Market Analysis: High-Fashion Partnerships, AI Integration, and DTC Expansion Transform the Global Eyewear Frames Market

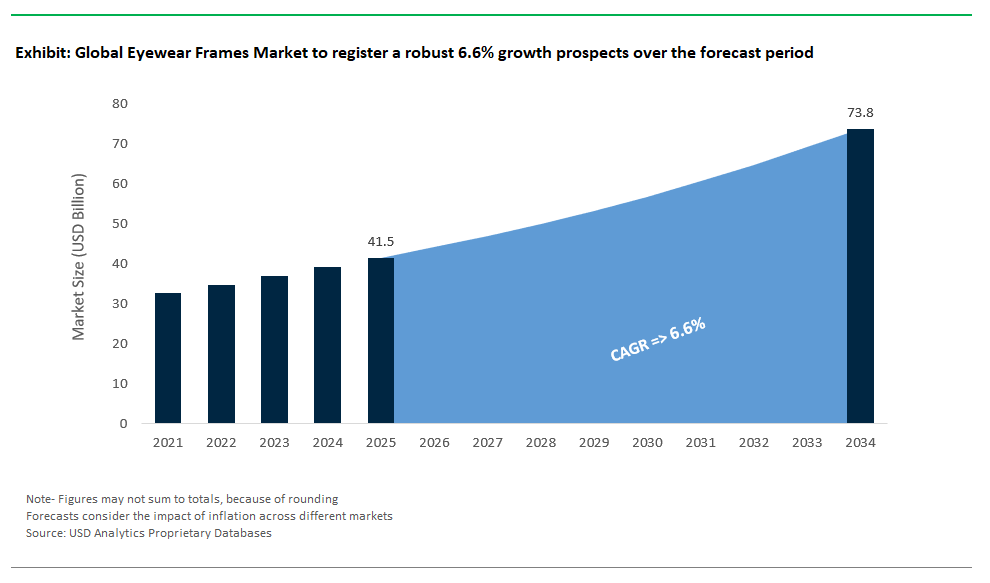

The Global Eyewear Frames Market Size is estimated at $41.5 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 6.6% to reach $73.8 Billion by 2034.

The global eyewear frames market is experiencing a significant wave of innovation and collaboration, as leading brands and technology giants redefine the landscape with high-profile partnerships, digital integration, and consumer-centric strategies. In February 2025, the continued alliance between luxury fashion powerhouse Maison Margiela and trendsetting eyewear brand Gentle Monster resulted in the launch of their third collaborative collection. Comprising eight cutting-edge sunglasses designs and 12 optical frames, this release not only underscores the persistent synergy between high-fashion and eyewear but also sets the tone for future designer collaborations, reinforcing the eyewear frame segment’s appeal as a statement accessory and style differentiator.

Smart technology integration is becoming a major force in frame innovation. At Computex 2025, ASUS introduced its "HealthAI Genie" and advanced wearable health solutions, illustrating the momentum behind artificial intelligence and personalized wellness features in consumer devices. While ASUS’s showcase included smart eyewear concepts rather than standalone frames, these developments reflect the broader industry trend where smart eyewear frames are evolving to incorporate sensors, health tracking, and augmented reality capabilities, fueling the next generation of digital eyewear.

Market leaders are also doubling down on smart glasses and AI-powered frames. EssilorLuxottica, the global eyewear giant, continues to expand its footprint in smart eyewear with investments in technologies such as Ray-Ban Meta Smart Glasses. The company’s strategic commitment to integrating digital functionalities like hands-free communication, voice assistants, and real-time information overlays into everyday frames is rapidly reshaping consumer expectations. These AI-driven features are turning ordinary eyewear into multifunctional lifestyle tools, positioning EssilorLuxottica at the forefront of smart eyewear innovation and setting benchmarks for competitors in the global eyewear frames market.

Lens technology and eye health concerns are also influencing frame design trends. Since the introduction of advanced blue-light blocking lens technology by Johnson & Johnson Vision in late 2023, the industry has seen continued growth in demand for frames that are compatible with specialized lenses. With increasing screen time and digital device use worldwide, consumers are prioritizing eyewear that helps mitigate digital eye strain. As a result, manufacturers are focusing on ergonomic designs, lightweight materials, and compatibility with high-performance lenses, ensuring that fashion and function go hand in hand in new frame releases.

The rise of direct-to-consumer (DTC) eyewear brands is revolutionizing access and personalization. Industry disruptors such as Warby Parker and Lenskart are accelerating their global reach, leveraging robust e-commerce platforms, virtual try-on experiences, and AI-driven customization tools. These brands empower consumers to select, visualize, and tailor frames online driving innovation in both frame design and material use while making high-quality eyewear more accessible to global markets. The result is an increasingly dynamic and competitive eyewear frames market, where digital convenience, customization, and brand-driven style define the purchasing experience.

Emerging Innovations in the Eyewear Frames Market

Trend: Adoption of Shape-Memory Alloys for Customized Fit

The eyewear frames market is experiencing a remarkable shift through the adoption of shape-memory alloys, notably titanium-nickel blends like Nitinol, which are significantly enhancing both durability and wearer comfort. Eyewear frames constructed from these advanced alloys provide superior resilience, effortlessly regaining their original shape after substantial deformation far outperforming traditional materials such as acetate. Prominent brands like Marchon’s Flexon and Eschenbach’s TITANflex are leveraging these alloys, creating frames capable of enduring extensive bending and twisting while consistently maintaining their structural integrity. Patent filings also suggest manufacturers are actively developing innovative "custom-fit" frames utilizing 3D-printed Nitinol inserts, designed to precisely adapt to facial contours through gentle heat application.

This innovative material trend is particularly advantageous for specialized consumer segments such as pediatric wearers and athletes, significantly reducing frame damage rates and minimizing frequent adjustments. Enhanced flexibility and reduced pressure points encourage greater comfort and compliance, particularly among children, addressing a primary barrier to sustained eyewear usage. Consequently, shape-memory alloy frames substantially contribute to improved visual health outcomes by promoting consistent use, positioning these materials as a driving trend for market expansion in eyewear technology.

Opportunity: Sensory-Integrated Smart Frames for Neurodivergent Populations

A compelling opportunity within the eyewear frames market lies in the development of sensory-integrated smart frames specifically tailored for neurodivergent populations, particularly individuals on the autism spectrum who frequently face challenges due to heightened sensitivity to environmental stimuli such as excessive light and sound. Integrating specialized technologies, including blue-light filtering lenses and sound-dampening features, these smart frames have shown promising early results in reducing sensory overload episodes.

Innovative research initiatives from institutions like ETH Zurich and the University of California have developed prototype smart glasses embedded with advanced dry EEG and EOG sensors integrated discreetly into the temple arms. These frames continuously monitor real-time neurophysiological signals to detect early signs of sensory overstimulation, automatically triggering adaptive responses such as lens dimming, gentle vibrations, or sound masking. Clinical pilot studies have indicated that these smart eyewear solutions effectively reduce anxiety and sensory overload episodes by up to 25% among autistic children in controlled environments. Ongoing advances in low-power sensor technologies further support prolonged daily use, presenting significant opportunities for widespread adoption in this niche but highly impactful market segment, substantially enhancing quality of life for neurodivergent individuals.

Competitive Landscape: Eyewear Frames Market

The eyewear frames market operates at the intersection of fashion, healthcare, and technology, characterized by rapid design innovation, evolving consumer preferences, and premiumization trends. Demand is driven by the rising prevalence of vision disorders, increasing awareness of eye health, and the growing role of eyewear as a lifestyle accessory. The market is further fueled by smart eyewear integration, sustainable materials, and omnichannel retail strategies. Leading players are competing through expansive brand portfolios, strong distribution networks, and continuous investment in advanced materials and technologies to deliver frames that combine style, durability, and functionality.

EssilorLuxottica – Global Powerhouse in Eyewear Design and Distribution

EssilorLuxottica stands as the undisputed leader in the eyewear frames market, leveraging its unmatched portfolio of proprietary brands such as Ray-Ban, Oakley, Persol, Oliver Peoples, and Vogue Eyewear, alongside an extensive array of licensed luxury brands including Giorgio Armani, Prada, Chanel, and Versace. This diverse brand mix positions the company to cater to every consumer segment, from premium fashion eyewear to performance-focused designs. With approximately 18,000 retail outlets under banners like LensCrafters, Pearle Vision, and GrandVision, EssilorLuxottica has established a global omnichannel presence, integrating digital eye exams and personalized virtual try-on technologies. The company is actively exploring smart eyewear solutions while investing heavily in R&D for advanced materials and ergonomic designs. Its strategic expansion through acquisitions and licensing deals ensures dominance across luxury, mass-market, and prescription eyewear categories, making it the benchmark for innovation, style, and distribution in the global eyewear frames industry.

Safilo Group – Diversified Portfolio with Sustainability Focus

Safilo Group, a key Italian player, is known for blending craftsmanship with modern design across its proprietary brands such as Carrera, Polaroid Eyewear, and Smith Optics, complemented by a robust lineup of licensed fashion labels. The company operates manufacturing units in Italy, China, and the U.S., maintaining strict quality standards while scaling global distribution. Recent initiatives underscore Safilo’s commitment to sustainability, notably its collaboration with The Ocean Cleanup to produce eyewear from ocean waste plastic, signaling an eco-conscious shift in product strategy. The renewal of key licensing agreements, such as Levi’s through 2029, reinforces Safilo’s stronghold in lifestyle segments. With an expanding focus on performance eyewear and value-driven offerings, Safilo continues to capitalize on rising demand for sustainable and stylish frames, positioning itself as a competitive force in both premium and accessible eyewear categories.

Kering Eyewear – Redefining Luxury and Smart Eyewear

Kering Eyewear dominates the luxury eyewear space with its exclusive portfolio of high-fashion brands, including Gucci, Saint Laurent, Balenciaga, and Alexander McQueen. Strategic acquisitions such as LINDBERG, known for premium titanium frames, and Maui Jim, a leader in high-end sunglasses, have solidified Kering’s leadership in the ultra-premium segment. The company’s innovation agenda is exemplified by its partnership with Google to develop AI-powered smart glasses, merging cutting-edge technology with sophisticated design a move that positions Kering as a trendsetter in connected eyewear. By integrating sun lens production through the acquisition of Italian lens manufacturer Lenti, Kering strengthens its vertical integration, ensuring quality control and operational agility. Its focus on premium aesthetics, superior craftsmanship, and advanced technologies positions Kering Eyewear as a global leader in redefining luxury eyewear for the future.

Marchon Eyewear (VSP Global) – Fashion-Forward and Performance-Driven Frames

Marchon Eyewear, under VSP Global, combines a strong portfolio of in-house brands like Airlock, Marchon NYC, and Flexon with a diverse range of licensed names, including Calvin Klein, Nike, Lacoste, and Salvatore Ferragamo. Renowned for durability and technological innovation, Marchon leverages materials such as memory metals for its Flexon brand, ensuring long-lasting, flexible eyewear solutions. Its expansive distribution network benefits from VSP Global’s integrated vision care model, providing Marchon with direct access to eye care professionals and retail channels worldwide. Recent strategies emphasize portfolio expansion and trend-driven designs, complemented by lifestyle and performance eyewear for sports enthusiasts. By balancing affordability, fashion, and performance, Marchon Eyewear caters to a broad consumer base seeking both style and function in their eyewear choices.

Charmant Group – Titanium Expertise and Premium Comfort

Charmant Group stands out for its mastery in titanium eyewear manufacturing, offering premium frames that deliver unmatched comfort, lightness, and durability. Renowned collections like Line Art Charmant and Charmant Titanium Perfection exemplify the brand’s precision engineering and material innovation, including the development of proprietary alloys such as “Excellence Titanium.” The company invests significantly in R&D, supported by collaborations with universities to enhance ergonomic design and structural integrity. Recent initiatives include AI-powered marketing campaigns and leadership restructuring to strengthen its global brand presence. With a strong footprint in premium optical frames and a reputation for elegance and functionality, Charmant Group continues to lead in high-end titanium eyewear, appealing to consumers who prioritize quality, durability, and sophisticated aesthetics.

Market Share and Segmentation Insights: Eyewear Frames Market

By Frame Type: Full-Rim Frames Dominate, Rimless Frames Expand Fastest

In 2025, full-rim frames are expected to hold the largest share at 51.2%, making them the most popular choice in the eyewear frames market. Their dominance is attributed to exceptional durability, extensive style options, and affordability, appealing to both fashion-forward and practical consumers. Full-rim frames continue to be the go-to option for prescription lenses and everyday eyewear. Meanwhile, rimless frames are projected to grow at the fastest CAGR of 7.2% through 2034, driven by the rising preference for lightweight, minimalist designs among professionals and business executives seeking comfort and a sleek look. Semi-rimless frames maintain a strong presence, combining aesthetic appeal with functionality, particularly among younger demographics who desire a balance of fashion and practicality.

.png)

By End User: Women Lead, Kids’ Frames Record Highest Growth

Women represent the largest end-user segment, accounting for 39.6% of the market share in 2025, primarily due to higher fashion-conscious spending, preference for premium eyewear, and adoption of luxury designer frames. Female consumers frequently seek multiple pairs for different occasions, boosting sales of stylish full-rim and semi-rimless options. In contrast, the kids’ segment is poised for the fastest expansion, registering a CAGR of 8.1% during the forecast period. This surge is fueled by the increasing prevalence of myopia among children and the growing demand for durable, flexible, and colorful frames designed to withstand active lifestyles. Additionally, unisex frames are gaining traction as gender-neutral fashion trends continue to rise, while men’s eyewear remains steady with consistent demand for classic, functional designs.

United States: Sustainable Materials and Inclusive Designs Reshape Eyewear Frames Market

The United States eyewear frames market is witnessing a transformative shift toward sustainability and inclusivity, spearheaded by leading industry players and reinforced by evolving consumer preferences. In June 2025, VSP Vision a major U.S. vision benefits provider announced that 53% of its frames now utilize sustainable materials, surpassing their original sustainability target. This milestone reflects a broader trend in which eco-friendly production processes and recycled or bio-based materials are increasingly in demand, as American consumers become more environmentally conscious. Additionally, the “Made in the USA” label is a crucial purchase factor for over half of American eyewear shoppers, influencing not just manufacturing location but also supply chain decisions and brand loyalty. As a result, domestic manufacturing has seen a resurgence, offering a competitive edge for brands that can promise provenance and quality alongside sustainability.

Beyond eco-credentials, the U.S. market is setting benchmarks for diversity and innovation in design. For example, National Vision’s January 2024 collaboration with Vontélle Eyewear introduced limited-edition frames designed for wider nose bridges and larger lenses, addressing the needs of underrepresented face shapes and advancing the industry’s push for inclusivity. Direct-to-consumer (DTC) brands like Warby Parker and Zenni Optical are also thriving, blending robust online sales with strategic brick-and-mortar expansions to offer personalized experiences and convenient access to a wide variety of frames. Meanwhile, the U.S. remains an early adopter of smart eyewear technologies, as evidenced by strong consumer interest in Ray-Ban Meta Smart Glasses and other AI-integrated products showcased in early 2025. This convergence of sustainability, inclusivity, and technology is redefining the competitive landscape of eyewear frames in the United States.

China: Myopia Epidemic and Fashion-Driven Growth Fuel Expanding Eyewear Frame Market

China’s eyewear frames market is uniquely shaped by the country’s ongoing myopia epidemic and a rapidly evolving consumer landscape. The World Health Organization estimates that by 2050, nearly half the global population will be myopic, with China accounting for the highest proportion due to increasing rates among children and adolescents. This demographic shift is driving unprecedented demand for prescription eyewear frames across the nation. In response, the Chinese government has rolled out public health campaigns and vision care initiatives to raise awareness and improve access to affordable, fashionable eyewear an effort that is fueling both the mass and premium segments. The proliferation of corrective lenses and frames is particularly evident in urban centers, where eye care is seen as both a health necessity and a style statement.

As disposable incomes rise and urbanization accelerates, Chinese consumers are placing greater emphasis on branded, fashion-forward eyewear. International fashion trends and celebrity influences are increasingly mirrored in local frame designs, leading to a surge in demand for stylish options. At the same time, China’s role as a global manufacturing hub cannot be understated: domestic eyewear companies are leveraging advanced production techniques to deliver both quantity and quality at scale, serving not only local consumers but also international markets. The sector is further boosted by government policies that incentivize innovation and support the modernization of manufacturing facilities, ensuring Chinese eyewear brands stay competitive in both technology and aesthetics. With a dynamic fusion of public health imperatives and fashion aspirations, China’s eyewear frames market is poised for robust long-term growth.

Germany: Precision Engineering and Eco-Innovation Define German Eyewear Frame Market

Germany’s eyewear frames market is renowned for its precision engineering, high adoption rates, and commitment to both technological innovation and sustainability. The country’s aging population drives a significant demand for corrective eyewear, with national health statistics showing strong uptake of prescription lenses and frames to address prevalent conditions like myopia and astigmatism. German consumers are known for their discerning eye for quality and durability, favoring frames that not only provide functional benefits but also align with the nation’s reputation for engineering excellence. Premium brands such as Rodenstock and Zeiss have solidified their positions as leaders, delivering technologically advanced frames that emphasize precise fitting and longevity, while also setting benchmarks for the luxury eyewear segment.

Environmental consciousness is another defining feature of the German market. Manufacturers are rapidly adopting sustainable materials and green production methods in response to rising consumer demand for eco-friendly products. This includes the use of recycled acetates, biodegradable plastics, and low-impact manufacturing processes. German frame designers also lead the way in minimalist, “quiet luxury” aesthetics, with brands like Götti and Markus T celebrated for their lightweight, screw-less, and innovative designs. These brands demonstrate a successful fusion of design-led innovation and practical wearability, appealing to both the domestic and broader European market. As a result, Germany continues to be a powerhouse in the global eyewear industry, balancing heritage craftsmanship with forward-looking sustainability and design trends.

Japan: Craftsmanship and Tech Innovation Drive Japan's Eyewear Frame Industry

Japan’s eyewear frames market is characterized by a unique blend of traditional craftsmanship and cutting-edge technology, responding to both demographic needs and evolving consumer preferences. Like China, Japan’s rapidly aging society and high rates of myopia ensure a consistent demand for prescription eyewear. Japanese brands such as JINS have carved out a reputation for integrating technology directly into their frames incorporating features like blue light-blocking lenses and even smart sensors catering to a tech-savvy population. This integration is not limited to lenses; the frames themselves are often designed for compatibility with wearable tech, reflecting Japan’s status as a global leader in both eyewear manufacturing and consumer electronics.

In addition to technological innovation, Japanese eyewear is renowned for its attention to detail and superior materials. Artisanal frame production using titanium, acetate, and other lightweight, durable materials is a hallmark of Japanese manufacturing, with a strong emphasis on comfort and longevity. The influence of Japanese and South Korean pop culture has elevated demand for trendy sunglasses and distinctive frame shapes, making fashion a significant driver of sales. E-commerce growth exemplified by the expansion of companies like Owndays has made stylish, high-quality eyewear more accessible, further fueling market expansion. Overall, Japan’s eyewear frame market remains vibrant, combining meticulous craftsmanship, advanced functionality, and a fashion-forward ethos.

United Kingdom: Sustainability and Online Innovation Shape UK Eyewear Frame Market

The United Kingdom’s eyewear frames market is experiencing growth driven by demographic trends and evolving consumer values. The country’s significant aging population has increased demand for corrective eyewear, while rising public awareness of eye health has led to greater uptake of preventive and fashionable frames. Public health campaigns and optometry initiatives continue to educate consumers on the importance of regular eye exams, boosting both the corrective and style segments of the market. UK eyewear shoppers also increasingly value environmental sustainability, prompting brands to adopt recycled materials and ethical production processes, particularly in response to younger consumers’ expectations for corporate responsibility.

A notable trend in the UK is the rise of secondhand and vintage eyewear, with online platforms enabling the “second life” of spectacles and feeding demand for unique, retro frames. This is complemented by a strong online retail presence, where e-commerce platforms offer a wide range of frames and innovative virtual try-on technologies, enhancing accessibility and convenience for buyers. The UK market’s combination of sustainability, digital innovation, and style-driven purchasing reflects the broader shift toward eco-friendly consumption and technological adoption. As a result, the UK eyewear frames sector is set to continue evolving, balancing tradition and innovation to meet the needs of a diverse and discerning consumer base.

Eyewear Frames Market Report Scope

Eyewear Frames Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$41.5 Billion

|

|

Market Size (2034)

|

$73.8 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product (Plastic/Acetate, Metal, Others), By Frame (Full-Rim Frames, Semi-Rimless Frames, Rimless Frames), By Shape (Square/Rectangular Frames, Oval & Round Frames, Aviator Frames, Cat-Eye Frames, Others), By End User (Men, Women, Unisex, Kids), By Category (Mass Market, Premium/Luxury), By Distribution Channel (Offline Stores (Brick-and-Mortar), Online Stores (E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

EssilorLuxottica SA, Safilo Group S.p.A., Fielmann Group AG, Hoya Corporation, Marchon Eyewear, Inc., Warby Parker, ZEISS Group, Bausch + Lomb, Johnson & Johnson Vision Care, Luxottica Group, Kering Eyewear, Carl Zeiss AG, Marcolin, De Rigo Vision

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Eyewear Frames Market Segmentation

By Product

- Plastic/Acetate

- Metal

- Others

By Frame

- Full-Rim Frames

- Semi-Rimless Frames

- Rimless Frames

By Shape

- Square/Rectangular Frames

- Oval & Round Frames

- Aviator Frames

- Cat-Eye Frames

- Others

By End User

By Category

- Mass Market

- Premium/Luxury

By Distribution Channel

- Offline Stores (Brick-and-Mortar)

- Online Stores (E-commerce)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Eyewear Frames Market

- EssilorLuxottica SA

- Safilo Group S.p.A.

- Fielmann Group AG

- Hoya Corporation

- Marchon Eyewear, Inc.

- Warby Parker

- ZEISS Group

- Bausch + Lomb

- Johnson & Johnson Vision Care

- Luxottica Group

- Kering Eyewear

- Carl Zeiss AG

- Marcolin

- De Rigo Vision

* List Not Exhaustive

Research Coverage

This USDAnalytics report delivers a comprehensive analysis of the global eyewear frames market from 2025 to 2034, examining key factors such as high-fashion partnerships, the rise of AI-integrated smart frames, and the growing influence of direct-to-consumer (DTC) brands.

The study presents detailed segmentation by product (plastic/acetate, metal, others), frame type (full-rim, semi-rimless, rimless), shape (rectangular, oval, aviator, cat-eye, others), end user (men, women, unisex, kids), category (mass market, premium/luxury), and distribution channel (offline stores, online e-commerce).

Regional insights span North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with focused analysis on top markets including the United States, China, Germany, Japan, and the United Kingdom. The report evaluates how trends in sustainability, blue-light blocking technology, and smart sensory frames are reshaping both product innovation and consumer preferences.

Competitive landscape coverage includes strategies and advancements by leading companies such as EssilorLuxottica, Safilo Group, Kering Eyewear, Marchon Eyewear, and others. This USDAnalytics research highlights emerging opportunities, future outlook, and actionable intelligence for manufacturers, retailers, and stakeholders aiming to capitalize on the evolving global eyewear frames market.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.