Exterior Architectural Coating Market Growth Anchored in Sustainable Facade Technologies, Latin America Expansion, and High-Durability Finishes

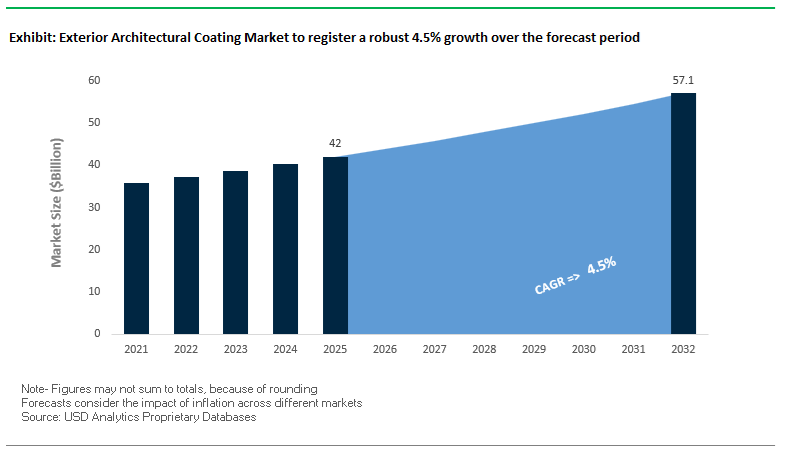

The global Exterior Architectural Coating Market reached a valuation of USD 42 billion in 2025 and is projected to expand at a CAGR of 4.5% between 2025 and 2032, reaching USD 57.2 billion by 2032. This growth is driven by the rising demand for high-performance exterior coatings that deliver weather resistance, UV stability, moisture protection, and long-term durability across residential, commercial, and infrastructure applications.

A key structural driver is the global emphasis on sustainable construction and energy-efficient building envelopes. Exterior coatings are increasingly being engineered not just for protection and aesthetics but also for functional performance, including heat reflection, thermal insulation, and even energy generation. The integration of coatings into green building strategies and decarbonization initiatives is accelerating the adoption of low-VOC, waterborne, and powder-based architectural coatings.

The market is also benefiting from the continued expansion of urban housing, renovation cycles, and infrastructure upgrades, particularly in emerging economies. Demand is rising for premium exterior finishes, including textured, metallic, and ultra-matte coatings that combine aesthetic appeal with long-term performance. Additionally, advancements in resin technologies and pigment systems are enabling coatings with enhanced resistance to harsh climates, pollution, and biological degradation, extending maintenance cycles and reducing lifecycle costs.

Mega Acquisitions, Solar-Active Coatings, and Low-Carbon Powder Innovations Reshape Market Dynamics

The exterior architectural coatings market is undergoing a strategic transformation driven by major acquisitions, sustainability-led innovation, and advanced material development. In April 2026, Sherwin-Williams announced the acquisition of BASF’s architectural paints business in Brazil, including the Suvinil brand, for $1.15 billion. This move significantly strengthens Sherwin-Williams’ position in Latin America’s high-growth exterior masonry and decorative coatings segment, enabling deeper penetration into residential and commercial markets.

Vertical integration strategies are also gaining momentum. In March 2025, Nippon Paint Holdings acquired AOC, LLC, enhancing its access to advanced resin technologies that are critical for high-durability exterior coatings. This acquisition aligns with Nippon’s “asset-assembly” strategy, aimed at strengthening supply chain control and accelerating innovation in architectural and industrial coatings.

Sustainability-driven innovation is redefining product development. In October 2025, AkzoNobel became the exclusive supplier for a solar-absorbing wall coating technology, transforming building exteriors into passive energy-generating surfaces. This represents a significant shift toward functional coatings that contribute to building energy efficiency and decarbonization goals. Further reinforcing this trend, in September 2025, AkzoNobel, Arkema, and BASF collaborated to develop low-carbon powder coatings, utilizing bio-based and mass-balance resins to reduce Scope 3 emissions while maintaining long-term durability.

Aesthetic and performance innovations are also shaping market differentiation. In April 2026, AkzoNobel launched its Futura Collection 2026–2029, featuring ultra-matte finishes and anodic-effect coatings that replicate anodized aluminum while offering superior weatherability. Similarly, in March 2026, Jotun announced a new bonded metallics facility in Malaysia, targeting high-end exterior finishes with enhanced UV and corrosion resistance, particularly suited for tropical climates.

Capacity expansion and localization strategies are further supporting market growth. In March 2025, PPG Industries inaugurated a waterborne coatings plant in Thailand, strengthening its ability to supply low-VOC exterior architectural coatings across Asia-Pacific. Additionally, PPG’s MOONWALK® automated paint mixing system, which reached its 3,000th installation in August 2025, is being adapted for architectural applications, enabling precision color matching and reducing material waste in large-scale exterior projects.

US GSA Buy Clean Initiative Driving Low-Carbon Exterior Architectural Coatings Adoption

The operationalization of the U.S. General Services Administration Buy Clean Initiative in 2026 is transforming procurement dynamics within the exterior architectural coatings market by embedding carbon accountability into federal purchasing decisions. Under this framework, all coatings specified for federally funded infrastructure projects must be supported by product-specific Environmental Product Declarations, ensuring transparent lifecycle assessment from raw material sourcing through manufacturing. This requirement is accelerating the adoption of low-VOC exterior coatings, waterborne formulations, and energy-efficient production technologies. The GSA’s Global Warming Potential benchmarks further require coatings to rank within the top 20% to 40% of low-carbon products, effectively excluding legacy solvent-based systems from high-value federal tenders. This shift is reinforcing demand for sustainable architectural coatings that meet stringent environmental compliance standards while maintaining performance durability. The policy aligns with the broader national objective of reducing greenhouse gas emissions by 50% to 52% by 2030, placing measurable pressure on coating manufacturers to decarbonize supply chains, optimize raw material selection, and enhance production efficiency. State-level adoption of similar frameworks in California, Colorado, and Washington is creating a harmonized regulatory landscape, where low-carbon coatings are becoming a baseline requirement across public infrastructure projects. This convergence is strengthening the market position of manufacturers offering environmentally compliant, high-performance exterior wall coatings with verified low embodied carbon profiles.

China GB/T 41649-2024 Elevating Weathering Resistance and Crack-Bridging Performance Standards

China’s GB/T 41649-2024 standard is redefining performance expectations for high-performance exterior architectural coatings across the Asia-Pacific construction sector. The updated regulation significantly raises durability benchmarks, particularly in terms of artificial weathering resistance, mechanical flexibility, and pollution resilience. Exterior wall coatings are now required to withstand a minimum of 3,500 hours of xenon arc weathering without exhibiting chalking, cracking, or blistering, representing a substantial increase over previous standards. This requirement is driving innovation in resin chemistry, pigment stabilization, and binder systems to enhance long-term UV resistance and structural integrity. Additionally, the mandated tensile elongation range of 200% to 300% is enabling coatings to accommodate substrate movement and thermal expansion, which is critical in high-density urban developments with varied climatic exposure. The introduction of stricter dirt-pickup resistance metrics is also influencing formulation strategies, with coatings required to maintain gloss retention and color stability above 90% following pollution exposure tests. These performance thresholds are directly impacting material selection and coating design, favoring advanced acrylics, elastomeric coatings, and hybrid systems with superior environmental resistance. With over 65% of municipal infrastructure projects in Tier 1 Chinese cities mandating compliance, GB/T 41649-2024 is acting as a catalyst for the widespread adoption of durable, weather-resistant exterior coatings tailored for long service life and reduced maintenance cycles.

Cool Wall Coatings Enhancing Urban Heat Island Mitigation and Energy Efficiency

The increasing intensity of urban heat island effects is driving demand for cool wall coatings that incorporate high solar reflectance and infrared-reflective pigments. These advanced exterior architectural coatings are designed to reduce heat absorption on building facades, thereby improving energy efficiency and occupant comfort. High Solar Reflectance Index coatings are capable of lowering surface temperatures by up to 20°C compared to conventional dark-colored finishes, significantly reducing thermal stress on building envelopes. In high-temperature climate zones, the adoption of cool wall technologies is delivering annual cooling energy savings ranging from 10% to 40%, with payback periods typically between three to five years based on current energy cost structures. These performance benefits are positioning cool coatings as a critical component of sustainable building design and energy-efficient construction strategies. Furthermore, large-scale deployment of reflective coatings across urban environments is projected to reduce ambient city temperatures by up to 2°C, contributing to climate resilience and reducing heat-related health risks. Certification frameworks such as LEED and WELL are reinforcing this trend by incentivizing coatings with Solar Reflectance Index values exceeding 64 for vertical applications, encouraging manufacturers to develop high-performance reflective coatings that meet both regulatory and environmental performance benchmarks.

Photocatalytic Self-Cleaning Exterior Coatings for Pollution Control and Maintenance Reduction

Photocatalytic exterior coatings incorporating titanium dioxide are emerging as a high-value innovation segment within the architectural coatings market, particularly for urban infrastructure and high-rise applications. These coatings leverage ultraviolet light to initiate catalytic reactions that decompose organic pollutants, enabling continuous surface cleaning and improved air quality. Advanced formulations introduced in 2026 demonstrate nitrogen oxide removal efficiencies of up to 45% in the immediate vicinity of coated surfaces, effectively transforming building exteriors into active pollution mitigation systems. This capability is particularly relevant in densely populated urban centers with high vehicular emissions and industrial pollution. In addition to air purification, these coatings significantly reduce maintenance requirements by preventing the accumulation of organic contaminants, algae, and fungi. Industry data indicates that self-cleaning coatings can decrease the frequency of pressure washing by 50% to 70%, resulting in substantial reductions in long-term operations and maintenance costs. The ability to decompose up to 99.9% of surface-borne volatile organic compounds and allergens further enhances their value proposition for commercial and public infrastructure projects. Adoption is accelerating across regions such as China, Japan, and the European Union, where municipal tenders increasingly specify photocatalytic coatings for applications including tunnels, transit systems, and high-rise facades to address urban pollution challenges and maintain structural aesthetics.

Exterior Architectural Coating Market Share by Product Type in 2025: Emulsion Paints Lead with Advanced Acrylic Durability

100% Acrylic Waterborne Emulsions Dominate Exterior Coatings with Long-Term Weather Protection

The exterior architectural coating market by product type in 2025 is led by emulsions, holding 48.00% market share, driven by the widespread adoption of 100% acrylic waterborne emulsion paints for superior exterior durability. These coatings deliver an optimal balance of weatherability, flexibility, breathability, and ease of application across diverse substrates including stucco, masonry, concrete, wood siding, and fiber cement. Unlike standard interior coatings, exterior acrylic emulsions are engineered with higher binder content, UV-resistant pigments, and advanced mildewcides, ensuring resistance to UV radiation, moisture intrusion, freeze-thaw cycles, and thermal expansion without cracking or peeling. A key growth driver within this segment is the rise of elastomeric wall coatings (EWC), high-build 100% acrylic formulations (10–20 mils DFT) designed for crack-bridging and waterproofing of concrete and EIFS systems. With 15–25 year warranties and lifetime performance claims, emulsion coatings remain the cornerstone of high-performance exterior paint systems globally.

Exterior Architectural Coating Market Share by Finish in 2025: Gloss Level Drives Performance, Aesthetics, and Application Decisions

Gloss and Sheen Selection Dominates with 64% Share, Balancing Durability and Modern Design Trends

The exterior architectural coatings market by finish in 2025 is dominated by gloss level finishes, accounting for 64.00% market share, as sheen selection directly impacts durability, aesthetics, and surface performance. Gloss hierarchy plays a critical role, where high-gloss and semi-gloss finishes offer superior washability, moisture resistance, and hardness, making them ideal for doors, trims, shutters, and high-touch exterior surfaces. Conversely, the prevailing trend for large wall surfaces is shifting toward satin and matte finishes, which provide a modern, low-reflectance aesthetic while effectively concealing substrate imperfections such as cracks and uneven textures. This is particularly valuable in renovation and repainting projects, which dominate coating demand globally. Advanced matte acrylic exterior coatings now deliver improved dirt pick-up resistance, mildew protection, and UV stability, bridging the gap between aesthetics and performance. The critical role of gloss in both visual outcome and substrate preparation requirements reinforces its dominance over niche finishes like textured and special effects coatings.

Exterior Architectural Coating Market Competitive Landscape Shaped by Sustainability, Smart Manufacturing, and High-Performance Finishes

The exterior architectural coating market is dominated by global leaders leveraging advanced formulations, sustainable coatings technologies, and digital integration. Competitive dynamics are driven by premium durable finishes, regional expansion in Asia-Pacific, smart manufacturing investments, and innovation in eco-friendly, energy-efficient architectural coatings.

Sherwin-Williams leads exterior coatings market with dominant distribution and premium durable finishes

The Sherwin-Williams Company maintains a commanding leading market share in the exterior architectural coating market, supported by its extensive network of over 5,000 company-operated stores and strong integration of Valspar® and European acquisitions. The company introduced "Universal Khaki" as the 2026 Coil and Extrusion Color of the Year, targeting high-performance aluminum substrates meeting AAMA 2605 standards. Financially, Sherwin-Williams projects adjusted diluted EPS of $11.50 to $11.90 in 2026, reflecting 5.4% growth in its architectural coatings segment amid macroeconomic uncertainty. Through its Linetec collaboration, the company launched Warm Mahogany (129211), aligning with modern, nature-inspired exterior design trends. Its strategic focus on premium coatings such as the BEHR DYNASTY line addresses growing demand for long-lasting, sustainable exterior finishes. This positioning reinforces leadership in high-performance architectural coatings and advanced façade solutions.

PPG Industries strengthens high-margin coatings portfolio through divestiture and digital integration

PPG Industries has strategically reshaped its portfolio by divesting its U.S. and Canadian architectural coatings business for $2 billion, enabling focus on higher-margin industrial and aerospace coatings while maintaining a 20–25% global share. The company is investing $300 million in advanced manufacturing, including a major Tennessee facility set to enhance supply for mobility and adjacent architectural markets. Strong double-digit growth in Asia, particularly in China, India, and Vietnam, is offsetting slower European demand, highlighting its geographic diversification strategy. PPG achieved 9% organic growth in its Performance Coatings segment, driven by demand for advanced exterior finishes in aviation and infrastructure. Its PPG LINQ™ digital platform enhances contractor productivity through real-time coating performance analytics, ensuring precise film thickness and color uniformity. This digital integration strengthens its value proposition in large-scale façade coating projects.

AkzoNobel advances sustainable architectural coatings through merger strategy and laser-curing innovation

AkzoNobel is undergoing a transformative phase with its announced merger of equals with Axalta, creating a global coatings powerhouse focused on sustainable industrial and architectural coatings. The company improved operational efficiency, achieving a 14.2% adjusted EBITDA margin supported by pricing discipline and a €200 million cost-saving initiative. Its collaboration with IPG Photonics introduces laser-curing powder coating technology, significantly reducing energy consumption compared to traditional curing processes. The 2026 "Rhythm of Blues" color collection reflects evolving urban design preferences toward bio-based and calming palettes. AkzoNobel raised €1.1 billion through a dual-tranche bond to accelerate adoption of bio-attributed raw materials in partnership with BASF and Arkema. These initiatives position the company at the forefront of low-carbon exterior coating technologies.

Asian Paints dominates Asia-Pacific exterior coatings demand with design-led innovation and smart manufacturing

Asian Paints commands a leading position in the Asia-Pacific exterior architectural coatings market, which contributes 46% of global demand, with the company tracking a 6.1% regional growth trajectory. Its "Moonlit Silk" (7809) color launch under ColourNext highlights a shift toward earthy, tactile design aesthetics aligned with the "Slow Joy" trend. The company has evolved into a comprehensive home décor ecosystem, with premium product lines such as Royale and Apex Ultima integrating waterproofing and eco-conscious "Solar Punk" finishes. Investments in advanced manufacturing facilities in Southern India are enabling efficient supply to rapidly urbanizing markets, where residential applications account for 63.0% of demand. Asian Paints is also leading the "IRL" design movement, emphasizing durable, weather-resistant textures suited for tropical climates. This strategy strengthens its leadership in high-performance exterior coatings across emerging economies.

Nippon Paint accelerates APAC leadership with acrylic resin dominance and self-cleaning coating technologies

Nippon Paint Holdings is reinforcing its leadership in the Asia-Pacific exterior coatings market through its "Asset Assembler" strategy, optimizing regional leaders such as NIPSEA and DuluxGroup (DGL). The company is benefiting from a projected recovery in China’s construction sector, supported by infrastructure investments and urban renewal initiatives. Its dominance in acrylic resins, which account for 43.1% of global usage, ensures superior UV resistance and long-term color retention in exterior coatings. Expansion in Australia and New Zealand, with projected 5.7% long-term growth, further diversifies its revenue base. Nippon Paint is also advancing self-cleaning and photocatalytic coatings that use solar energy to degrade pollutants, targeting premium commercial buildings. These innovations position the company strongly in next-generation smart and sustainable façade coatings.

BASF Coatings drives innovation in functional and sustainable exterior coatings through advanced materials and AI integration

BASF Coatings is strengthening its position in the exterior architectural coatings market with a projected EBITDA of €6.2 billion to €7.0 billion, supported by increased production capacity from its Zhanjiang Verbund site. The company introduced WB 2K DTM technology, enabling direct-to-metal coating systems that reduce material usage by 20% while improving efficiency. Its Acronal® dispersions are widely used for high-gloss, durable exterior coatings, particularly in industrial façade applications. BASF is integrating AI-powered formulation tools under its "Winning Ways" strategy, allowing precise carbon footprint analysis for coating systems. Strategic partnerships with construction firms are advancing "Cool Roof" technologies that mitigate urban heat island effects. With functional ceramic coatings holding 43.6% market share, BASF is well-positioned in sustainable and energy-efficient exterior coating solutions.

China Exterior Architectural Coatings Market: Dual-Carbon Mandates and “Liquid Stone” Innovation Driving Transformation

China is rapidly transforming its exterior architectural coatings market under its Dual-Carbon strategy, with strict mandates targeting carbon reduction in construction. A major shift is the adoption of liquid stone (ceramic-based coatings), which reduce structural load by ~75% compared to natural stone, making them ideal for high-rise buildings.

Technological innovation is also accelerating. Advanced systems combining radiative cooling topcoats with aerogel insulation layers can reduce surface temperatures by up to 10°C, significantly improving energy efficiency. Regulatory enforcement under the Ecological and Environmental Code (2026) is phasing out high-VOC coatings, while large-scale smart city retrofit programs are deploying photocatalytic coatings that actively break down pollutants like NOx. Additionally, infrastructure programs such as “Sponge Cities” are driving demand for high-build elastomeric coatings to improve water resistance in flood-prone areas.

United States Exterior Architectural Coatings Market: Climate Resilience and Labor Efficiency Driving Innovation

The U.S. market is increasingly focused on climate-resilient building envelopes, particularly in response to extreme weather conditions. States representing ~35% of construction activity (e.g., California, Texas, Florida) now mandate minimum Solar Reflectance Index (SRI) levels for exterior coatings.

Innovation is addressing both performance and labor challenges. New breathable moisture-barrier primers block 99.9% of external water while allowing internal vapor escape, making them ideal for humid regions. Additionally, ultra-high-build one-coat systems are reducing application time by ~30%, helping offset skilled labor shortages. Infrastructure funding is also driving demand for anti-carbonation coatings on bridges and overpasses. Meanwhile, industry consolidation—such as PPG’s divestiture of its architectural segment—signals a shift toward specialized, high-performance coatings.

India Exterior Architectural Coatings Market: Infrastructure Boom and Cooling Technologies Driving Rapid Growth

India is one of the fastest-growing markets, driven by infrastructure expansion and innovation in climate-adaptive coatings. The Gati Shakti master plan and housing programs like PMAY are significantly boosting demand for low-VOC waterborne exterior coatings.

Product innovation is a key differentiator. Companies are launching lotus-effect nanocoatings that provide super-hydrophobic, stain-resistant surfaces, alongside high-reflectivity coatings capable of reducing indoor temperatures by ~5°C. Consolidation (e.g., JSW–AkzoNobel synergy) is strengthening supply of zinc-rich anticorrosive primers for highways and infrastructure. Additionally, monsoon-driven challenges have led to development of antifungal coatings with up to 10-year resistance, while smart city initiatives are accelerating adoption of heat-reflective coatings across government buildings.

Germany Exterior Architectural Coatings Market: Biocide-Free Chemistry and Renovation Wave Driving Sustainability Leadership

Germany is leading Europe’s transition toward biocide-free exterior coatings, driven by stricter REACH regulations (2026). Manufacturers are developing mineral-stabilized emulsions that prevent mold growth without conventional chemical preservatives.

Government support is a major catalyst. Subsidies under KfW programs are tied to ETICS (Exterior Thermal Insulation Composite Systems), increasing demand for high-reflectance coatings. Innovation is also strong in digitalization, with AI-driven color matching and predictive maintenance systems improving lifecycle performance. Additionally, circular economy initiatives are introducing recycled-monomer acrylic coatings, while industrial applications—such as hydrogen infrastructure—are driving demand for epoxy-polyurethane hybrid coatings.

UAE Exterior Architectural Coatings Market: Extreme Climate Engineering and Regulatory Push Driving Demand

The UAE serves as a global testbed for desert-grade exterior coatings, designed to withstand extreme UV radiation, sand abrasion, and high salinity. Government initiatives—such as Abu Dhabi’s plan to retrofit 30,000 buildings by 2030—are driving demand for cool and energy-efficient coatings.

Regulatory frameworks are also shaping the market. Dubai’s TVOC cap (≤300 µg/m³) and restrictions on certain biocides are accelerating the transition to waterborne systems, which now account for ~71.5% market share. Innovation includes self-healing silane coatings that resist sand damage and maintain performance over time. Additionally, growth in luxury hospitality is driving demand for premium aesthetic finishes, while mega-projects like the Red Sea developments are increasing use of UV-resistant exterior primers.

Japan Exterior Architectural Coatings Market: Seismic Resilience and Fluoropolymer Longevity Driving Advanced Applications

Japan’s market is defined by precision engineering and disaster resilience, with coatings designed to withstand seismic activity and harsh environmental conditions. New high-elongation elastomeric coatings (>800%) maintain waterproofing even when buildings develop microcracks during earthquakes.

Material innovation is also a key strength. Japanese firms are advancing hydrophilic self-cleaning coatings that use rainwater to remove dirt, while fluoropolymer (FEVE) coatings now offer 30+ years of color retention. Additionally, hybrid formulations are blending traditional aesthetics with modern performance, particularly in heritage architecture. The healthcare sector is also driving demand for antimicrobial exterior coatings, reflecting Japan’s aging population and infrastructure needs.

Exterior Architectural Coating Market Report Scope

Exterior Architectural Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$42 Billion

|

|

Market Size (2032)

|

$57.2 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Resin Type (Acrylic, Alkyd, Polyurethane, Epoxy, Polyester, Fluoropolymers, Polysiloxanes and Silicones, Others), By Technology (Water-borne, Solvent-borne, Powder Coatings, UV-Curable), By Product Type (Emulsions, Primers and Sealers, Enamels, Stains and Varnishes, Textured Coatings, Specialty Coatings), By Application (Masonry and Concrete, Metal, Wood, Plastics and Composites, Glass), By End-Use Sector (Residential, Commercial, Industrial), By Finish (Gloss Level, Special Effects, Textured), By Price Point (Economy, Mid-range, Premium)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Jotun A/S, Kansai Paint Co., Ltd., Masco Corporation, RPM International Inc., Hempel A/S, BASF SE, Berger Paints India Limited, Benjamin Moore & Co., DAW SE, SKSHU Paint Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Exterior Architectural Coating Market Segmentation

By Resin Type

- Acrylic

- Alkyd

- Polyurethane

- Epoxy

- Polyester

- Fluoropolymers

- Polysiloxanes and Silicones

- Others

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- UV-Curable

By Product Type

- Emulsions

- Primers and Sealers

- Enamels

- Stains and Varnishes

- Textured Coatings

- Specialty Coatings

By Application

- Masonry and Concrete

- Metal

- Wood

- Plastics and Composites

- Glass

By End-Use Sector

- Residential

- Commercial

- Industrial

By Finish

- Gloss Level

- Special Effects

- Textured

By Price Point

- Economy

- Mid-range

- Premium

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Exterior Architectural Coating Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- Kansai Paint Co., Ltd.

- Masco Corporation

- RPM International Inc.

- Hempel A/S

- BASF SE

- Berger Paints India Limited

- Benjamin Moore & Co.

- DAW SE

- SKSHU Paint Co., Ltd.

*- List not Exhaustive