Facade Coatings Market Expansion Driven by Energy-Efficient Building Skins, Insulated Facade Systems, and Premium Architectural Finishes

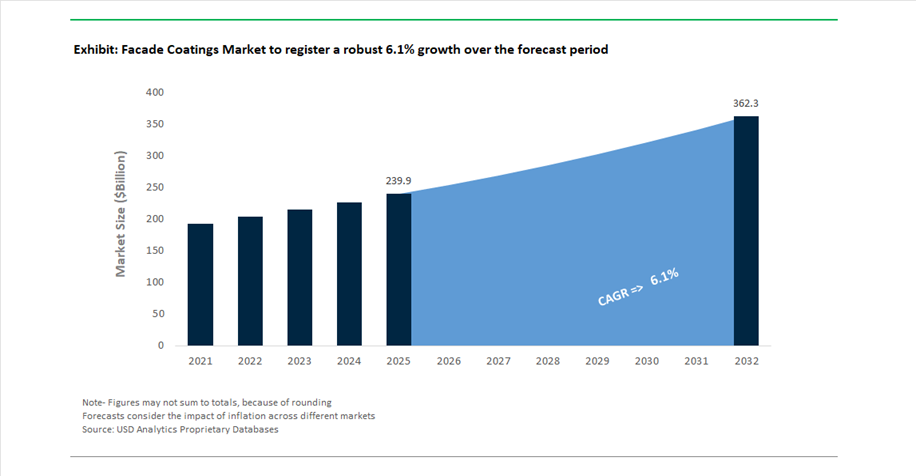

The global Facade Coatings Market was valued at USD 239.9 billion in 2025 and is projected to grow at a CAGR of 6.1% between 2025 and 2032, reaching USD 363.1 billion by 2032. This robust growth reflects the increasing importance of high-performance facade coatings in modern construction, where exterior surfaces are expected to deliver not only aesthetic appeal but also thermal efficiency, durability, and environmental performance.

A key structural driver is the global push toward energy-efficient buildings and climate-neutral construction, particularly in Europe and developed markets targeting net-zero emissions by 2050. Facade coatings are increasingly integrated into External Wall Insulation Systems (EWIS) and advanced building envelopes, enabling improved thermal insulation, reduced energy consumption, and enhanced occupant comfort. Additionally, the demand for weather-resistant, UV-stable, and pollution-resistant coatings is rising in urban environments exposed to harsh climatic conditions and air pollutants.

The market is also benefiting from the rapid evolution of premium architectural design trends, including metallic finishes, ultra-matte textures, and customized color solutions for high-rise commercial and residential projects. Innovations in resin chemistry, pigment technology, and coating formulations are enabling longer service life, reduced maintenance cycles, and superior color retention. Furthermore, the integration of functional coatings, such as solar-absorbing and heat-reflective systems, is transforming facades into active components of a building’s energy system.

Solar-Active Facades, and Insulated System Dominance Redefine Competitive Landscape

The facade coatings market is undergoing a strategic transformation driven by large-scale acquisitions, sustainability-focused innovation, and vertical integration strategies. In April 2026, Sherwin-Williams announced the acquisition of BASF’s architectural paints business in Brazil for $1.15 billion, including the Suvinil brand. This move establishes Sherwin-Williams as a dominant player in Latin America’s facade coatings segment, particularly in exterior masonry applications where demand is rapidly expanding.

Sustainability and energy integration are emerging as defining innovation themes. In October 2025, AkzoNobel became the exclusive supplier for a solar-absorbing facade coating technology, enabling building exteriors to function as passive heating systems. This marks a transition from traditional protective coatings to “active facades” that contribute to energy generation and building efficiency. Complementing this, Sto SE & Co. KGaA was recognized in January 2026 as the global leader in External Wall Insulation Systems (EWIS), reinforcing the growing importance of integrated facade solutions combining coatings with insulation.

Capacity expansion and regional localization are further strengthening market dynamics. In July 2025, Sto SE & Co. KGaA inaugurated a new production facility in Melbourne, enhancing supply chain efficiency and reducing carbon emissions associated with long-distance transport. Meanwhile, Nippon Paint Holdings advanced its vertical integration strategy through the March 2025 acquisition of AOC, securing access to advanced resin technologies critical for high-performance facade coatings.

Product innovation is increasingly focused on durability and aesthetics. In April 2026, AkzoNobel launched its Futura Collection 2026–2029, featuring anodic and ultra-matte finishes that replicate premium metallic facades while delivering superior UV resistance. Similarly, in November 2025, Jotun introduced hybrid epoxy coatings designed for metal facades in corrosive environments, addressing durability challenges in coastal and industrial urban areas.

Market dynamics in emerging economies are also evolving rapidly. In February 2026, Kansai Nerolac Paints divested a portion of its Indian coatings business to the JSW Group, enabling JSW Paints to expand its “Think Beautiful” facade initiative. This shift reflects increasing competition and localization strategies in high-growth markets like India. Additionally, in January 2026, PPG Industries launched the MASTER’S MARK BALLARD™ coating line, targeting premium residential facade applications in China with advanced adhesion and low-emission properties.

Tightening VOC Regulations Accelerating Transition to Low-Emission Facade Coatings Technologies

The global facade coatings market is undergoing a structural shift as regulatory bodies intensify enforcement of volatile organic compound emission limits, directly impacting formulation strategies and product portfolios. In the United States, the Environmental Protection Agency has aligned national VOC standards with California Air Resources Board thresholds, introducing stricter reactivity-based limits for architectural and aerosol coatings. This has accelerated the transition toward water-borne facade coatings, high-solid systems, and low-VOC alkyd-modified chemistries that deliver compliance without compromising durability. A critical milestone is the January 17, 2027 compliance deadline for aerosol coatings, which is forcing manufacturers to reformulate specialty facade coatings used in touch-up and niche applications. Across Europe, the expansion of REACH restrictions on solvent chemistries has driven a measurable increase in innovation, with patent filings for low-emission and circular coating formulations rising by approximately 20% between 2024 and 2025. Lifecycle assessment data indicates that shifting from solvent-borne to advanced low-VOC systems can reduce the environmental impact of facade coatings by up to 46%, reinforcing their role in sustainable construction. These regulatory developments are embedding environmental compliance as a core performance metric, driving demand for eco-friendly facade coatings, low-VOC architectural paints, and sustainable exterior coating solutions across residential and commercial infrastructure projects.

Commercial-Scale Integration of Bio-Based Acrylic Binders in Exterior Wall Coatings

The adoption of bio-based acrylic binders is transitioning from pilot-scale innovation to commercial-scale deployment within the facade coatings industry, driven by corporate decarbonization targets and increasing demand for sustainable construction materials. Production capacity for bio-based resins derived from plant oils and biomass-balanced feedstocks expanded by approximately 12% annually across the Asia-Pacific region during 2024, reflecting strong global demand. By early 2026, water-based bio-resins have captured around 42% of the bio-based coatings segment, largely due to their compatibility with architectural applications and regulatory preference for low-emission systems. Major chemical manufacturers have accelerated commercialization through the introduction of biomass-balanced and USDA-certified bio-based coating portfolios, enabling substitution of petroleum-derived acrylic binders in exterior wall coatings. This transition is further supported by a 25% increase in patent activity focused on circular bio-based formulations that enhance recyclability of coated substrates and reduce end-of-life environmental impact. The integration of renewable raw materials into facade coatings is also aligning with Scope 3 emission reduction strategies across construction value chains, positioning bio-based coatings as a critical component in achieving carbon-neutral building targets. These developments are strengthening the market for sustainable facade coatings, bio-based architectural paints, and circular coating technologies in both developed and emerging construction markets.

High Solar Reflectance Facade Coatings Supporting Saudi Arabia’s Mega Infrastructure Projects

Large-scale infrastructure developments under Saudi Vision 2030 are generating significant demand for advanced facade coatings engineered for extreme climatic conditions. Giga-projects such as NEOM and the Red Sea Project are integrating high solar reflectance coatings as a standard specification to mitigate urban heat accumulation and improve building energy efficiency. These coatings utilize infrared-reflective nano-pigments to achieve elevated Solar Reflectance Index values, directly reducing heat absorption on building exteriors. Field testing indicates that high-performance reflective facade coatings can lower indoor ambient temperatures by approximately 5°C to 7°C in arid environments, significantly reducing reliance on air conditioning systems. In addition to thermal performance, there is a growing requirement for multifunctional facade coatings that combine reflectivity with self-cleaning and anti-fungal properties, ensuring durability in both desert and coastal conditions. With over one trillion dollars in active and planned infrastructure investments, the demand for coatings that meet international green building standards such as LEED and EDGE is becoming a baseline requirement for project approval. This is creating a high-value opportunity for manufacturers specializing in cool wall coatings, energy-efficient exterior coatings, and climate-adaptive facade solutions tailored for large-scale urban developments in the Middle East.

Germany BEG Subsidy Program Accelerating Energy-Efficient Facade Retrofit Coatings Demand

Germany’s Federal Funding for Efficient Buildings program is acting as a primary catalyst for the expansion of the facade retrofit coatings market across Europe. The updated 2025 BEG framework offers subsidies covering up to 40% of total project costs for facade insulation and high-performance exterior coatings when implemented as part of comprehensive energy-efficiency upgrades. Additional incentives under the BEG EM program provide a 15% base subsidy, with an extra 5% bonus for projects aligned with Individual Renovation Roadmaps, encouraging systematic upgrades of building envelopes. To qualify for these incentives, retrofit projects must meet stringent thermal performance targets, often requiring U-values below 0.20 W per square meter Kelvin. This is driving demand for thick-film insulated coatings and advanced facade systems capable of delivering superior thermal resistance alongside weather protection. The influence of Germany’s subsidy model is extending across Europe, with countries such as France allocating approximately 2.8 billion dollars through similar programs to promote external wall insulation and energy-efficient renovation. This regulatory and financial support ecosystem is accelerating the adoption of high-performance facade coatings, energy-saving exterior paints, and thermally efficient building envelope solutions, creating sustained growth opportunities in the European retrofit market.

Facade Coatings Market Share by Product Type in 2025: Emulsions and Paints Lead with Cost Efficiency and Sustainability Transition

Emulsion-Based Facade Coatings Dominate Due to Scalability, Ease of Application, and Low-VOC Shift

The facade coatings market by product type in 2025 is led by emulsions and paints, accounting for 38% market share, driven by their strong position in large-scale residential and commercial construction projects. These coatings are widely preferred due to their cost-effectiveness, ease of application, and extensive color versatility, making them the default choice for developers and contractors. The segment’s dominance is further reinforced by increasing adoption of water-borne and low-VOC emulsion coatings, particularly across Europe and North America, where stringent environmental regulations are accelerating the shift away from solvent-based systems. Modern acrylic emulsion facade coatings also offer improved weather resistance, UV stability, and breathability, ensuring long-term durability on exterior surfaces. While advanced solutions such as self-cleaning, anti-graffiti, and nano-coatings are gaining traction, emulsions continue to anchor the market due to their balance of performance, affordability, and regulatory compliance, positioning them as the backbone of global facade coating demand.

Facade Coatings Market Share by Application Type in 2025: Renovation Boom Drives Demand for High-Performance Coatings

Renovation and Refurbishment Segment Leads Amid Aging Infrastructure and Energy Efficiency Upgrades

The facade coatings market by application type in 2025 is dominated by renovation and refurbishment, capturing 58% market share, reflecting the growing need to upgrade aging building infrastructure in developed regions such as Europe and North America. This segment’s leadership is driven by extensive facade recoating, repair, and restoration activities, as older buildings require enhanced protection against environmental degradation. Additionally, energy efficiency retrofits and net-zero building initiatives are significantly boosting demand for advanced coating solutions, including heat-reflective coatings, self-cleaning facade systems, and low-maintenance exterior paints. These technologies help improve thermal insulation, reduce energy consumption, and extend building lifecycle performance, aligning with global sustainability targets. Compared to new construction, renovation projects often demand higher-performance coatings with enhanced adhesion and durability, making them a critical revenue driver in the global facade coatings market, particularly as urban redevelopment and green building regulations continue to accelerate worldwide.

Facade Coatings Market Competitive Landscape Driven by Energy-Efficient Technologies and Sustainable Materials

The facade coatings market is characterized by intense competition among global leaders focused on energy-efficient coatings, self-cleaning technologies, and low-carbon materials. Market dynamics are shaped by urbanization, retrofit demand, smart facade systems, and increasing adoption of sustainable, high-performance architectural coatings across commercial and residential sectors.

AkzoNobel accelerates facade coatings innovation with self-cleaning resins and Axalta merger strategy

AkzoNobel is reinforcing its leadership in the facade coatings market through the ongoing merger with Axalta Coating Systems, expected to finalize by the end of 2026, creating a global powerhouse in architectural coatings. The company introduced the first hydrophilic resin-based self-cleaning facade coating, enabling rainwater-driven pollutant removal and reducing maintenance costs for high-rise structures. Its partnership with IPG Photonics to deploy laser-curing powder coatings reduces energy consumption by up to 30%, advancing sustainable facade finishing. Financially, AkzoNobel improved its adjusted EBITDA margin to 14.2%, supported by its Industrial Excellence program. The company also plays a critical role in Calosol heat-absorbing facade technologies, transforming building exteriors into energy-generating surfaces. These advancements position AkzoNobel at the forefront of smart and sustainable facade coatings.

PPG Industries strengthens facade coatings portfolio through sustainability-driven products and regional expansion

PPG Industries has strategically repositioned its facade coatings business following the $2 billion divestiture of its North American architectural coatings segment, allowing greater focus on industrial, aerospace, and EV-related applications. The company reported strong double-digit growth in Asia-Pacific markets such as India and Vietnam, capitalizing on the region’s significant share in global construction activity. 44% of PPG’s revenue now comes from sustainably advantaged products, including its Envirocron® dielectric coatings used in infrastructure insulation. The company is investing $300 million in North American manufacturing to support supply chain regionalization under the "China Plus One" strategy. These initiatives enhance its competitiveness in advanced facade protection systems. PPG’s portfolio emphasizes durable, energy-efficient, and environmentally compliant facade coatings.

Sherwin-Williams maintains U.S. facade coatings dominance through premium products and distribution strength

The Sherwin-Williams Company continues to dominate the U.S. facade coatings market, supported by its extensive network of over 5,000 company-operated stores ensuring rapid product availability and service. The company issued 2026 EPS guidance of $11.50 to $11.90, reflecting resilience despite a softer demand environment. Strategic acquisitions such as Suvinil and Gross & Perthun have strengthened its portfolio with high-performance epoxy and polyurethane primers, addressing rising demand for specialized primer coatings. Its Powdura® ECO line incorporates up to 25% recycled plastic, aligning with sustainability goals. Additionally, the launch of "Universal Khaki" aligns with AAMA 2605 standards for durable aluminum facades. This combination of logistics, innovation, and premium offerings solidifies its leadership in exterior facade coatings.

Nippon Paint drives facade coatings growth through fluoropolymer innovation and urban retrofit demand

Nippon Paint Holdings is expanding its footprint in the facade coatings market through its "Asset Assembler" strategy, focusing on high-growth regions such as Europe and Asia-Pacific. The company is experiencing strong growth in TUC segments driven by urban renewal and facade retrofitting projects, particularly in China and Southeast Asia. Its development of low-contractibility fluoropolymer powder coatings enables thick-film applications up to 1000 µm, ideal for heavy-duty coastal and industrial environments. Nippon Paint is also enhancing consumer engagement through its "Slow Joy" color palette, emphasizing bio-inspired textures and durability in extreme climates. These innovations strengthen its positioning in premium and high-performance facade coatings. The company continues to benefit from rising demand for long-lasting, weather-resistant exterior solutions.

BASF Surface Technologies advances facade coatings sustainability through bio-based resins and cost optimization

BASF SE is strengthening its facade coatings portfolio through increased production capacity from its Zhanjiang Verbund site, supporting higher demand for emulsion resins in architectural applications. The company has formed strategic partnerships with AkzoNobel and Arkema to develop bio-attributed resins, significantly lowering Scope 3 emissions in facade coatings across Europe. BASF achieved €1.7 billion in cost reductions and is targeting €2.3 billion by 2026 through supply chain optimization and operational efficiency. Its projected EBITDA of €6.2 billion to €7.0 billion reflects strong financial positioning. The company is also balancing expansion with emissions targets of 17.2 to 18.2 million metric tons of CO2. These initiatives reinforce BASF’s leadership in sustainable and high-performance facade coating technologies.

Kansai Paint strengthens Asia-Pacific facade coatings leadership with cool roof technologies and polyurethane systems

Kansai Paint is leveraging its robust market share in Asia-Pacific to drive adoption of polyurethane-based facade coatings. The company introduced next-generation cool roof coatings featuring infrared-reflective pigments that reduce surface temperatures by up to 15°C, addressing urban heat challenges in South Asia. Its vertical integration across automotive and industrial coatings enables the transfer of advanced resin technologies into facade applications, enhancing durability and chemical resistance. Kansai Paint is also focusing on low-VOC and zero-emission formulations to meet tightening environmental regulations in North America.

China Facade Coatings Market: Dual-Carbon Mandates and Smart Urbanization Driving Global Leadership

China leads the global facade coatings market, driven by its Dual-Carbon strategy and large-scale urban development. Regulatory enforcement under updated air pollution laws has accelerated a ~60% shift from solvent-based to waterborne systems in major cities.

Technology integration is a defining feature. AI-driven robotic coating systems are improving application efficiency by ~15%, while nano-TiO₂ photocatalytic coatings are being deployed in airports and megastructures for self-cleaning and NOx reduction. Additionally, BIPV-integrated ETFE coatings are being widely used in net-zero districts, and ceramic microsphere-based coatings are helping reduce urban heat island effects. With over 18,000 facade projects completed in 2025, China continues to dominate in both scale and innovation.

India Facade Coatings Market: Smart Cities and Cooling Technologies Driving Rapid Growth

India is one of the fastest-growing markets, supported by infrastructure expansion and sustainability initiatives. Investments such as Asian Paints’ $235 million waterborne coating facility (2025) are strengthening domestic capacity for facade coatings.

Government programs are major drivers. The Smart Cities Mission mandates self-cleaning and antimicrobial facade coatings for premium public infrastructure, while PMAY housing schemes are accelerating adoption of low-VOC waterborne emulsions. Innovation is focused on climate adaptation, with high-SRI reflective coatings reducing heat load in dense urban areas and elastomeric coatings enabling durability for complex architectural designs. Emerging applications such as AI-powered kinetic facades are also driving demand for advanced, high-durability coating systems.

United States Facade Coatings Market: Infrastructure Renewal and Green Building Standards Driving Demand

The U.S. market is driven by infrastructure modernization and sustainability regulations under the Infrastructure Investment and Jobs Act (IIJA). Updated EPA “Safer Choice” guidelines (2026) have made zero-emission acrylic and epoxy primers the standard for federally funded projects.

Innovation is centered on durability and climate resilience. New moisture-resistant coatings can withstand extreme weather conditions such as 250 km/h wind-driven rain, while low-E facade coatings are being widely deployed to meet LEED and net-zero building standards. The expansion of semiconductor facilities is also driving demand for ESD-safe and low-outgassing facade sealers, particularly in cleanroom-adjacent environments. Industry consolidation—such as the AkzoNobel–Axalta merger—is further strengthening the high-performance coatings segment.

Germany Facade Coatings Market: Circular Economy and Bio-Resin Innovation Driving Sustainability Leadership

Germany is the benchmark for sustainable facade coatings, driven by strict EU regulations and circular economy initiatives. A major breakthrough is the commercialization of bio-based facade resins, developed through collaborations between leading chemical companies.

Demand is fueled by large-scale renovation projects, with a $400 million backlog in energy retrofit applications, increasing use of panelized and over-clad facade coatings. Regulatory mandates now require Digital Product Passports (DPP) for all facade materials, ensuring transparency in recyclability and carbon footprint. Additionally, Germany is leading in biocide-free mineral coatings, which inhibit fungal growth naturally without chemical additives, reinforcing its position in eco-friendly innovation.

Saudi Arabia Facade Coatings Market: Mega-Projects and Extreme Climate Engineering Driving High-Performance Demand

Saudi Arabia is a global testbed for extreme-performance facade coatings, driven by Vision 2030 megaprojects such as NEOM and the Red Sea Project, which account for ~25% of regional demand for high-performance fluoropolymer coatings.

The harsh desert environment is driving innovation in UV-stable silicone-modified elastomeric coatings, capable of maintaining performance for 20+ years under intense heat and sand exposure. Government retrofit programs in Riyadh are also increasing adoption of cool facade technologies, reducing air-conditioning loads by up to 30%. Regulatory enforcement under SABER compliance is phasing out solvent-based coatings, accelerating the transition to low-VOC waterborne systems, while coastal infrastructure projects are driving demand for marine-grade epoxy primers.

South Korea Facade Coatings Market: Smart Facades and 6G Integration Driving Next-Generation Applications

South Korea is pioneering smart facade coatings, integrating advanced materials with digital infrastructure. Government investment of $1.5 billion in 6G R&D (2026) is driving development of terahertz-transparent coatings that enable seamless high-frequency communication through building exteriors.

Innovation is also expanding into energy and electronics. Electrochromic coatings are enabling dynamic glazing systems that adjust transparency based on sunlight, improving energy efficiency. The rise of OLED media facades is increasing demand for anti-reflective and self-cleaning coatings, while photocatalytic coatings are being mandated in public buildings for air purification. Additionally, integration of dielectric and fire-resistant coatings in EV charging infrastructure is further expanding application scope, positioning South Korea at the forefront of next-generation facade technologies.

Facade Coatings Market Report Scope

Facade Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$239.9 Billion

|

|

Market Size (2032)

|

$363.1 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Resin Type (Acrylic, Silicone, Polyurethane, Epoxy, Fluoropolymers, Polyester, Others), By Technology (Water-borne, Solvent-borne, Powder Coatings, High-Solids), By Product Type (Emulsions and Paints, Primers and Sealers, Self-cleaning, Anti-graffiti, Heat-Reflective, Anti-microbial, Nano-coatings), By Substrate (Masonry and Concrete, Metal, Wood and Composite Siding, Glass, Plastics and Fiber Cement), By Application Type (New Construction, Renovation and Refurbishment), By End-Use Sector (Residential, Commercial, Institutional, Industrial), By Functional Performance (Weather and UV Protection, Thermal Insulation, Waterproofing and Damp-proofing, Fire Retardant, Aesthetic)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., Jotun A/S, Sika AG, Sto SE & Co. KGaA, BASF SE, Kansai Paint Co., Ltd., Asian Paints Limited, RPM International Inc., Hempel A/S, DAW SE, Benjamin Moore & Co., SKSHU Paint Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Facade Coatings Market Segmentation

By Resin Type

- Acrylic

- Silicone

- Polyurethane

- Epoxy

- Fluoropolymers

- Polyester

- Others

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- High-Solids

By Product Type

- Emulsions and Paints

- Primers and Sealers

- Self-cleaning

- Anti-graffiti

- Heat-Reflective

- Anti-microbial

- Nano-coatings

By Substrate

- Masonry and Concrete

- Metal

- Wood and Composite Siding

- Glass

- Plastics and Fiber Cement

By Application Type

- New Construction

- Renovation and Refurbishment

By End-Use Sector

- Residential

- Commercial

- Institutional

- Industrial

By Functional Performance

- Weather and UV Protection

- Thermal Insulation

- Waterproofing and Damp-proofing

- Fire Retardant

- Aesthetic

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Facade Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Jotun A/S

- Sika AG

- Sto SE & Co. KGaA

- BASF SE

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- RPM International Inc.

- Hempel A/S

- DAW SE

- Benjamin Moore & Co.

- SKSHU Paint Co., Ltd.

*- List not Exhaustive