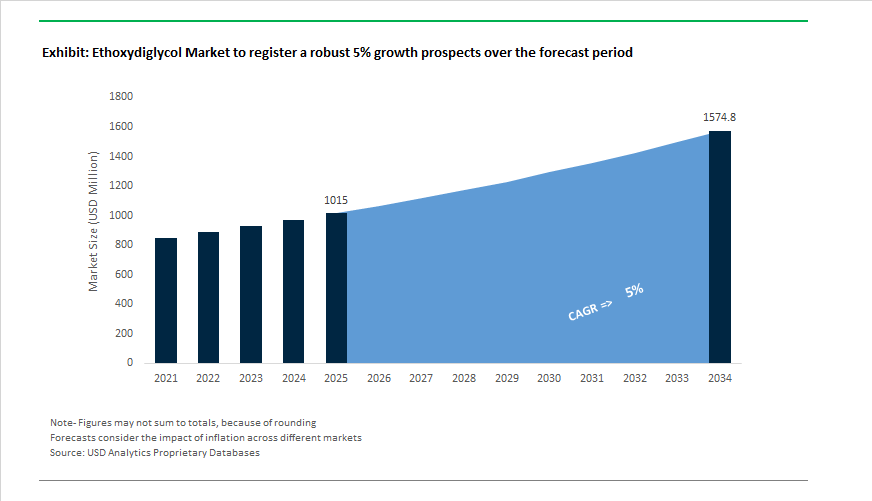

Ethoxydiglycol Market to Reach $1,574.6 Million by 2034 as Cosmetic Solvency Demand and Bio-Based Feedstocks Reshape Supply

The Ethoxydiglycol Market is projected to grow from $1,015 Million in 2025 to $1,574.6 Million by 2034, registering a CAGR of 5%, supported by expanding personal care formulations, pharmaceutical solvent applications, and a structural shift toward bio-based glycol derivatives. However, 2025 exposed the fragility of the supply chain. In September 2025, a severe shortage of cosmetic-grade ethoxydiglycol disrupted the European self-tanning industry, directly affecting brands such as St. Tropez and Bondi Sands. Major suppliers including BASF, INEOS, and LyondellBasell reported depleted inventories in the UK and broader EU markets. The shortage was driven by upstream ethylene oxide tightness, unplanned maintenance cycles, and surging demand for high-solvency carriers in hybrid skincare products containing retinoids and exfoliating acids.

India is emerging as a strategic export base. India Glycols Limited confirmed commissioning of Phase II expansion at its Kashipur facility by Q2 FY25, adding approximately 5,000 MT/year of specialty chemicals capacity including glycol ethers and ethoxylates. This strengthens India’s positioning as a competitive hub for cosmetic- and pharma-grade ethoxydiglycol exports into Europe and Southeast Asia. Regulatory calibration is also underway: India’s Ministry of Chemicals and Fertilizers extended enforcement timelines for Quality Control Orders (QCO) on ethylene derivatives to September 12, 2026, granting manufacturers additional time to secure BIS certification. These regulatory adjustments are reshaping import flows and encouraging domestic value addition, particularly for high-purity grades used in dermatological formulations.

Sustainability is redefining upstream economics. In October 2025, Sustainea—a joint venture between Braskem and Sojitz—announced a $400 million investment to construct a bio-MEG plant in Lafayette, U.S. This project provides renewable monoethylene glycol feedstock essential for next-generation bio-based ethoxydiglycol. Complementing this, Technip Energies partnered with Shell Catalysts & Technologies in 2024 to commercialize Bio-2-Glycols technology derived from glucose. These developments enable consumer brands to transition toward fossil-independent solvent systems, aligning with 2026 sustainability mandates in Europe and North America. Meanwhile, INOVYN expanded ethylene oxide derivative capacity in 2025 to mitigate European supply bottlenecks, reinforcing feedstock security for glycol ether production.

Application diversification is accelerating demand beyond cosmetics. Dow introduced an optimized ethoxydiglycol grade in 2024 designed to enhance solubility and stability in complex skin and hair care systems, enabling higher active loading without destabilization. In pharmaceuticals, Aurigene Pharmaceutical Services launched its Aurigene.AI drug discovery platform, indirectly boosting demand for high-purity solvent systems used in transdermal and topical delivery research. Simultaneously, Hexion pivoted toward specialty derivatives targeting technical-grade applications such as offset printing cleaners and wood preservatives. On the supply side, China’s 2026 anti-overcapacity policies are expected to curtail 5–10% of smaller glycol ether operations, consolidating market share among integrated producers like Sinopec and BASF-YPC. BASF’s 800,000-ton ethylene glycol plant in China, stabilized through 2025–2026, further secures upstream reliability for Asia-Pacific customers.

Trends and Opportunities in the Ethoxydiglycol Market

Strategic Substitution and Regulatory Reassessment in Consumer Formulations

- Regulatory agencies are intensifying oversight of glycol ethers due to concerns around volatility, occupational exposure, and environmental impact. This has triggered a structural reassessment of ethoxydiglycol usage in consumer-facing and aerosolized formulations.

- As of January 17, 2025, U.S. Environmental Protection Agency finalized amendments to the National Volatile Organic Compound Emission Standards for Aerosol Coatings. These revisions introduced tighter reactivity thresholds and expanded reporting obligations for chemical manufacturers operating under NAICS 32551 and 325998. Traditional glycol ethers, including diethylene glycol diethyl ether, are increasingly challenged in retail aerosol applications where compliance costs and formulation risk have risen sharply.

- Regional air quality mandates have further accelerated substitution. In October 2025, South Coast Air Quality Management District strengthened Rule 1173 by reducing allowable fugitive emission thresholds from 50,000 ppm to 10,000 ppm. This 80% tightening has forced producers to reassess solvent volatility profiles, prompting a gradual shift toward higher molecular weight or lower vapor pressure alternatives such as dipropylene glycol methyl ether in facilities operating in high-compliance regions.

- From a commercial standpoint, these regulatory pressures have translated into higher operating and monitoring costs. In response, Dow implemented portfolio-wide price adjustments across its glycol ether offerings in August 2025. The move reflects a broader industry strategy to preserve margins while funding enhanced environmental controls, leak detection systems, and compliance documentation.

Consolidation and Niche Specialization in High-Purity Ethoxydiglycol Production

- Parallel to regulatory-driven substitution, the ethoxydiglycol market is consolidating around high-purity production, with pharmaceutical and electronics applications absorbing a disproportionate share of value.

- In 2025, demand for pharmaceutical-grade ethoxydiglycol, commonly marketed as Transcutol®, expanded rapidly due to its proven role as a dermal penetration enhancer and intracutaneous depot solvent. At purities exceeding 99.9 %, ethoxydiglycol enables the solubilization of poorly water-soluble active pharmaceutical ingredients while minimizing systemic toxicity. This functionality has positioned it as a preferred excipient in advanced topical, transdermal, and controlled-release drug delivery systems.

- To support this demand, leading suppliers are investing in multi-stage fractional distillation and precision purification technologies. Industry disclosures from February 2025 indicate that high-purity ethoxydiglycol now accounts for more than 75% of specialty solvent revenue in regulated Western markets, as technical-grade volumes face displacement due to quality, traceability, and documentation gaps.

- At the supply chain level, production is becoming increasingly concentrated among a limited number of technically capable manufacturers. This consolidation is strategically important given the regulatory status of ethylene oxide, the primary precursor, which remains classified as a high-priority air toxic. Control over EO sourcing, purification, and handling has become a competitive moat in the ethoxydiglycol market.

Critical Co-Solvent Role in Low-VOC Industrial Maintenance Coatings

- Despite the global shift toward waterborne and low-VOC coating systems, ethoxydiglycol continues to play a critical enabling role in high-performance industrial maintenance coatings where durability cannot be compromised.

- In January 2025, Dow received multiple BIG Innovation Awards for its next-generation coalescing agents, including the Dalpad™ A Plus series. These formulations illustrate how glycol-based derivatives are being re-engineered to cut semi-volatile organic compound emissions by more than 60% while preserving film integrity, adhesion, and corrosion resistance. Ethoxydiglycol remains a key reference solvent in these systems due to its high water solubility and controlled evaporation profile.

- Infrastructure-driven demand reinforces this opportunity. A 5.3% increase in U.S. architectural coating value in mid-2024 highlighted renewed investment in durable infrastructure assets. In waterborne industrial maintenance coatings, ethoxydiglycol enables smooth film formation under high humidity or low-temperature conditions, reducing defects such as blistering and poor coalescence.

- In aerospace and marine environments, where coatings are expected to deliver multi-year corrosion protection, ethoxydiglycol is increasingly deployed in hybrid solvent systems. These blends combine the environmental advantages of water-based chemistries with the performance resilience traditionally associated with solventborne formulations.

Selective Penetration Enhancement in Advanced Agrochemical Adjuvants

- The agrochemical sector presents a structurally attractive opportunity for ethoxydiglycol as regulators push for reduced pesticide volumes and higher application efficiency.

- A 2024–2025 study published in Frontiers in Agronomy demonstrated that advanced adjuvant systems, including refined glycol ethers, can boost active ingredient efficacy by up to 50%. This allows for meaningful reductions in application rates while maintaining weed and pest control performance, directly aligning with the European Green Deal objective of cutting total pesticide use by half by 2030.

- Formulation innovation is accelerating in emerging markets as well. In November 2025, UPL and Insecticides India Limited launched a new generation of dual-action herbicides, including products such as Altair and Centurion EZ. These formulations depend on solvent systems that deliver rapid cuticular penetration, rainfastness, and consistent field performance. Ethoxydiglycol’s unique solubility and penetration-enhancing properties give it a defensible niche over conventional surfactants in these precision agriculture applications.

Competitive Landscape of the Ethoxydiglycol Market

The Ethoxydiglycol market is characterized by a dual structure: premium pharmaceutical-grade suppliers competing on purity, regulatory compliance, and dermal delivery science, and integrated petrochemical majors leveraging ethylene oxide capacity for industrial solvent leadership across coatings, brake fluids, and cleaning formulations.

Gattefossé sets the global purity benchmark with Transcutol® in pharma and dermal delivery

Gattefosse is widely regarded as the premium reference in ethoxydiglycol, marketed under the iconic Transcutol® brand. Its Transcutol® CG (Cosmetic Grade) and Transcutol® P (Pharmaceutical Grade) are extensively cited in dermatological and transdermal research for skin-penetration enhancement. In late 2025, the company expanded its clinical dossier for Transcutol® P, validating its solubilization of poorly water-soluble New Chemical Entities in topical drug delivery. With purity exceeding 99.5% and ultra-low ethylene glycol and diethylene glycol impurities, Gattefossé is the preferred partner for regulated global brands. Its strategic focus on efficacy boosting enables formulators to reduce active ingredient loadings while improving bioavailability.

Dow leverages ethylene oxide scale to dominate industrial and low-VOC glycol ether supply

Dow Inc. is a global heavyweight in glycol ethers, utilizing deep integration into ethylene and ethylene oxide to secure cost leadership in ethoxydiglycol production. Its CARBITOL™ Low Gravity solvent is widely used in wood stains, textile dyeing, and printing inks. In 2025, Dow optimized its Louisiana and Texas assets to increase output of low-VOC glycol ethers, aligning with 2026 sustainability mandates for greener industrial solvents. By early 2026, 89% of Dow’s R&D portfolio was aligned with sustainability goals, including bio-attributed feedstocks. Backward integration shields its ethoxydiglycol supply chain from the feedstock volatility experienced during 2024–2025, reinforcing merchant market stability.

Clariant advances high-margin healthcare solvents through VitiPure® and green ethoxylates

Clariant positions ethoxydiglycol within its Industrial and Consumer Specialties portfolio, focusing on coupling-agent performance in household and industrial cleaning formulations. Under its “Winning Ways” strategy confirmed in February 2026, Clariant prioritizes high-margin Health Care and Personal Care segments. The VitiPure® excipient line, launched in 2024–2025, includes high-purity ether derivatives optimized for stable, colorless parenteral formulations. Its Clariant IGL Specialty Chemicals joint venture has emerged as a leader in green ethoxylates in India, strengthening APAC solvent supply chains. By integrating sustainability with pharmaceutical-grade purity, Clariant reinforces its role in regulated solvent markets.

INEOS controls transatlantic ethoxydiglycol bulk trade through alkoxylation scale

INEOS Group, via its INEOS Oxide division, operates one of the world’s largest alkoxylation capacities, positioning it as a dominant ethylene oxide derivative producer. In 2026, its subsidiary INOVYN expanded specialty chemical capacity to support automotive and electronics solvent demand. Ethoxydiglycol plays a critical role in high-performance brake fluids and hydraulic systems, particularly in advanced automotive platforms. During 2025–2026, INEOS accelerated hydrogen integration initiatives, utilizing hydrogen byproducts to power energy-intensive distillation for high-purity glycol ethers. With production hubs in Antwerp and the US Gulf Coast, INEOS maintains logistical dominance in bulk ethoxydiglycol trade across Europe and North America.

BASF strengthens carbon transparency and care chemical integration in ethoxydiglycol

BASF SE leverages its Verbund integration to deliver energy-efficient ethoxydiglycol with full carbon traceability. Reporting €59.7 billion in 2025 sales, BASF targets EBITDA expansion toward €10–12 billion by 2028, with Nutrition and Care as a core growth pillar. In 2026, BASF introduced Product Carbon Footprint transparency across its glycol ether portfolio, offering precise CO2 data per kilogram sold. Its “Winning Ways” strategy reinforces European BDO and EO value chain security, ensuring solvent supply reliability. BASF’s high-purity grades support spandex and synthetic fiber manufacturing, where ethoxydiglycol functions as a viscosity modifier and processing aid in advanced textile production.

Ethoxydiglycol Market Share and Segmentation Insights

Cosmetic Grade Ethoxydiglycol Leads Formulation Demand Across Premium Personal Care Products

Cosmetic grade ethoxydiglycol accounts for 52% of total market share in 2025, driven by its widespread adoption in skin care, hair care, and color cosmetics. Its exceptional solvency for both polar and non-polar ingredients, low odor profile, and skin-friendly nature make it a preferred solvent, coupling agent, and penetration enhancer in high-performance personal care formulations. Global beauty brands increasingly rely on cosmetic grade ethoxydiglycol to improve active ingredient delivery, texture uniformity, and product stability in moisturizers, serums, conditioners, and makeup. Industrial grade ethoxydiglycol holds a significant secondary share, serving coatings, industrial cleaners, and chemical intermediates where purity thresholds are lower but solvency efficiency remains critical. Pharmaceutical grade represents an important segment, supporting topical and transdermal drug delivery systems that require strict regulatory compliance, consistent purity, and reliable enhancement of active pharmaceutical ingredient absorption.

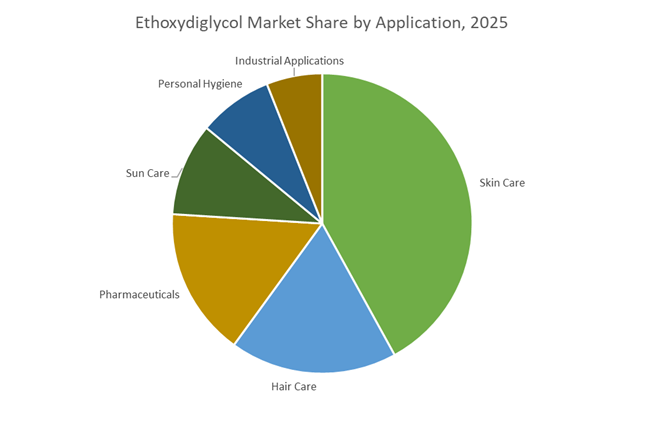

Skin Care Applications Anchor Consumption Supported by Expanding Pharmaceutical and Sun Care Use

Skin care represents 42% of global ethoxydiglycol demand in 2025, positioning it as the largest application segment. The ingredient is extensively used in anti-aging creams, cleansers, and serums to dissolve actives, enhance skin penetration, and improve sensory performance. Hair care follows as a significant segment, incorporating ethoxydiglycol into conditioners and treatments to support ingredient delivery to the scalp and hair shaft. Pharmaceutical applications maintain strong uptake in dermatological products such as antifungals, corticosteroids, and hormone therapies, where formulation stability and bioavailability are essential. Sun care is a fast-growing segment, leveraging ethoxydiglycol to solubilize organic UV filters and reduce greasy residue in sunscreen products. Personal hygiene maintains steady demand, while industrial applications remain niche, using ethoxydiglycol in inks, coatings, and specialty cleaning formulations.

China Ethoxydiglycol Market: EO Value Chain Expansion, GMP-Certified Polyglycols, and 56% Global Ethylene Capacity Growth

China dominates the global Ethoxydiglycol Market as the largest growth engine in the ethylene oxide (EO) value chain, transitioning from a net importer to a self-sufficient downstream derivatives powerhouse. In Nov 2025, Clariant inaugurated its upgraded multi-purpose EOD facility at Daya Bay, Huizhou, following a CHF 80 million investment, approximately $99 million. The site became the first in China to secure Drug GMP certification for specific polyglycols, positioning it as a strategic production base for high-purity healthcare-grade ethoxydiglycol used in drug delivery and cosmetic solubilization systems.

According to Bloomberg New Energy Finance data, China is expected to account for 56% of global net new ethylene capacity additions in 2026, ensuring stable, cost-competitive EO feedstock supply for domestic ethoxydiglycol manufacturers. China National Petroleum Corporation is accelerating its shift toward higher-value chemical production, including specialty solvent by-products and membrane materials. Meanwhile, the Ministry of Industry and Information Technology of China introduced 2025 mandates incentivizing low-VOC solvent production to meet Green Production targets. Demand is expanding rapidly in liquid laundry detergents and industrial cleaners, where technical-grade ethoxydiglycol functions as a coupling agent for complex surfactant systems, reinforcing China’s leadership across both bulk and specialty grades.

United States Ethoxydiglycol Market: USP-NF Grade Leadership, $ Cost Advantage, and Advanced Transdermal Systems

The United States Ethoxydiglycol Market is defined by high-purity USP-NF grade solvent production and innovation in advanced topical and transdermal drug delivery systems. In Sept 2025, Gattefossé inaugurated its first North American manufacturing facility in Lufkin, Texas, dedicated to pharmaceutical excipients and cosmetic-grade solvents. By March 2025, the facility achieved critical ISO certifications, ensuring compliance with stringent formulation standards required by U.S. pharma and prestige beauty brands.

R&D momentum intensified in Feb 2026 with adoption of Nanoemulfoam drug delivery systems, utilizing ethoxydiglycol to increase transdermal flux of active ingredients by up to 7.4x versus traditional foam carriers. A structural cost advantage stems from ethane-based EO production along the U.S. Gulf Coast, offering more competitive economics compared to naphtha-based European feedstocks. The Cosmetic Ingredient Review continues to affirm ethoxydiglycol safety in cosmetics at concentrations up to 80%, a materially higher threshold than EU limits. Domestic specialty chemical firms such as Hexion are increasingly developing ethoxydiglycol derivatives for high-growth electronics coatings and advanced industrial formulations, strengthening U.S. dominance in premium solvent applications.

India Ethoxydiglycol Market: ₹2.16 Lakh Crore PLI Boost and Regulatory Traceability Reform

India’s Ethoxydiglycol Market is expanding under the Make in India framework and Production Linked Incentive schemes that have catalyzed over ₹2.16 lakh crore, exceeding $26 billion, in realized investments by late 2025. Regulatory reform in July 2025 under the Ministry of Health and Family Welfare introduced the Cosmetics Amendment Rules 2025, mandating batch-wise raw material traceability, significantly tightening compliance standards for solvent suppliers including cosmetic-grade ethoxydiglycol producers.

Decentralized licensing empowers State Licensing Authorities to expedite approvals for specialty chemical units, reducing compliance cycle times. Rule 34(10) enables export labeling flexibility aligned with importing country regulations, strengthening India’s position as a global export hub for ethoxydiglycol-based formulations. Infrastructure support from the Gujarat Renewable Energy Ecosystem ensures access to green power for low-carbon chemical processing, a key requirement for multinational beauty brands. The convergence of regulatory modernization, export flexibility, and green manufacturing capacity positions India as a rapidly scaling specialty solvent production center within the global ethoxydiglycol market.

France Ethoxydiglycol Market: SCCS Regulation, Upcycling Innovation, and Haute Couture Formulation Science

France remains the innovation epicenter of the Ethoxydiglycol Market, particularly within luxury cosmetics and specialty solvent R&D. In Jan 2026, Gattefossé launched the Poseidon program, integrating sustainable water management across the lifecycle of its Transcutol ethoxydiglycol portfolio. French manufacturers are advancing upcycling initiatives, transforming by-products from perfume and food industries into sustainable carrier solvents for premium beauty applications.

Collaboration with CTIBiotech in 2025 resulted in the first Bioimpedance 3D bioprinted skin chip platform, enabling solvent penetration testing linked directly to human-equivalent data. Advanced 2026 formulation collections focus on stabilizing delicate oil-soluble bioactives within water-rich serums using ethoxydiglycol as a high-efficiency solubilizer. France also leads EU regulatory influence via the Scientific Committee on Consumer Safety, which restricts ethoxydiglycol to 2.6% in certain leave-on cosmetics and 10% in rinse-off products, shaping compliance standards across the European specialty solvent market.

South Korea Ethoxydiglycol Market: K-Beauty Penetration Science, K-REACH Updates, and Functional Cosmetic Growth

South Korea’s Ethoxydiglycol Market is driven by K-Beauty innovation focused on enhanced dermal delivery of high-potency actives such as Vitamin C and retinol. In Sept 2025, the Ministry of Food and Drug Safety issued Announcement No. 2025-63 updating Cosmetic Safety Standards, tightening nitrosamine and co-solvent limits. In Aug 2025, the Ministry of Employment and Labor revised MSDS requirements to align with 2024 K-REACH amendments, effective July 2026 for chemical mixtures containing ethoxydiglycol.

Functional cosmetics in South Korea increasingly employ ethoxydiglycol to achieve sub-micron emulsion systems that enhance absorption and deliver the signature glass-skin aesthetic. The upgraded Technical Center of Excellence in Shanghai, operated by Gattefossé, supports North Asian formulation customization, including Korean market-specific solvent systems. From July 2026 onward, all ethoxydiglycol-containing mixtures must update SDS Section 15 classifications under revised K-REACH rules, emphasizing environmental hazard categories. This regulatory sophistication, combined with formulation innovation, positions South Korea as a global leader in high-performance cosmetic solvent applications within the ethoxydiglycol market.

Ethoxydiglycol Market Report Scope

Ethoxylates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24 Billion

|

|

Market Size (2034)

|

$34.5 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Type (Alcohol Ethoxylates, Fatty Amine Ethoxylates, Fatty Acid Ethoxylates, Ethylenediamine Ethoxylates, Methyl Ester Ethoxylates, Castor Oil Ethoxylates), By End-Use Industry (Household and Personal Care, Agrochemicals, Oil and Gas, Pharmaceuticals and Biotechnology, Industrial and Institutional Cleaning, Textiles and Leather Processing), By Function (Emulsifiers and Dispersants, Wetting Agents, Foaming and Defoaming Agents, Solubilizers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Clariant AG, Huntsman International LLC, INEOS Oxide, SABIC, Sasol Limited, Nouryon, Evonik Industries AG, Shell Chemicals, Kao Corporation, Croda International Plc, India Glycols Limited, Stepan Company, Wilmar International Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethoxydiglycol Market Segmentation

By Type

- Cosmetic Grade

- Pharmaceutical Grade

- Industrial Grade

By Functionality

- Solubilizers and Co-Solvents

- Humectants and Skin-Conditioning Agents

- Penetration Enhancers

- Viscosity Modifiers

- Fragrance Fixatives

By Application

- Skin Care

- Hair Care

- Sun Care

- Pharmaceuticals

- Personal Hygiene

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethoxydiglycol Industry

- BASF SE

- Dow Inc.

- Huntsman Corporation

- Clariant AG

- Croda International Plc

- Eastman Chemical Company

- INEOS Oxide

- LyondellBasell Industries N.V.

- India Glycols Limited

- Arakawa Chemical Industries, Ltd.

- Givaudan SA

- Alzo International Inc.

- Guangdong KOMO Co., Ltd.

- Finetech Industry Limited

- Merck KGaA

*- List not Exhaustive