Monoethanolamine Market 2025–2034: Capacity Expansion, CCUS Adoption, and Detergent Neutralization Driving $9.9 Billion Outlook

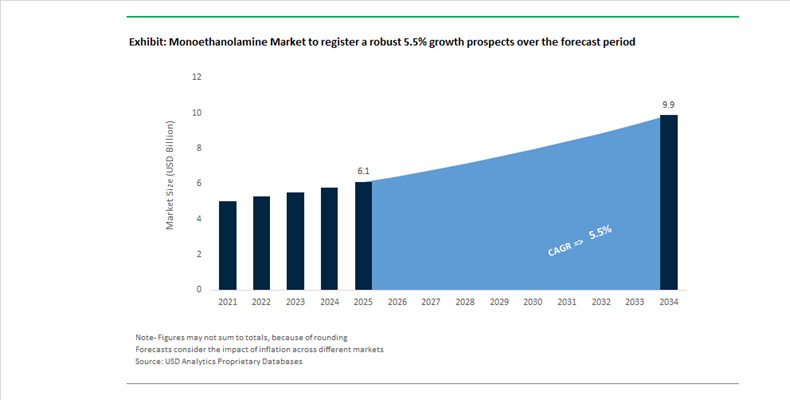

The Monoethanolamine (MEA) Market is projected to grow from $6.1 billion in 2025 to $9.9 billion by 2034, registering a CAGR of 5.5%. Market expansion is being shaped by three structural demand pillars: gas sweetening and carbon capture systems, liquid detergent neutralization, and agrochemical intermediates. MEA remains the benchmark primary ethanolamine due to its dual amine and hydroxyl functionality, enabling strong acid gas absorption, surfactant neutralization, and corrosion inhibition. The market is simultaneously experiencing regional capacity redistribution, cost pressure from energy-intensive ethylene oxide (EO) routes, and strategic portfolio optimization among global petrochemical majors.

In September 2024, BASF SE inaugurated a world-scale alkyl ethanolamines plant at its Antwerp Verbund site, increasing global capacity by nearly 30% to exceed 140,000 metric tons annually. This expansion strengthened supply security for gas treatment chemicals, coatings binders, and water treatment formulations. The strategic relevance of BASF’s intermediates business was further validated in early 2026 when Nouryon recognized BASF as a 2025 Supplier of the Year, underscoring the importance of MEA and ethylene oxide feedstock stability for downstream polymer and surfactant applications. Across Asia-Pacific, between late 2023 and 2024, at least six new ethanolamine units exceeding 50,000 metric tons annually were commissioned, primarily using EO-based production routes to serve Southeast Asian and Latin American agrochemical demand. In 2025, Reliance Industries commenced operations at its 3.60 mtpa Jamnagar methanol complex, indirectly reinforcing domestic feedstock security for ethanolamine derivatives and reducing India’s reliance on imports.

Pricing and corporate restructuring have also influenced supply dynamics. Effective July 15, 2025, Dow Inc. implemented a $0.05/lb price increase across MEA, DEA, and TEA portfolios in North America, citing sustained raw material and energy cost pressures. In January 2026, Dow launched its “Transform to Outperform” restructuring initiative following a $2.4 billion net loss in 2025, targeting operational streamlining and workforce reductions that directly affect its ethanolamine value chain. Similarly, in January 2026, SABIC signed agreements to divest its European Petrochemical business to AEQUITA, repositioning its oxygenated solvent and ethanolamine assets toward higher-growth regions.

Demand-side acceleration is particularly visible in environmental and homecare applications. Between 2024 and 2025, global adoption of high-purity MEA (above 99%) in Carbon Capture, Utilization, and Storage (CCUS) expanded significantly, with more than 500 gas-processing facilities globally utilizing MEA-based absorption systems. Typical annual plant consumption ranges from 350 to 500 metric tons to meet tightening emissions standards. In parallel, 2025 industry data indicated MEA’s presence in over 60% of newly launched liquid detergent formulations worldwide, spanning more than 1,200 product lines. Its performance as both a pH adjuster and foam enhancer has reinforced its dominance over alternative neutralizing agents. In late 2024, India Glycols reported a surge in domestic ethanolamine shipments following hygiene mandates for public institutions, further consolidating MEA’s role in institutional cleaning chemistry. The convergence of CCUS expansion, detergent reformulation, regional capacity scaling, and corporate restructuring continues to redefine competitive positioning across the global monoethanolamine value chain.

Monoethanolamine Market Trends and Opportunities

Trend: Strategic Investment in High-Purity Monoethanolamine for CCUS Infrastructure

Monoethanolamine is reinforcing its role as the reference solvent for post-combustion carbon capture as CCUS projects move decisively from pilots to full-scale deployment. The current investment cycle is defined by Final Investment Decisions that require consistent, high-purity MEA to sustain absorber efficiency, limit solvent degradation, and control operating costs over multi-decade asset lives. According to updates tracked by the Global CCS Institute, capture capacity under construction reached a new high in 2025, with tens of millions of tonnes per annum scheduled to come online in the near term. MEA-based aqueous systems continue to anchor the amine solvent mix because of their proven CO₂ affinity, predictable kinetics, and bankability in project finance models.

National decarbonization strategies are reinforcing demand visibility. In India, CCUS has been identified as the most economically viable pathway for decarbonizing hard-to-abate steel assets, with long-term roadmaps calling for demonstration projects before 2030 and full retrofits thereafter. These programs explicitly reference MEA as a baseline solvent for blast furnace flue gas capture due to its availability and operational familiarity. At the technology level, 2025 pilot programs integrating iron oxide nanoparticles into MEA solutions are gaining traction. These enhancements aim to accelerate absorption and desorption cycles and reduce the reboiler energy penalty, directly improving levelized capture costs. As megaton-scale plants standardize solvent specifications, suppliers capable of delivering low-impurity, oxidation-resistant MEA at scale are becoming strategic partners rather than commodity vendors.

Trend: Formulation Shift in Agrochemicals Toward MEA-Based Herbicide Salts

In agrochemicals, MEA is displacing traditional neutralizing agents as manufacturers seek higher loading efficiency, improved stability, and safer handling profiles. MEA-based salts of systemic herbicides such as glyphosate and 2,4-D are increasingly preferred because they enable concentrated formulations at 480 g/L and above without excessive viscosity. This directly supports logistics efficiency and precision dosing in large-scale farming operations. Compared with isopropylamine salts, MEA formulations demonstrate superior thermal stability and reduced crystallization risk during storage and transport, which is critical in tropical and arid climates.

Regulatory and operational considerations further strengthen this trend. MEA’s lower volatility reduces inhalation risk for applicators and aligns with tightening occupational exposure expectations. Reformulated products using MEA-neutralized actives also show enhanced leaf-cuticle penetration and improved rainfastness, delivering more consistent field performance under variable weather conditions. Beyond crop protection, MEA is expanding into foliar nutrition as a complexing agent that improves micronutrient bioavailability. Research released in early 2025 highlights its role in reducing nutrient runoff while supporting precision agriculture objectives. This convergence of efficacy, safety, and environmental performance is positioning MEA as a multifunctional building block in next-generation agrochemical formulations.

Opportunity: MEA-Based Gas Treating for Renewable Hydrogen and Biogas

The acceleration of renewable hydrogen and biogas upgrading is opening a structurally attractive opportunity for MEA-based gas treating systems. Decentralized amine scrubbing units are emerging as cost-effective solutions for removing CO₂ and H₂S from raw biogas and biomass-derived syngas. Technical evaluations in 2024 and 2025 confirm that 30% aqueous MEA solutions can upgrade biogas streams containing 35 to 40% CO₂ to pipeline-grade biomethane with methane purity approaching 98%. This performance is particularly compelling for small and mid-scale digesters where membranes or cryogenic separation remain capital intensive.

The shift toward carbon utilization further amplifies this opportunity. Commercial deployments of methane pyrolysis platforms such as those developed by Levidian are relying on upstream amine treatment to condition feed gas before conversion to clean hydrogen and solid carbon products. In parallel, policy drivers under the European Union Renewable Energy Directive are stimulating decentralized biogas hubs across Northern Europe. Pilot projects in Denmark and Germany are testing water-lean MEA systems blended with glycols to cut reboiler energy demand by up to 30%. These advances position MEA as a cornerstone solvent in modular, resilient green gas infrastructure.

Opportunity: Multi-Functional Additives for Green Construction Chemicals

MEA is gaining renewed relevance in construction chemicals as sustainability metrics become embedded in building codes and procurement standards. In cement manufacturing, MEA-based alcohol-amine formulations act as grinding aids that reduce particle agglomeration during milling, improving energy efficiency in one of the world’s most energy-intensive industrial processes. Studies published during 2024 and 2025 demonstrate that these additives can increase early compressive strength while lowering specific energy consumption, directly supporting lower clinker intensity and reduced CO₂ emissions.

Beyond grinding, MEA delivers corrosion inhibition benefits in reinforced concrete. By forming a hydrophobic passive layer on steel rebar, MEA-based inhibitors slow chloride-induced corrosion, extending the service life of bridges, marine structures, and coastal infrastructure. This dual functionality aligns strongly with LEED and BREEAM certification pathways, where durability and embodied carbon reduction are evaluated together. Importantly, MEA enables higher substitution rates of slag and fly ash without compromising mechanical performance, supporting the cement industry’s 2025 and beyond targets for lowering emissions per tonne. As green construction shifts from niche to mainstream, MEA’s versatility across energy reduction, durability, and sustainability positions it as a high-value additive rather than a commodity input.

Monoethanolamine Market Share and Segmentation Insights

Monoethanolamine Dominates the Monoethanolamine Market Due to Versatile Chemical Reactivity and Industrial Applications

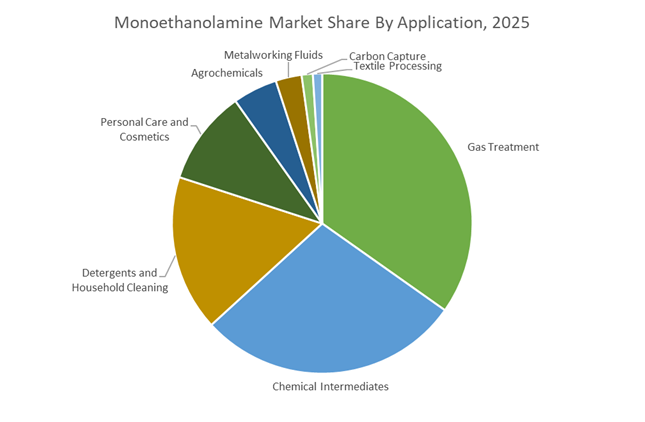

Monoethanolamine (MEA) accounted for 48.60% of the Monoethanolamine Market share in 2025, establishing it as the most widely used ethanolamine across multiple industrial sectors. MEA is a primary amine compound with high chemical reactivity, making it a critical raw material in several industrial processes including natural gas sweetening, chemical synthesis, surfactant manufacturing, agrochemical production, and metalworking fluid formulations. In gas processing facilities, MEA is extensively used to remove acid gases such as hydrogen sulfide (H₂S) and carbon dioxide (CO₂) from natural gas streams, ensuring that processed gas meets pipeline quality standards. The compound also serves as a key intermediate in the production of ethoxylated surfactants, corrosion inhibitors, and emulsifiers used across detergent and personal care industries. In 2025, the rapid expansion of carbon capture and storage (CCS) technologies has significantly strengthened demand for monoethanolamine. MEA-based solvent systems are widely used in post-combustion CO₂ capture processes, where the solvent selectively absorbs carbon dioxide from flue gas streams, positioning MEA as a benchmark solvent for industrial carbon capture systems.

Gas Treatment Sector Drives the Largest Demand for Monoethanolamine

Gas treatment accounted for 34.80% of the Monoethanolamine Market share in 2025, making it the largest application segment for ethanolamine-based solvents. Gas treatment processes are widely used in natural gas processing plants, petroleum refineries, ammonia production facilities, and syngas purification systems, where acid gas removal is essential to meet environmental regulations and product purity specifications. Ethanolamine-based solvents such as MEA and DEA are highly effective at absorbing carbon dioxide and hydrogen sulfide from hydrocarbon gas streams, allowing operators to produce pipeline-quality natural gas and prevent corrosion in downstream processing infrastructure. The global expansion of natural gas production, liquefied natural gas (LNG) facilities, and petrochemical processing capacity continues to sustain strong demand for gas treatment chemicals. In 2025, process optimization has become a major focus for gas processors seeking to reduce operational costs. Facilities are implementing advanced amine circulation control, heat integration systems, and optimized solvent blends that improve acid gas removal efficiency while lowering energy consumption required for solvent regeneration in gas sweetening units.

Monoethanolamine Market Competitive Landscape

The monoethanolamine (MEA) market in 2026 is driven by high-purity grades, CCUS applications, and amine stability optimization. Competitive advantage centers on integrated EO-ammonia value chains, low-nitrosamine formulations, and bulk logistics systems supporting gas treatment, agrochemicals, and pharmaceutical-grade MEA demand.

BASF strengthens high-purity MEA leadership through Verbund integration and strategic distribution partnerships

BASF SE is leveraging its Verbund integration to deliver high-purity monoethanolamine at industrial scale while optimizing cost efficiency and supply reliability. Its partnership with OQEMA enhances distribution reach across the UK, targeting cleaning, industrial treatment, and specialty chemical markets. With €59.7 billion in 2025 sales, BASF is focusing on agrochemical applications where MEA acts as a key solubilizing agent in herbicide formulations. The company’s production hubs in Ludwigshafen and Zhanjiang enable resource-efficient manufacturing aligned with EU decarbonization mandates. BASF is also strengthening its position in ethylene amines and ion exchange resins, reinforcing its role across downstream MEA derivatives. Its strategy prioritizes carbon intensity reduction and high-value specialty applications.

Dow drives MEA pricing power and feedstock security through ethylene integration and operational simplification

Dow Inc. maintains its role as a global price setter in the monoethanolamine market, supported by its “Transform to Outperform” strategy targeting $2 billion EBITDA improvement. The company implemented MEA price increases in 2025 to offset raw material volatility, reinforcing margin stability across detergents and cement additives. With $40 billion in annual sales, Dow focuses on performance materials, coatings, and gas treatment applications where MEA serves as a corrosion inhibitor and pH regulator. Its expanded ethylene supply agreement with MEGlobal ensures feedstock security, mitigating upstream risks in ethanolamine production. Dow’s integrated supply chain and operational simplification enhance resilience in volatile market conditions. Its scale and pricing discipline position it as a key global benchmark player.

SABIC leverages energy integration to dominate bulk MEA supply for oilfield chemicals and surfactants

SABIC is capitalizing on its integration with Saudi Aramco to provide cost-advantaged, high-volume monoethanolamine solutions. Its MEA 99 grade supports the production of ethylene diamine, taurine, and specialty chemicals used in pulp processing and dyestuffs. The company is a major supplier to oilfield chemical markets, where MEA is essential for H₂S removal and drilling fluid bactericides. SABIC’s logistics infrastructure, including pipeline and ISO-tank delivery, enables efficient servicing of large-scale refineries and gas processing plants. The company is also expanding into personal care surfactants such as coco monoethanolamide for shampoos and cosmetics. Its vertically integrated model ensures supply stability and cost competitiveness across global markets.

INEOS expands MEA capacity and positions for carbon capture growth through acquisitions and energy investments

INEOS Group is strengthening its monoethanolamine market position through strategic acquisitions and infrastructure investments. The integration of Eastman’s Texas City site has expanded its production capacity and customer base in North America. INEOS is implementing cost-reflective pricing strategies while investing £150 million in its Grangemouth site to enhance sustainability and operational efficiency. The company is actively advocating for large-scale carbon capture infrastructure, positioning its amine technologies for EU decarbonization targets exceeding 50 million tonnes of CO₂ capture annually. Despite energy cost pressures in Europe, INEOS maintains strong operational resilience. Its focus on CCUS and integrated chemical production reinforces its long-term competitiveness.

Huntsman accelerates specialty MEA innovation for pharmaceuticals and carbon capture applications

Huntsman Corporation is transitioning toward high-margin specialty monoethanolamine applications, particularly in pharmaceuticals and environmental solutions. With over 60 global manufacturing and R&D facilities and approximately $6 billion in revenue, Huntsman is a key supplier of high-purity MEA for API synthesis and buffering systems. The company is advancing amine-based carbon capture technologies that significantly reduce industrial CO₂ emissions. Its focus on differentiated “Effect Chemicals” supports applications in cement additives, metalworking fluids, and advanced gas treatment. Huntsman’s R&D-driven approach enhances performance and regulatory compliance in high-growth sectors. Its strategy emphasizes specialty innovation over commodity volume.

Nippon Shokubai advances integrated EO-based MEA production for green chemicals and hydrogen supply chains

Nippon Shokubai Co., Ltd. is leveraging its vertically integrated ethylene oxide value chain to ensure stable, high-quality monoethanolamine production. Its Osaka operations enable precise process control, supporting applications in superabsorbent polymers and fine chemicals. The company is expanding into green chemistry through bio-based monomers and advanced absorbent materials showcased in 2026. Its collaboration with Mitsubishi Heavy Industries on ammonia cracking systems positions it within the emerging hydrogen supply chain, where amines play a key role in gas separation. Nippon Shokubai’s sustainability initiatives, including biodegradable materials and low-carbon ammonia, align with global decarbonization trends. Its diversification into future materials strengthens its competitive positioning.

United States: Decarbonized Production, Semiconductor-Grade Purity, and Carbon Capture Scale-Up

The United States monoethanolamine market is undergoing a structural shift driven by decarbonization commitments, reshoring of high-purity chemicals, and renewed investment in carbon capture infrastructure. In September 2025, BASF confirmed that its standard grade ethanolamine portfolio at the Geismar, Louisiana Verbund site would transition to production supported by 100% renewable electricity credits starting Q4 2025. This initiative is designed to lower the product carbon footprint of MEA by an average of 4.5% through 2026, a material differentiator for customers in gas treating, detergents, and industrial cleaning who are increasingly tracking Scope 3 emissions. Parallel to sustainability-led upgrades, Huntsman Corporation expanded its U.S. footprint with a new E-GRADE® unit in Texas during late 2025, targeting semiconductor and electronics customers that require ultra-high-purity ethanolamines for wafer processing and advanced packaging, a segment closely aligned with 2026 reshoring priorities.

Pricing and regulatory compliance continue to shape commercial strategy. Dow Chemical implemented a USD 0.05 per pound price increase on all MEA grades in February 2025, reflecting higher production costs and resilient demand from agriculture and gas sweetening applications. On the regulatory front, tightening requirements under the Toxic Substances Control Act are pushing U.S. manufacturers to invest in closed-loop containment and vapor recovery systems ahead of 2026 VOC reduction mandates for industrial formulations. At the same time, funding priorities from the U.S. Department of Energy are reinforcing MEA’s strategic role as the benchmark solvent in post-combustion carbon capture pilots along the Gulf Coast, where aqueous MEA systems remain central to large-scale CO₂ sequestration programs.

Germany: Capacity Expansion, Distribution Reach, and Energy-Efficient Regeneration

Germany’s monoethanolamine market is characterized by capacity-led scale, regulatory alignment, and process innovation aimed at lowering lifecycle energy intensity. In 2025, BASF commissioned a new alkyl ethanolamines plant at its Antwerp Verbund site, lifting global ethanolamine derivative capacity by nearly 30% to more than 140,000 metric tons annually. This expansion strengthens supply security for MEA across Western Europe, particularly for specialty chemicals, personal care, and gas treating customers that require consistent quality and short lead times. Complementing this capacity build, BASF’s distribution partnership with OQEMA AG was broadened through 2024–2025, improving logistics coverage for high-purity MEA in Germany and neighboring markets.

Regulatory and R&D dynamics further differentiate the German landscape. Manufacturers are reformulating MEA-based detergents to comply with the European Chemicals Agency microplastic-related reporting and discharge expectations for 2025–2026, ensuring that MEA used as an emulsifier does not contribute to persistent environmental residues. Under BASF’s updated “Winning Ways” strategy, approximately EUR 2 billion per year is allocated to R&D, with more than 80% directed toward sustainable processes. A priority area is energy-efficient MEA regeneration in gas treating units, a critical lever for lowering operating costs and emissions in acid gas removal systems used across Europe’s refining and chemical sectors.

China: EO Feedstock Scale, Polymer Dispersant Innovation, and Agrochemical Demand

China continues to consolidate its position as a leading producer and exporter of technical-grade monoethanolamine, underpinned by rapid upstream expansion in ethylene oxide capacity. Between 2024 and 2025, national MEA output volumes increased by more than 8%, directly linked to large-scale EO additions that improved feedstock availability and cost competitiveness. In November 2025, BASF commissioned a high-performance production line in Nanjing’s Jiangbei New Material Technology Park, applying Controlled Free Radical Polymerization to manufacture MEA-derived dispersants. This investment enhances formulation flexibility for coatings, construction chemicals, and water treatment applications heading into 2026.

State-led modernization is reinforcing sustainability objectives. The PetroChina Jilin Petrochemical upgrading program in 2025 integrated advanced energy-saving technologies into ethanolamine units, reducing the carbon intensity of bulk MEA production. On the demand side, domestic consumption of MEA for agrochemical synthesis rose by 6.8% in late 2025, driven by national food security policies that favor organophosphate pesticide production. This combination of feedstock scale, process efficiency, and agricultural demand anchors China’s role as a global reference point for cost-competitive MEA supply.

Saudi Arabia: Supply Disruption, Circular Feedstocks, and CCS-Led Demand

Saudi Arabia’s monoethanolamine market is shaped by its dual role as a critical supplier and an emerging center for carbon capture infrastructure. In July 2025, Dow Chemical declared force majeure on ethanolamines from its Al-Jubail complex following an unplanned mixed-feed cracker outage. The disruption extended through Q3 2025, tightening global MEA availability and highlighting the strategic importance of Middle Eastern supply reliability. In parallel, SABIC integrated its TRUCIRCLE™ circular solutions portfolio with ethanolamine production, offering certified circular MEA derived from plastic waste to meet rising European demand for sustainable personal care and detergent intermediates.

Longer term, Saudi Arabia is positioning itself as a carbon capture and storage hub. According to the Global CCS Institute report released in October 2025, the Kingdom is expected to play a central role in global CCS deployment. This outlook is driving investment in MEA-based gas sweetening and CO₂ capture systems across NEOM and Jubail industrial zones, reinforcing steady regional demand for high-volume aqueous MEA solutions.

India: Indigenous CCS Innovation, Feedstock Volatility, and Personal Care Growth

India’s monoethanolamine market is increasingly influenced by domestic innovation and end-use diversification. In 2025, the Indian Institute of Technology Guwahati, in collaboration with NTPC Limited, developed an advanced amine-based CO₂ capture technology that reduces energy consumption by 31% compared with conventional aqueous MEA systems. This breakthrough strengthens India’s position in localized CCS solutions for power generation and industrial emitters. However, feedstock sensitivity remains a constraint. A 7% rise in domestic ethylene oxide prices during Q1 2025 translated directly into higher MEA prices, prompting agrochemical manufacturers to optimize formulations and adopt more efficient MEA blends.

Beyond industrial uses, personal care is emerging as a structurally important outlet. Demand for MEA as a pH adjuster and emulsifier grew by 9% in 2025, reflecting rapid urbanization and consumption growth in Tier-2 and Tier-3 cities. This shift is encouraging domestic producers and importers to focus on cosmetic-grade consistency and regulatory compliance, supporting steady downstream demand through 2026.

Comparative Snapshot: Country-Level Dynamics in the Monoethanolamine Market

Monoethanolamine Market County Level Snapshot

|

Country / Region

|

Strategic Driver

|

Industrial Focus

|

Technology or Policy Lever

|

Market Implication

|

|

United States

|

Decarbonization, CCS funding

|

Gas treating, semiconductors

|

Renewable power, closed-loop systems

|

Premium, low-PCF MEA positioning

|

|

Germany

|

Capacity scale, sustainability

|

Specialty chemicals, detergents

|

Energy-efficient regeneration

|

Stable high-purity supply

|

|

China

|

EO feedstock expansion

|

Agrochemicals, dispersants

|

Polymerization innovation

|

Cost-competitive exports

|

|

Saudi Arabia

|

CCS hub development

|

Gas sweetening

|

Circular MEA, large-scale CCS

|

Strategic global supply role

|

|

India

|

Indigenous CCS R&D, urban demand

|

Power, personal care

|

Energy-efficient capture

|

Diversified end-use growth

|

Monoethanolamine Market Report Scope

Monoethanolamine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.1 Billion

|

|

Market Size (2034)

|

$9.9 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Monoethanolamine, Diethanolamine, Triethanolamine), By Application (Gas Treatment, Agrochemicals, Detergents and Household Cleaning, Personal Care and Cosmetics, Chemical Intermediates, Textile Processing, Metalworking Fluids, Carbon Capture), By End-User Industry (Oil and Gas, Agriculture, Pharmaceuticals, Cosmetics and Personal Care, Construction, Textiles), By Distribution Channel (Direct Sales, Specialty Formulators and Distributors)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Huntsman, SABIC, INEOS Oxide, Nouryon, LyondellBasell Industries, Sinopec, Oriental Union Chemical, Thai Ethanolamines, Sintez OKA, Indorama Ventures, Celanese, KCC, Sadara Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Monoethanolamine Market Segmentation

By Product Type

- Monoethanolamine

- Diethanolamine

- Triethanolamine

By Application

- Gas Treatment

- Agrochemicals

- Detergents and Household Cleaning

- Personal Care and Cosmetics

- Chemical Intermediates

- Textile Processing

- Metalworking Fluids

- Carbon Capture

By End-User Industry

- Oil and Gas

- Agriculture

- Pharmaceuticals

- Cosmetics and Personal Care

- Construction

- Textiles

By Distribution Channel

- Direct Sales

- Specialty Formulators and Distributors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Monoethanolamine Market

- BASF

- Dow

- Huntsman

- SABIC

- INEOS Oxide

- Nouryon

- LyondellBasell Industries

- Sinopec

- Oriental Union Chemical

- Thai Ethanolamines

- Sintez OKA

- Indorama Ventures

- Celanese

- KCC

- Sadara Chemical

- *- List not Exhaustive