines act as emulsifiers, foam boosters, and grease-cutting agents. Gas treatment follows as the second-largest application, with MEA and DEA critical to acid gas removal in energy infrastructure amid rising global demand for cleaner fuels. Personal care remains a significant segment, using ethanolamines to stabilize creams, shampoos, and cosmetics. Agrochemicals rely on ethanolamines for glyphosate salts and pesticide dispersants, improving formulation performance. Construction applications utilize ethanolamines as cement grinding aids and concrete admixture components, while metalworking fluids represent a growing segment for corrosion protection during machining. Textile processing remains niche, employing ethanolamines in scouring and fabric preparation prior to dyeing.

Competitive Landscape of the Global Ethanolamines Industry (2026)

The global Ethanolamines Market is highly consolidated, with top-tier manufacturers leveraging backward integration into Ethylene Oxide (EO) to secure feedstock stability and cost leadership. In 2025 to 2026, strategic priorities have shifted toward high-purity grades, low-nitrosamine derivatives, carbon capture amines, and regional capacity optimization to comply with tightening environmental regulations across Europe and North America.

BASF SE expands alkyl ethanolamines capacity to capture carbon capture and water treatment growth

BASF SE remains a dominant force in the ethanolamines industry, producing over 300 amine derivatives through its Verbund integration model. In late 2024, BASF inaugurated a world-scale alkyl ethanolamines plant in Antwerp, Belgium, raising global capacity by nearly 30% to exceed 140,000 metric tons annually. The expansion targets high-growth intermediates such as Dimethyl Ethanolamine and Methyl Diethanolamine, critical for gas treatment and water treatment flocculants. By 2025, BASF transitioned multiple intermediate units to 100% renewable electricity, offering low Product Carbon Footprint amine profiles. Its integrated hubs in Ludwigshafen, Antwerp, Geismar, and Nanjing ensure feedstock security and supply resilience.

Dow Inc. leads North American ethanolamines with strategic price discipline and asset optimization

Dow Inc. accounts for nearly 45% of North American ethanolamine capacity, positioning it as the regional leader in Monoethanolamine, Diethanolamine, and Triethanolamine production. In July 2025, Dow implemented a $0.05 per pound price increase across its portfolio, citing feedstock and energy volatility. Despite a force majeure triggered by an unplanned outage at Al-Jubail in 2025, Dow maintained operational dominance. Under its 2025 to 2026 restructuring plan, the company is shutting higher-cost European upstream assets to focus on higher-margin derivatives. Dow’s ethanolamines serve as core intermediates for advanced surfactants and DOWSIL silicone specialties.

INEOS Oxide strengthens Atlantic basin dominance through EO integration and emission reduction

INEOS Oxide has emerged as a top-three global ethanolamines producer following its 2024 acquisition of LyondellBasell’s EO & Derivatives business in Bayport, Texas. This secured cost-advantaged feedstock for Gulf Coast amine production. In 2025, INEOS committed £30 million to its Hull site to reduce emissions by 75%, aligning with the UK’s net-zero industrial cluster goals. Integration of Bayport and Plaquemine facilities, supported by AI-driven predictive maintenance, is projected to cut unplanned downtime by 30%. Effective October 2025, INEOS adjusted pricing on glycol and amine derivatives to offset logistics inflation while safeguarding supply for gas dehydration and polyester resin markets.

Huntsman Corporation pivots toward performance ethanolamines for cement and personal care

Huntsman Corporation is transitioning from commodity ethanolamines toward value-added performance amines, particularly Triethanolamine for cement grinding aids and cosmetic pH adjustment. Responding to European Commission restrictions on Diethanolamine in 2025, Huntsman prioritized low-VOC and low-nitrosamine formulations tailored to regulatory compliance. The company’s Arabian Amines joint venture provides a strategic Middle Eastern manufacturing base serving fast-growing Asia-Pacific demand. Huntsman differentiates through specialty amine blends and polyetheramines that enhance moisture resistance in coatings and construction materials, reinforcing its niche leadership in agrochemical and infrastructure applications.

SABIC leverages hydrocarbon advantage to lead MEA supply for GCC carbon capture

SABIC capitalizes on Saudi Arabia’s hydrocarbon reserves to maintain low-cost leadership in ethanolamines. At K 2025, SABIC showcased its BLUEHERO and TRUCIRCLE initiatives, utilizing amine intermediates to support EV battery electrification and circular plastics. The company dominates the Middle East & Africa ethanolamine market, valued at approximately $0.3 billion in 2026. SABIC is a major supplier of Monoethanolamine for industrial carbon capture projects sanctioned between 2026 and 2030 across the GCC. Strategically, it is advancing circular feedstock integration to deliver certified bio-renewable ethanolamine derivatives by the end of 2026.

LOTTE Chemical Corporation restructures toward high-purity and semiconductor-grade amines

LOTTE Chemical Corporation is undergoing structural transformation in 2025 to 2026, reducing reliance on commodity petrochemicals and expanding into high-performance and semiconductor-grade chemicals. The company is scaling green materials and high-purity ethanolamines for pharmaceutical and food applications at integrated sites in South Korea and Indonesia. Although 2025 recorded operating losses due to seasonal weakness and startup costs, LOTTE projects profitability recovery in Q1 2026 as inventory normalization concludes. Through LOTTE Chemical Indonesia, it is strengthening supply to ASEAN detergent and surfactant markets, reinforcing its strategic foothold in Southeast Asia’s expanding amine demand.

China: Smart Verbund Integration and High-Purity Localization

China’s ethanolamines market is entering a structurally advanced phase driven by large-scale integrated investments and tighter environmental oversight. In November 2025, BASF commenced production at the core of its €10 billion Zhanjiang Verbund site. This complex includes world-scale ethanolamines and ethylene oxide units designed as a Smart Verbund, with full transition to renewable electricity targeted by 2026. The configuration significantly lowers energy intensity per ton of ethanolamine while improving feedstock efficiency through deep backward integration, reinforcing China’s position as a regional supply anchor for both commodity and specialty grades.

Parallel capacity expansion is occurring in eastern China. BASF-YPC, the 50:50 joint venture between BASF and Sinopec, finalized the expansion of its Nanjing site in late 2025, adding capacity for specialty alkyl ethanolamines such as dimethyl ethanolamine and methyl diethanolamine. These grades are increasingly critical in gas sweetening systems and high-performance coatings across Asia. Regulatory pressure is also reshaping operating standards. Effective January 1, 2026, China’s Ecological Environment Monitoring Regulation mandates real-time monitoring of VOC and amine emissions across chemical clusters. This requirement is accelerating investments in high-efficiency gas scrubbing systems and advanced ethanolamine-based absorbents. In parallel, producers in Guangdong have scaled ultra-high-purity ethanolamine production to support the 2026 ramp-up of domestic 7nm and 5nm semiconductor fabs, signaling a strategic pivot toward electronics-grade intermediates.

United States: Semiconductor-Grade Differentiation and Gas Treatment Demand

The U.S. ethanolamines market is increasingly defined by purity-led differentiation and sustained demand from gas processing infrastructure. In May 2025, Huntsman Corporation inaugurated a new E-GRADE® production unit at its Conroe, Texas facility. This unit is engineered to deliver high-purity, low-trace-metal amines, including quaternary amines required for advanced semiconductor nodes and AI-driven data center hardware. The move reflects growing domestic emphasis on localized supply of electronic-grade chemicals under broader semiconductor reshoring initiatives.

At the same time, bulk ethanolamine demand remains resilient due to natural gas processing. Dow completed the expansion of its monoethanolamine capacity in Louisiana during the 2025 cycle, targeting carbon dioxide and hydrogen sulfide removal in shale gas streams. Regulatory considerations are also influencing plant design and operations. Under the national OSHA heat safety standard scheduled for 2026, ethanolamine producers are integrating automated and remote monitoring systems to limit worker exposure during high-temperature distillation and esterification steps. These changes are increasing capital intensity but improving operational continuity and compliance resilience.

Belgium (European Union): Specialty Focus and Green Surfactant Transition

Belgium has emerged as a strategic hub for high-value ethanolamine derivatives within the European Union. BASF inaugurated a major alkyl ethanolamine production plant at its Antwerp Verbund site in late 2024 and early 2025, lifting its global alkyl ethanolamine capacity beyond 140,000 metric tons per year. This expansion supports downstream demand in coatings, agrochemicals, and specialty surfactants, while leveraging Antwerp’s integrated logistics and feedstock access.

Environmental policy is reshaping product portfolios across Europe. In 2025, manufacturers accelerated the shift toward readily biodegradable monoethanolamine variants engineered to comply with the 2026 EU Ecolabel requirements for household detergents and personal care formulations. At the same time, structural cost pressures are prompting asset rationalization. In July 2025, Dow announced the planned shutdown of selected upstream European assets by mid-2026, including energy-intensive cracker units. This right-sizing strategy is redirecting capital toward high-margin specialty amine derivatives rather than volume-driven base chemicals.

India: Policy-Backed Import Substitution and Formulation Growth

India’s ethanolamines market is being reshaped by industrial policy support and downstream formulation demand. Under the Production Linked Incentive scheme, the government approved capital outlays for 12 new specialty chemical projects in 2025, including domestic ethanolamine manufacturing aimed at reducing import dependence for pharmaceutical and agrochemical intermediates. These investments are strengthening supply security for triethanolamine and related grades used as stabilizers, emulsifiers, and pH adjusters.

Demand growth is also being reinforced by healthcare and fuel policy alignment. As of September 2025, the Department of Pharmaceuticals confirmed domestic production capacity for 26 key drug intermediates, many of which rely on triethanolamine in formulation chemistry. Additionally, the Ministry of Petroleum advanced the 20% ethanol blending target to the 2025–26 Ethanol Supply Year. Higher ethanol blends require enhanced corrosion inhibitors and stabilizers, directly increasing the consumption of ethanolamine-derived additives in fuel systems and storage infrastructure.

Saudi Arabia: Scale-Up and Electrification-Oriented Portfolio Shift

Saudi Arabia is positioning ethanolamines within a broader downstream diversification and electrification strategy. In August 2025, SABIC confirmed that its one million metric ton capacity Petrokemya project was over 95% complete, with pilot commissioning underway and full-scale operations expected through 2026. The project includes downstream amine intermediates, reinforcing the Kingdom’s role as a low-cost, large-scale producer serving both domestic and export markets.

Strategic focus is also shifting toward advanced applications. Under SABIC’s BLUEHERO™ initiative, highlighted in late 2025, the company is prioritizing specialized amine-based materials for electric vehicle battery systems and power electronics. This marks a clear move beyond traditional gas treatment and surfactant applications, aligning ethanolamine chemistry with the automotive electrification and energy transition value chain entering 2026.

Strategic Snapshot: Ethanolamines Market by Country

Ethanolamines Market County Level Snapshot

|

Country

|

Core Strategic Driver

|

Key Applications

|

Market Orientation

|

|

China

|

Verbund integration and emission regulation

|

Gas treatment, coatings, semiconductors

|

Scale with purity upgrade

|

|

United States

|

Semiconductor reshoring and shale gas

|

Electronic-grade amines, MEA

|

Purity-led differentiation

|

|

Belgium (EU)

|

Specialty capacity and ecolabel compliance

|

Surfactants, coatings

|

High-margin specialization

|

|

India

|

PLI incentives and ethanol blending

|

Pharma, agrochemicals, fuels

|

Import substitution

|

|

Saudi Arabia

|

Downstream scale-up and EV focus

|

Amine intermediates, EV systems

|

Portfolio diversification

|

Ethanolamines Market Report Scope

Ethanolamines Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$6.2 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Type (Monoethanolamine, Diethanolamine, Triethanolamine, Alkyl Ethanolamines), By Purity Grade (Industrial Grade, Pharmaceutical Grade, Semiconductor Grade), By Application (Surfactants and Detergents, Gas Treatment, Agrochemicals, Personal Care, Textile Processing, Metalworking Fluids, Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Huntsman Corporation, China Petroleum & Chemical Corporation, INEOS Group Limited, SABIC, Indorama Ventures Public Company Limited, LyondellBasell Industries N.V., Alkyl Amines Chemicals Limited, Nouryon, Jiaxing Jinyan Chemical Co., Ltd., Shijiazhuang Haisen Chemical Co., Ltd., Oriental Union Chemical Corporation, Sintez OKA Group, Celanese Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethanolamines Market Segmentation

By Product Type

- Monoethanolamine

- Diethanolamine

- Triethanolamine

- Alkyl Ethanolamines

By Purity Grade

- Industrial Grade

- Pharmaceutical Grade

- Semiconductor Grade

By Application

- Surfactants and Detergents

- Gas Treatment

- Agrochemicals

- Personal Care

- Textile Processing

- Metalworking Fluids

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethanolamines Industry

- BASF SE

- Dow Inc.

- Huntsman Corporation

- China Petroleum & Chemical Corporation

- INEOS Group Limited

- SABIC

- Indorama Ventures Public Company Limited

- LyondellBasell Industries N.V.

- Alkyl Amines Chemicals Limited

- Nouryon

- Jiaxing Jinyan Chemical Co., Ltd.

- Shijiazhuang Haisen Chemical Co., Ltd.

- Oriental Union Chemical Corporation

- Sintez OKA Group

- Celanese Corporation

*- List not Exhaustive