Organic Personal Care Products Market Overview: Growth Potential and Strategic Insights

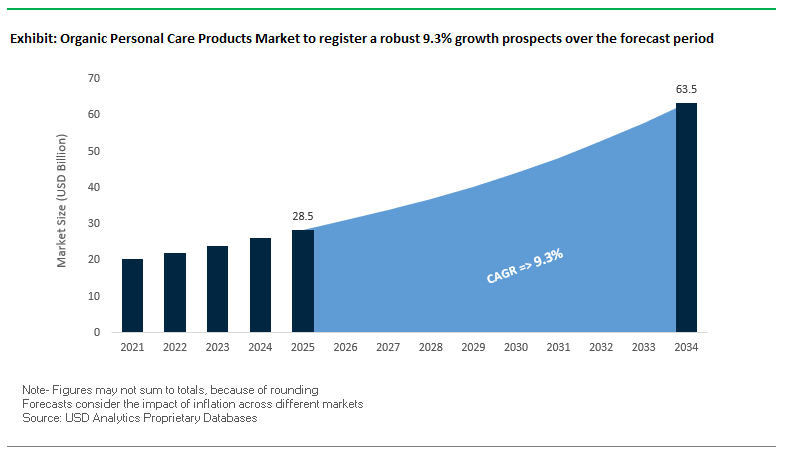

The global organic personal care products market is projected to grow from USD 28.5 billion in 2025 to USD 63.4 billion by 2034, registering a CAGR of 9.3%. This portfolio of consumer products is increasing rapidly with increasing demand from consumers for chemical-free, plant-based, and sustainably sourced products. Health-conscious consumers, particularly in the skincare market, are fueling the demand for open manufacturing process and organic-certified ingredients. Europe is a leadership market due to strict ingredient regulation, and Asia-Pacific is a high-growth market due to urbanization, increasing disposable incomes, and increasing awareness on ingredient safety.

Key Insights for Industry Professionals

- Ingredient Safety and Transparency – Skincare dominates the organic category as consumers seek chemical-free, non-toxic formulations.

- Regional Leadership – Europe leads due to regulatory standards, while Asia-Pacific experiences accelerated adoption driven by income growth.

- Omnichannel Distribution – While supermarkets and hypermarkets remain vital, e-commerce is enabling niche brands to scale globally.

- Ethical Sourcing – Brands like Dr. Bronner’s demonstrate leadership in fair trade, organic raw material sourcing, and regenerative farming.

- Sustainable Packaging Innovation – Glass, post-consumer recycled plastics, and fiber bottles from certified wood pulp are reducing environmental impact.

Organic Personal Care Products Market Analysis: Strategic Developments and Industry Momentum

The market is seeing geographic expansions, sustainability commitments, and strategic acquisitions as companies position themselves to take advantage of burgeoning demand. Shein's Sustainability Report of August 2025 set out renewable energy goals and supplier audits, reaffirming its circular fashion commitment through the "SHEIN Exchange" resale platform. Evolve Organic Beauty increased sustainable packaging in April 2025 with refill products packaged in wood-pulp fiber packaging, an entirely recyclable, paper-waste-free option.

High-growth market expansion is accelerating. Miranda Kerr's Kora Organics re-launched in India in April 2025 in association with Beautindia, capitalizing on the expansion of organic skincare uptake in Asia-Pacific. L'Oréal strengthened its dermatological beauty portfolio in taking control of UK skincare brand Medik8 in July 2025, with clinical expertise, as further consolidation of niche players in the organic arena into multinational portfolios.

Strategic retail partnerships are proving effective for consumer targeting. Juice Beauty's August 2024 collaboration with Credo Beauty facilitated the launch of a clean, organic makeup line in a specialist retail setting, targeting high-intent consumers. Heritage brands are doubling down on sustainability leadership Weleda's century-long sustainability reforestation program, launched in 2021, is planting a million trees in partnership with British charity Treesisters, reinforcing its green credentials.

Transformative Trends and High-Growth Opportunities in the Organic Personal Care Products Market

Farm-to-Face Traceability Building Consumer Confidence

The farm-to-face revolution is shifting the paradigm of transparency in the organic personal care market, with companies increasingly using blockchain to ensure ingredient origin verification. Blockchain offers an immutable record of each transaction along the supply chain, allowing consumers to track an ingredient's path from farm to finished product. Research on blockchain in agri-supply chains validated its success in giving verifiable information, avoiding counterfeiting, and maintaining authenticity. Within the cosmetics industry, blockchain platforms are increasingly being utilized to monitor ethical sourcing of raw materials like shea butter and tea tree oil, safeguarding both the product's integrity and the livelihood of farming communities. Customers can read QR codes on packaging to immediately view information on origin, processing, and sustainability certification, minimizing the risk of "greenwashing" and enhancing brand authenticity in a competitive market.

Waterless Formulations Solving for Sustainability and Portability

Water scarcity issues, particularly in areas prone to drought, are driving the transition to waterless beauty formulations in the organic personal care marketplace. Solid conditioners, powders, balms, and shampoos provide high concentrations of active ingredients without the excess water content. Studies indicate that a 100g bar of solid shampoo can be used for up to three 250ml liquid bottles, greatly minimizing packaging waste and water consumption. Apart from environmental benefits, these products are convenient in that they are spill-proof, traveling-friendly, and TSA-approved, making them perfect for an active lifestyle. In regions like the Middle East, where water conservation is not only an environmental but also a cultural imperative, brands are rapidly building waterless product ranges, driving adoption and establishing themselves as sustainability leaders.

Men's Organic Grooming Ready for Fast Expansion

The men's organic grooming segment is largely untapped with huge growth potential. Research finds that younger male consumers, especially Millennials and Gen Z, are consciously looking for clean-labeled, vegan, cruelty-free, and paraben-free personal care products. Social media is fueling this trend Chinese websites, for instance, have seen a 167% increase in searches for men's beauty, with more than 100,000 "How to Look Handsome" posts. This cultural change is making it mainstream for men to have grooming habits and paving the way for natural brands to extend themselves into shaving cream, beard oil, and facial skincare specifically for men.

Pet Organic Care as the Next Frontier

Pet humanization is forging a new category of growth in organic personal care. As of 2023, 70% of U.S. households had a pet (APPA), and human-grade grooming products infused with natural ingredients such as aloe vera, oatmeal, and herbal extracts are what consumers are looking for. Market research attests to growing demand for pet care that excludes harsh chemicals and allergens. Major players are reacting by embracing human-grade certifications, biodegradable packaging, and environmentally friendly manufacturing processes, developing a premium sub-market whereby transparency, safety, and quality are prominent drivers of purchase.

Market Share Insights of the Organic Personal Care Products Industry

Organic Personal Care Market Share by Product: Skin Care Leads, Hair Care Gains Momentum

Skin care commands a 32% share of the organic personal care market, driven by surging demand for chemical-free cleansers, moisturizers, and anti-aging solutions. Brands such as Burt’s Bees and The Body Shop are leaders in this space, leveraging consumer preference for “clean label” formulations. Hair care follows at 25%, with sulfate-free shampoos, conditioners, and Ayurvedic-inspired treatments seeing rapid adoption. Oral care, cosmetics, fragrances, and deodorants are also expanding as consumers extend their preference for organic options to all areas of personal hygiene and grooming. Aluminum-free deodorants and essential oil-based perfumes are experiencing notable growth, while baby care, sunscreens, and intimate hygiene products strengthen the “Others” category, diversifying the market’s revenue base.

.png)

Organic Personal Care Market Share by Ingredient: Plant-Based Dominates While Mineral-Based Sees Strategic Growth

Plant-based ingredients hold a commanding 65% share, reflecting strong consumer trust in botanicals such as aloe vera, coconut oil, and shea butter. These ingredients are perceived as safe, effective, and environmentally friendly. Mineral-based components like zinc oxide and titanium dioxide are particularly valued in sunscreens and makeup for their natural UV protection and skin-friendly profile. While animal-based ingredients such as beeswax and lanolin still feature in some organic formulations, demand is gradually shifting toward vegan-friendly plant-based alternatives. This transition aligns with the rising popularity of cruelty-free certifications and ethical consumerism.

Competitive Landscape – Key Players Defining the Organic Personal Care Products Industry

Organic personal care market brings together tradition-tested heritage brands and new, digitally native brands, both leveraging ingredient integrity and sustainability narratives as differentiators. Major players that are present include Estée Lauder Companies Inc. (Aveda), The Hain Celestial Group (Avalon Organics), L'Oréal S.A., Natura &Co, The Body Shop, Shiseido Co. Ltd., Johnson & Johnson, Amway, Forest Essentials, Mamaearth, Burt's Bees, Juice Beauty, Tata Harper, KORA Organics, Melvita, Others.

Dr. Bronner's – Ethical, Regenerative, and Activist-Driven

Dr. Bronner's is the world leader in fair trade purchasing, responsible sourcing, and regenerative agriculture. It purchased $19.2 million worth of fair trade raw materials and planted more than 243,000 trees in dynamic agroforestry initiatives in 2023. Its commitment to sustainability also reaches packaging, with 75% PCR composition among materials and a high emphasis on social donations, giving $5.7 million to causes from animal protection to drug policy reform.

Tata Harper Skincare – Luxury Organic with Farm-to-Face Control

Producing all of its high-end skincare in-house at its Vermont farm, Tata Harper exercises full in-house control over production and formulation. Green glass bottles and anti-aging herbal infusions are hallmarks. Acquired by AmorePacific in 2022 for $124 million, Tata Harper's "Follow Your Bottle" transparency initiative enables consumers to trace each product's production process.

Juice Beauty – USDA Organic and Celebrity Endorsements

Juice Beauty produces products with a certified organic juice base instead of water to offer nutrient-rich skincare and cosmetics. Familiar with partnerships with Gwyneth Paltrow and Kate Hudson, the company has an "internet-first" direct-to-consumer model with retail partnerships like its limited-edition makeup collection with Credo Beauty.

Weleda – A Hundred-Year-Old Biodynamic Beauty Pioneer

Founded in 1921, Weleda integrates anthroposophy, biodynamic farming, and natural products. It has over 50 subsidiaries globally and produces most of its ingredients in biodynamic gardens, including one 50-acre farm in Germany. The most recent retailing innovation is "City Spas" in European capital cities, offering experiential brand experiences alongside its traditional products like Skin Food and Arnica Essence.

United States: Technology-Enhanced Customization and Clean-Label Innovation

The U.S. organic personal care products market operates in a regulatory landscape that emphasizes ingredient transparency and consumer safety, despite the absence of a unified federal definition for "organic" in cosmetics. Oversight from the USDA Organic certification for agricultural inputs and the FDA’s cosmetic labeling rules drives heightened accountability. American brands are capitalizing on AI and Big Data analytics to analyze consumer feedback, identify market gaps, and develop highly customized organic formulations. This shift toward personalization is elevating product appeal among discerning consumers who value efficacy alongside natural composition.

E-commerce and digital marketing are major growth engines, with brands leveraging social media influencers, targeted online campaigns, and educational content to promote clean-label products. Innovations include multi-functional organic formulations such as vegan anti-aging serums, mineral-based sunscreens, and products free from parabens and sulfates that cater to health-conscious and eco-aware consumers. Sustainability is integral to brand positioning, with widespread adoption of biodegradable packaging, refillable containers, and ethical sourcing strategies to build consumer trust and enhance brand equity in a competitive market.

European Union: Regulatory Leadership and Ingredient Innovation

The European Union remains a global benchmark for organic personal care standards, underpinned by strict regulations like the Corporate Sustainability Reporting Directive (CSRD), which mandates detailed sustainability disclosures. Well-recognized certifications, including ECOCERT and COSMOS Organic, provide standardized definitions for product authenticity, helping combat greenwashing and ensuring consumer trust. The EU’s eco-design agenda supports a circular economy approach, encouraging the use of innovative packaging such as bottles made from certified wood pulp and implementing bans on the destruction of unsold goods.

Chemical safety is a priority, with proactive bans on harmful substances like PFAS expected to extend into cosmetics, accelerating the industry’s shift toward safe, plant-based formulations. R&D investment is directed toward upcycled ingredients from food production waste and the creation of bio-based materials through green chemistry, fostering innovation that aligns with both environmental and consumer safety goals. This regulatory rigor and commitment to sustainability position the EU as a leader in shaping the future of the organic personal care sector.

India: Ayurveda-Driven Growth and D2C Brand Expansion

India’s organic personal care products market is anchored in its Ayurvedic heritage, with a strong consumer preference for formulations featuring traditional botanicals like turmeric, neem, and sandalwood. The rise of direct-to-consumer (D2C) brands leveraging mobile apps, dedicated websites, and social media has allowed companies to bypass traditional retail and build loyal customer bases through personalized marketing and education.

Government and NGO initiatives promoting organic farming and biodiversity-based sourcing further strengthen consumer trust and support industry growth. E-commerce expansion via platforms such as Nykaa, Amazon, and Flipkart is extending brand reach into tier 2 and tier 3 cities, driving penetration beyond metro markets. Sustainability is an increasing focus, with Indian brands introducing recycled plastic packaging and adopting plastic-positive initiatives to ensure that more plastic is recycled than consumed, aligning with global eco-conscious trends while maintaining competitive pricing.

China: E-Commerce-Driven Growth and Premium Organic Formulations

China’s organic personal care products market is expanding rapidly as consumer awareness of ingredient safety and clean beauty principles gains traction. The shift away from synthetic chemicals toward natural and organic alternatives is propelled by both health concerns and aspirational beauty standards. Government backing for sustainable product development and investments in high-tech industries are modernizing manufacturing and strengthening distribution capabilities.

E-commerce platforms enhanced by livestreaming commerce serve as key retail channels, enabling brands to educate, engage, and convert large audiences in real time. R&D is a growing priority, with companies investing in innovative organic formulations that balance efficacy and safety to meet the evolving preferences of an increasingly sophisticated consumer base. This integration of modern retail strategies with advanced product development is positioning China as a competitive force in both domestic and export-oriented organic personal care markets.

Organic Personal Care Products Market Report Scope

Organic Personal Care Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.5 Billion

|

|

Market Size (2034)

|

$63.4 Billion

|

|

Market Growth Rate

|

9.3%

|

|

Segments

|

By Product (Skin Care, Hair Care, Oral Care, Cosmetics, Fragrances, Deodorants, Others), By Ingredient (Plant-based, Animal-based, Mineral-based), By Distribution Channel (Online (E-commerce Websites, Company-Owned Websites), Offline (Hypermarkets & Supermarkets, Specialty Stores, Pharmacies, Others)), By Gender (Women, Men, Kids), By End-Use (Mass Market, Professional), By Pricing (Economical, Mid-Range, Premium)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Estée Lauder Companies Inc. (Aveda), The Hain Celestial Group (Avalon Organics), L'Oréal S.A., Natura &Co, The Body Shop, Shiseido Co. Ltd., Johnson & Johnson, Amway, Forest Essentials, Mamaearth, Burt's Bees, Juice Beauty, Tata Harper, KORA Organics, Melvita, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Personal Care Products Market Segmentation

By Product

- Skin Care

- Hair Care

- Oral Care

- Cosmetics

- Fragrances

- Deodorants

- Others

By Ingredient

- Plant-based

- Animal-based

- Mineral-based

By Distribution Channel

- Online

- E-commerce Websites

- Company-Owned Websites

- Offline

- Hypermarkets & Supermarkets

- Specialty Stores

- Pharmacies

- Others

By Gender

By End-User

By Pricing

- Economical

- Mid-Range

- Premium

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Organic Personal Care Products Market

- Estée Lauder Companies Inc. (Aveda)

- The Hain Celestial Group (Avalon Organics)

- L'Oréal S.A.

- Natura &Co

- The Body Shop

- Shiseido Co. Ltd.

- Johnson & Johnson

- Amway

- Forest Essentials

- Mamaearth

- Burt's Bees

- Juice Beauty

- Tata Harper

- KORA Organics

- Melvita

* List Not Exhaustive

Research Coverage

This report investigates the Organic Personal Care Products Market with an in-depth analysis of ingredient trends, distribution strategies, regulatory influences, and competitive positioning, enabling stakeholders to identify high-growth opportunities in this expanding sector. Compiled by USDAnalytics, it delivers strategic breakthroughs, analysis reviews, and highlights on how plant-based innovation, ethical sourcing, sustainability-focused packaging, and omnichannel retail models are reshaping the market through 2034. This report is an essential resource for executives, R&D leaders, brand strategists, and investors seeking actionable insights on market expansion across premium, mid-range, and mass market segments, backed by comprehensive segmentation and regional profiling. Scope includes-

- Segmentation:

- By Product: Skin Care, Hair Care, Oral Care, Cosmetics, Fragrances, Deodorants, Others

- By Ingredient: Plant-based, Animal-based, Mineral-based

- By Distribution Channel: Online, Offline

- By Gender: Women, Men, Kids

- By End-User: Mass Market, Professional

- By Pricing: Economical, Mid-Range, Premium

- Geographic Scope: 25+ countries across North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

- Timeframe: Historic data from 2021–2024, forecasts from 2025–2034.

- Companies: Profiles and analysis of 15+ leading players in the organic personal care industry.

Methodology

The research adopts a robust hybrid approach, combining primary and secondary intelligence to ensure comprehensive coverage. Primary research includes structured interviews with brand executives, sustainability officers, packaging innovators, ingredient suppliers, and retail buyers to capture firsthand insights. Secondary research draws on certified organic product databases, government trade statistics, retail sales trackers, sustainability reports, and industry publications. Market sizing applies both top-down and bottom-up modeling, segmenting by product, ingredient type, distribution channel, and region, then validating through triangulation with market share data from leading players. Forecasting incorporates regulatory trend analysis, consumer adoption curves, and innovation pipelines, while competitive benchmarking evaluates differentiation in brand positioning, product innovation, and ESG performance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.